Chapter 09 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-48 (Continued-4)

The above data table provides the results of a sensitivity analysis.

Specifically, we are looking at the sensitivity of the breakeven point to

the assumption regarding sales mix for the two products. Based on the

above results management will form a judgment as to the sensitivity of

the B/E point to changes in the sales mix. The greater the perceived

sensitivity, the greater the uncertainty in the calculations (and therefore

in the CVP model). Given greater uncertainty, management may invest

resources to provide a more refined estimate of sales mix.

6. Given the assumed sales mix (25%:75%), the required sales volume (in

total units) to generate a before-tax profit, πB, of $ 75,000 is 63,803 units

(rounded up):

Targeted before-tax profit target, πB = $75,000

Fixed Costs (F) = $378,000

7. Given the assumed sales mix, what is the required sales volume (in total

units) to generate an after-tax profit, πA, equal to 10% of sales dollars?

Let Q = the required sales volume (in units) to achieve the profit objective

πB= Total sales − Total variable cost − Total fixed cost (F)

9-48 (Continued-5)

9-70

Education.

Chapter 09 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

(0.10 × (sp/unit × Q)) ÷ (1 − t) = Total contribution margin − F

(0.10 × (sp/unit × Q)) ÷ (1 − t) = (cm per unit × Q) − F

(0.10 × $28.00/unit × Q) ÷ (1 − 0.30) = ($7.10 × Q) − $378,000

8. The point of this question is to get the students started thinking about the

competitive context in which the firm operates. There are many different

relevant points that could be made. If the discussion is slow to start, ask

them to think about what a firm like HPC must do to be competitive.

There are a number of critical success factors that are likely to be

important for both domestic and foreign subscriptions. These would

include quality of presentation and timeliness and accuracy of

information, as well as competitive price. However, other factors will differ

across countries. For example, in some countries the cost of distribution

including selling and handling costs are quite high, so that it is critical in

these countries to devise new ways to deliver the subscriptions profitably.

Other factors include changes in literacy rates, the business climate, and

investment opportunities in different countries.

9-71

Education.

Chapter 09 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-49 CVP Analysis; Strategy; Sensitivity Analysis (75-90 min)

1.

Current Proposed

Selling price per unit $600.00 $600.00

Less: variable cost per unit:

