Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

11-36 Make or Buy (45-60 min)

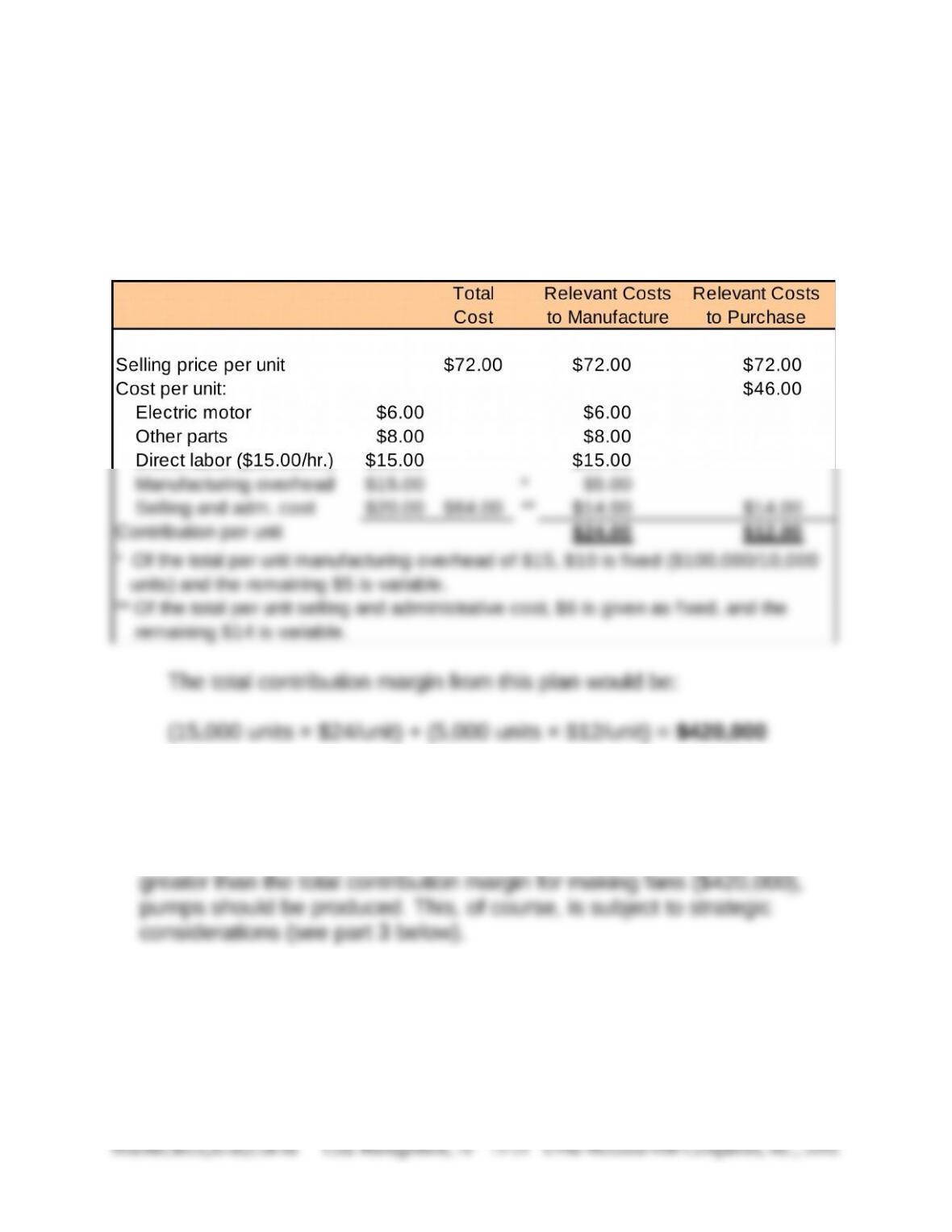

1. Since the per-unit contribution margin for manufactured fans ($24) is

higher than for purchased fans ($12), the company should manufacture as

many fans as possible (15,000), and purchase the remainder (5,000) from

Harris Products.

