Chapter 12 – Strategy and the Analysis of Capital Investments

12-56 Sensitivity Analysis; Equipment-Replacement Decision (45-60

minutes)

1. The maximum amount of annual variable operating expenses, pre-tax,

that would make this an attractive investment from a present-value

standpoint = $99,206 as follows:

Net investment outlay, time 0 = $460,000

Differential salvage value, e-o-y 6 = $90,000

Net investment outlay − PV of salvage differential = $409,197

Year PV factor s (@ 10%)

1 0.90909 (1 ÷ (1+0.10)1)

2 0.82645 (1 ÷ (1+0.10)2)

3 0.75131 etc.

4 0.68301

Therefore, maximum annual operating cost, new asset

2. Recalculation, based on an after-tax basis:

Combined (federal and state) income tax rate = 35.00%

After-tax WACC (discount rate) = 8.00%

12-93

Chapter 12 – Strategy and the Analysis of Capital Investments

12-56 (Continued-1)

Gain/Loss on sale:

Selling price = $40,000

NBV = $60,000

Tax savings due to deductibility of loss = loss x tax

rate = $20,000 × 0.35 = $7,000

Net-of-tax initial investment outlay, time 0 =

Pretax amount – tax savings due to loss

Annual tax shield, existing asset = $3,500

Annual tax shield, replacement asset = $29,167 $25,667

PV of differential depreciation tax shield (@ 8%) =

$25,667 × 4.623 (see below) = $118,657

4 0.73503

5 0.68058

6 0.63017

4.62300

(above answer is rounded to three decimal places)

12-94

Chapter 12 – Strategy and the Analysis of Capital Investments

12-56 (Continued-2)

PV of after-tax variable operating costs, replacement asset

=

after-tax net investment outlay − PV of after-tax differential

salvage values − PV of differential tax savings due to depreciation

PV of annuity = annuity amount × annuity factor

annuity amount = PV of annuity ÷ annuity factor

= $297,478 ÷ 4.623 = $64,347

Therefore, maximum annual after-tax variable operating expenses new

asset

3. Additional (i.e., strategic) factors that might bear upon this decision:

a) Are any competitors of the Mendoza Company contemplating a

similar investment? Would such investments by competitors pose a

strategic risk to the Mendoza Company?

b) Are there any environmental-management benefits associated with

the new equipment?

c) What would be the impact of the proposed investment on other non-

financial performance indicators, such as (1) on-time delivery

performance, (2) customer response times, or (3) process up time?

d) Is Mendoza competing on the basis of price? Would the proposed

investment allow the company to establish/maintain its position as a

low-cost competitor?

12-95

Hill Education.

Chapter 12 – Strategy and the Analysis of Capital Investments

12-57 Present Value Analysis; Sensitivity Analysis; Spreadsheet Applications (60

Minutes)

