Chapter 14 – Operational Performance Measurement: Sales, Direct Cost Variances, and the Role of Nonfinancial

Performance Indicators

Chapter 14

Operational Performance Measurement: Sales, Direct Cost Variances, and the

Role of Nonfinancial Performance Indicators

Learning Objectives

LO 14-1 Explain the essence of control systems in general and operational control systems in

particular

LO 14-2 Explain the total operating-income variance for a given period

LO 14-3 Develop a general framework for subdividing the total operating-income variance into

component variances

LO 14-4 Develop standard costs for product costing, performance evaluation, and control

LO 14-5 Record manufacturing cost flows and associated variances in a standard cost system

LO 14-6 Discuss major operating functions and the need for nonfinancial performance indicators

New in this Edition

Revision of four end-of-chapter problems

Revision/updating of two Real-World Focus (RWF) items (Demystifying a Consumer Gas Utility

Bill, and Controlling Labor Costs through the Use of “Workforce-Management Systems”)

Four totally new Real-World Focus (RWF) items (Managing Health Care Costs through Use of

Standard Cost Information; Managing Supply-Chain Costs; Using Technology to Manage Energy

and Water Consumption; and the NFL Takes the Lead in Promoting Sustainability and

Environmental Responsibility)

Teaching Suggestions

This chapter and the next explain the role of standard costs, flexible budgets, and variances in the

planning and control of operations and in the assessment of short-run operating results. I usually begin

this chapter with an introduction to control systems in general and, more specifically, management

accounting and control systems, financial control, and operational control. Particular emphasis is placed

on the strategic role of standard costing: to motivate improvements in both operational effectiveness and

efficiency. I then introduce students to the notion of flexible versus master (static) budgets, which are key

components of a traditional financial control model. I explain how these tools can be used to explain why

actual and master budget operating income differed for a period. In other words, I begin with the notion

that, traditionally, such tools can be used to answer the following question: why did actual operating

income for the period just ended differ from the operating income contained in our master (static) budget?

This total difference, or variance, is referred to as the “total operating-income variance” for the period.

(This is also referred to as the “total static (master) budget variance for the period.”)

Thus, students learn the importance of flexible budgets and standard costs for operational and financial

control purposes, as part of an organization’s comprehensive management accounting and control system.

Before shifting to the calculations of direct cost variances, I discuss the determination of cost standards in

practice, taking into account the “new manufacturing environment” and using benchmarking and activity

analysis.

I often cover this chapter in two class meetings. In the first class I cover the determination of operating

income and contribution margin variances and the development of standard costs and variance analysis.

14-1

Education.

Chapter 14 – Operational Performance Measurement: Sales, Direct Cost Variances, and the Role of Nonfinancial

Performance Indicators

The general framework presented in the chapter is a particularly useful tool that allows students to

structure their analysis. Please see text Exhibit 14.2, Exhibit 14.4 and Exhibit 14.7 for general

guidelines.

On the second class-day I pick some longer problems and cover the limitations, behavioral and

implementation issues. For accounting majors I will also make sure the class understands the accounting

entries that accompany standard cost systems. Finally, as indicated by the revised title for this chapter, I

discuss the strategic role of nonfinancial information in a comprehensive management accounting and

control system. In this regard, we discuss basic business processes (such as operating processes) and the

limitations of traditional financial control mechanisms for helping to improve such processes. Special

attention can be given to Just-in-Time (JIT) manufacturing, as a strategic operating process choice, and

the need for both financial and nonfinancial performance indicators within this context. Finally, Exhibit

14.14 (Customer Response Time) and Process Cycle Efficiency (PCE) are introduced as specific

examples of nonfinancial performance indicators that are relevant to the control of a JIT system.

Assignment Matrix

End-of-Chapter Exercises & Problems

Chapter Learning Objectives

Text Features

7th

ed.

EOC

6th

ed.

EOC

Transition

6e to 7e

X = included in Connect

Est.

