Archives

978-0077733773 Chapter 1 Cases Part 1

Chapter 1 – Cost Management and Strategy Chapter 1 Cost Management and Strategy Teaching Notes for Cases 1-1. Critical Success Factors The critical success factors for Kirsten’s business, including the proposed new publishing business are related to the needs of […]

978-0077733773 Chapter 1 Cases Part 2

Chapter 1 – Cost Management and Strategy 1.3 POGS at the Park, POGS at home: C-ing Business Expansion Opportunities This article explains the competitive environment for a minor league baseball team. An innovative manager of the team uses strategic cost […]

978-0077733773 Chapter 1 Lecture Note Part 1

Chapter 01 – Cost Management and Strategy Chapter 1 Cost Management and Strategy Learning Objectives 1. Explain the use of cost management information in each of the four functions of management and in different types of organizations with emphasis on […]

978-0077733773 Chapter 1 Lecture Note Part 2

Chapter 01 – Cost Management and Strategy 1-46 1-35 30 min. X 1-47 1-36 Revised 30 min. X X X 1-37 Deleted . 1-48 1-38 20 min. X 1-49 1-39 20 min. X X X 1-40 Deleted 1-50 1-41 Revised […]

978-0077733773 Chapter 1 Solution Manual Part 1

Chapter 01 – Cost Management and Strategy CHAPTER 1: COST MANAGEMENT AND STRATEGY QUESTIONS 1-1 Firms Using Cost Management. Here are some examples; there are many possible answers. 1. Walmart: to keep costs low by streamlining restocking and sales 2. […]

978-0077733773 Chapter 1 Solution Manual Part 2

Chapter 01 – Cost Management and Strategy 1.24The IMA definition of management accounting states that: a. Management accounting is the process of gathering, reporting, and analyzing information for management decision making b. Management accounting is a profession that involves preparation […]

978-0077733773 Chapter 1 Solution Manual Part 3

Chapter 01 – Cost Management and Strategy 1-38 Risk Management, Enterprise Sustainability, and Lean Accounting (40 min) 1. There are two IMA Statements on Management Accounting (SMA) on Enterprise Risk Management. “Enterprise Risk Management: Frameworks, Elements and Integration” (2006), and […]

978-0077733773 Chapter 1 Solution Manual Part 4

Chapter 01 – Cost Management and Strategy PROBLEMS 1-45 Strategy; Downsizing Luxury (15 min) BMW, Tiffany, Audi and Mercedes-Benz are-well known luxury brands and their products are know to be among the most highly-regarded and expensive in their respective product […]

978-0077733773 Chapter 1 Solution Manual Part 5

Chapter 01 – Cost Management and Strategy 1-52 Strategy: Cost-Cutting in the Pharmaceutical Industry (15 min) Valeant operates in the pharmaceutical industry, an industry that is known for its reliance on innovation, attention to safety, and customer confidence rather than […]

978-0077733773 Chapter 10 Cases Part 1

Chapter 10 – Strategy and the Master Budget Chapter 10 Strategy and the Master Budget Teaching Notes for Cases 10-1: 1Emerson Electric Company Background Emerson is an $8 billion company. Its successful strategy is efficient, quality, and low cost production. […]

978-0077733773 Chapter 10 Cases Part 2

Chapter 10 – Strategy and the Master Budget Sales of motor homes have started to slow in recent months, partly because of high fuel prices. Motor- home retail sales fell about 21% to 7,328 units in the first two months […]

978-0077733773 Chapter 10 Cases Part 3

Chapter 10 – Strategy and the Master Budget Students should identify activity-based costing and management (ABC/M) as an appropriate tool to address many of these issues. They should recognize the need to use benchmarking data for comparison once ABC is […]

978-0077733773 Chapter 10 Cases Part 4

Chapter 10 – Strategy and the Master Budget Exhibit 5 Activity Evaluation Matrix Performance Strategic Non-Strategic Perform Well Cell 1 Continue Cell 2 Drop or Create Niche Perform Poorly Cell 3 Improve Cell 4 Drop 10-31 Education. Copyright © 2016 […]

978-0077733773 Chapter 10 Cases Part 5

Chapter 10 – Strategy and the Master Budget Reading 10-3: “How Challenging Should Profit Budget Targets Be? This article argues for using “highly achievable” budget targets, and explains six key advantages for doing so, including the favorable effect on a […]

978-0077733773 Chapter 10 Cases Part 6

Chapter 10 – Strategy and the Master Budget Reading 10-7: Planning for Uncertainty—Rolling Forecasts Corporate financial planning expert Steve Player highlights how CPA financial executives can use nimble rolling forecasts to replace annual budgets. Discussion Questions 1. According to the […]

978-0077733773 Chapter 10 Lecture Note

Chapter 10 – Strategy and the Master Budget Chapter 10 Strategy and the Master Budget Learning Objectives (LOs) 1. Describe the role of budgets in the overall management process. 2. Discuss the importance of strategy and its role in the […]

978-0077733773 Chapter 10 Solution Manual Part 1

Chapter 10 – Strategy and the Master Budget CHAPTER 10: STRATEGY AND THE MASTER BUDGET QUESTIONS 10-1 Compel strategic planning and facilitate implementation of strategic plans. An organization’s strategy, strategic plans, and budgets are interrelated. Preparing budgets compels reviews of […]

978-0077733773 Chapter 10 Solution Manual Part 10

Chapter 10 – Strategy and the Master Budget 10-56 (Continued-3) 2. What additional real-life refinements would you envision for the budgets you prepared above in (1)? What additional budgets would you anticipate preparing for the company were you in charge […]

978-0077733773 Chapter 10 Solution Manual Part 11

Chapter 10 – Strategy and the Master Budget 10-58 (Continued-4) Cell E8 contains the cost of the new compound, per pound of laundry; cell G99 contains the cost difference: the anticipated fine versus the increased processing cost attributable to the […]

978-0077733773 Chapter 10 Solution Manual Part 2

Chapter 10 – Strategy and the Master Budget 10-26 Budgeted Cash Receipts and Disbursements (30 minutes) 1. Budgeted Cash Receipts: November: Cash sales = $120,000 Collection of accounts receivable: From Oct sales: ($100,000 × 0.95) × 0.40 × 0.75 × […]

978-0077733773 Chapter 10 Solution Manual Part 3

Chapter 10 – Strategy and the Master Budget 10-33 Accounts Receivable Collections and Sensitivity Analysis (50 minutes) Original Assumptions/Data: Actual credit sales for March $130,000 Actual credit sales for April $160,000 Estimated credit sales for May $210,000 Estimated collections in […]

978-0077733773 Chapter 10 Solution Manual Part 4

Chapter 10 – Strategy and the Master Budget 10-37 (Continued) 2. Budgeted Operating Income–Current Year: Sales Revenue (2,500 units × $1,500 per unit) = $3,750,00 0 Less: Variable Costs (2,500 units × $1,000 per unit) = $2,500,00 0 $1,250,00 Less: […]

978-0077733773 Chapter 10 Solution Manual Part 5

Chapter 10 – Strategy and the Master Budget 10-42 Activity-Based Budgeting (ABB) with Continuous Improvement (40 Minutes) 1. Unit-Level: Pick packing, Data entry—Lines Batch-Level: Requisition handling, Data entry—Requisitions, Desktop delivery 2. Budgeted cost for each activity and for the division […]

978-0077733773 Chapter 10 Solution Manual Part 6

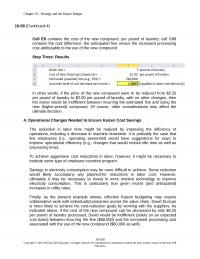

Chapter 10 – Strategy and the Master Budget the upcoming year. This increased evaluation of expenditures would make it 10-47 (Continued) difficult to include budgetary slack in the budget for the upcoming year and likely uncover opportunities of cost savings […]

978-0077733773 Chapter 10 Solution Manual Part 7

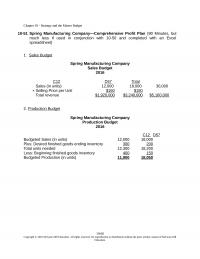

Chapter 10 – Strategy and the Master Budget 10-51 Spring Manufacturing Company—Comprehensive Profit Plan (90 Minutes, but much less if used in conjunction with 10-50 and completed with an Excel spreadsheet) 1. Sales Budget Spring Manufacturing Company Sales Budget 2016 […]

978-0077733773 Chapter 10 Solution Manual Part 8

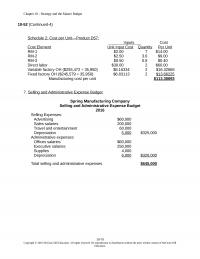

Chapter 10 – Strategy and the Master Budget 10-52 (Continued-4) Schedule 2: Cost per Unit—Product D57: Inputs Cost Cost Element Unit Input Cost Quantity Per Unit RM-1 $2.00 7 $14.00 RM-2 $2.50 3.6 $9.00 RM-3 $0.50 0.8 $0.40 7. Selling […]

978-0077733773 Chapter 10 Solution Manual Part 9

Chapter 10 – Strategy and the Master Budget analysis is a tool that allows us to vary one or more of these inputs in order to examine the resulting effect on one or more budgets (e.g., operating income or cash […]

978-0077733773 Chapter 11 Cases Part 1

Chapter 11 – Decision Making with a Strategic Emphasis Chapter 11 Decision Making with a Strategic Emphasis Teaching Notes for Cases Case 11-1: Product-Promotion Strategies; Use of Probabilities Question 1: Exquisite Foods Incorporated (EFI) wishes to select the most profitable […]

