Chapter 10 – Strategy and the Master Budget

10-37 (Continued)

2. Budgeted Operating Income–Current Year:

Sales Revenue (2,500 units × $1,500 per unit) =

$3,750,00

0

Less: Variable Costs (2,500 units × $1,000 per unit) =

$2,500,00

0

$1,250,00

Operating Income =

0

3. Scenario Analysis:

Percentage Change from Baseline

Sales

Volume

Selling

Price

Variable

Cost Total Fixed

Scenarios (units) per Unit per Unit Costs

a 0.00% 10.00% 0.00% 10.00%

b 0.00% 0.00% 5.00% (5.00%)

c (8.00%) 10.00% 0.00% 0.00%

Sales

Volume

Selling

Price

Variable

Cost Total Fixed

Scenario (units) per Unit per Unit Costs

Baseline 2,500 $1,500 $1,000 $200,000

a 2,500 $1,650 $1,000 $220,000

b 2,500 $1,500 $1,050 $190,000

c 2,300 $1,650 $1,000 $200,000

$ Difference % Change

Baseline

Operating

Budgeted

Operating

From

Baseline

from

Baseline

Scenario Income Income Op. Income Op. Income

Baseline $1,050,000 $1,050,000 $0 0.00%

a $1,050,000 $1,405,000 $355,000 33.81%

b $1,050,000 $935,000 ($115,000) (10.95%)

c $1,050,000 $1,295,000 $245,000 23.33%

10-30

Chapter 10 – Strategy and the Master Budget

10-38 Cash Budgeting: Not-for-Profit Context (45 minutes)

1. “Endowment fund:” a gift (contribution) whose principal must be maintained but whose

income may be expended. (You might use the example of an “endowed professorship”

as an example.)

2.