Time

1. Essence of Ctl. systems

2. Explain total operating- income variance

3. Component Variances

4. Standard setting

5. Journal entries

6. Operating Functions/ Nonfinancial Indicators

Service

Ethics

Brief Exercises

14-13

14-14

Revised

X

5 min

X

14-14

14-17

–

X

10 min

X

X

14-15

14-13

–

X

5 min

X

14-16

14-16

–

X

5 min

X

14-17

14-15

–

X

5 min

X

14-18

14-18

Revised

X

5 min

X

14-19

14-19

Revised

X

5 min

X

14-20

14-20

Revised

X

5 min

X

14-21

14-21

Revised

X

5 min

X

14-22

14-22

Revised

X

5 min

X

Exercises

14-23

14-26

–

X

50 min

X

X

X

14-24

14-27

–

X

45 min

X

X

14-25

14-28

–

X

45 min

X

X

14-26

14-29

–

X

30 min

X

14-27

14-30

–

X

20 min

X

14-28

14-31

–

X

50 min

X

14-29

14-32

Revised

X

25 min

X

X

14-30

14-33

Revised

X

45 min

X

X

14-31

14-34

–

–

40 min

X

X

14-32

14-35

–

X

15 min

X

Continued on next page …

Chapter 14 Assignment Matrix—Continued

End-of-Chapter Assignments

Chapter Learning Objectives

Text Features

14-2

Education.

Chapter 14 – Operational Performance Measurement: Sales, Direct Cost Variances, and the Role of Nonfinancial

Performance Indicators

7th

ed.

EOC

6th

ed.

EOC

Transition

6e to 7e

X = included in Connect

Est.

Time

1. Essence of Ctl. systems

2. Explain total operating- income variance

3. Component Variances

4. Standard setting

5. Journal entries

6. Operating Functions/ Nonfinancial Indicators

Strategy

Service

International

Ethics

Sustainability

14-33

14-36

–

–

25 min

X

X

14-34

14-37

–

–

15 min

X

X

14-35

14-23

–

–

20 min

X

X

14-36

14-38

–

X

15 min

X

14-37

14-40

Revised

X

40 min

X

X

14-38

14-39

–

X

30 min

X

X

14-39

14-24

–

–

15 min

X

X

14-40

14-25

–

–

45 min

X

X

X

X

14-41

14-41

–

–

45 min

X

X

14-42

14-42

–

X

45 min

X

X

X

Problems

14-43

14-43

–

–

90 min

X

X

14-44

14-44

Revised

–

25 min

X

X

14-45

14-45

Revised

–

35 min

X

14-46

14-46

Revised

–

45 min

X

X

X

14-47

14-47

–

–

45 min

X

14-48

14-48

–

–

60 min

X

X

14-49

14-49

Revised

–

60 min

X

X

X

X

14-50

14-50

–

–

50 min

X

X

X

X

14-51

14-51

Revised

–

75 min

X

X

X

X

X

14-52

14-53

–

–

30 min

X

X

X

X

14-53

14-54

–

–

60 min

X

X

X

X

14-54

14-55

–

–

40 min

X

X

X

X

–

14-52

Deleted

Lecture Notes

Management Accounting and Control Systems (MACS): I generally start this chapter with a

discussion of the following elements, which are each part of an organization’s comprehensive

management accounting and control system (MACS):

Operational control (i.e., control of major operational processes)

Financial control:

Master budget

Flexible budget

Standard costs

Variances

Variances

A variance is the difference between an actual operating result and a budgeted or standard amount for the

operation. Variances are labeled as favorable or unfavorable. A favorable variance (F) has the effect of

14-3

Education.

Chapter 14 – Operational Performance Measurement: Sales, Direct Cost Variances, and the Role of Nonfinancial

Performance Indicators

increasing short-run operating profit while an unfavorable variance (U) has the effect of decreasing

short-run operating profit. Various revenue and cost variances are key outputs of a traditional financial

control system used to explain the total operating-income variance for the period, as explained more fully

below.

Total Operating-Income Variance = Static Budget Variance = Master Budget Variance

An indication of the financial effectiveness of operations during the period is the total operating

income variance, which defined as the difference between actual operating income for the period and the

amount of operating income reflected in the master (static) budget for the period. See text Exhibit 14.1.

Master (Static)

Actual Operating Income Budget Operating Income

Total Operating-Income Variance

I generally tell students that short-term operating profit is a function of five factors: selling price per unit,

variable cost per unit, total fixed costs, sales volume (quantity), and sales mix. If we assume a single-

product context, then any operating-income variance for the period should be explainable by the other

four factors being different from plans. The process of explaining the total operating income variance is

referred to as “variance decomposition.” Exhibit 14.2 can be used to provide students with the “big

picture” of variance analysis.

