Chapter 19 – Strategic Performance Measurement—Investment Centers

CHAPTER 19: STRATEGIC PERFORMANCE MEASUREMENT—

INVESTMENT CENTERS

QUESTIONS

19-1 Investment centers are commonly used when there are a number of business

units to be compared, and/or when top management intends to evaluate the

economic performance of the business unit relative to alternative investments. By

definition, managers of these business units exercise control over revenues,

amount of profit divided by the amount invested in the business unit.

19-2 Return on investment (ROI) is the ratio of some measure of “profit” to some

19-3 The primary measurement issues for ROI are:

1. The effect of accounting policies, which affect the determination of “income.”

2. Other measurement issues for income, which include the handling of non-

19-4 The primary advantages of using return on investment (ROI) as a performance

indicator are:

The primary limitations of return on investment (ROI) as a performance indicator

are:

1. It has an excessive short-term focus.

19-1

Education.

Chapter 19 – Strategic Performance Measurement—Investment Centers

19-5 We can enhance the ROI measure’s usefulness by making it the product of two

ratios:

ROI = (Profit ÷ Sales) × (Sales ÷ Assets)

“operating profit.” For the company as a whole, “profit” can be defined as “net

income.”

Asset turnover, the amount of sales achieved per dollar of investment, measures

the manager’s ability to manage both sales and assets, that is, to produce

increased sales from a given level of investment in assets. Together, the two

components of ROI tell a more complete story of the manager’s performance and

enhance top management’s ability to evaluate and compare the different units.

19-6 The key advantage of residual income (RI) is that it deals effectively with the

limitation of ROI: ROI has a disincentive for the managers of the most profitable

units to make new investments. With residual income, no matter how profitable

the unit, there is still an incentive for new profitable investment. In contrast, a key

19-7 Economic value added (EVA®) is a profitability measure that approximates the

“economic earnings” of an investment center. Operationally, we define EVA® as

business unit’s income after-tax cash earnings and after deducting an imputed

Thus, RI and EVA® are similar in form but are strikingly different in terms of

measurement. Thus, the overall objective of EVA® is to provide an estimate of

the value added to (or destroyed by) each strategic investment unit during a

19-2

Education.

Chapter 19 – Strategic Performance Measurement—Investment Centers

given period. As such, EVA® is one approach to what we call “Value-Based

Management.”

19-8 The three most widely accepted methods are: (1) the comparable uncontrolled

price method, (2) the resale price method, and (3) the cost-plus method. The

profit percentage determined from comparison of sales of the seller to unrelated

parties, or sales of unrelated parties to other unrelated parties.

19-9 The “arm’s-length” standard says that transfer prices should be set so they reflect

the price that would have been set by unrelated parties acting independently. It is

19-10 Expropriation happens when a foreign government takes ownership and control

of assets the domestic investor has invested in that country. When there is a

significant risk of expropriation, the domestic firm can take appropriate actions

19-3

Education.

Chapter 19 – Strategic Performance Measurement—Investment Centers

BRIEF EXERCISES

19-11 ROI = Return on Sales × Asset Turnover

19-12 ROI = (Profit ÷ Sales) × (Sales ÷ Assets)

19-13

Return on Sales (ROS) = Profit ÷ Sales

Asset Turnover (AT) = Sales ÷ Assets

Return on Investment (ROI) = Profit ÷ Assets

19-14

NBV ROI = Profit ÷ NBV of Assets

= 5%

19-15 ROI = Return on sales (ROS) × Asset Turnover (AT)

19-4

Education.

Chapter 19 – Strategic Performance Measurement—Investment Centers

19-16 Mattress Sets:

ROI = (Operating Profit ÷ Sales) × (Sales ÷ Assets)

Bed Frames:

ROI = (Operating Profit ÷ Sales) × (Sales ÷ Assets)

19-17 Return on Sales (ROS) = Operating Profit ÷ Sales

19-18 Residual Income (RI) = Income − (Required Rate of Return × NBV of average

assets)

19-19 Residual Income (RI) = Income – (Required Rate of Return × NBV of average

assets)

19-5

Education.

Chapter 19 – Strategic Performance Measurement—Investment Centers

19-20 Residual Income (RI) = Income – (Required rate of return × NBV of assets)

19-6

Education.

Chapter 19 – Strategic Performance Measurement—Investment Centers

EXERCISES

19-21 Return on Investment (ROI); Comparison of Three Investment

Centers (Divisions) (15 minutes)

Answers shown in bold:

X Y Z

Sales $1,500,000 $750,000 $3,750,000i

Income $150,000 $75,000 $18,750h

Investment (assets) $600,000 $7,500,000d$2,500,000

Calculations:

aROS = Income ÷ Sales = $150,000 ÷ $1,500,000 = 10%

bAT = Sales ÷ Investment (assets) = $1,500,000 ÷ $600,000 = 2.5

cROI = ROS × AT = 10% × 2.5 = 25.00%

dInvestment (assets) = Income ÷ ROI = $75,000 ÷ 0.01 = $7,500,000

eROS = Income ÷ Sales = $75,000 ÷ $750,000 = 10%

19-7

Education.