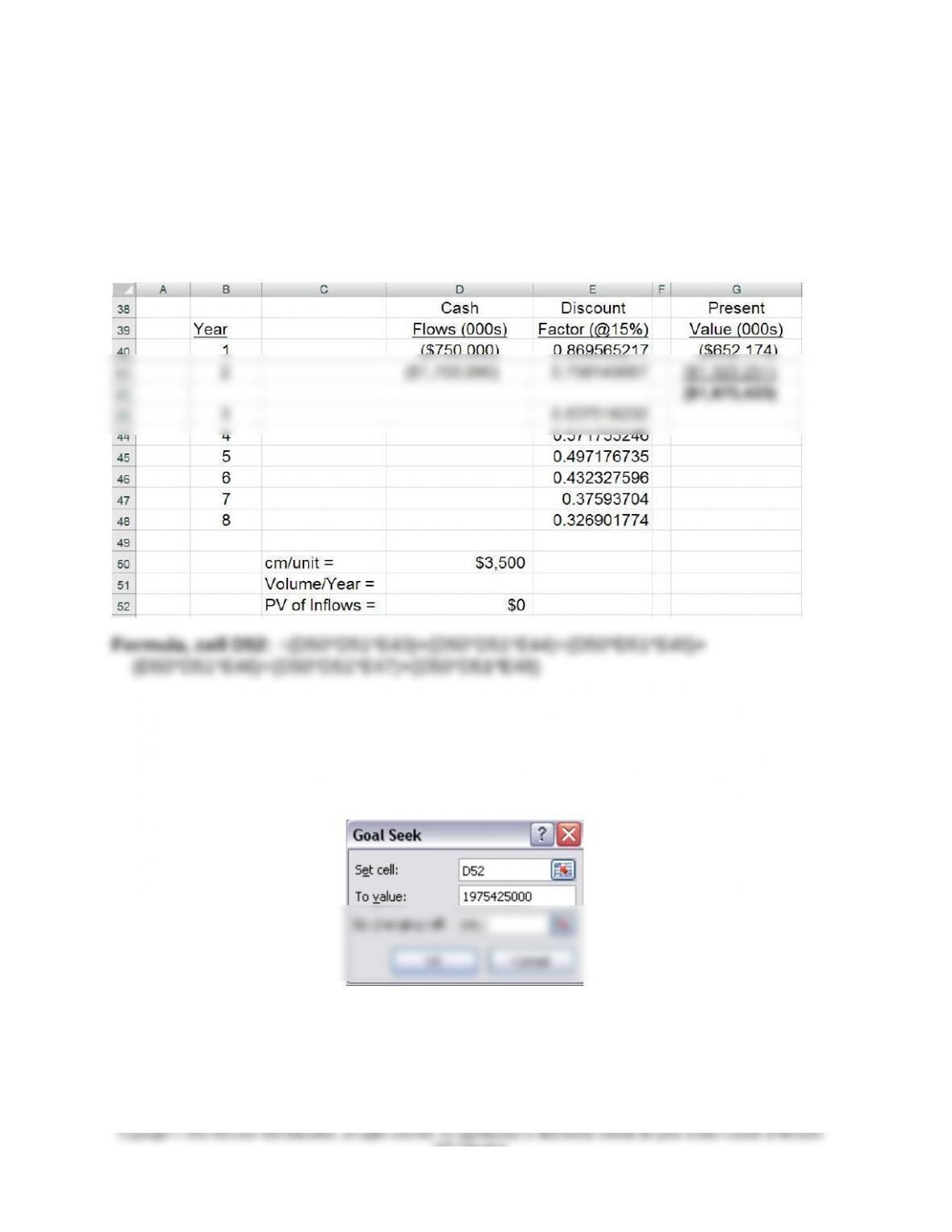

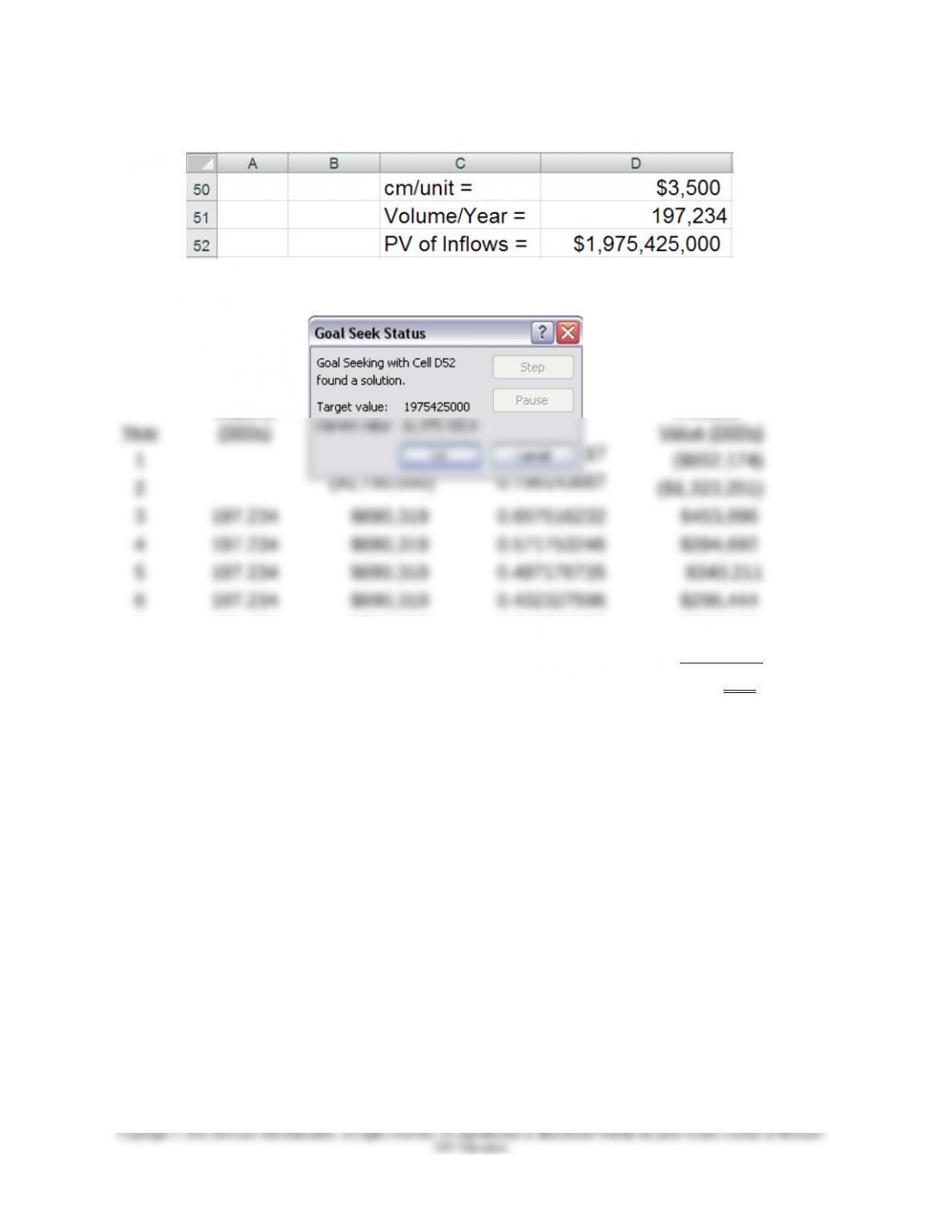

1. The minimum volume of car sales, per year, in the six-year life of the plant that is

needed to make this proposed investment acceptable using NPV as decision

criterion is 197,234, as follows:

Note: The discount factors in Column D were calculated using the following equation:

PV factori = 1 ÷ (1 + r)i, where r = discount rate (WACC) and i = year (i = 1, 8).

Goal Seek Window:

After running GOAL-SEEK, the result is as follows:

12-96

Hill Education.

Chapter 12 – Strategy and the Analysis of Capital Investments

12-57 (Continued-1)

And the GOAL SEEK window will have changed to:

Check:

Discount

Volume

Cash Flows

Factor

Present

7 197.234 $690,319 0.375937040 $259,516

8 197.234 $690,319 0.326901774 $225,666

($0)

12-97

Chapter 12 – Strategy and the Analysis of Capital Investments

12-57 (Conitnued-2)