Flexible Budget Variance and Sales Volume Variance

The key to the decomposition of the total operating-income variance for a period is the introduction of a

flexible budget (FB) based on outputs (i.e., on actual unit sales). A first-level decomposition of the

“operating income variance” for a single-product firm results in a total flexible budget (FB) variance

and a sales volume variance. See text Exhibit 14.4.

A flexible budget (FB) based on output is developed using budgeted selling price per unit, budgeted

(standard) direct costs per unit, and budgeted total fixed costs for the actual output level achieved during

the period. Once this FB is determined, a first-level decomposition of the total operating income variance

can be performed. The sales volume variance is the difference between the master budget and the

flexible budget (FB) based on output. It measures the effects of changes in output on sale revenues,

expenses, contribution margins, and operating income. The total flexible-budget variance is the

difference between actual operating income of the period and the flexible budget based on output. It

measures the effects of efficiencies in using resources on expenses, contribution margins, and operating

income and the effects of changes in selling prices of output units on sales revenues and subsequent

effects on contribution margin and operating income. Together, the sales volume variance + the total

flexible budget variance = total operating income variance, as indicated below:

Actual Operating Flexible Budget Master

Income Based on Output (Static) Budget

Total Flexible-Budget Variance Sales Volume Variance

Standard Costs and Input Quantities

A standard cost is a measure of the cost that should be incurred to manufacture a product or provide a

service. Establishing a standard requires careful analysis of operations. A standard can be an ideal

standard or a currently attainable standard. An ideal standard demands perfect implementation and

14-4

Chapter 14 – Operational Performance Measurement: Sales, Direct Cost Variances, and the Role of Nonfinancial

Performance Indicators

maximum efficiency in every aspect of the operation and is not easily attainable. A currently attainable

standard sets the performance criterion at a level that workers with proper training and experience can

attain most of the time without extraordinary effort. An example of a standard cost sheet is provided in

Exhibit 14.5.

A firm can use activity analysis, historical data, benchmarks, market expectation, target cost, or strategic

decision to set the standards. Setting the standard using activity analyses requires analyses of all activities

required to complete a job, project, or operation. It is often expensive and time-consuming.

Benchmarking is the process of measuring products, services, and activities against the best performance.

Using benchmarking to set standard has the advantage of using the best performance anywhere as the

standard and help the firm to maintain its competitive edge. The target cost for a product is the cost that

will yield the desired profit margin, given the market price of the product.

The availability of standard cost (and revenue) information enables the managerial accountant to

breakdown the total flexible budget variance into its components: a total selling price variance and a

flexible budget variance for each cost, variable and fixed. The fixed cost variances are called “spending

variances.”

Further decomposition of the fixed cost variances would be to assign each spending variance to a

responsibility center (product, department, geographic region, manager, etc.). The series of variable cost

flexible budget variances can each be broken down into price (p) and quantity/efficiency (q) components,

as discussed below for direct labor and direct materials.

Direct Cost Variances: Materials and Labor

A manufacturing firm usually has a standard cost sheet that details the standard quantity and standard cost

for all the significant cost elements of the operations. Typical standards include standards for direct

materials (DM) and direct labor (DL). A DM flexible budget variance can be separated, for each material,

into a DM price and a DM usage variance. A DL flexible budget variance can be further divided into DL

rate and DL efficiency variances, by developing a second flexible budget, that is, one based on actual

resource inputs (actual units of material or actual labor hours worked). A diagrammatic representation of

the variance decomposition process for DM and DL costs follows (see Exhibit 14.7, Exhibit 14.8,

Exhibit 14.9, and Exhibit 14.10):

Direct Materials Variances

FB Based on Output

Actual FB Based on Inputs (Standard Quantity of DM Allowed for

Cost Incurred (Quantity Used × Standard Cost) Output Achieved × Standard Cost)

(AQ × AP) (AQ × SP) (SQ × SP)

Price Variance Usage Variance1

NOTE: If the company calculates the DM price variance at point of purchase, this variance is referred to

as the direct materials purchase price variance. When this is the case, then AQ in the price variance

formula refers to the Actual Quantity purchased. For the usage (efficiency) variance calculation, AQ

stands for Actual Quantity issued to (consumed in) production.

If the price variance for materials is not calculated until the materials are issued to production, then AQ in

the above diagram stands in all cases for Actual Quantity used (issued to production) during the period.