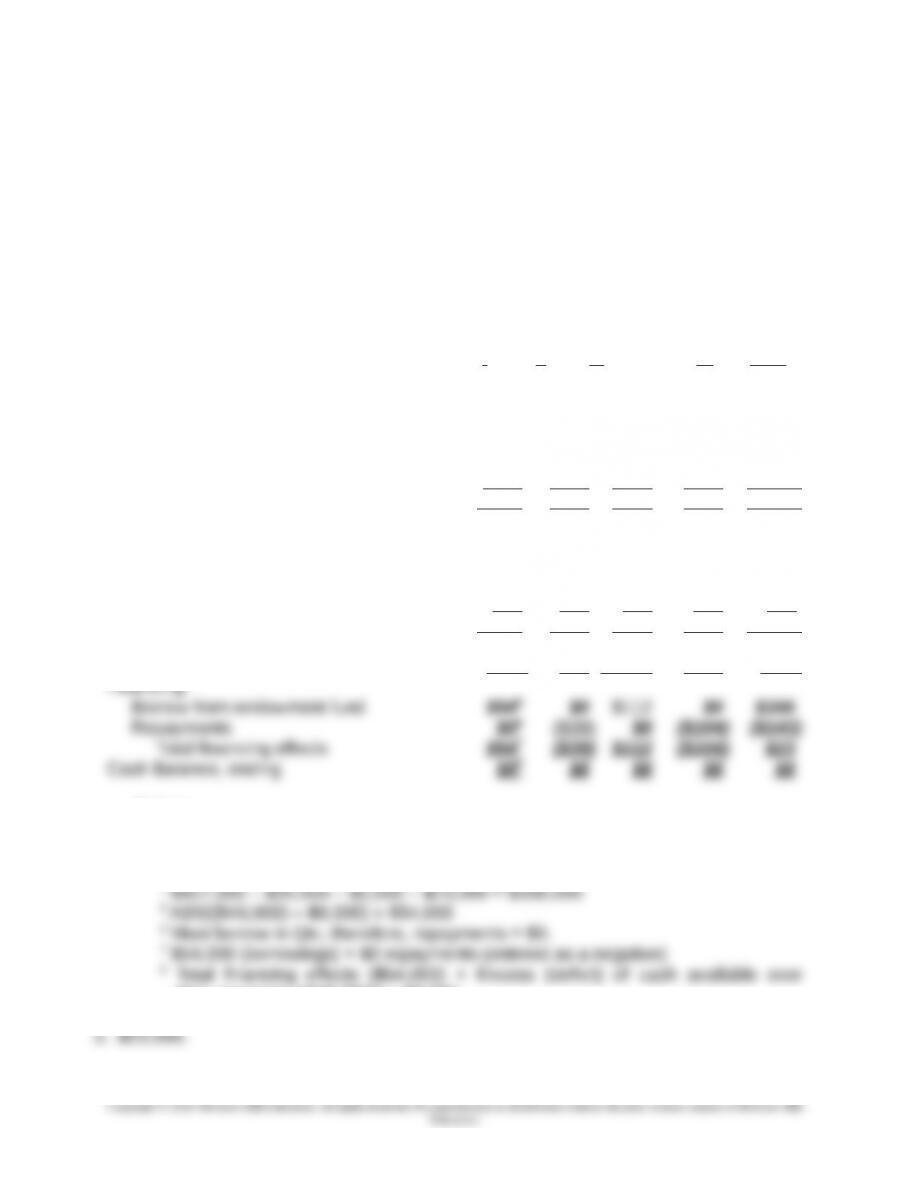

Cash Budget for Tri-County Social Service Agency

2016

(in thousands)

Quarters

I II III IV Year

Cash Balance, beginning $11 $8 $8 $8 $11

Receipts:

Grants $80 $70 $75 $75 $300

Contracts (evenly during year) $201$201$201$201$80

Mental Health Income (+5 in Qtrs. II, III) $20 $25 $30 $30 $105

Charitable donations $250 $350 $200 $400 $1 ,200

Total Cash Available $381 2

$473 $333 $533 $1 ,696

Less: Disbursements:

Salaries and Benefits $3354$342 $342 $346 $1,365

Office expenses $70 $65 $71 $50 $256

Equipment purchases & maintenance $2 $4 $6 $5 $17

Specific assistance $20 $15 $18 $20 $73

Total disbursements $427 3

$426 $437 $421 $1 ,711

Excess (deficiency) of cash available

over disbursements ($46 ) $47 ($104) $112 ($15 )

Notes:

1 Annual total ($80,000) ÷ 4

2 $11,000 + $80,000 + $20,000 + $20,000 + $250,000 = $381,000

3 $381,000 – ($46,000) = $427,000

4 $427,000 – $20,000 – $2,000 – $70,000 = $335,000

disbursements (($46,000)) = $8,000

10-31

Chapter 10 – Strategy and the Master Budget

10-38 (Continued)

4. It is probable that both donations and requests for services are unevenly distributed

Chapter 10 – Strategy and the Master Budget

10-39 Budgeting: Not-for-Profit (NFP) Context (30 minutes)

1. Stewardship is defined by Merriam-Webster Online Dictionary as “the conducting,

supervising, or managing of something; especially: the careful and responsible

management of something entrusted to one’s care.”

The Socially Responsible Investment Guidelines cited states: “Although it is a

moral and legal fiduciary responsibility of the trustees to ensure an adequate return

on investment for the support of the work of the church, their stewardship

embraces broader moral concerns.” Also, the principles of stewardship lists two

fundamental and interdependent principles: “The Conference should exercise

responsible financial stewardship over its economic resources.” and “The

Conference should exercise ethical and social stewardship in its investment

policy.”

The latter states: “Socially responsible investment involves investment strategies

based on Catholic moral principles. These strategies are based on the moral

demands posed by the virtues of prudence and justice. They recognize the reality

that socially beneficial activities and socially undesirable or even immoral activities

are often inextricably linked in the products produced and the policies followed by

2. “These two major principles work together to encourage the Conference to identify

investment opportunities that meet both our financial needs and our social criteria.