978-0077733773 Chapter 11 Cases Part 2

Chapter 11 – Decision Making with a Strategic Emphasis Purchased Manufactured Manufactured In-line Skates In-line Skates Snowboard Bindings Total Units 6,000 1,000 12,000 Per Unit Total Per Unit Total Per Unit Total Selling price $98 $588,000 $98 $98,000 $60 $720,000 […]

978-0077733773 Chapter 11 Cases Part 3

Chapter 11 – Decision Making with a Strategic Emphasis For the vast majority of consumer products the Mass/Club channel will require the lowest trade margins followed by Grocery stores, and Convenience/Specialty stores. However, in the cola industry on-shelf pricing is […]

978-0077733773 Chapter 11 Cases Part 4

Chapter 11 – Decision Making with a Strategic Emphasis Teaching Notes for Readings 11-28 Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. Chapter 11 – Decision Making with […]

978-0077733773 Chapter 11 Lecture Note

Chapter 11 – Decision Making with a Strategic Emphasis Chapter 11 Decision Making with a Strategic Emphasis Learning Objectives LO 11-1 Define the decision-making process and identify the types of cost information relevant for decision making. LO 11-2 Use relevant […]

978-0077733773 Chapter 11 Solution Manual Part 1

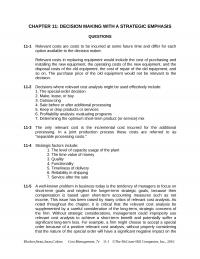

CHAPTER 11: DECISION MAKING WITH A STRATEGIC EMPHASIS QUESTIONS 11-1 Relevant costs are costs to be incurred at some future time and differ for each option available to the decision maker. Relevant costs in replacing equipment would include the cost […]

978-0077733773 Chapter 11 Solution Manual Part 10

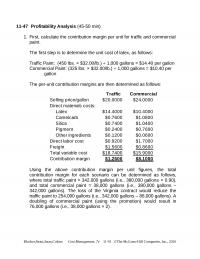

11-47 Profitability Analysis (45-50 min) 1. First, calculate the contribution margin per unit for traffic and commercial paint. The first step is to determine the unit cost of latex, as follows: The per-unit contribution margins are then determined as follows: […]

978-0077733773 Chapter 11 Solution Manual Part 2

11-22 (Continued) 4. Opportunity cost incurred if sales of 5,000 units to regular customers are lost by accepting the special sales order: Lost contribution margin, sales to regular customers: Selling price per unit = $20.00 Variable cost per unit: Direct […]

978-0077733773 Chapter 11 Solution Manual Part 3

11-27 (Continued) Check: 4. The following strategic factors should be considered. What will be the effect on the firm’s image if T-2 is dropped? Will this result in an unfavorable reaction from key customers of T-1 and of other product […]

978-0077733773 Chapter 11 Solution Manual Part 4

11-30 (continued-5) Note that the products have the same per unit profit, but Flash has the higher contribution margin per unit, and Clash has the higher contribution per direct labor hour (DLH). Thus, Flash would be the more profitable product […]

978-0077733773 Chapter 11 Solution Manual Part 5

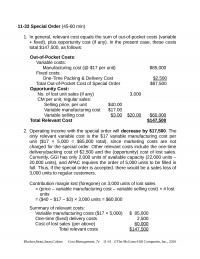

11-33 Special Order (45-60 min) 1. In general, relevant cost equals the sum of out-of-pocket costs (variable + fixed), plus opportunity cost (if any). In the present case, these costs total $147,500, as follows: Out-of-Pocket Costs: Variable costs: Manufacturing cost […]

978-0077733773 Chapter 11 Solution Manual Part 6

11-36 Make or Buy (45-60 min) 1. Since the per-unit contribution margin for manufactured fans ($24) is higher than for purchased fans ($12), the company should manufacture as many fans as possible (15,000), and purchase the remainder (5,000) from Harris […]

978-0077733773 Chapter 11 Solution Manual Part 7

11-39 (continued-2) and long-term pricing strategy to make sure it is consistent with long-term strategy with established profit targets. Hillside should evaluate the effectiveness of its advertising and promotional efforts. Are the targeted customers being reached? Since the products have […]

978-0077733773 Chapter 11 Solution Manual Part 8

11-46 (Continued-1) $4.000 $27,435 $27,389 $4.250 $28,087 $27,944 $4.500 $28,739 $28,500 Based on the above analysis and graph, we see that for these two alternatives (gas-powered vs. hybrid model), and 60,000 miles total usage over a four-year period, the lifetime […]

978-0077733773 Chapter 11 Solution Manual Part 9

11-44 (continued-1) 2. The net first-year cost savings from closing the plant are estimated as $7,200 (in thousands), as follows: The depreciation amounts are not relevant to the decision because they represent portions of sunk costs that are being Corporate […]

978-0077733773 Chapter 12 Cases Part 1

Chapter 12 – Strategy and the Analysis of Capital Investments Chapter 12 Strategy and the Analysis of Capital Investments Teaching Notes for Cases 12-1: Floating Investments (Source: Paul Rouse and Leigh Houghton, “Instructional Case: Floating Investments,” Journal of Accounting Education, […]

978-0077733773 Chapter 12 Cases Part 2

Chapter 12 – Strategy and the Analysis of Capital Investments 2. Perform a detailed financial analysis of the Park Hill Acres superstore option assuming the Webster Street store remains open. In your analysis include your judgments and rationale for dealing […]

978-0077733773 Chapter 12 Cases Part 3

Chapter 12 – Strategy and the Analysis of Capital Investments 12-21 Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. Chapter 12 – Strategy and the Analysis of Capital […]

978-0077733773 Chapter 12 Cases Part 4

Chapter 12 – Strategy and the Analysis of Capital Investments Reading 12-2: How ABC Was Used in Capital Budgeting This article presents a case study on the difference that ABC makes on the investment decision of a new project. A […]

978-0077733773 Chapter 12 Cases Part 5

Chapter 12 – Strategy and the Analysis of Capital Investments asset, additional net working capital required) 5. Financing (cost of equity capital; income tax rate, t) 6. Operating costs (both variable (supplies) and fixed (personnel, utilities, insurance, etc.) In this […]

978-0077733773 Chapter 12 Lecture Note Part 1

Chapter 12 – Strategy and the Analysis of Capital Investments Chapter 12 Strategy and the Analysis of Capital Investments Learning Objectives LO 12-1Explain the strategic role of capital-investment analysis LO 12-2Describe how accountants can add value to the capital-budgeting process […]

978-0077733773 Chapter 12 Lecture Note Part 2

Chapter 12 – Strategy and the Analysis of Capital Investments Effects of cash flows include direct and indirect (tax) effects. Direct effects include cash receipts, cash payments, or cash commitments. Indirect or tax effects are changes in income-tax payments precipitated […]

978-0077733773 Chapter 12 Solution Manual Part 1

Chapter 12 – Strategy and the Analysis of Capital Investments CHAPTER 12: STRATEGY AND THE ANALYSIS OF CAPITAL INVESTMENTS QUESTIONS 12-1 Capital-budgeting decisions: (a) are long-term in nature (i.e., they affect profitability and cash flows for many years into the […]

978-0077733773 Chapter 12 Solution Manual Part 10

Chapter 12 – Strategy and the Analysis of Capital Investments 12-56 Sensitivity Analysis; Equipment-Replacement Decision (45-60 minutes) 1. The maximum amount of annual variable operating expenses, pre-tax, that would make this an attractive investment from a present-value standpoint = $99,206 […]

978-0077733773 Chapter 12 Solution Manual Part 11

Chapter 12 – Strategy and the Analysis of Capital Investments SUM = $ 159,900 $ 115,833 12-58 (Continued-2) Alternatively: a) For 8%: ($14,545 × 10.935) + (0.116 × $7,273) = $159,900 b) For 12%: ($14,545 × 7.943) + (0.042 × […]

978-0077733773 Chapter 12 Solution Manual Part 12

Chapter 12 – Strategy and the Analysis of Capital Investments 12-61 Research Assignment, Strategy (45 Minutes) This assignment pertains to the following article: Thomas L. Barton and John B. MacArthur, “The New Hue of Green for the Management Accountant,” Strategic […]

978-0077733773 Chapter 12 Solution Manual Part 2

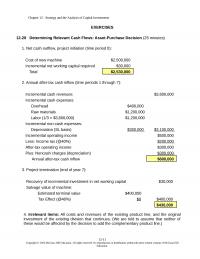

Chapter 12 – Strategy and the Analysis of Capital Investments EXERCISES 12-28 Determining Relevant Cash Flows: Asset-Purchase Decision (25 minutes) 1. Net cash outflow, project initiation (time period 0): Cost of new machine $2,500,000 2. Annual after-tax cash inflow (time […]

978-0077733773 Chapter 12 Solution Manual Part 3

Chapter 12 – Strategy and the Analysis of Capital Investments 12-34 Determining Cash Flows; Basic Capital Budgeting (15 minutes) 1. The after-tax cash flow from disposal of the old machinery = after-tax gain on sale = ($1,800 – $0) × […]

978-0077733773 Chapter 12 Solution Manual Part 4

Chapter 12 – Strategy and the Analysis of Capital Investments 12-39 (Continued) Step 2: Complete the following “Goal Seek” dialog box: Step 3: Results 4. Many firms raise the discount rate in evaluating a particular capital investment in view of […]

978-0077733773 Chapter 12 Solution Manual Part 5

Chapter 12 – Strategy and the Analysis of Capital Investments 12-44 (Continued-1) PV factor Year CF PV CF Net investment outlay 1.000 0 ($480,000) ($480,000 ) After-tax cash inflow 0.909 1 $208,000 $189,072 After-tax cash inflow 0.826 2 $208,000 $171,808 […]