Materials and purchased parts 180.00 195.00

Direct labor 55.00 62.50

Variable overhead 70.00 80.00

Variable GSA per unit 25.00 25.00

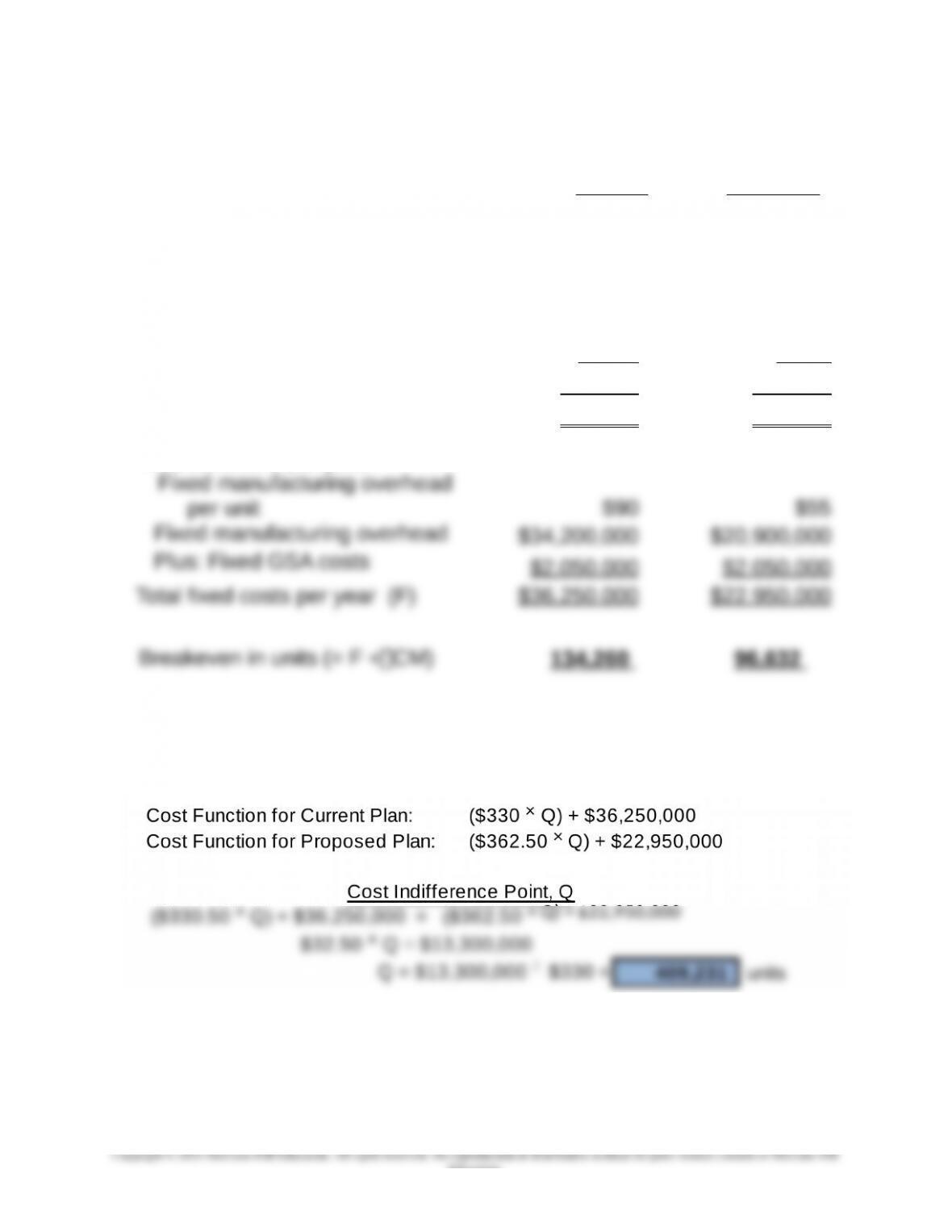

Total variable cost per unit $330.00 $362.50

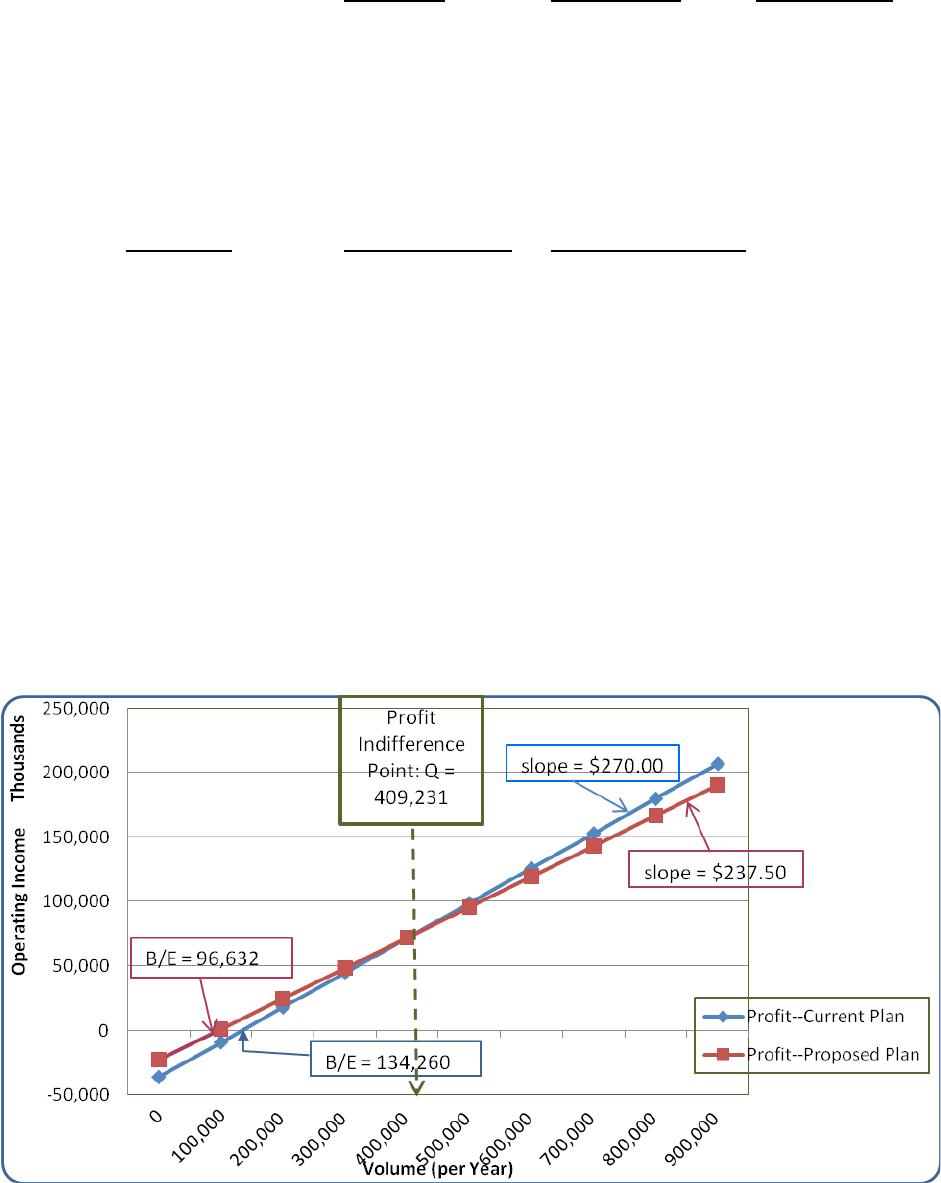

Contribution margin per unit (CM) $270.00 $237.50

Total fixed cost per year:

2. Indifference Point Calculation: the indifference point, in terms of cost, is

defined as the volume level (Q) in which total cost is the same for both

production options, as follows:

The above calculation shows that at the current level of 380,000 units,

the firm would prefer the low-fixed-cost strategy (i.e., the proposed

plan)

9-72

Education.

Chapter 09 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-49 (continued-1)

3. a) SolarFlex’s strategy is best described as differentiation, since the firm

has succeeded by innovation in product design. Further, the firm

operates in an industry in which innovation and product design are

critical to success. An important element of the firm’s strategy is also

the fact that the technology, as for many firms in the industry, is not

proven. That is, there is a significant level of risk that the firm’s

b) The calculations in part 2 above support a decision to go to the new

plan; at the current level of 380,000 units, costs are lower for the new

plan, and will continue to be lower for the new plan as long as volume

stays below 409,231 units.

Strategically, the new plan is preferred since it is an appropriate

response to the firm’s risk, as noted in part a above. By reducing

operating leverage (that is, by reducing manufacturing fixed costs

from $34,200,000 to $20,900,000) the firm is less exposed to a

possible failure of the innovation and then drop-off in sales. The

reduction in fixed costs also helps the firm to manage cash flows.

Thus, the new plan is more consistent with the firm’s strategy of

Sensitivity analysis. Since uncertainty is important in this case,

SolarFlex should use some of the tools as illustrated below. Note that

the proposed method is preferred if projected demand increases.

9-73

Chapter 09 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-49 (continued-3)