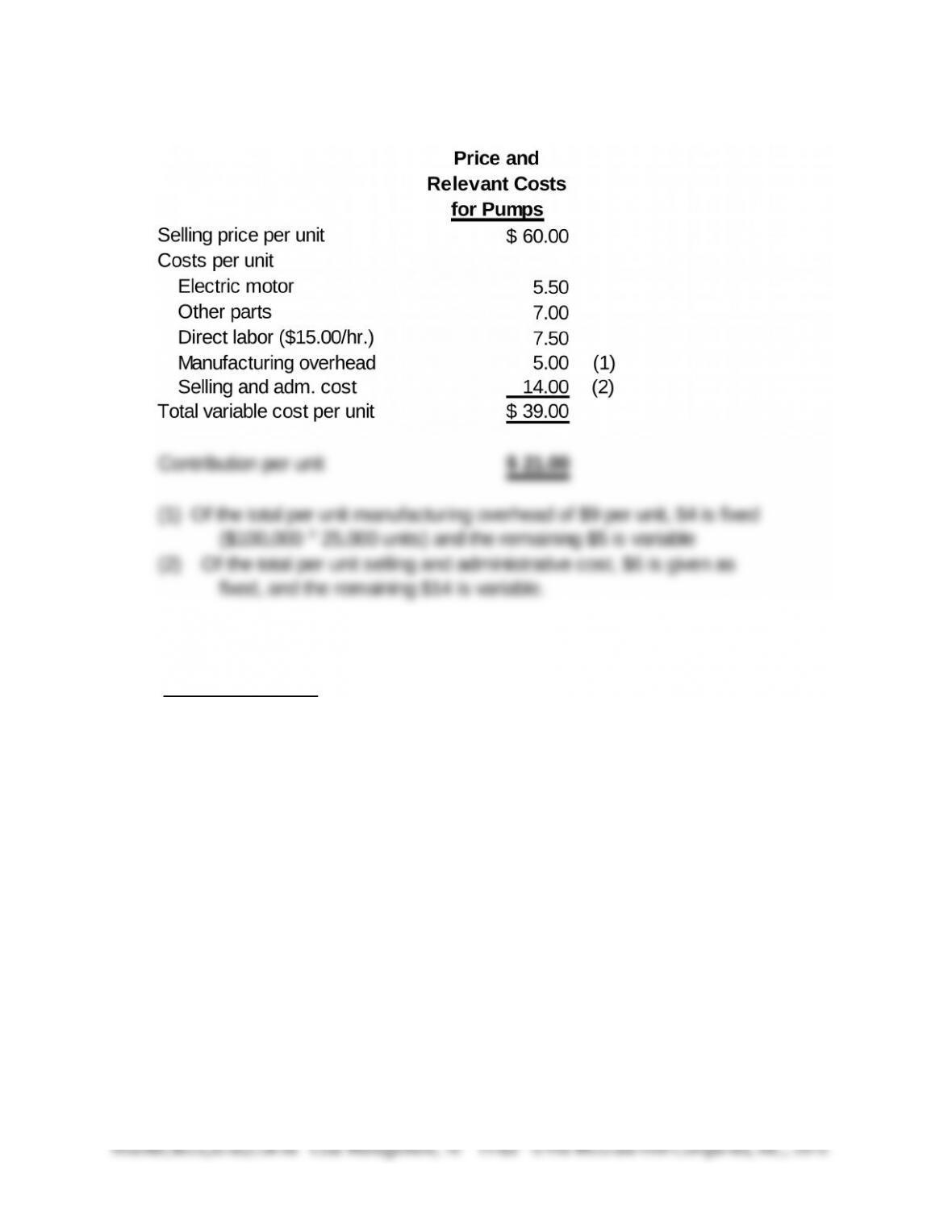

2. The total contribution margin for the marine pumps = $21 per unit ×

25,000 units = $525,000

Since the total contribution margin from making pumps ($525,000) is

11-36 (Continued-1)

3. Some of the possible strategic factors to consider are:

Re: The pumps:

Will the sale of pumps introduce Martens to new markets and new

customers that might benefit other product lines?