978-0077733773 Chapter 12 Solution Manual Part 6

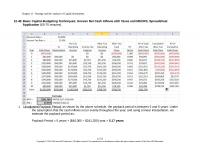

Chapter 12 – Strategy and the Analysis of Capital Investments 12-48 Basic Capital-Budgeting Techniques; Uneven Net Cash Inflows with Taxes and MACRS; Spreadsheet Application (60-75 minutes) 1. Unadjusted Payback Period: as shown by the above schedule, the payback period is […]

978-0077733773 Chapter 12 Solution Manual Part 7

Chapter 12 – Strategy and the Analysis of Capital Investments 12-49 (Continued-4) 5. Modified internal rate of return (MIRR): A summary table for Problem12-49 appears below. 12-63 Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without […]

978-0077733773 Chapter 12 Solution Manual Part 8

Chapter 12 – Strategy and the Analysis of Capital Investments 12-73 Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. Chapter 12 – Strategy and the Analysis of Capital […]

978-0077733773 Chapter 12 Solution Manual Part 9

Chapter 12 – Strategy and the Analysis of Capital Investments 12-54 (Continued–1) 2. The following spreadsheet excerpt contains the PV of each alternative: Sample Calculation: Cell D111 = after-tax cash operating cost ($48,000 = (8,000 machine hours × $10/machine hour) […]

978-0077733773 Chapter 13 Cases Part 1

Chapter 13 – Cost Planning for the Product Life Cycle: Target Costing, Theory of Constraints, and Strategic Pricing Chapter 13 Cost Planning for the Product Life Cycle: Target Costing, Theory of Constraints, and Strategic Pricing Teaching Notes for Cases 13-1. […]

978-0077733773 Chapter 13 Cases Part 2

Chapter 13 – Cost Planning for the Product Life Cycle: Target Costing, Theory of Constraints, and Strategic Pricing Let’s discuss the elements of the target costing model and how these elements are developed. At this point in the discussion I […]

978-0077733773 Chapter 13 Lecture Note

Chapter 13 – Cost Planning for the Product Life Cycle: Target Costing, Theory of Constraints, and Strategic Pricing Chapter 13 Cost Planning for the Product Life Cycle: Target Costing, Theory of Constraints, and Strategic Pricing Learning Objectives 1. Explain how […]

978-0077733773 Chapter 13 Solution Manual Part 1

Chapter 13 – Cost Planning for the Product Life Cycle: Target Costing, Theory of Constraints, and Strategic Pricing CHAPTER 13: Cost Planning for the Product Life Cycle: Target Costing, Theory of Constraints, and Strategic Pricing QUESTIONS 13-1 Target costing is […]

978-0077733773 Chapter 13 Solution Manual Part 2

Chapter 13 – Cost Planning for the Product Life Cycle: Target Costing, Theory of Constraints, and Strategic Pricing 3. The airfare costs are the largest component of cost and this category could have room for improvement. By further negotiating group […]

978-0077733773 Chapter 13 Solution Manual Part 3

Chapter 13 – Cost Planning for the Product Life Cycle: Target Costing, Theory of Constraints, and Strategic Pricing 13-39 (continued -1) b. Morrow appears to compete in what Robin Cooper calls the “confrontation” strategy (When Lean Enterprises Collide, Harvard Business […]

978-0077733773 Chapter 13 Solution Manual Part 4

Chapter 13 – Cost Planning for the Product Life Cycle: Target Costing, Theory of Constraints, and Strategic Pricing 13-45 (continued) at times (as for tables in this case) can be sold from inventory. 13-46 Theory of Constraints (30 min) With […]

978-0077733773 Chapter 13 Solution Manual Part 5

Chapter 13 – Cost Planning for the Product Life Cycle: Target Costing, Theory of Constraints, and Strategic Pricing 13-48 Life-Cycle Costing; Ethics (25 min) 1. Kate Stephen’s analysis based on the prepared report fails to consider the very significant amount […]

978-0077733773 Chapter 14 Cases Part 1

Chapter 14 – Operational Performance Measurement: Sales, Direct Cost Variances, and the Role of Nonfinancial Performance Measures Chapter 14 Operational Performance Measurement: Sales, Direct Cost Variances, and the Role of Nonfinancial Performance Measures Teaching Notes for Case Case 14-1: Pet […]

978-0077733773 Chapter 14 Cases Part 2

Chapter 14 – Operational Performance Measurement: Sales, Direct Cost Variances, and the Role of Nonfinancial Performance Measures Reading 14-5: Larry Grasso, “Are ABC and RCA Accounting Systems Compatible with Lean Management?,” Management Accounting Quarterly, Vol. 7, No. 1 (Fall 2005), […]

978-0077733773 Chapter 14 Lecture Note

Chapter 14 – Operational Performance Measurement: Sales, Direct Cost Variances, and the Role of Nonfinancial Performance Indicators Chapter 14 Operational Performance Measurement: Sales, Direct Cost Variances, and the Role of Nonfinancial Performance Indicators Learning Objectives LO 14-1 Explain the essence […]

978-0077733773 Chapter 14 Solution Manual Part 1

Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and the Role of Nonfinancial Performance Measures CHAPTER 14: OPERATIONAL PERFORMANCE MEASUREMENT: SALES, DIRECT– COST VARIANCES, AND THE ROLE OF NONFINANCIAL PERFORMANCE MEASURES QUESTIONS 14-1 A master budget represents forecasted operating […]

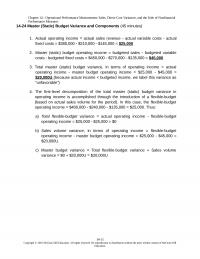

978-0077733773 Chapter 14 Solution Manual Part 2

Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and the Role of Nonfinancial Performance Measures 14-24 Master (Static) Budget Variance and Components (45 minutes) 1. Actual operating income = actual sales revenue actual variable costs actual 2. […]

978-0077733773 Chapter 14 Solution Manual Part 3

Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and the Role of Nonfinancial Performance Measures 14-30 Flexible Budget and Operating-Income Variances (40 minutes) 1. Budget data: a. Flexible budget for 20,000 units Sales 20,000 × $4.50 = $90,000 Variable […]

978-0077733773 Chapter 14 Solution Manual Part 4

Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and the Role of Nonfinancial Performance Measures 14-37 Standard Costing and Journal Entries (40 minutes) 1. Materials Inventory (6,000 gals. × $10.00/gal.) 60,000 Materials Purchase-Price Variance 2,700 2. WIP Inventory (2,500 […]

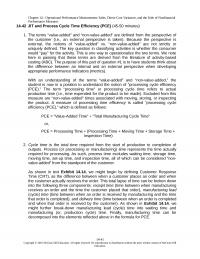

978-0077733773 Chapter 14 Solution Manual Part 5

Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and the Role of Nonfinancial Performance Measures 14-42 JIT and Process Cycle Time Efficiency (PCE) (45-50 minutes) 1. The terms “value-added” and “non-value-added” are defined from the perspective of the customer […]

978-0077733773 Chapter 14 Solution Manual Part 6

Q P SP AP SQ AQ [(AP − SP) × (AQ − SQ)] SQ × (AP – SP) SP × (AQ SQ) Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and The Role of Nonfinancial Performance Measures 14-45 (continued) […]

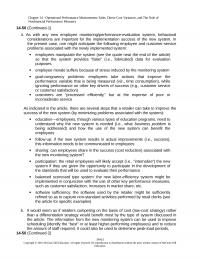

978-0077733773 Chapter 14 Solution Manual Part 7

Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and The Role of Nonfinancial Performance Measures 14-50 (Continued-1) 4. As with any new employee monitoring/performance-evaluation system, behavioral considerations are important for the implementation success of the new system. In the […]

978-0077733773 Chapter 14 Solution Manual Part 8

Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and The Role of Nonfinancial Performance Measures 14-51 (Continued-2) the quality of information produced by the organization’s comprehensive management accounting and control system. One desirable quality is that such information be […]

978-0077733773 Chapter 15 Cases Part 1

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management Chapter 15 Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management Teaching Notes for Readings Reading 15-1: Kennard T. Wing, “Using Enhanced Cost Models in Variance Analysis for Better Control […]

978-0077733773 Chapter 15 Cases Part 2

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management departments). The cost model used in the pilot implementation is depicted in Figure 1 of the article. Idle capacity costs (6% of total) were excluded from the cost base. […]

978-0077733773 Chapter 15 Lecture Note

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management Chapter 15 Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management Learning Objectives 1. Distinguish between the product-costing and control purposes of standard costs for manufacturing overhead 2. Use flexible […]

978-0077733773 Chapter 15 Solution Manual Part 1

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management CHAPTER 15: OPERATIONAL PERFORMANCE MEASUREMENT: INDIRECT-COST VARIANCES AND RESOURCE-CAPACITY MANAGEMENT QUESTIONS 15-1 The total factory overhead can be the same as the standard amount allowed for the current period’s […]

978-0077733773 Chapter 15 Solution Manual Part 2

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management 15-24 (Continued-1) 15-11 Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. Chapter 15 – Operational Performance Measurement: […]

978-0077733773 Chapter 15 Solution Manual Part 3

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management 15-31 Three-Variance Factory Overhead Analysis (40 minutes) 1. Standard variable factory overhead rate per direct labor hour (DLH): = Budgeted Total Variable Factory Overhead ÷ Budgeted Total Direct Labor […]