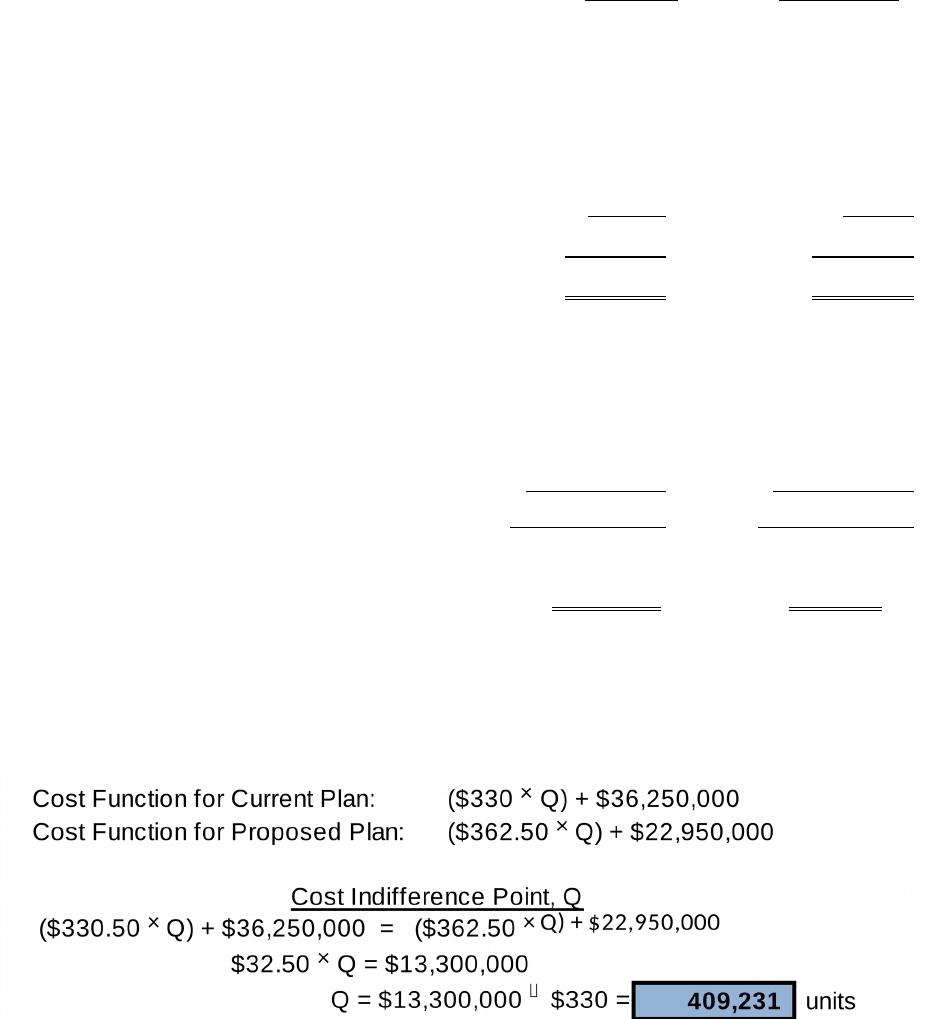

Current Proposed Difference

CM $270.00 $237.50 $32.50

Fixed Cost $36,250,000 $22,950,000 $13,300,000

Assumed Levels of

Demand Profit-Current Profit-Proposed

0 -36,250,000 -22,950,000

100,000 -9,250,000 800,000

200,000 17,750,000 24,550,000

300,000 44,750,000 48,300,000

400,000 71,750,000 72,050,000

500,000 98,750,000 95,800,000

4. Excel Charts (P-V function for each of the two decision alternatives)

9-74

Chapter 09 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-49 (continued-4)