Can Martens compete in the marine pump market? How

competitive is this market, and what are the critical success factors

that are likely to lead to success for Martens?

How reliable are the estimates used to develop the predictions for

revenues and costs for the pumps? How reliable is the market

research that predicted growth in pump sales?

Will the sale of pumps affect Martens’ image in either a positive or

negative fashion? For example, will Martens’ current customers

view Martens as a high quality/innovative manufacturer of pumps?

How long is the expected growth in pump sales expected to

continue?

11-36 (Continued-2)

Re: The purchase of attic fans from Harris Products:

What are the alternative uses of Martens’ production capacity, in

addition to pumps and attic fans that might produce higher

contribution?

How reliable is Martens’ information that Harris is a reliable producer

of quality products?

How will Martens’ customers react, if at all, to know that the attic fans

are not manufactured by Martens?

11-37 Make or Buy; Strategy; Ethics (45-50 min)

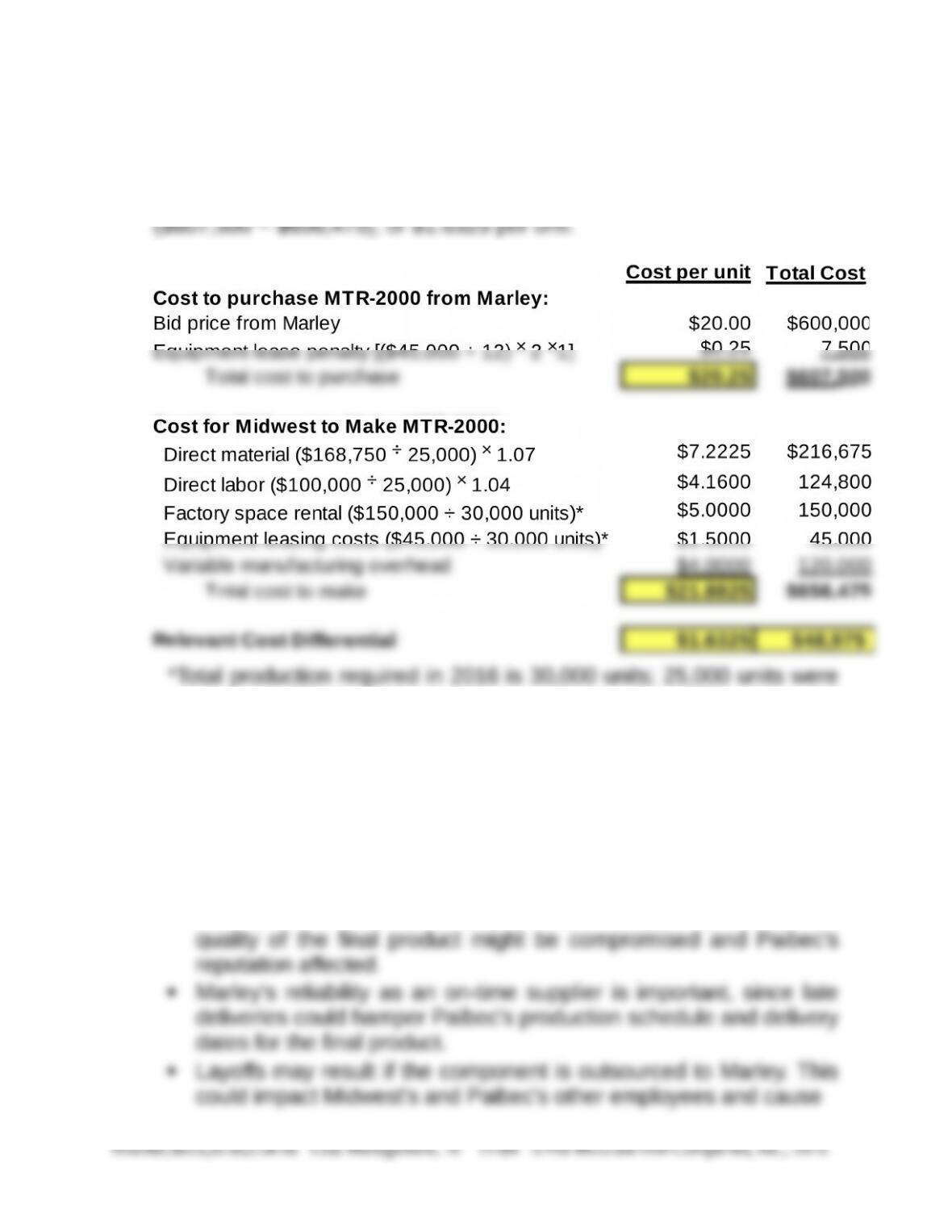

1. An analysis of per unit and total costs for 30,000 units shows that the

Midwest Division should purchase the parts for a savings of $48,975

produced in 2015. Unit variable costs are based on 2015 costs and

units; fixed costs in total are expected to be the same in 2016 as they

were in 2015.

2. Strategic factors that the Midwest Division and Paibec Corporation

should consider before agreeing to purchase MTR-2000 from Marley

Company include the following:

The quality of the Marley component should be equal to, or better

than, the quality of the internally made component, or else the

11-37 (continued-1)

3. Referring to the specific standards for ethical practice by a

management accountant (http://www.imanet.org/PDFs/Statement

%20of%20Ethics_web.pdf ) , Lynn Hardt should consider the ethical

standards of competence, integrity, and objectivity:

Competence

Prepare complete and clear reports and recommendations after

appropriate analysis of relevant and reliable information. John has

asked Lynn to adjust and falsify her report and leave out some

manufacturing overhead costs.

Integrity

Refrain from either actively or passively subverting the attainment

of the organization's legitimate and ethical objectives, Paibec has

a legitimate objective of trying to obtain the component at the

Credibility

Communicate information fairly and objectively. Hardt needs to

perform an objective make-or-buy analysis and communicate the

results objectively.

11-37 (continued-2)

Disclose all relevant information that could reasonably be

expected to influence an intended user’s understanding of the

reports, comments, and recommendations presented. Hardt needs

to fully disclose the analysis and the expected cost increases.

11-38 Outsourcing Call Centers (40-45 min)

1. The corporate overhead cost is irrelevant since in total it will not

change whether or not the call center is returned to Atlanta (i.e., it is

not an avoidable cost).