978-0077733773 Chapter 15 Solution Manual Part 4

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management Note: An Excel spreadsheet solution file for this assignment is embedded below. You can open this “object” by doing the following: 1. Right click anywhere in the worksheet area […]

978-0077733773 Chapter 15 Solution Manual Part 5

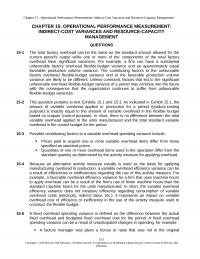

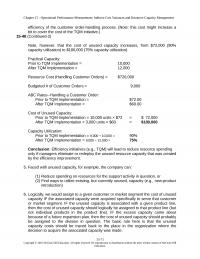

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management 15-38 (Continued-1) 3. If the fixed factory overhead rate was based on practical capacity rather than theoretical (maximum) capacity, Yuba Machine Company’s reported operating income at May 31, 2017 […]

978-0077733773 Chapter 15 Solution Manual Part 6

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management 15-41 (Continued-1) does say, however, that when practical capacity is used to set fixed overhead rates, then allocated cost (to outputs) equals the ratio of actual output to practical […]

978-0077733773 Chapter 15 Solution Manual Part 7

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management 15-45 Four-Variance Analysis; Journal Entries (60-75 Minutes) 1. Standard Factory Overhead Rates Variable factory OH $3,600,000 600,000 DLHs = $ 6.00per DLH Fixed factory OH $3,000,000 600,000 […]

978-0077733773 Chapter 15 Solution Manual Part 8

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management efficiency of the customer order-handling process. (Note: this cost might increase a bit to cover the cost of the TQM initiative.) 15-48 (Continued-2) Note, however, that the cost of […]

978-0077733773 Chapter 15 Solution Manual Part 9

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management 15-51 Decision-Making under Uncertainty (Appendix) (30-40 minutes) 1. Payoff Table Possible Courses of State of the Market Expected Value of Each Action Strong Weak Prob. = 0.3 Prob. = […]

978-0077733773 Chapter 16 Cases

Chapter 16 – Operational Performance Measurement: Further Analysis of Productivity and Sales Chapter 16 Operational Performance Measurement: Further Analysis of Productivity and Sales Teaching Notes for Cases Case 16-1 Dallas Consulting Group* This case serves as a review of sales […]

978-0077733773 Chapter 16 Lecture Note Part 1

Chapter 16 – Operational Performance Measurement: Further Analysis of Productivity and Sales Chapter 16 Operational Performance Measurement: Further Analysis of Productivity and Sales Learning Objectives 1. Explain the strategic role of the flexible budget in analyzing productivity and sales. 2. […]

978-0077733773 Chapter 16 Lecture Note Part 2

Chapter 16 – Operational Performance Measurement: Further Analysis of Productivity and Sales 3. Obtain Information and Conduct Analyses of the Alternatives Schmidt calculates the sales quantity, market share and market size variances. Schmidt also conducts further economic analysis which shows […]

978-0077733773 Chapter 16 Solution Manual Part 1

Chapter 16 – Operational Performance Measurement: Further Analysis of Productivity and Sales CHAPTER 16: OPERATIONAL PERFORMANCE MEASUREMENT: FURTHER ANALYSIS OF PRODUCTIVITY AND SALES QUESTIONS 16-1 Productivity is the ratio of output to input. It is a measure of the amount […]

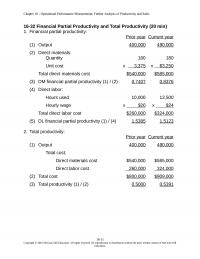

978-0077733773 Chapter 16 Solution Manual Part 2

Chapter 16 – Operational Performance Measurement: Further Analysis of Productivity and Sales 16-32 Financial Partial Productivity and Total Productivity (20 min) 1. Financial partial productivity: Prior year Current year (1) Output 400,000 490,000 (2) Direct materials: Quantity 160 180 (3) […]

978-0077733773 Chapter 16 Solution Manual Part 3

Chapter 16 – Operational Performance Measurement: Further Analysis of Productivity and Sales 16- 40 Sales Variances; Quarter to Quarter (20 min) 1. Contribution Income Statement for Hathaway 16-21 Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution […]

978-0077733773 Chapter 16 Solution Manual Part 4

Chapter 16 – Operational Performance Measurement: Further Analysis of Productivity and Sales 16-45 Partial Operational and Financial Productivity; Total Productivity (30 min) 1. Operational Partial Productivity MF LI Difference * The direction of variances denotes the advantage of LI over […]

978-0077733773 Chapter 16 Solution Manual Part 5

Chapter 16 – Operational Performance Measurement: Further Analysis of Productivity and Sales 16-49 (continued -1) 3. MEMO TO: Rajat Patel, Integrated Medical Care FROM: Joseph Marin, Marin & Associates I have calculated the financial partial productivity measure for IMC for […]

978-0077733773 Chapter 16 Solution Manual Part 6

Chapter 16 – Operational Performance Measurement: Further Analysis of Productivity and Sales 16-54 Market Size and Market Share Variances (15 min) WS= Welcome Signs; BH= Birdhouses 1. Budget Actual (per month)____ Diane’s Designs Industry Share Diane’s Designs Industry Share 2. […]

978-0077733773 Chapter 16 Solution Manual Part 7

Chapter 16 – Operational Performance Measurement: Further Analysis of Productivity and Sales 16-57 Comparative Income Statements and Sales Performance Variances; Current to Prior Year (25 min) 1. 16-58 Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution […]

978-0077733773 Chapter 17 Cases Part 1

Chapter 17 – The Management & Control of Quality Chapter 17 The Management & Control of Quality Teaching Notes for Cases Case 17-1: Precision Systems, Inc. This case illustrates that quality cost information can play an important role in alerting […]

978-0077733773 Chapter 17 Cases Part 2

Chapter 17 – The Management & Control of Quality intubation treatment. As for contract physicians, hospitals must compete for their patronage by providing them quality in services they consider important. Also, the contract physicians usually are the ones who choose […]

978-0077733773 Chapter 17 Cases Part 3

Chapter 17 – The Management & Control of Quality Teaching Notes for Readings Reading 17-1: “GE Takes Six Sigma Beyond the Bottom Line” by G. T. Lucier and S. Seshadri, Strategic Finance (May 2001), pp. 40-46. This article reports the […]

978-0077733773 Chapter 17 Cases Part 4

Chapter 17 – The Management & Control of Quality Reading 17-7: Brian H. Maskell and Frances A. Kennedy, “Why Do We Need Lean Accounting and How Does It Work?” The Journal of Corporate Accounting and Finance (March/April 2007), pp. 59-73. […]

978-0077733773 Chapter 17 Cases Part 5

Chapter 17 – The Management & Control of Quality Reading 17-10: Keith T. Jones and Clement C. Chen, “The Pervasive Success of 6 Sigma at Caterpillar: Accounting and Finance Efforts Are a Good Example,” by Strategic Finance (April 2010), pp. […]

978-0077733773 Chapter 17 Lecture Note

Chapter 17 – The Management and Control of Quality Chapter 17 The Management and Control of Quality Learning Objectives 1. Discuss the strategic importance of quality 2. Define accounting’s role in the management and control of quality 3. Develop a […]

978-0077733773 Chapter 17 Solution Manual Part 1

Chapter 17 – The Management and Control of Quality CHAPTER 17: THE MANAGEMENT AND CONTROL OF QUALITY QUESTIONS 17-1 As shown in Exhibit 17.1, investments in quality can lead to improved business processes, which in turn result in improved quality […]

978-0077733773 Chapter 17 Solution Manual Part 2

Chapter 17 – The Management and Control of Quality 17-37 (Continued) The request by Sanchez is unethical because it would suppress information that could influence an understanding of the results of operations by the company. Also, by withholding information about […]

978-0077733773 Chapter 17 Solution Manual Part 3

Chapter 17 – The Management and Control of Quality 17-42 (Continued) X Probability, f(x) x*f(x) (x – 0.199991) 2 f(x) 0.1996 0.02 0.003992 0.00000000305762 0.1997 0.05 0.009985 0.00000000423405 0.1998 0.12 0.023976 0.00000000437772 0.1999 0.11 0.021989 0.00000000091091 0.2000 0.45 0.090000 0.00000000003645 […]

978-0077733773 Chapter 17 Solution Manual Part 4

Chapter 17 – The Management and Control of Quality 17-48 (Continued) 3. There are likely opposing points of view. Companies that are included in portfolios of high performance in the environmental (or social) area are certainly likely to favor such […]

978-0077733773 Chapter 17 Solution Manual Part 5

Chapter 17 – The Management and Control of Quality 17-55 (Continued-2) Note: The following chart is no longer available on the FirstEnergy website, but is viewed as instructive nonetheless. Radioactive Waste Produced: Projected (2007) vs. Actual (First Three Quarters 2007) […]

978-0077733773 Chapter 17 Solution Manual Part 6

Chapter 17 – The Management and Control of Quality 17-62 (Continued-1) Education—employees as well as managers need to be educated regarding the reasons for change (i.e., the business purpose for the change); as well, these the “lean enterprise,” employee compensation […]

978-0077733773 Chapter 17 Solution Manual Part 7

Chapter 17 – The Management and Control of Quality 17-66 (Continued-2) Since JIT involves smooth and efficient flows throughout the entire value chain, have suppliers and customers been consulted and included in any planning 17-62 Copyright © 2016 McGraw-Hill Education. […]

978-0077733773 Chapter 17 Solution Manual Part 8

Chapter 17 – The Management and Control of Quality 17-71 (Continued-1) 5. Data for Trend Analysis (2016 and 2017 Category Results) 6. Bar Chart: COQ Report, 2016 and 2017 12345 0.00% 5.00% 10.00% 15.00% 20.00% 25.00% Duncan Materials: COQ Trend […]