10-33

Chapter 10 – Strategy and the Master Budget

10-40 Budgeting for a Service Firm (75 minutes)

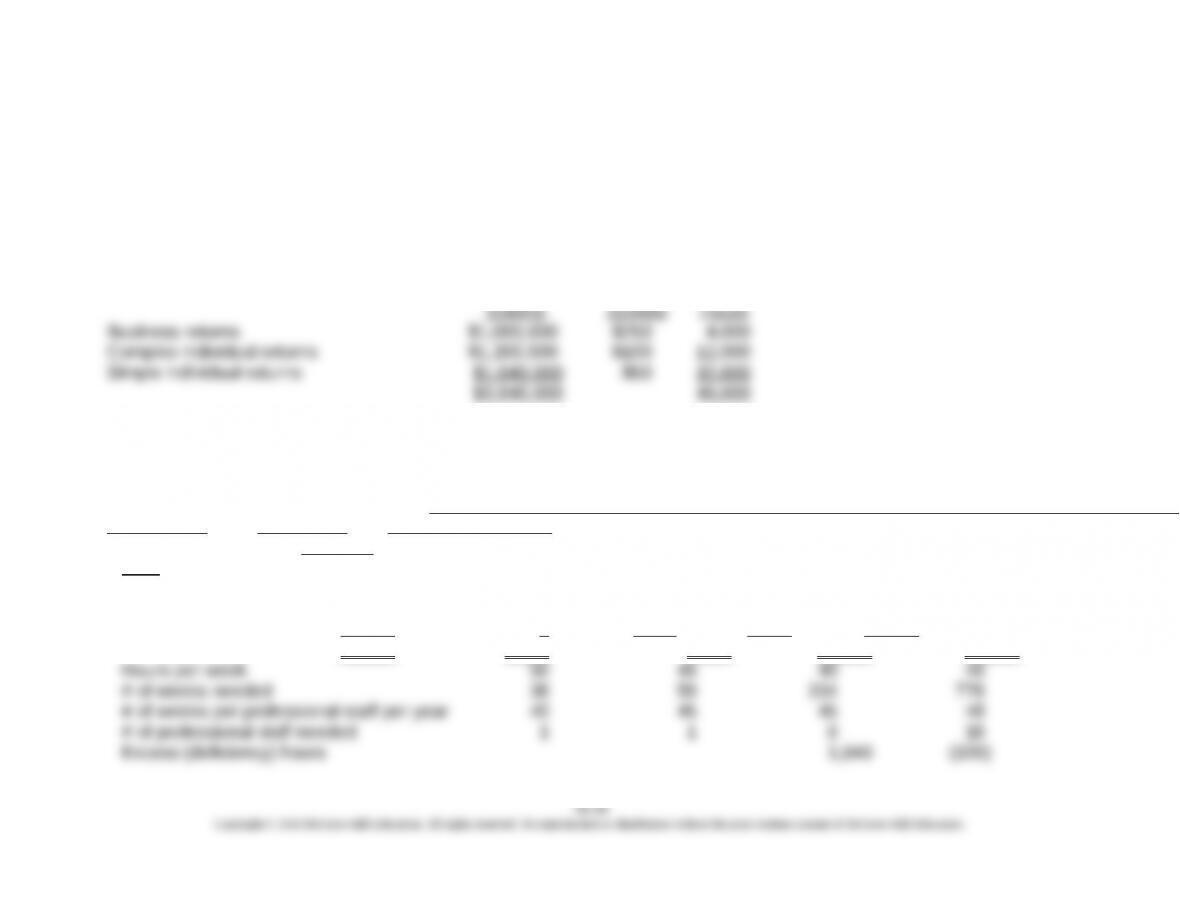

1.