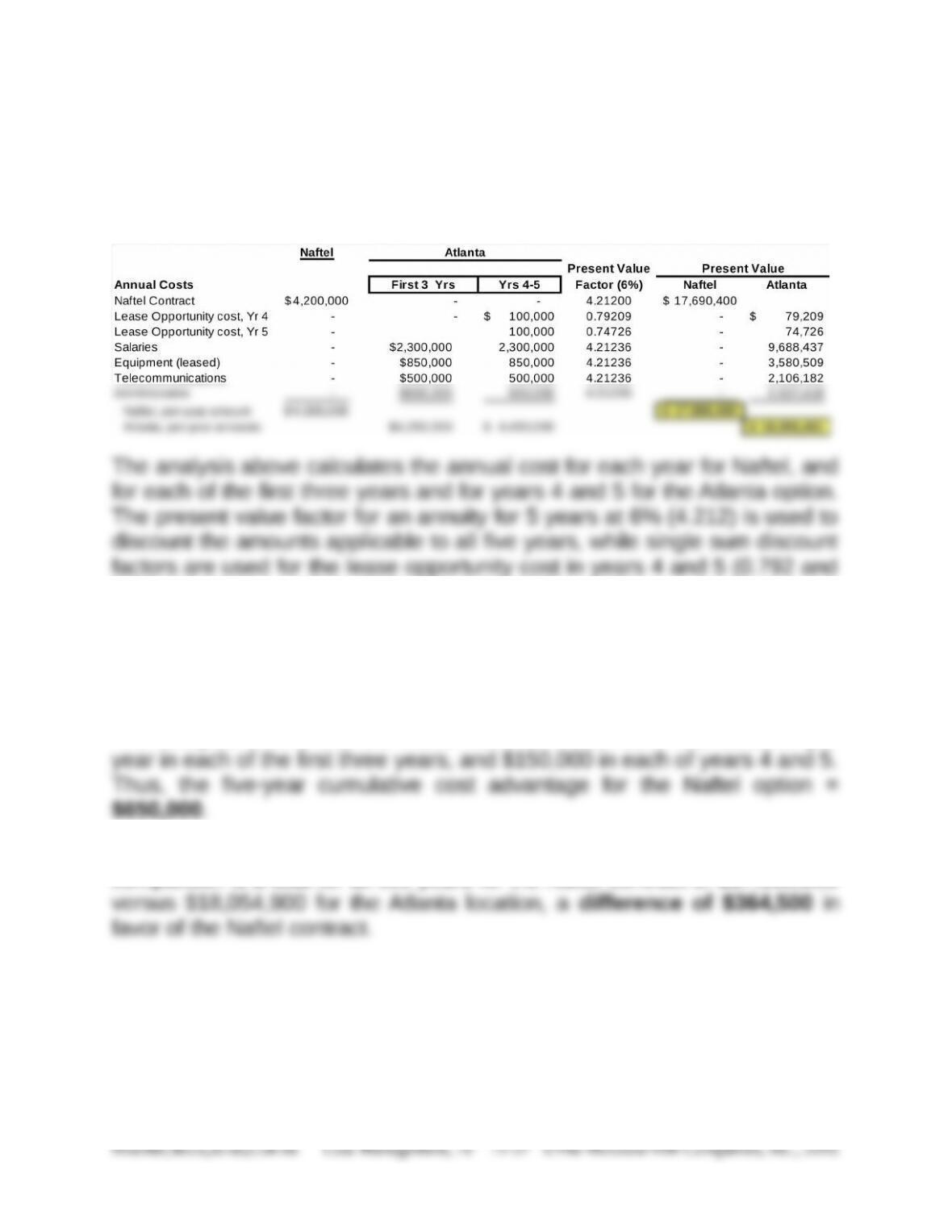

0.747 for Year 4 and Year 5, respectively). The present value tables are

located at the end of Chapter 12. (NOTE: the results reported above are

based on exact present-value factors; if the factors from the text, which are

rounded, are used, the answer will be slightly different from that presented

above.)

The analysis shows that the Naftel contract would save MB $50,000 per

When analyzed on a present value basis (@ a 6% discount rate), the

comparison is a total for all five years for the Naftel contract of $17,690,000

Whether you consider the undiscounted or the present-value analysis, it is

clear that the Naftel contract has the lower cost. But, the difference is not

great relative to total cost, so that strategic issues are important in making

the final decision. Some of these strategic issues are discussed in parts 2

and 3 below. In addition:

11-38 (continued)

Since customer service is very important for MB’s success,

would the location of the call center in Atlanta or at Naftel provide

the better quality of customer service? This is the dominant

strategic question, especially since the cost difference is not

significant relative to total cost.

Since the banking business was (at the time of the decision)

forecast to be in troubled times for the next several months,

would it not be important to retain the admittedly small cost

advantage of the Naftel contract?

Given the difficult times predicted (at the time) for the banking

industry, would it not have been especially important to

differentiate the company from others? Customer service is one

important way to do that. If customer service in Atlanta could be

carefully managed so that it provides very high quality service,

this could be an important competitive advantage.