978-0077733773 Chapter 17 Solution Manual Part 9

Chapter 17 – The Management and Control of Quality 17-74 (Continued-2) 3. The report indicates that prevention, appraisal, and internal failure costs have increased from 2016 to 2017. The external failure cost category decreased by 2017. Lee Enterprises benefits from […]

978-0077733773 Chapter 18 Cases Part 1

Chapter 18 – Management Control and Strategic Performance Measurement Chapter 18 Management Control and Strategic Performance Measurement Teaching Notes for Cases 18-1 Industrial Chemical Company; Decentralization; Cost SBUs; International Background To begin class discussion you may wish to point out […]

978-0077733773 Chapter 18 Cases Part 2

Chapter 18 – Management Control and Strategic Performance Measurement Suggested Answer: The balanced scorecard was originally designed as a performance diagnostic system that supplements financial numbers with nonfinancial indicators expected to be drivers of Advantages of the BSC include: The […]

978-0077733773 Chapter 18 Lecture Note Part 1

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard Chapter 18 Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard Learning Objectives 1. Identify the objectives of management control. 2. Identify the types […]

978-0077733773 Chapter 18 Lecture Note Part 2

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard Exhibit 2: Risk Neutral and Risk Averse Utility Functions Using mathematical transforms such as the square root or the logarithm of the dollars of expected return […]

978-0077733773 Chapter 18 Solution Manual Part 1

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard CHAPTER 18: STRATEGIC PERFORMANCE MEASUREMENT: COST CENTERS, PROFIT CENTERS, AND THE BALANCED SCORECARD QUESTIONS 18-1 Performance evaluation can be thought of as the process by which […]

978-0077733773 Chapter 18 Solution Manual Part 10

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard 18-64 Research Assignment; Sustainability (45 min) The project upon which the article is based is a research project funded by the Institute of Management Accountants (IMA). […]

978-0077733773 Chapter 18 Solution Manual Part 2

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard 18-27 Research and Development: Risk Aversion and Performance Measurement (20 min) 1. Risk aversion, the tendency to avoid actions with uncertain outcomes (even with good probability […]

978-0077733773 Chapter 18 Solution Manual Part 3

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard 18-34 Outsourcing; Choice of Strategic Business Unit (15min) 1. P&G probably used a cost center to manage the print services unit, which would be a common […]

978-0077733773 Chapter 18 Solution Manual Part 4

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard 18-40 Financial Incentives and Auto Repair/Inspection Companies (20 min) The findings of the research suggest that in fact the financial incentives of the auto repair shop […]

978-0077733773 Chapter 18 Solution Manual Part 5

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard 18-45 (continued -1) PART THREE Reconciling Difference in Operating Income between Full and Variable Costing 2015 2016 Change in Inventory in Units 1,000 (1,000) Multiply times […]

978-0077733773 Chapter 18 Solution Manual Part 6

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard 18-50 (continued -1) Other GAAP issues include differences between profit centers in: a) Judgments of the allowance for bad debts g) The effect of judgment in […]

978-0077733773 Chapter 18 Solution Manual Part 7

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard 18-53 (continued -2) Variable Costs Variable Variable Total Units Mfg Selling Variable Sold Cost/unit Cost/Unit Cost (1) (2) (3) (1)x[(2)+(3)] United States Pharmaceutical 64,000 $4.00 $2.00 […]

978-0077733773 Chapter 18 Solution Manual Part 8

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard 18-56 (continued -1) There are at least two possible approaches: 1. develop a charge-back system for printing and duplicating, so that each of the users of […]

978-0077733773 Chapter 18 Solution Manual Part 9

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard 18-62 Contribution Income Statement for Profit Centers (40 min) 1. Data Summary: 18-81 Education. Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution […]

978-0077733773 Chapter 19 Cases Part 1

Chapter 19 – Strategic Performance Measurement: Investment Centers Chapter 19 Strategic Performance Measurement: Investment Centers Teaching Notes for Cases Case 19-1: Investment Centers 1. The prior performance measurement system was called “performance income,” and is best described as a profit […]

978-0077733773 Chapter 19 Cases Part 2

Chapter 19 – Strategic Performance Measurement: Investment Centers 19-11 Education. Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Chapter 19 – Strategic Performance Measurement: Investment Centers 19-12 Copyright © […]

978-0077733773 Chapter 19 Cases Part 3

Chapter 19 – Strategic Performance Measurement: Investment Centers ROI for the entire firm (absent any efficiency gains) was left unchanged by the transfers, 11.76% (see Table 6). The practice continued in year two (see Table 4): two segments were transferred […]

978-0077733773 Chapter 19 Cases Part 4

Chapter 19 – Strategic Performance Measurement: Investment Centers correct incentive, from the standpoint of the organization as a whole: subunit 2 will reject the special (supplemental) offer of $240 per unit from an external buyer. As such, subunit 1 would […]

978-0077733773 Chapter 19 Lecture Note Part 1

Chapter 19 – Strategic Performance Measurement: Investment Centers & Transfer Pricing Chapter 19 Strategic Performance Measurement: Investment Centers & Transfer Pricing Learning Objectives LO 19-1 Explain the use and limitations of return on investment (ROI) for evaluating investment centers. LO […]

978-0077733773 Chapter 19 Lecture Note Part 2

Chapter 19 – Strategic Performance Measurement: Investment Centers & Transfer Pricing 6. Measuring the Level of “Investment”: Allocating Shared Assets. As in joint cost allocation, top management should trace the assets to the business units that used them and allocate […]

978-0077733773 Chapter 19 Solution Manual Part 1

Chapter 19 – Strategic Performance Measurement—Investment Centers CHAPTER 19: STRATEGIC PERFORMANCE MEASUREMENT— INVESTMENT CENTERS QUESTIONS 19-1 Investment centers are commonly used when there are a number of business units to be compared, and/or when top management intends to evaluate the […]

978-0077733773 Chapter 19 Solution Manual Part 10

Chapter 19 – Strategic Performance Measurement—Investment Centers 4. Laws limiting the kind of tax-planning opportunities alluded to above in (3) differ across countries. The laws in some countries prohibit such practice altogether, while other countries provide at least some possibility […]

978-0077733773 Chapter 19 Solution Manual Part 11

Chapter 19 – Strategic Performance Measurement—Investment Centers Total Cost per Unit = $1,000 $1,200 $1,900 5. First and foremost, the transfer pricing method chosen must be legally acceptable in each of the countries involved. Second, the impact of the transfer […]

978-0077733773 Chapter 19 Solution Manual Part 2

Chapter 19 – Strategic Performance Measurement—Investment Centers 19-24 Target Sales Price; Return on Investment (ROI) (20 minutes) 1. ROI = Operating Income ÷ Investment (avg. total assets) Let X = target Operating Income: Target (required) total revenue = $900,000, calculated […]

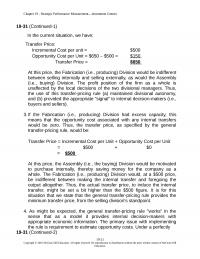

978-0077733773 Chapter 19 Solution Manual Part 3

Chapter 19 – Strategic Performance Measurement—Investment Centers 19-31 (Continued-1) In the current situation, we have: Transfer Price: Incremental Cost per unit = $500 the use of this transfer-pricing rule (a) maintained divisional autonomy, and (b) provided the appropriate “signal” to […]

978-0077733773 Chapter 19 Solution Manual Part 4

Chapter 19 – Strategic Performance Measurement—Investment Centers 19-36 (Continued-1) Further, such differences likely have incentive effects. For example, if the division in question currently generates an ROI greater than, say, 15% (or even 11%), it is not clear that the […]

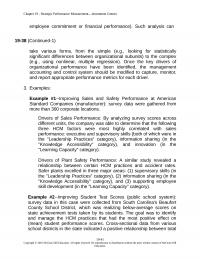

978-0077733773 Chapter 19 Solution Manual Part 5

Chapter 19 – Strategic Performance Measurement—Investment Centers employee commitment or financial performance). Such analysis can 19-38 (Continued-1) take various forms, from the simple (e.g., looking for statistically significant differences between organizational subunits) to the complex (e.g., using nonlinear, multiple regression). […]

978-0077733773 Chapter 19 Solution Manual Part 6

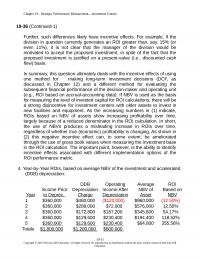

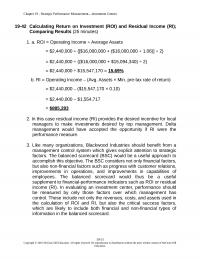

Chapter 19 – Strategic Performance Measurement—Investment Centers 19-42 Calculating Return on Investment (ROI) and Residual Income (RI); Comparing Results (25 minutes) 1. a. ROI = Operating Income ÷ Average Assets = $2,440,000 ÷ {[$16,000,000 + ($16,000,000 ÷ 1.06)] ÷ 2} […]

978-0077733773 Chapter 19 Solution Manual Part 7

Chapter 19 – Strategic Performance Measurement—Investment Centers 19-45 EVA® NOPAT and EVA® Capital; Financing Approach (60 Minutes) 1. Students should understand that EVA® is an approximation of an entity’s true (i.e., “economic”) profits for a period. This measure of profitability […]