Total hours for the budgeted activities:

Hourly

Budgeted Charge

Revenue Rate Required

Professional staff requirements for the budgeted revenue:

Senior

Total Hours

Manager Consultant _Consultant_

Required

Total Each Total

Business returns 4,000 0.30 1,200 0.20 800 0.502,000 0.00 0

Complex individual returns 12,000 0.05 600 0.15 1,800 0.404,800 0.40 4,800

Simple individual returns 32,800 0.00 0 0.00 0 0.20 6 ,560 0.80 26 ,240

Total Hours 48,800 1,800 2 ,600 13 ,360 31 ,040

Chapter 10 – Strategy and the Master Budget

Note: Because Consultants can be hired on a part-time basis, we round the calculation DOWN for this class of labor. The

other three labor classes are given (i.e., do not have to be planned for based on data in the problem).

Since, according to the present staffing plan and anticipated workload needs, there is an excess of senior

consultant hours, the budgeted cost for overtime hours worked by senior consultants would be $0.

10-35

Chapter 10 – Strategy and the Master Budget

10-40 (Continued-1)

2. Number of full-time consultants needed for the year:

No. of consultant-weeks needed for the year = 776 (from solution to requirement #1,

3. The manager’s total compensation, assuming that the revenues from preparing tax

returns remains the same:

Consultant’s pay:

Earning per year = $60,000

Hrs. worked/year = 1,920

Per senior consultant = $90,000

Per support staff = $40,000

Staffing Plan:

Partners = 1

Managers = 1

Education.

Chapter 10 – Strategy and the Master Budget

10-40 (Continued-2)

AccuTax, Inc.

Budgeted Operating Income

For the Year ended August 31, 2016

Revenue $3,840,000

Payroll expenses:

Partner $250,000

Manager 90,000

Senior consultants—base pay 720,000

Senior consultants—pay for overtime hours 0

Consultants:

Full-time $960,000

Part-time 10,000 970,000

Total compensation for the manager:

Salary (given) $90,000

Bonus (0.10 × [$1,237,000 − $500,000]) 73,700

Total $163,700

Note to Instructor: An Excel spreadsheet solution file is embedded in this document. You

can open the spreadsheet “object” that follows by doing the following:

1. Right click anywhere in the worksheet area below.

2. Select “Worksheet Object,” then “Open.”

3. To return to the Word document, select “File” and then “Close and return to…”

while you are in the spreadsheet mode.

Ex. 10-40 7e.xlsx

Chapter 10 – Strategy and the Master Budget

10–41 Activity–Based Budgeting (ABB) (30 Minutes)

1. Total budgeted cost for each activity and for the Business Services Division for

January 2016:

Budgeted Cost-

Activity Activity Driver Rate Total Cost

Storage 400,000 $0.4925 $ 197,000

Requisition Handling 30,000 $12.50 $ 375,000

Pick Packing 800,000 $ 1.50 $1,200,000

Data Entry 800,000 $ 0.80 $ 640,000

2. Activity-related data are not available. The only data you have is that budgeted

fixed cost per month is $1,000,000 and budgeted variable cost per carton is

$1.30. Using this approach, what is the estimated cost for the month? Compare

and comment on how your answer here differs from the answer to Requirement 1.

Budgeted total Cost for the Division for the Month of January:

correct, then the budget based on an ABC analysis should be more accurate in

terms of depicting the resource consumption (or resource demands) on the

organization for the coming month. Put another way, the use of a single, volume-

based cost driver will not likely capture the underlying economics of the

company’s support activities and associate cost.

3. Expected saving in costs—January 2016:

Requisition Handling (30,000 @ $12.50/requisition) = $ 375,000

Data Entry: number of lines (800,000 @ $0.80/line) = 640,000

(eliminate) the under-lying resource spending or deploy these resources

elsewhere. In other words, the savings will not likely occur automatically.

10-38

Education.

Chapter 10 – Strategy and the Master Budget

10-41 (Continued)

If the company uses a single cost-rate system based on the number of cartons

delivered, it will not be able to estimate the cost savings without special efforts to

10-39

Education.