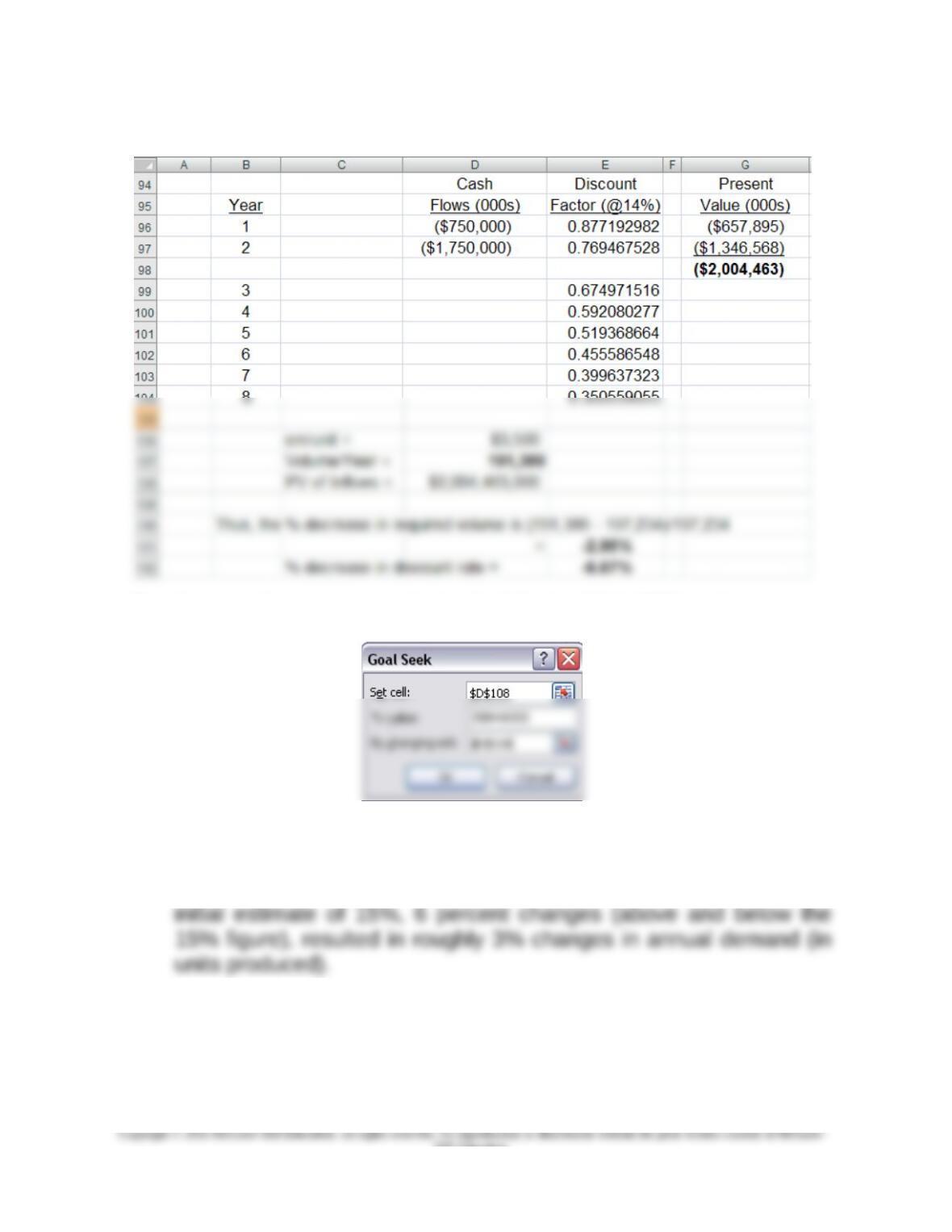

2. Sensitivity analysis:

a. if the company’s pre-tax WACC is 16% (rather than 15%), then the

required annual volume changes to 203,155 units (% change =

3.00%), as follows:

Cash Discount Present

Year Flows (000s) Factor (@16%) Value (000s)

1 ($750,000) 0.862068966 ($646,552)

2 ($1,750,000) 0.743162901 ($1,300,535)

($1,947,087)

3 0.640657674

4 0.552291098

5 0.476113015

6 0.410442255

b. if the company’s pre-tax WACC is 14% (rather than 15%), then the

12-98

Hill Education.

Chapter 12 – Strategy and the Analysis of Capital Investments

12-57 (Continued-3)

The above results were generated using the following GOAL SEEK entries:

2c. Sensitivity issue: based on the limited analysis above, it does not

appear that the results are very sensitive to the assumption

regarding the discount rate (WACC) used in the analysis. From the

3. Selected strategic considerations, including those related to risk

management, that would likely bear on this decision:

12-99

Hill Education.