Chapter 19 – Strategic Performance Measurement—Investment Centers

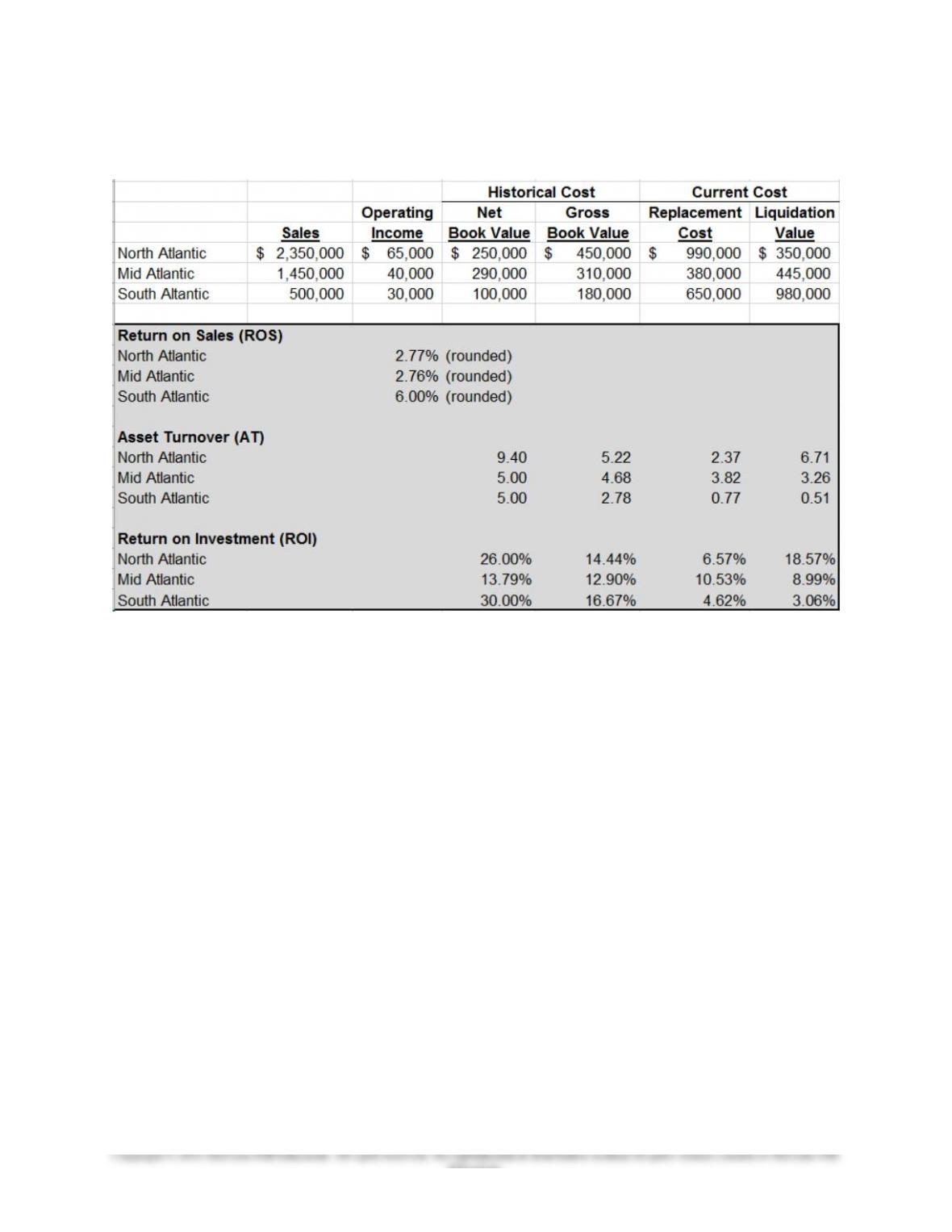

19-22 Return on Investment (ROI); Different Measures for Total Assets;

Spreadsheet Analysis (25 minutes)

Note:

Return on Sales (ROS) = Operating Income ÷ Sales

Asset Turnover (AT) = Sales ÷ Assets

Return on Investment (ROI) = ROS × AT (or, Operating Income ÷ Assets)

19-8

Education.

Chapter 19 – Strategic Performance Measurement—Investment Centers

19-23 Return on Investment (ROI); Return on Sales (ROS) and Asset

Turnover (AT) (25 minutes)

Revenue 2016 2017 2018

Southwest $ 14,900 $ 22,000 $ 26,000

Midwest 6,700 7,000 7,200

Southeast 12,400 13,000 13,300

Total $ 34,000 $ 42,000 $ 46,500

Net Operating Income

Southwest $ 1,100 $ 1,200 $ 1,350

Midwest 1,250 1,600 1,550

Southeast 1,000 1,200 1,600

Total $ 3,350 $ 4,000 $ 4,500

Average Total Assets

Southwest $ 14,000 $ 14,200 $ 16,800

Midwest 4,700 4,200 4,200

Southeast 5,300 5,600 5,600

Total $24,000 $24,000 $26,600

Return on Sales (ROS)

Southwest 7.4% 5.5% 5.2%

Midwest 18.7% 22.9% 22.5%

Southeast 8.1% 9.2% 12.0%

Firm 9.9% 9.5% 9.7%

Asset Turnover (AT)

Southwest 1.064 1.549 1.548

Midwest 1.426 1.667 1.714

Southeast 2.340 2.321 2.375

Firm 1.417 1.750 1.748

Return on Investment (ROI)

Southwest 7.9% 8.5% 8.0%

Midwest 26.6% 38.1% 36.9%

Southeast 18.9% 21.4% 28.6%

Firm-wide 14.0% 16.7% 16.9%

19-9

Education.

Chapter 19 – Strategic Performance Measurement—Investment Centers

Ex. 19-23 (Continued)

Notes:

1. Return on Sales (ROS) = Net Operating Income ÷ Sales

2. Asset Turnover (AT) = Sales ÷ Average Total Assets

3. Return on Investment (ROI) = ROS × AT (or, Net Operating Income ÷

Average Total Assets)