2. At the time of the decision (late 2008), the value of the dollar had

been increasing relative to most other currencies. This means that

the cost to MB of the service by Naftel would decrease in currency-

adjusted terms if the contract is in India’s currency, the Rupee. Other

3. The ethical issues in the decision here include the consideration of a

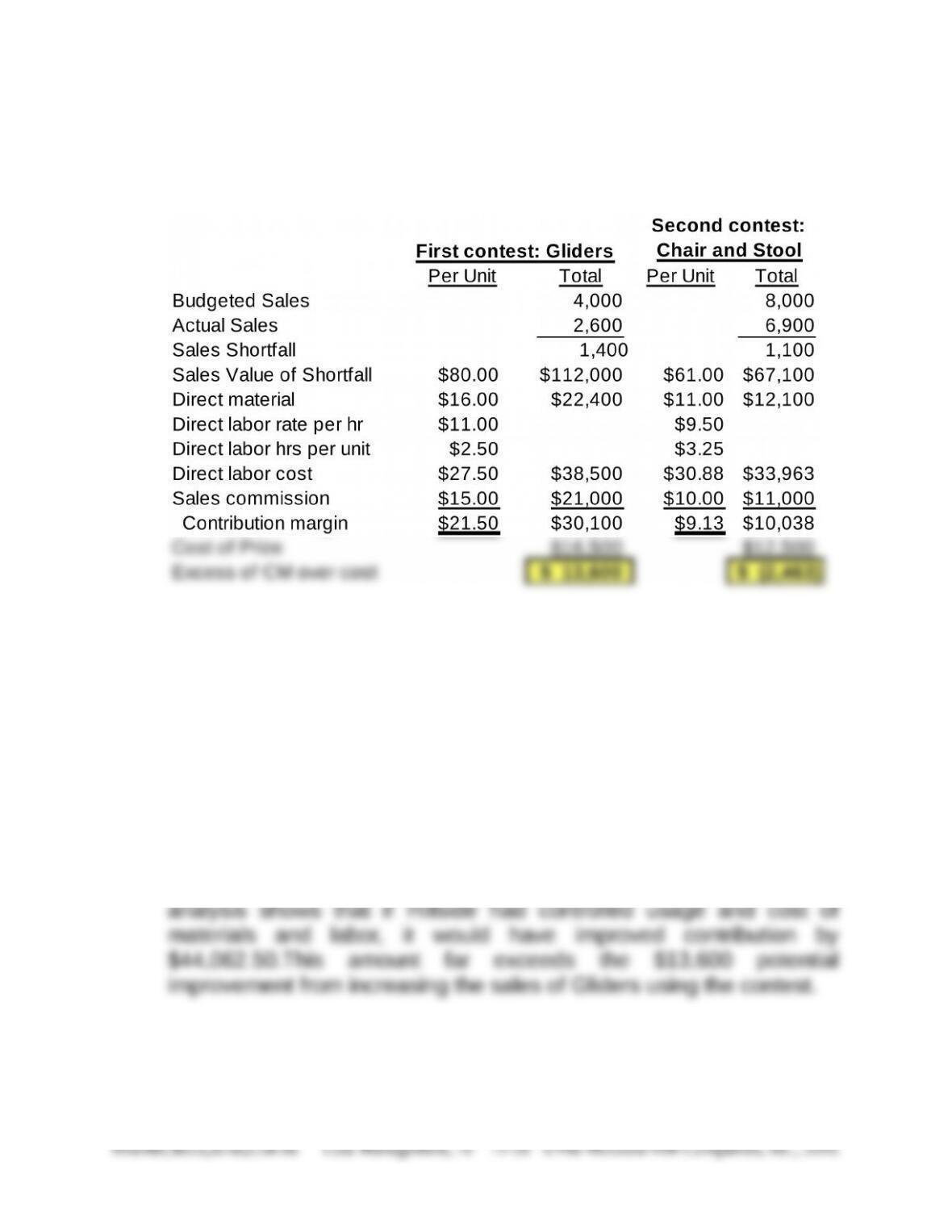

11-39 Project Analysis: Sales Promotions (60 min)

1. The relevant cost analysis follows:

The Glider contest has a $13,600 positive contribution margin net of

the estimated cost of the prize. On the other hand, the Chair-and-

Stool Set contest has a negative contribution of $2,463. Note that the

above solution uses actual rather than budgeted price and cost

information.