Chapter 12 – Strategy and the Analysis of Capital Investments

12-57 (Continued-4)

a) Given volatility in the demand for fossil fuels, and wide price swings in

the cost of gasoline, are there any embedded options (“real options”)

in this investment project?

b) A rather substantial investment outlay is required. How sensitive is the

decision to accept or reject the project with respect to required

volume?

c) Are the facilities being envisioned flexible in nature (which would allow

the company to quickly change/revise its product in response to

changes in consumer demand and preferences)?

d) Are there any risks associated with not investing in this new product?

That is, will there be associated effects on the company’s existing

product line(s)?

e) Would the company be at competitive risk were it not to invest in the

new technology? That is, is this new-car option available to the

company’s competitors? If these competitors invest in this area, would

the company be at strategic risk?

f) Does the company compete on the basis of product differentiation?

That is, is the new product consistent with the strategy the company is

pursuing? Will, for example, the new facilities allow for reduced

product-development times (i.e., increased speed to market) and/or

increased product quality, either of which would help the company

achieve its stated value proposition to its targeted customers.

12-100

Hill Education.

Chapter 12 – Strategy and the Analysis of Capital Investments

12-58 MACRS Depreciation and Capital-Budgeting Analysis; Sensitivity Analysis;

Spreadsheet Application (60 minutes)

1. The estimated after-tax NPV of this proposed investment is ($66,917), as follows:

Net investment outlay, time 0:

Purchase cost $500,000

Remodeling cost (25 units × $20,000 per unit) $500,000

Net investment outlay $1,000,000

After-tax cash inflow per year:

Pre-tax rental revenue, $500 units = 15 units × $500 × 12 = $90,000

Pre-tax rental revenue, $650 units = 10 units × $650 × 12 = $78,000

After-tax Cash Operating Expenses per Year:

Pre-tax expenses, $500 units ($90,000 × 0.16) = $14,400

Estimated NPV of Proposed Investment (@ 10% discount rate):

Net initial investment outlay, time 0 = ($1,000,000)

Plus: PV of after-tax rental revenues (9.427× $100,800) = $ 950,242

Plus: PV of MACRS depreciation tax savings

Note: the PV factor of 0.3372 for 27.5-year residential rental property is given in the

problem, but can be calculated as follows:

PV27YR = [ (t * Dep%i) ÷ (1+r)i] ÷ 100, where t = tax rate, Dep% = MACRS

depreciation rate (e.g., from Exhibit 12.4), r = WACC (discount rate), and i =

1,28.The MACRS depreciation rates for 27.5-year property must be obtained outside

the text (they are not disclosed in Exhibit 12.4.)