978-0077733773 Chapter 19 Solution Manual Part 8

Chapter 19 – Strategic Performance Measurement—Investment Centers 19-47 General Transfer-Pricing Rule; Goal Congruence (30-40 Minutes) 1. Using the general guideline presented in the chapter, the minimum price at which the Transmission Division (i.e., the producer) would sell standard transmissions to […]

978-0077733773 Chapter 19 Solution Manual Part 9

Chapter 19 – Strategic Performance Measurement—Investment Centers 19-49 (continued) If Partial Sales to Division A are OK: Division B should sell as many units as possible (in this case 50,000 of total demand) to outside consumers. The remaining capacity (20%, […]

978-0077733773 Chapter 2 Cases Part 1

Chapter 2 – Implementing Strategy: The Value Chain, the Balanced Scorecard, and the Strategy Map Chapter 2 Implementing Strategy: The Value Chain, the Balanced Scorecard, and the Strategy Map Teaching Notes for Cases 2-1. Atlantic City Casino: Value Chain Analysis; […]

978-0077733773 Chapter 2 Cases Part 2

Chapter 2 – Implementing Strategy: The Value Chain, the Balanced Scorecard, and the Strategy Map 2-2 “Applying the Balanced Scorecard to Small Companies” (Note: This article is referred to in the text of chapter 2) The use of the balanced […]

978-0077733773 Chapter 2 Lecture Note

Chapter 02 – Implementing Strategy: The Value Chain, the Balanced Scorecard, and the Strategy Map Chapter 2 Implementing Strategy: The Value Chain, the Balanced Scorecard, and the Strategy Map Learning Objectives 1. Explain how to implement a competitive strategy by […]

978-0077733773 Chapter 2 Solution Manual Part 1

Chapter 02 – Implementing Strategy: The Value Chain, the Balanced Scorecard, and the Strategy Map CHAPTER 2: IMPLEMENTING STRATEGY: THE VALUE CHAIN, THE BALANCED SCORECARD, AND THE STRATEGY MAP QUESTIONS 2-1 The two types of competitive strategy (per Michael Porter, […]

978-0077733773 Chapter 2 Solution Manual Part 2

Chapter 02 – Implementing Strategy: The Value Chain, the Balanced Scorecard, and the Strategy Map 2-35 Which of the following statements about the value-chain is correct? a. The two phases of the activities of the value-chain are the upstream activities […]

978-0077733773 Chapter 2 Solution Manual Part 3

Chapter 02 – Implementing Strategy: The Value Chain, the Balanced Scorecard, and the Strategy Map Financial: operating margin, cost per patient-day, percentage of overdue patient accounts, sales growth Customer: patient satisfaction, speed of service, number of referring physicians, measures of […]

978-0077733773 Chapter 2 Solution Manual Part 4

Chapter 02 – Implementing Strategy: The Value Chain, the Balanced Scorecard, and the Strategy Map 2-54 The Balanced Scorecard (20 min) An example of a balanced scorecard for Tartan Corp follows: Financial Sales, sales growth, by product and region Earnings, […]

978-0077733773 Chapter 2 Solution Manual Part 5

Chapter 02 – Implementing Strategy: The Value Chain, the Balanced Scorecard, and the Strategy Map 2-59 Strategy Requirements Under the Baldrige National Quality Award Program (30 min) The Baldrige program should be a good process for a firm not only […]

978-0077733773 Chapter 2 Solution Manual Part 6

Chapter 02 – Implementing Strategy: The Value Chain, the Balanced Scorecard, and the Strategy Map 2-64 (continued -1) Source: James R. Hagerty, “Harley, With Macho Intact, Tries to Court More Women,” The Wall Street Journal, October 31, 2011, p B1’ […]

978-0077733773 Chapter 2 Solution Manual Part 7

Chapter 02 – Implementing Strategy: The Value Chain, the Balanced Scorecard, and the Strategy Map 2-69 (continued -1) 3. In the 2011-2014 period Mexico’s peso has been stable relative to the U.S. dollar; The Canadian dollar also has been relatively […]

978-0077733773 Chapter 20 Cases Part 1

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation Chapter 20 Management Compensation, Business Analysis, and Business Valuation Teaching Notes for Cases 20-1. Midwest Petro-Chemical Company: Evaluation of a Firm; Strategy Adapted from teaching note provided by the case […]

978-0077733773 Chapter 20 Cases Part 2

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation Profitability Ratios Relevance 2008 2009 2010 2011 2012 2013 Return on A measure of management’s available assets. 6.46% 6.29% 5.23% 4.02% 3.68% Return on Equity A measure of management’s effectiveness […]

978-0077733773 Chapter 20 Cases Part 3

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation frequently are evaluated, and receive a large part of their compensation, based on sales. Such compensation systems are used to: (1) motivate sales More generally, just about everyone’s performance is […]

978-0077733773 Chapter 20 Cases Part 4

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation Thus, in the first three years following the implementation of CIPP, the plan seems to have successfully created a “win-win” situation for the manufacturing employees and John Deere as a […]

978-0077733773 Chapter 20 Cases Part 5

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation The correlation measures for customer survey and wait time are used to determine the amount of the compensation sub-pool for each of these BSC measures, as follows: 20-41 Copyright © […]

978-0077733773 Chapter 20 Cases Part 6

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation 20-2 The Role of Strategy This article presents a careful look at the role of local culture in the desirability of different management control systems. Local culture is defined in […]

978-0077733773 Chapter 20 Lecture Note

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation Chapter 20 Management Compensation, Business Analysis, and Business Valuation Learning Objectives LO 20-1 Identify and explain the types of management compensation LO 20-2 Identify the strategic role of management compensation […]

978-0077733773 Chapter 20 Solution Manual Part 2

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation 20-27 Alternative Compensation Plans (20 min) 1. On the negative side, stock option incentives tied to share prices are influenced by the broad economic factors affecting the stock market, many […]

978-0077733773 Chapter 20 Solution Manual Part 3

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation 20-35 (continued -1) 4. A down-side to the switch to IFRS is that companies will have to study the IFRS carefully and determine for example whether the company will use […]

978-0077733773 Chapter 20 Solution Manual Part 4

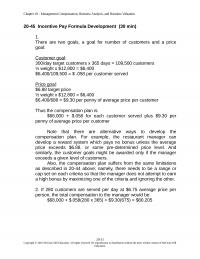

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation 20-45 Incentive Pay Formula Development (30 min) 1. There are two goals, a goal for number of customers and a price goal: Customer goal: 300/day target customers x 365 days […]

978-0077733773 Chapter 20 Solution Manual Part 5

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation 20-50 (continued -1) distress at the time of the study, the presence of this distress may have influenced the overall results. 4. The answers here could vary widely. One observation […]

978-0077733773 Chapter 20 Solution Manual Part 6

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation 20-53 (continued -1) A financial ratio analysis of BPP’s liquidity shows a company that is improving quite well on all measures. The receivables turnover and inventory turnover ratios are both […]

978-0077733773 Chapter 4 Cases Part 1

Chapter 4 – Job Costing Chapter 4 Job Costing Teaching Notes For Cases 4-1. Constructo Inc. (Under or Overapplied Overhead) This case has the learning objectives of: (1) explaining when it is appropriate for a company to use a job […]

978-0077733773 Chapter 4 Cases Part 2

Chapter 4 – Job Costing Exhibit TN-1 Existing Overhead Cost Allocation System Cost Center Component Component Component Group Part Group Part Group Part 4-7 Central Support Services (OAW) 5% of DM$ CONTRACT 15% of DM$ 40% of DM$ 150% of […]

978-0077733773 Chapter 4 Lecture Note

Chapter 04 – Job Costing Chapter 4 Job Costing Learning Objectives LO 4-1 Explain the types of costing systems. LO 4-2 Explain the strategic role of product costing. LO 4-3 Explain the flow of costs in a job costing system. […]

978-0077733773 Chapter 4 Solution Manual Part 1

Chapter 04 – Job Costing CHAPTER 4: JOB COSTING QUESTIONS 4-1 The strategic role of costing is to provide accurate cost information that is need managers, and refinement of strategic goals. 4-2 The three characteristics of costing systems are (1) […]

978-0077733773 Chapter 4 Solution Manual Part 2

Chapter 04 – Job Costing 4-31 Cost Flows; Applying Overhead (20 min) 1. Predetermined Overhead Rate = $1,980,000 ÷ 66,000 machine hours 2. Journal Entries: a. Materials Inventory 900,000 Accounts Payable 900,000 180,000 lbs x $5 = $900,000 b. Work-in-Process […]

978-0077733773 Chapter 4 Solution Manual Part 3

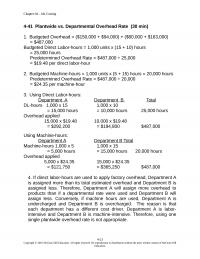

Chapter 04 – Job Costing 4-41 Plantwide vs. Departmental Overhead Rate (30 min) 1. Budgeted Overhead = ($150,000 + $94,000) + ($80,000 + $163,000) = $487,000 Budgeted Direct Labor-hours = 1,000 units x (15 + 10) hours 2. Budgeted Machine-hours […]

978-0077733773 Chapter 4 Solution Manual Part 4

Chapter 04 – Job Costing 4-46 (Continued -1) h. Selling& Administrative Expense 2,400 Accumulated Depreciation 2,400 i. Advertising Expense 5,500 Cash 5,500 j. Factory Overhead 13,500 Cash 13,500 k. Selling & Administrative Expense 13,250 Cash 13,250 l. Applied Overhead = […]