1 If there are multiple labor classes (categories) that are substitutable, then it is possible to break the direct labor

efficiency (quantity) variance into a direct labor mix variance and a direct labor mix variance. As noted below, if

there are multiple direct materials, and these materials are substitutable, then the direct materials quantity variance

can similarly be broken down into a mix variance and a yield variance.

14-5

Education.

Chapter 14 – Operational Performance Measurement: Sales, Direct Cost Variances, and the Role of Nonfinancial

Performance Indicators

Direct Labor Variances

FB Based on Output

Actual FB Based on Inputs (Standard DLHs Allowed for the

Cost Incurred Actual Hours x Standard Hourly Rate Output x Standard Hourly Rate)

(AH × AR) (AH × SR) (SH × SR)

Rate Variance Efficiency Variance

Standard Setting

At this point, the instructor can provide a more detailed explanation of the standard-setting process—that

is, the choices that need to be made and the technical details regarding standard costs.

Cost and Asset Flows and Journal Entries

I find it helpful to start this material with a discussion of the difference between standard costs and the use

of a standard cost system. I then transition to a discussion of the “big picture” or framework presented as

Exhibit 14.12.

For companies using a standard cost system and recognizing the materials price variance at point of

purchase, the raw materials inventory account debited (charged) for materials purchased during the

period. Any difference between the standard cost of items purchased and the actual price paid is recorded

in a separate “materials purchase price variance” account. Standard usage of raw materials (based on

output produced) at standard cost is charged to the Work-in-Process (WIP) Inventory account. Any

difference is charged to the “materials usage variance” account.

Direct labor is also charged to production (work in process) at standard rates for the standard allowed

hours for the units manufactured. The effect of paying a non-standard wage rate for the period is recorded

in a separate “direct labor rate variance” account while the effect of using a non-standard amount of labor

hours to produce the current period’s output is recorded in a separate “direct labor efficiency variance”

account.

The standard cost of units completed is transferred from the WIP Inventory account to the Finished Goods

Inventory account. Units sold are cleared from the Finished Goods Inventory account and charged to Cost

of Goods Sold (CGS)–again at standard manufacturing cost.

For those instructors covering journal entries, the discussion can conclude with an examination of the T–

accounts presented in Exhibit 14.13.

Limitations of Standard Costing and Short-Term Financial Performance Indicators

Standard cost variances are often reported to managers too late for them to take timely corrective

action.

Direct Labor (DL) has become less significant and tends to be more fixed than variable. A focus

on labor efficiency variances tends to encourage production of excess inventories (counter to, say,

a JIT philosophy).

A key objective in the new manufacturing environment is to increase quality. An overemphasis on

cost may result in lower quality. For example, focusing on the materials price variance may result

in the purchase of low quality materials.

14-6

Chapter 14 – Operational Performance Measurement: Sales, Direct Cost Variances, and the Role of Nonfinancial

Performance Indicators

Competitive conditions often require continuous improvement; attaining preset standards isn’t

sufficient.

The need to identify basic business processes and how such processes are most effectively

“controlled.”

Nonfinancial performance indicators are needed to supplement financial performance indicators.

The move to JIT can be used as a specific example of an operating process decision. Associated

with this process is the need to monitor and report key performance indicators, such as Customer

Response Time (CRT) and Process Cycle Efficiency (PCE), both of which are nonfinancial in

nature but strategically important from a control/performance reporting perspective.

Breakdown of Material and Labor Quantity (Efficiency) Variance

As noted above, if resource inputs (labor and materials) are substitutable, then cost efficiencies can be

achieved either by (1) using a less expensive mix of materials to produce a given level of output, or (2)

using less material (in total) to achieve that level of output. These two elements refer, respectively, to the

materials mix variance and the materials yield variance. When added together, these two variances equal

the sum of efficiency (usage) variance for all direct materials, calculated individually using the procedure

depicted in Exhibit 14.9. To break down the total materials quantity (usage) variance into mix and yield

components, we expand Exhibit 14.9 as follows:

1. The exhibit must be expanded to include (in a single exhibit) all substitutable materials

2. Existing column (2) is expanded to represent, for each direct material, the product of the actual

3. Existing column (3) is expanded to represent, for each direct material, the product of the standard

total quantity of all direct materials that should have been used during the period by the standard

input mix percentage for the direct material and by the standard cost per unit of the material

The difference between the total of column (2) and column (3) is the total materials usage (quantity)

variance. This variance can be broken down by inserting a new column (call it 2’) between the two, as

follows:

For each direct material, take the product of the actual total quantity of all direct materials used

during the period (same number used in revised column 2) multiplied by the standard input mix

percentage for the direct material and by the standard cost per unit of the material.