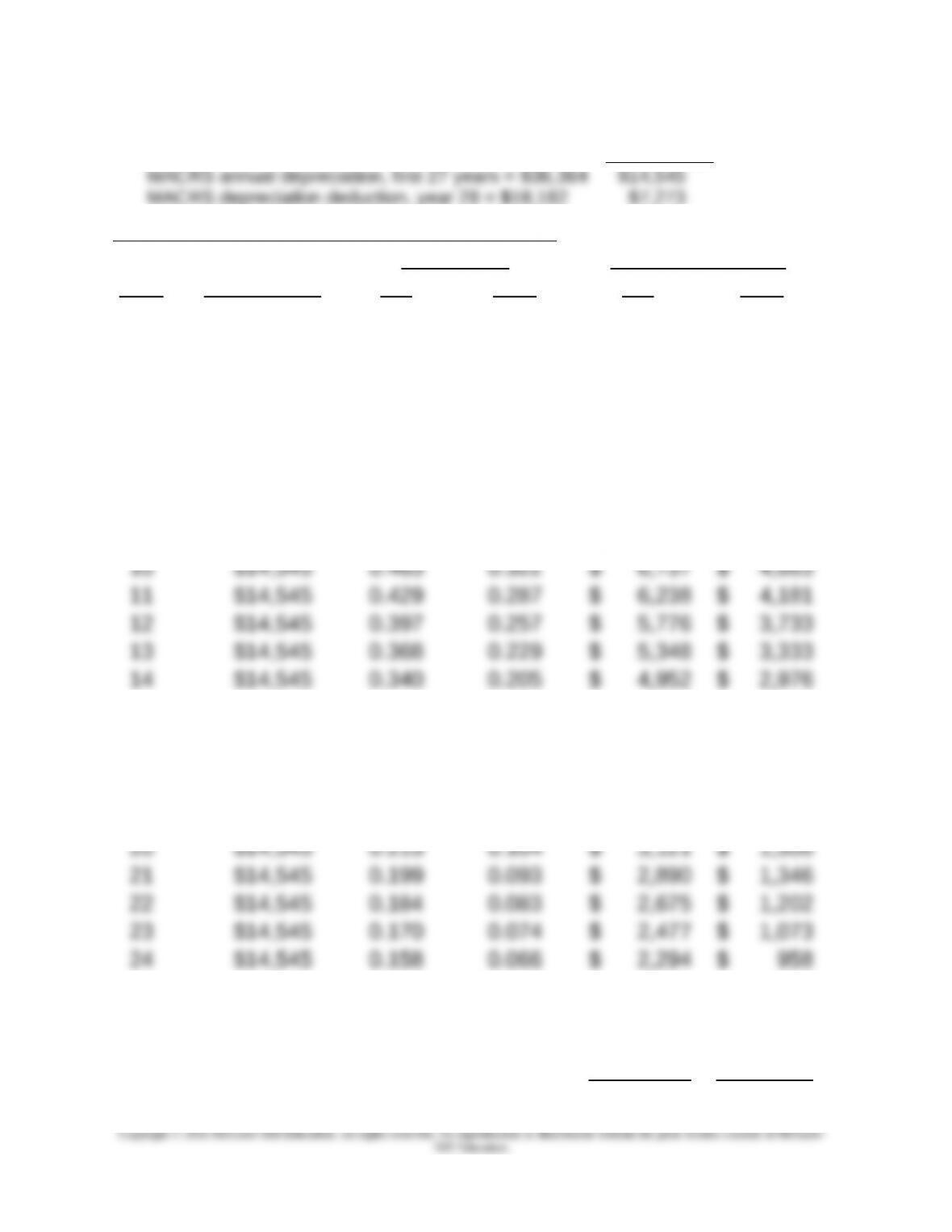

2. Sensitivity analysis:

a. If the discount rate were 8% (rather than 10%), the estimated NPV of the project

is now positive, as follows:

MACRS depreciation per year, first 27 years = 3.636%

Chapter 12 – Strategy and the Analysis of Capital Investments

12-58 (Continued-1)

Tax Savings

Present Value of MACRS Depreciation Deductions

PV Factors PV of Tax Savings

Year Tax Savings 8% 12% 8% 12%

1 $14,545 0.926 0.893 $ 13,468 $ 12,987

2 $14,545 0.857 0.797 $ 12,470 $ 11,596

3 $14,545 0.794 0.712 $ 11,547 $ 10,353

4 $14,545 0.735 0.636 $ 10,691 $ 9,244

5 $14,545 0.681 0.567 $ 9,899 $ 8,253

6 $14,545 0.630 0.507 $ 9,166 $ 7,369

7 $14,545 0.583 0.452 $ 8,487 $ 6,580

8 $14,545 0.540 0.404 $ 7,858 $ 5,875

9 $14,545 0.500 0.361 $ 7,276 $ 5,245

15 $14,545 0.315 0.183 $ 4,585 $ 2,657

16 $14,545 0.292 0.163 $ 4,246 $ 2,373

17 $14,545 0.270 0.146 $ 3,931 $ 2,118

18 $14,545 0.250 0.130 $ 3,640 $ 1,891

19 $14,545 0.232 0.116 $ 3,370 $ 1,689

25 $14,545 0.146 0.059 $ 2,124 $ 856

26 $14,545 0.135 0.053 $ 1,967 $ 764

27 $14,545 0.125 0.047 $ 1,821 $ 682

28 $7,273 0.116 0.042 $ 843 $ 305

12-102