978-0077733773 Chapter 4 Solution Manual Part 5

Chapter 04 – Job Costing 4-48 (continued -6) 4-41 Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. Chapter 04 – Job Costing 4-48 (continued -7) 6. When you […]

978-0077733773 Chapter 5 Cases Part 1

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis Chapter 5 Activity-Based Costing and Customer Profitability Analysis Teaching Notes for Cases 5-1 Blue Ridge Manufacturing (Activity-Based Costing for Marketing Channels) Case Description: Blue Ridge Manufacturing produces and sells towels for […]

978-0077733773 Chapter 5 Cases Part 2

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis The following points should come out in the discussion: Segment Net income declines because SG&A allocation to segment was too low under the Sales dollar method. Marketing costs (price promotions, merchandising, […]

978-0077733773 Chapter 5 Cases Part 3

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis The following questions were not part of the requirements in the case competition. The questions could serve as the basis for the final question in the live presentations at the Annual […]

978-0077733773 Chapter 5 Cases Part 4

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis The Value Chain Timber; do we harvest our own timber? Sorting and preparing timber; receiving the lumber in the pulp plant Pulp manufacturing Debarking; a 16×100 ft drum; tumbling the logs […]

978-0077733773 Chapter 5 Cases Part 5

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis 6. Identify the activity drivers for overheads activity-cost pools identified in this study and explain the reasons for the selection? Gasoline Sales Attendants (Labor): Volume of gasoline sold (a unit-level activity […]

978-0077733773 Chapter 5 Lecture Note Part 1

Chapter 05 – Activity-Based Costing and Customer Profitability Analysis Chapter 5 Activity-Based Costing and Customer Profitability Analysis Learning Objectives LO 5-1 Explain the strategic role of activity-based costing. LO 5-2 Describe activity-based costing (ABC), the steps in developing an ABC […]

978-0077733773 Chapter 5 Lecture Note Part 2

Chapter 05 – Activity-Based Costing and Customer Profitability Analysis 3. Steps in ABC Costing Step 1 – Identify resource costs and activities Step 2 – Assign overhead to activity center or cost pools using resource consumption cost driver Step 3 […]

978-0077733773 Chapter 5 Solution Manual Part 1

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis CHAPTER 5: ACTIVITY-BASED COSTING AND CUSTOMER PROFITABILITY ANALYSIS QUESTIONS 5-1 Undercosting a product may appear to have increased the reported profit the product earned (assuming the firm did not lower its […]

978-0077733773 Chapter 5 Solution Manual Part 2

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis 5-31 Applications of ABC Costing in Government (20 min) 1,2. Some of the examples are noted in the text, including the U.S. Postal Service, the U.S. Patent Office, and the U.S. […]

978-0077733773 Chapter 5 Solution Manual Part 3

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis 5-38 (continued) 3. The total value chain cost provides the firm a long-term perspective of the product cost, in addition to the short term manufacturing cost. Different industries have different cost […]

978-0077733773 Chapter 5 Solution Manual Part 4

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis 5-42 (continued-1) The budgeted unit costs per pound are: Mona Loa Coffee Malaysian Coffee Direct unit costs: Direct materials $4.20 $3.20 Direct labor 0.30 $4.50 0.30 $3.50 Indirect unit costs: Purchasing […]

978-0077733773 Chapter 5 Solution Manual Part 5

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis 5-45 (continued-3) Activity-based costing provides ADA with more detailed and better estimates of product costs. For example by using ABC, ADA becomes aware that the cost of Diomycin is lower ($0.4818 […]

978-0077733773 Chapter 5 Solution Manual Part 6

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis 5-48 Personnel Planning; TDABC(30 min) 1. Unlike a manufacturing company, almost all costs for a service company are indirect in nature. Almost all of these costs are supplied in advance; short-term […]

978-0077733773 Chapter 6 Cases Part 1

Chapter 6 – Process Costing Chapter 6 Process Costing Teaching Notes for Cases and Articles Teaching Notes For Cases 6-1. The Rossford Plant (Two Production Processes with the Traditional Volume-Based Costing System) The Rossford Plant case focuses on issues of […]

978-0077733773 Chapter 6 Cases Part 2

Chapter 6 – Process Costing PROCESS COSTING SYSTEM – FULL SOLUTION Question 1: What journal entries should be made to record this period’s activities? The case information is used to generate the following journal entries. Account Titles Debits1Credits , Cash […]

978-0077733773 Chapter 6 Lecture Note

Chapter 06 – Process Costing Chapter 6 Process Costing Learning Objectives 1. Identify the types of firms or operations for which a process costing system best supports the organization’s competitive strategy 2. Explain and calculate equivalent units 3. Describe the […]

978-0077733773 Chapter 6 Solution Manual Part 1

Chapter 06 – Process Costing CHAPTER 6: PROCESS COSTING QUESTIONS 6-1 A company that should use a process costing system typically has homogenous 6-2 Process costing is likely used in industries such as chemicals, oil refining, textiles, paints, flour, canneries, […]

978-0077733773 Chapter 6 Solution Manual Part 2

Chapter 06 – Process Costing 6-29 (continued -1) 3. As in most process industries, sustainability issues arise in the manufacture of refined sugar. For example, the sugar company produces a large amount of shredded cane as one of the outputs […]

978-0077733773 Chapter 6 Solution Manual Part 3

Chapter 06 – Process Costing 6-37: Weighted Average Method (20 min) 1.,2. 6-38 FIFO Method (20 min) — see solution above 6-39 Weighted-Average Method (30-40 min) 6-21 Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without […]

978-0077733773 Chapter 6 Solution Manual Part 4

Chapter 06 – Process Costing 6-43 (continued -1) 4. The request is a violation of the controller’s responsibility to prepare accurate production cost reports. The ethical principles of integrity and objectivity require the controller to use the best available estimate […]

978-0077733773 Chapter 6 Solution Manual Part 5

Chapter 06 – Process Costing 6-49 (continued -1) 2. 4. a. $69,167 b. $65,793 c. $1,487,167 d. $119,060 6-41 Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. a. […]

978-0077733773 Chapter 6 Solution Manual Part 6

Chapter 06 – Process Costing 6-52 Implementing Process Cost Systems; Activity-based Costing; Standard Costing (25 min) Case 1: Because of the moderate volatility in materials prices and because of the relatively large percentage of costs in ending work-in-process, the FIFO […]

978-0077733773 Chapter 7 Cases Part 1

Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products Chapter 7 Cost Allocation: Departments, Joint Products, and By- Products Teaching Notes for Cases 7-1. Revenue Allocation; Utility Industry; Strategy This case concerns the process used in the state of […]

978-0077733773 Chapter 7 Cases Part 2

Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products Case 7-3 Business Services Corporation The case involves the allocation of the indirect costs associated with holding and distributing replacement parts used in servicing the computer and other business products […]

978-0077733773 Chapter 7 Lecture Note

Chapter 07 – Cost Allocation: Departments, Joint Products, and By-Products Chapter 7 Cost Allocation: Departments, Joint Products, and By-Products Learning Objectives 1. Identify the strategic role and objectives of cost allocation. 2. Explain the ethical issue of cost allocation. 3. […]

978-0077733773 Chapter 7 Solution Manual Part 1

Chapter 07 – Cost Allocation: Departments, Joint Products, and By-Products CHAPTER 7: COST ALLOCATION: DEPARTMENTS, JOINT PRODUCTS, AND BY-PRODUCTS QUESTIONS 7-1 The four objectives in the strategic role of cost allocation are to achieve effective cost management through methods which: […]

978-0077733773 Chapter 7 Solution Manual Part 2

Chapter 07 – Cost Allocation: Departments, Joint Products, and By-Products 7-24 Cost Allocation and Taxation at Nonprofit Organizations (10 min) The nonprofit has an incentive to allocate a relatively large portion of the common costs to the business activity to […]

978-0077733773 Chapter 7 Solution Manual Part 3

Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products 7-30 Joint Products; As the text notes, the physical units method often involves inappropriate allocation of costs as the physical measure may be unrelated to the ultimate value of the […]

978-0077733773 Chapter 7 Solution Manual Part 4

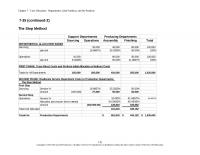

Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products 7-35 (continued-2) The Step Method 7-31 Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. Chapter 7 – Cost […]

978-0077733773 Chapter 7 Solution Manual Part 5

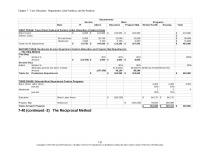

Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products 7-38 (continued -2) The Reciprocal Method 7-41 Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. Chapter 7 – […]

978-0077733773 Chapter 7 Solution Manual Part 6

Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products 7-40 (continued -2) The Reciprocal Method 7-51 Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. Chapter 7 – […]

978-0077733773 Chapter 7 Solution Manual Part 7

Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products 7-43 (continued -1) 4. No, NBP should not process RBL further. Increase in sales revenue: 80,000 x ($12 – $10) = $160,000 7-61 Copyright © 2016 McGraw-Hill Education. All rights […]

978-0077733773 Chapter 7 Solution Manual Part 8

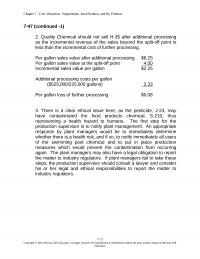

Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products 7-47 (continued -1) 2. Quality Chemical should not sell H-35 after additional processing as the incremental revenue of the sales beyond the split-off point is less than the incremental cost […]

978-0077733773 Chapter 8 Cases Part 1

Chapter 8 – Cost Estimation Chapter 8 Cost Estimation Teaching Notes for Cases 8-1. High-Low Method and Regression Analysis 1, 2. The spreadsheet below shows the analysis of the Brenham Hospital data using both regression and high-low methods. Before either […]