The difference between the total of column 2 and the total of column 3 is the total materials usage

(quantity) variance for the period. The difference between column and column 2’ is the materials mix

variance, while the difference between column 2’ and column 3 is the materials yield variance.

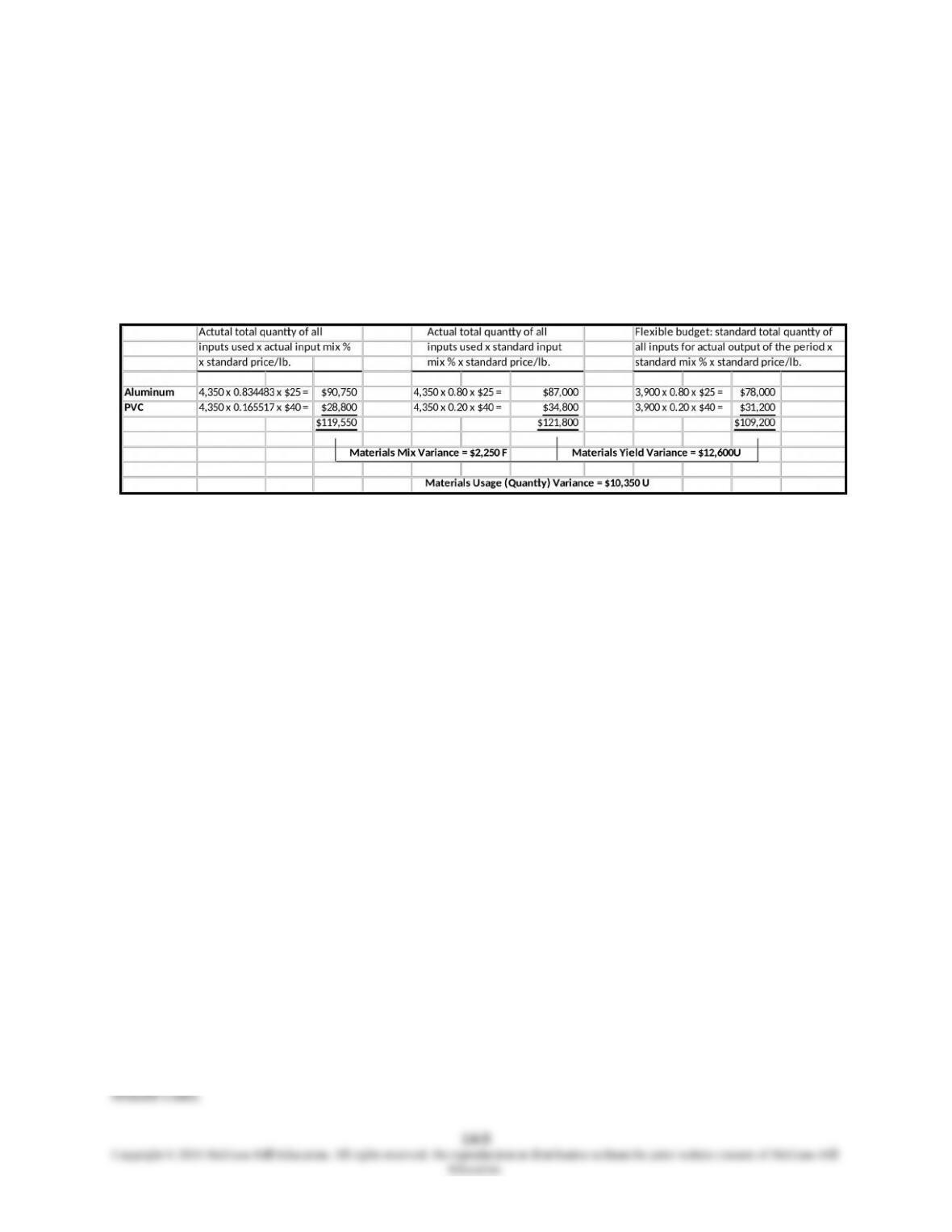

Example: Consider, for example, the direct materials information presented in text Exhibit 14.8. Assume

that management of Schmidt Machinery Company has some latitude in substituting aluminum and PVC.