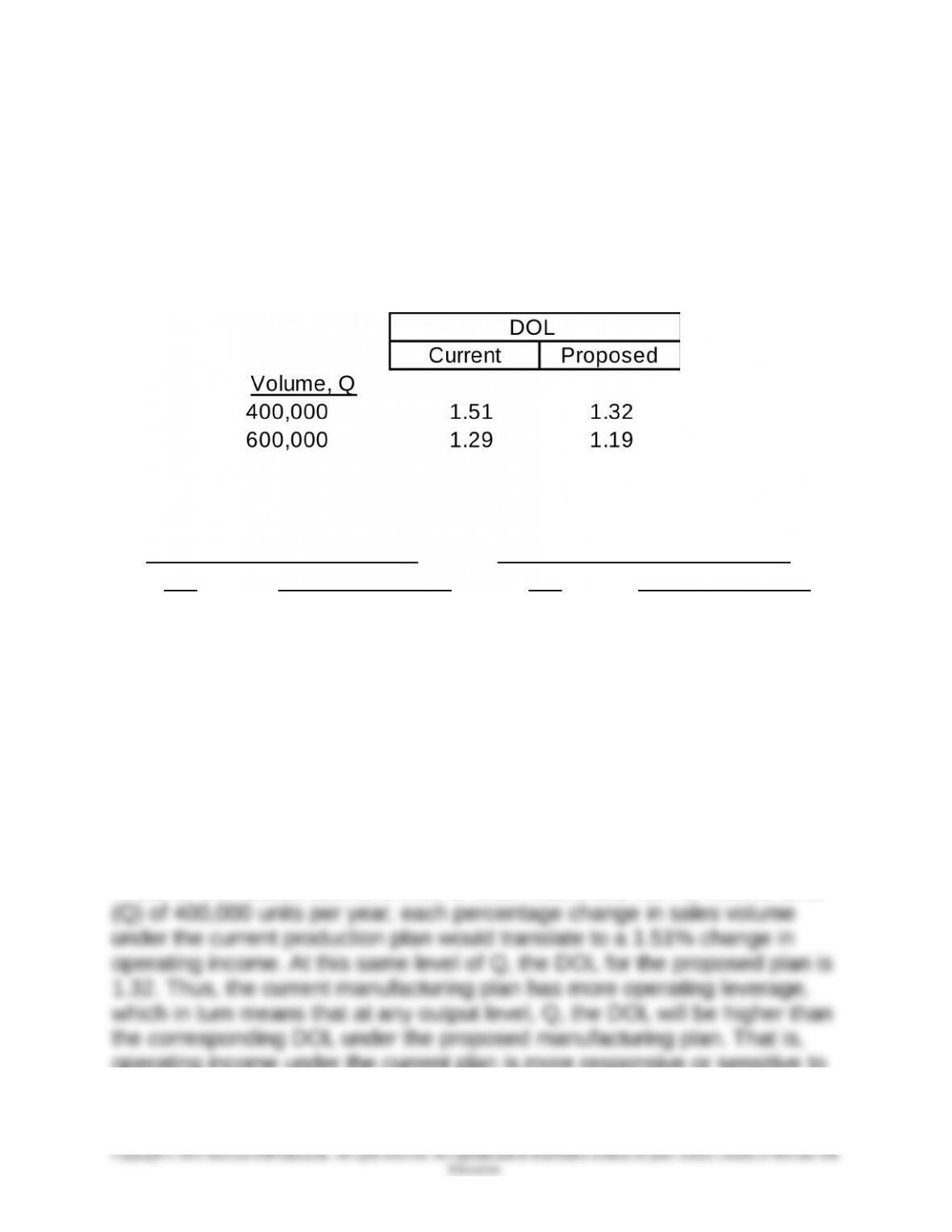

5. Calculation and interpretation of degree of operating leverage (DOL)

under each decision alternative at Q = 400,000 units and at Q = 600,000

units.

DOL, at any volume level, Q = CM ÷ Operating Income

Backup information for DOL calculations:

DOL Components (Current) DOL Components (Proposed)

CM Operating Income CM Operating Income

$108,000,000 $71,750,000 $95,000,000 $72,050,000

$162,000,000 $125,750,000 $142,500,000 $119,550,000

Operating leverage refers to the extent to which fixed costs characterize an

organization’s cost structure. The greater the fixed costs, the greater the

operating leverage and the more sensitive or responsive profits are to

changes in sales volume.

A measure of the extent to which profits vary in response to changes in

sales volume is the degree of operating leverage (DOL). DOL represents

the percentage change in operating profit per percentage change in sales.

Thus, for the results above, a DOL of 1.51 means that from a volume level

operating income under the current plan is more responsive or sensitive to

9-75

Chapter 09 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-49 (continued-5)

changes in sales volume. Relative to the proposed plan, the current plan

would generate greater percentage reductions in operating income if sales

volume declines, but greater percentage increases in operating income in

response to increases in sales volume. In this sense, the operating risk

associated with the current plan is greater than the operating risk

associated with the proposed plan.

9-76

Education.

Chapter 09 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

Problem 9-50: CVP Analysis; Sustainability; Uncertainty; Decision Tables

(60-75 min)

1. Lifetime cost functions: let Y = lifetime cost, and v = cost per gallon of

gas

Regular model:

Lifetime Cost (Y) = Fixed Cost + Variable Cost

Lifetime Cost (Y) = $17,000 + (2,608.7 gals. × v)

Hybrid model:

Lifetime Cost (Y) = Fixed Cost + Variable Cost

Lifetime Cost (Y) = $18,500 + (2,222.2 gals. × v)

2. Breakeven gas price (point of cost indifference): let “v” = breakeven price

per gallon

Lifetime Cost–Gas Model = Lifetime Cost–Hybrid Model

$17,000 + (2,608.7 gals. × v) = $18,500 + (2,222.2 gals. × v)

3. Graph of Lifetime Cost Function–Regular and Hybrid Models

X (price Lifetime Cost

per gal.) Gas Model Hybrid

$2.750 $24,174 $24,611

$3.000 $24,826 $25,167

9-77

Education.