978-0077733773 Chapter 8 Cases Part 2

Chapter 8 – Cost Estimation Case 8-5 Predicting the Effect of Poverty on High School Graduation Rate High School graduation rates are a key measure of economic development and potential for economic growth. The data below show the graduation rates […]

978-0077733773 Chapter 8 Lecture Note Part 1

Chapter 08 – Cost Estimation Chapter 8 Cost Estimation Learning Objectives 1. Explain the strategic role of cost estimation. 2. Apply the six steps of cost estimation. 3. Use each of the cost estimation methods: the high-low method and regression […]

978-0077733773 Chapter 8 Lecture Note Part 2

Chapter 08 – Cost Estimation An Illustration Cost Estimation: The Use of Regression Analysis in the Gaming Industry Harrah’s own many large casinos throughout the world, but particular in Las Vegas, where it operates The Flamingo, Caesars Palace, and Paris […]

978-0077733773 Chapter 8 Solution Manual Part 1

Chapter 08 – Cost Estimation CHAPTER 8: COST ESTIMATION QUESTIONS 8-1 Cost estimation is the process of developing a well-defined relationship between a cost object and its cost driver for the purpose of predicting the cost. The cost predictions are […]

978-0077733773 Chapter 8 Solution Manual Part 2

Chapter 08 – Cost Estimation 8-30 Cost Relationships (10 min) N = Number of Cleaning Services Total annual cost is: (Note: 100 service calls per month = 1,200 service calls per year; we need total annual service since $165,000 is […]

978-0077733773 Chapter 8 Solution Manual Part 3

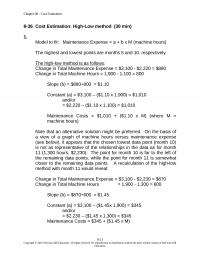

Chapter 08 – Cost Estimation 8-36 Cost Estimation: High-Low method (30 min) 1. Model to fit: Maintenance Expense = a + b x M (machine hours) The highest and lowest points are months 5 and 10, respectively. The high-low method […]

978-0077733773 Chapter 8 Solution Manual Part 4

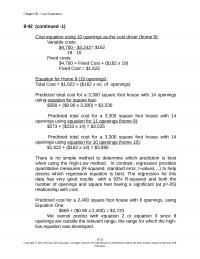

Chapter 08 – Cost Estimation 8-42 (continued -1) Cost equation using 10 openings as the cost driver (home 9): Variable costs: $4,700 – $3,242= $162 19 – 10 Fixed costs: $4,700 = Fixed Cost + ($162 x 19) Fixed Cost […]

978-0077733773 Chapter 8 Solution Manual Part 5

Chapter 08 – Cost Estimation 8-45 (continued -1) The global nature of the Pilot Shop’s operations adds another limitation to the analysis. The purchasing and shipping costs will vary with international business conditions and also with fluctuations in 8-41 Copyright […]

978-0077733773 Chapter 8 Solution Manual Part 6

Chapter 08 – Cost Estimation 8-50 (continued -1) To potentially improve the measurement of the employment rate, the regression analysis shown below uses the unemployment rate for college graduates 25 years or older (also from the Bureau of Labor Statistics […]

978-0077733773 Chapter 8 Solution Manual Part 7

Chapter 08 – Cost Estimation 8-55 Cross-Sectional Regression; Ranks; Follows from 8-54 (35 min) The regression results are shown below. Note that none of the independent variables are significant. To examine the possibility that the size of the company may […]

978-0077733773 Chapter 8 Solution Manual Part 8

Chapter 08 – Cost Estimation 8-57 Cross-Sectional Regression (30 min) 1. Regression Statistics Multiple R 0.976518934 R Square 0.953589229 999 Adjusted R Square 0.95001917 Standard Error 25458.32309 Observations 15 ANOVA df SS MS F Significance F Regression 1 1.73119E+11 1.73E+11 […]

978-0077733773 Chapter 9 Cases Part 1

Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit Analysis Chapter 9 Short-Term Profit Planning: Cost-Volume-Profit Analysis Teaching Notes for Cases Case 9-1: CVP Analysis; Strategy This problem can perhaps be visualized most easily by first constructing a table that shows the […]

978-0077733773 Chapter 9 Cases Part 2

Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit Analysis TN-1: Example of Spreadsheet Solution for Alltel Case Alltel Pavilion EXPECTED PAYING ATTENDANCE 8,251 GIVEN TOTAL REVENUE FROM TICKETING PER CAPITA $ 26.99 GIVEN TOTAL REVENUE FROM ANCILLARIES PER CAPITA $ 13.09 […]

978-0077733773 Chapter 9 Cases Part 3

Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit Analysis As before, πB = TR – VC – FC = (sp*X) – (vc*X) – FC = $5X For Alternative #2: πB = 0.05($60X) ÷ (1 – 0.40) = $5X As before, πB […]

978-0077733773 Chapter 9 Lecture Note Part 1

Chapter 09 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis Chapter 9 Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis Learning Objectives LO 9-1 Explain cost-volume-profit (CVP) analysis, the CVP model, and the strategic role of CVP analysis. LO 9-2 Apply CVP analysis […]

978-0077733773 Chapter 9 Lecture Note Part 2

Chapter 09 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis Another analytical approach to sensitivity analysis is to express the factors of the CVP model as random variables, and then to examine the outputs of the model probabilistically. This approach also […]

978-0077733773 Chapter 9 Solution Manual Part 1

Chapter 09 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis CHAPTER 9 SHORT-TERM PROFIT PLANNING: COST-VOLUME-PROFIT (CVP) ANALYSIS QUESTIONS 9-1 The underlying relationship depicted in a cost-volume-profit (CVP) analysis is that costs, revenues, and operating profits (Y) all change in a […]

978-0077733773 Chapter 9 Solution Manual Part 2

Chapter 09 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis 9-24 Cost Planning: The Cost of an MBA; Time Value of Money (20 minutes) Using the present value factor (4.212) for an annuity for five years at 6% shows that the […]

978-0077733773 Chapter 9 Solution Manual Part 3

Chapter 09 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis 9-32 Further Analysis–Degree of Operating Leverage (DOL) (40-45 min) 1. Demonstrating that DOL represents the % change in operating income DOL = CM ÷ Operating Income (OI), for any given sales […]

978-0077733773 Chapter 9 Solution Manual Part 4

Chapter 09 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis 9-37 (Continued-1) 4. BE units = F ÷ contribution margin per unit = ($500,000 + $160,000) ÷ ($80.00 − $41.50)/unit = $660,000 ÷ $38.50/unit = 17,143 units πB= Sales − variable […]

978-0077733773 Chapter 9 Solution Manual Part 5

Chapter 09 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis 9-40 (Continued-1) Step Two: Run Goal Seek Step Three: Results Thus, at 1,280 tests per year, the total cost under each of the two decision alternatives would be the same: $256,000. […]

978-0077733773 Chapter 9 Solution Manual Part 6

Chapter 09 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis 9-44 CVP Analysis; Uncertainty/Sensitivity Analysis (60-75 min) 1. To break even, during the first year of operations, 3,649 clients (rounded up) must visit the law office being considered by Don Carson […]

978-0077733773 Chapter 9 Solution Manual Part 7

Chapter 09 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis 9-46 (Continued-1) Total Relevant Cost, Current Plan = Total Relevant Cost, Proposed Plan ($43.50 × Q) + $6,000,000 = ($58.75 × Q) + $3,000,000 ($58.75 − $43.50)/unit × Q = $6,000,000 […]

978-0077733773 Chapter 9 Solution Manual Part 8

Chapter 09 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis 9-48 (Continued-4) The above data table provides the results of a sensitivity analysis. Specifically, we are looking at the sensitivity of the breakeven point to the assumption regarding sales mix for […]

978-0077733773 Chapter 9 Solution Manual Part 9

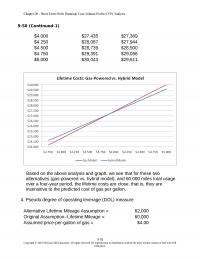

Chapter 09 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis 9-50 (Continued-1) $4.000 $27,435 $27,389 $4.250 $28,087 $27,944 $4.500 $28,739 $28,500 $4.750 $29,391 $29,056 $5.000 $30,043 $29,611 Based on the above analysis and graph, we see that for these two 4. […]

Accounting Chapter 1 1 Cost management has moved from a traditional role of product costing and operational control to a broader strategic focus

1. Which of the following does not represent a main focus of cost management information? A. Strategic management. B. Performance measurement. C. Planning and decision making. D. Preparation of financial statements. E. Internal audit and control. AACSB: Reflective Thinking AICPA: […]

Accounting Chapter 1 2 The competitive strategy of differentiation is implemented by a firm’s targeted, careful attention to

AACSB: Reflective Thinking AICPA: BB Critical Thinking AICPA: FN Risk Analysis Accessibility: Keyboard Navigation Blooms: Remember Difficulty: 1 Easy Learning Objective: 01-04 Explain the different types of competitive strategies. Topic: Competitive Strategies 38. The competitive strategy of differentiation is implemented […]

Accounting Chapter 1 3 Explain these ideas, using as a framework your need to develop a plan for interviewing successfully for a challenging professional

AACSB: Reflective Thinking AICPA: BB Critical Thinking AICPA: FN Risk Analysis Accessibility: Keyboard Navigation Blooms: Understand Difficulty: 2 Medium Learning Objective: 01-03 Explain the contemporary management techniques and how they are used in cost management to respond to the contemporary […]