As indicated in Exhibit 14.5, the standard mix of aluminum to PVC is 4:1 (i.e., 80%:20%). In Exhibit

14.8 we see that during October the actual direct materials mix was 83.4483%:16.5517% (i.e., 3,630

pounds:720 pounds). Total actual pounds of direct materials used = 3,630 + 720 = 4,350. Actual units

produced in October = 780. Total direct material units that should have been used (at standard) to produce

780 units = 5 lbs./unit x 780 units = 3,900 lbs.

14-7

Chapter 14 – Operational Performance Measurement: Sales, Direct Cost Variances, and the Role of Nonfinancial

Performance Indicators

As shown by the calculations below, the total direct materials usage (quantity) variance for October was

$10,350U. This total variance is explained by a favorable mix variance ($2,250) and an unfavorable yield

variance ($12,600). The mix variance is favorable because the units produced this period (780) used a

greater percentage of the less expensive raw material, aluminum. On the other hand, this shift to the

lower-cost material seems to have required total direct material inputs (4,350 lbs.) much higher than

should have been the case (3,900 lbs.).

Schmidt Machinery Company

October 2016

Materials Usage Variance and Breakdown into Mix and Yield Components

Economic Order Quantity (EOQ)

In most cases, students cover this material in an operations management (or, production & operations

management) class they take as part of the requirements for an accounting major. This is not universal,

however. Therefore, in the space below we present a discussion of EOQ, which the instructor can choose

to use in conjunction with Chapter 14.

As implied by its name, the EOQ model specifies the optimal order size, based on two key assumptions:

1. Demand for (and therefore use of) items ordered is fairly uniform throughout the year

2. Each new order is delivered in full when the inventory level reaches zero

In the basic EOQ model, total annual cost of stocking a given inventory item is equal to the sum of the

total purchase price of the item, plus the cost of ordering (assumed a batch-level cost, that is, fixed in

terms of order size), plus the cost of holding (carrying) the item in inventory. If we let D = annual demand

for the item, C = purchase price per unit, S = cost of placing an order, i = the cost of holding one unit in

inventory for one year (expressed as a percentage of C), and Q = order size (i.e., amount ordered each

time an order is placed), then the total annual cost of inventory (including cost of the item, holding costs,

plus ordering costs) can be written as:

TC = DC + (D/Q)S + (Q/2)Ci

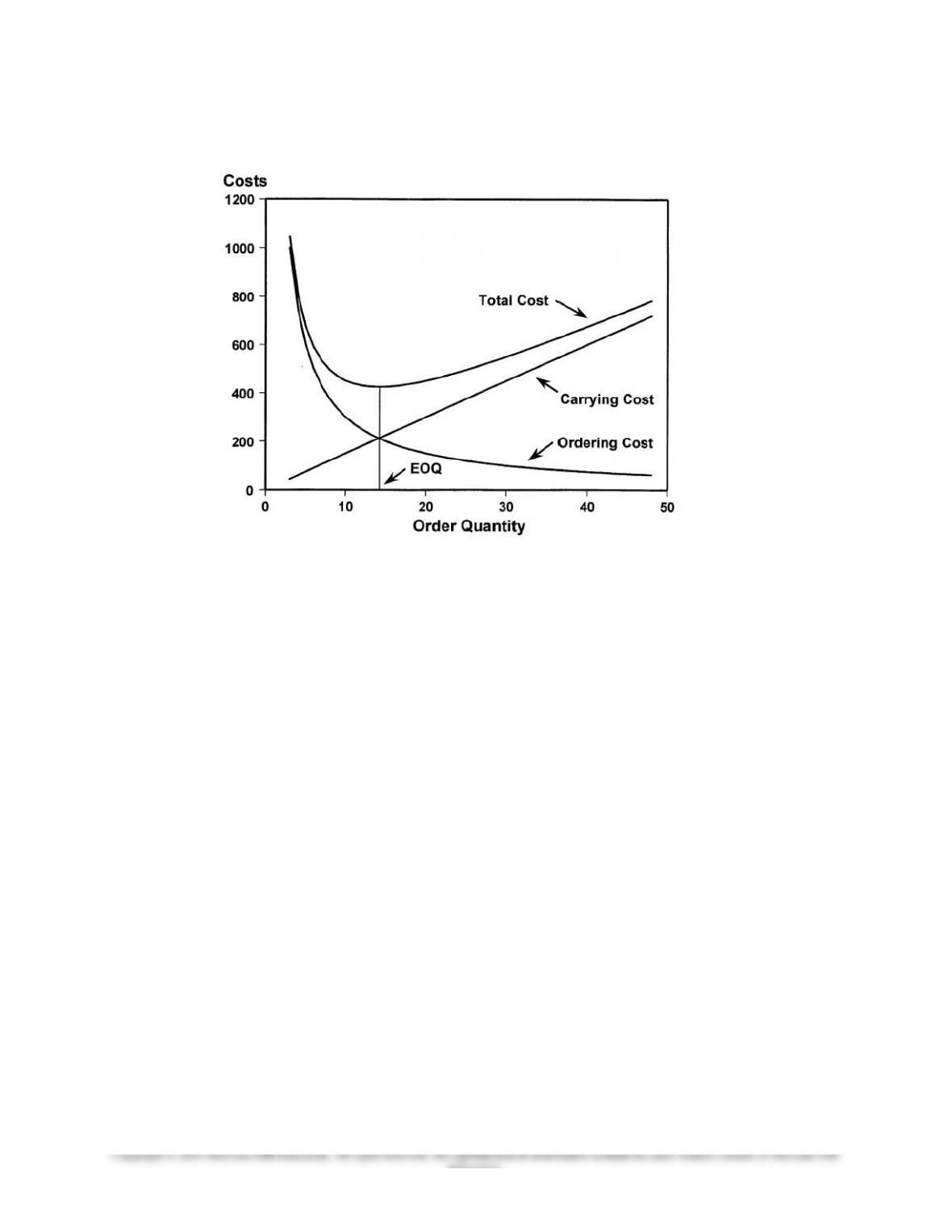

Figure A below depicts, for a hypothetical example, alternative ordering strategies (order sizes) and the

resulting impact on total inventory-related cost (TC) as well as component costs, (D/Q)S and (Q/2)Ci

(with assumed uniform inventory usage, the average inventory held during a period = Q/2). Thus, the key

issue is determining the optimal order size for the inventory item in question. Note that as the order size

increases, annual ordering costs ((D/Q)S) decrease while annual holding costs ((Q/2)Ci) increase. The

goal is to minimize TC, that is, the goal is to choose an order size (Q) that minimizes total inventory-

Chapter 14 – Operational Performance Measurement: Sales, Direct Cost Variances, and the Role of Nonfinancial

Performance Indicators

Figure A: Relationship between Order Size (Quantity), Annual Carrying Cost, Annual Ordering

Cost, and Total Inventory-Related Cost

One approach to determining the optimal order size (EOQ) is to use the Solver routine in Excel (note,

however, that because the underlying model—as shown above in Figure A—is nonlinear, you should not

chose Linear optimization under Solver). As depicted in Figure A, EOQ (given the preceding

assumptions) will occur when Inventory Carrying Costs and Inventory Holding Costs are in balance (15

units in the given example).

For a concrete example of determining EOQ, assume the following:

D = 24,000 units (annual demand)

C = $35 per unit (inventory purchase price)

S = $50 (the cost of placing an order)

i = 18% (inventory holding cost, expressed as a percentage of inventory cost)

Using Solver, we find that EOQ = 617.21 units. This would result in a total purchase cost of $840,000

(24,000 × $35/unit), annual ordering cost of $1,944, and an annual inventory holding cost of $1,944. Total

Cost (TC) under this ordering plan = $843,888.

As an alternative to using the Solver routine in Excel, we could use the following formula to determine

the EOQ:

In the preceding example, we have the following inputs:

2DS = 2 × 24,000 × $50 = $2,400,000

Ci = $35/unit × 0.18 = $6.3

14-9

Education.

Chapter 14 – Operational Performance Measurement: Sales, Direct Cost Variances, and the Role of Nonfinancial

Performance Indicators

Thus,

EOQ = = 617.214

Finally, it is worth emphasizing to students that the basic EOQ model can be extended to address

important “real-world” extensions, such as the existence of quantity discounts or storage space (or

financial) restrictions that might exist.

14-10

Education.