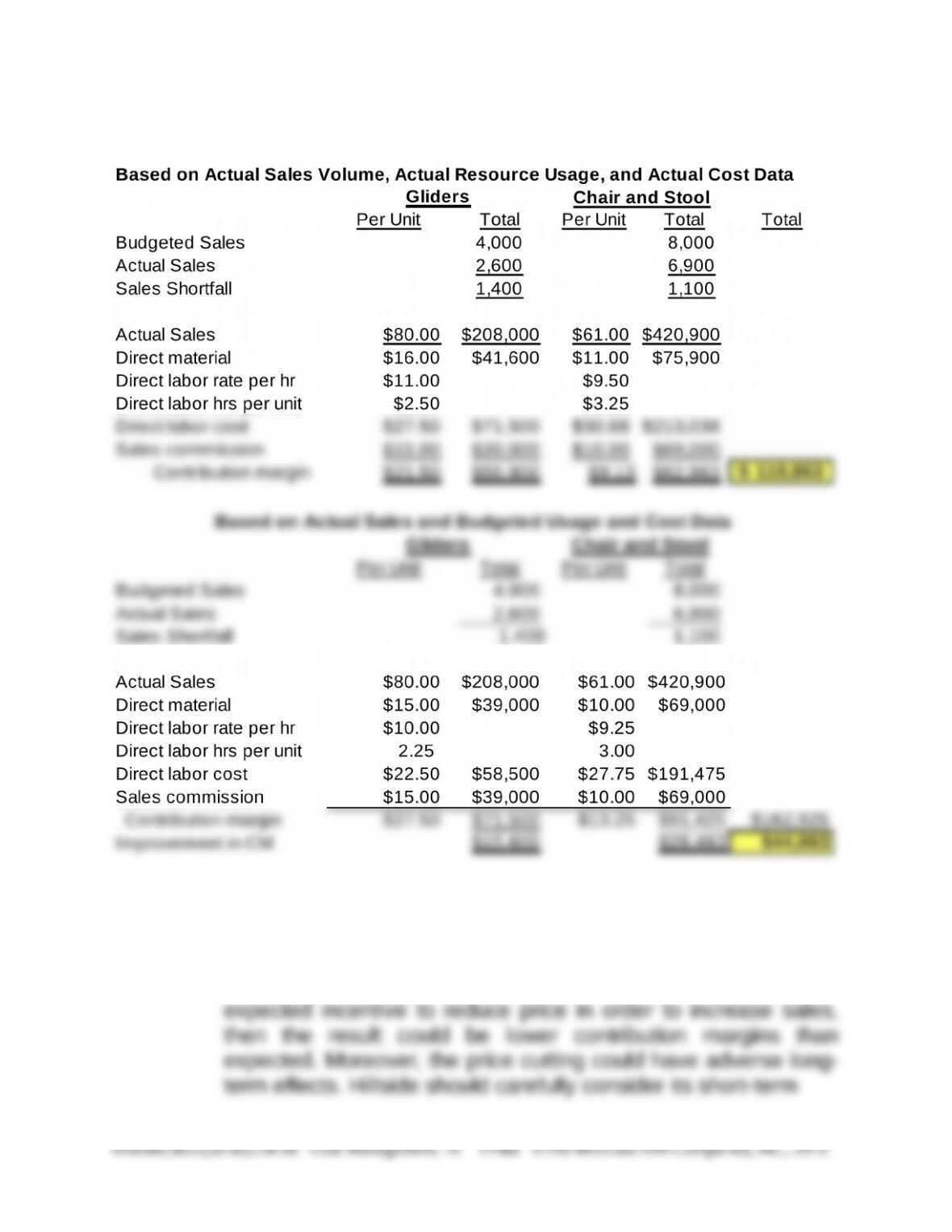

The analysis below compares the contribution margin for each

product based on actual sales volume at actual cost, actual

selling price, and actual resource usage to the product contribution

margins based on actual sales volume at budgeted cost,

budgeted selling price, and budgeted resource usage. The

Thus, strategically, it is important for Hillside to focus on cost

management as well as improving sales.

11-39 (continued-1)

2. Some strategic factors that should be considered:

The contest appears to reward an increase of sales in units.

However, the average sales price for each product has already

fallen below budgeted levels. If the contest provides an