Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Chapter 20 - Management Compensation, Business Analysis, and Business Valuation

20-35 (continued -1)

4. A down-side to the switch to IFRS is that companies will have to

study the IFRS carefully and determine for example whether the

company will use the “cost model” or the “revaluation model” for long-

lived assets, both of which models are permitted under IFRS. The

cost model is based on purchase cost less depreciation or

of accounting, it is likely that many U.S. companies will choose the

cost model.

5. Another down-side to the switch to IFRS is the period of training and

confusion that is likely to take place after the convergence. It will

take some time for financial staffs of the U.S. global corporations to

become proficient at the new accounting standards. Offsetting this

concern is that fact that the FASB and the IASB have in recent years

and to develop the required expertise for IFRS.

Useful reference:

IASB.org (http://www.ifrs.org/Home.htm)

20-21

Chapter 20 - Management Compensation, Business Analysis, and Business Valuation

20-36 Business Analysis (30 min)

The financial ratios are shown below:

First, the calculation of free cash flow.

Cash Flow From Operations 2016 2015

Net Income $ 325,000 $ 357,500

Plus Depreciation Expense 60,000 50,000

+Decrease (-inc) in AccRec and Inv (135,000) —

+Increase (-dec) in Cur. Liabl. 25,000 —

The ratios are as follows:

Financial Ratios 2016 2015 Industry

Liquidity Ratios

Accounts Receivable Turnover 18.67 16.00 11.10

Inventory Turnover 8.93 14.86 10.50

Current Ratio 3.98 3.06 2.30

Quick Ratio 2.05 2.06 1.90

Cash Flow Ratios

Earnings per Share $ 0.181 $ 0.199 -

The turnover ratios and the return on assets and return on equity ratios for

2016 use the average of the 2016 and 2015 balances in the denominator.

These ratios for 2015 use the relevant amounts in 2015 with no averaging

since data is not available for 2014.

The financial ratios for Williams Company show good performance on

increase in inventory should be investigated; what portion, if any, of the

inventory is obsolete or unsalable? Management should check to make

sure that purchasing and inventory management procedures are being

maintained properly and that the trend of declining inventory turnover does

not continue.

The profitability ratios are unfavorable. The gross margin percentage is

less than the industry average, as is the return on assets ratio. The gross

margin ratio has not changed significantly from 2015 to 2016, showing that

the company has been able to control costs of sales as sales have fallen.

However, return on assets and return on equity have fallen significantly and

20-23

Education.

Chapter 20 - Management Compensation, Business Analysis, and Business Valuation

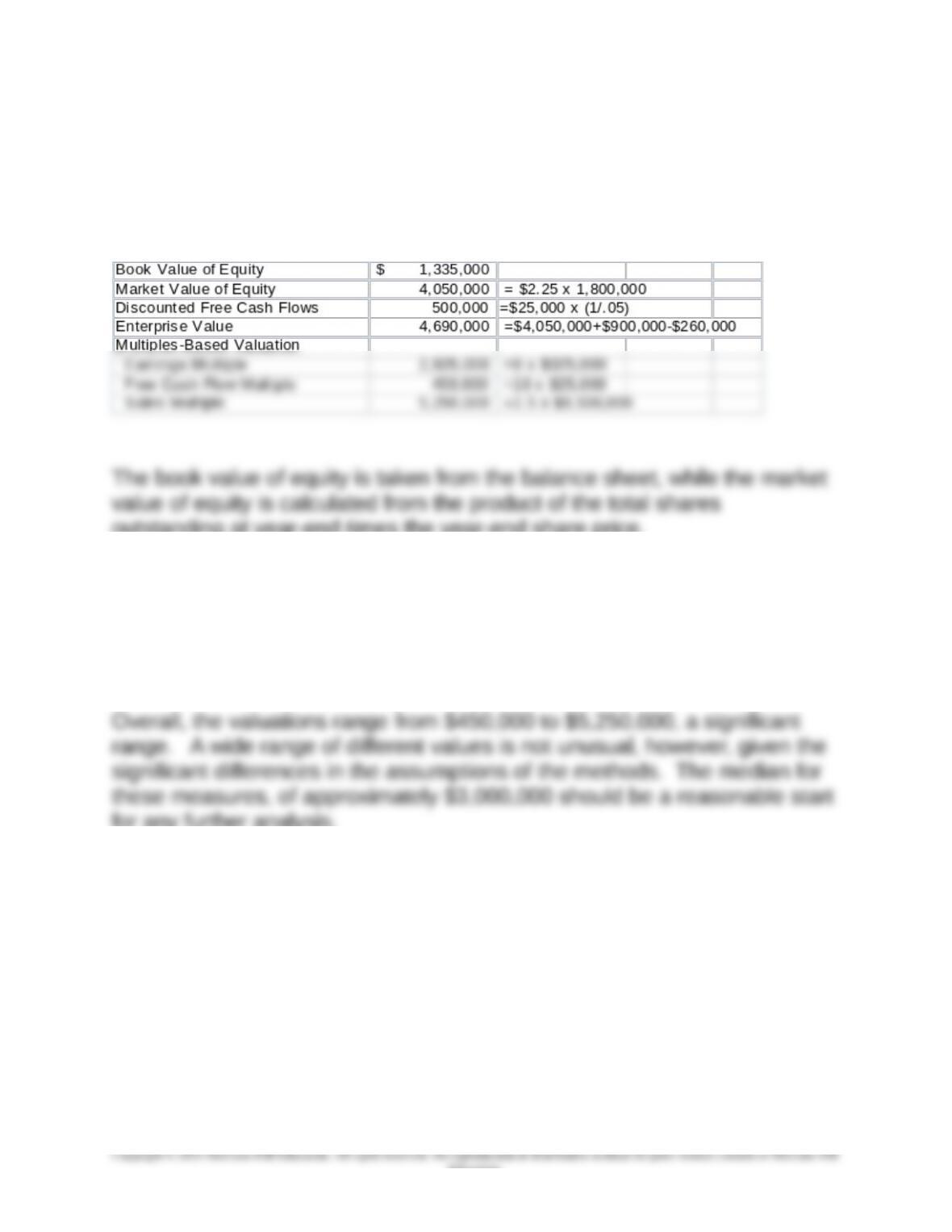

20-37 Business Valuation (30 min)

The book value of equity, market value of equity (market capitalization),

discounted cash flow, enterprise value, and multiples-based valuations for

Williams Company for 2016 are shown below.

outstanding at year-end times the year-end share price.

The DCF valuation is based on the assumption that free cash flows will

continue indefinitely, so that the discount rate used is the reciprocal of the

cost of capital, or 1/.05.

The multiples-based valuations utilize the industry average multiples times

Williams’ earnings, free cash flow and sales.

for any further analysis.

20-24

Education.

Chapter 20 - Management Compensation, Business Analysis, and Business Valuation

20-38 Business Valuation (15 min)

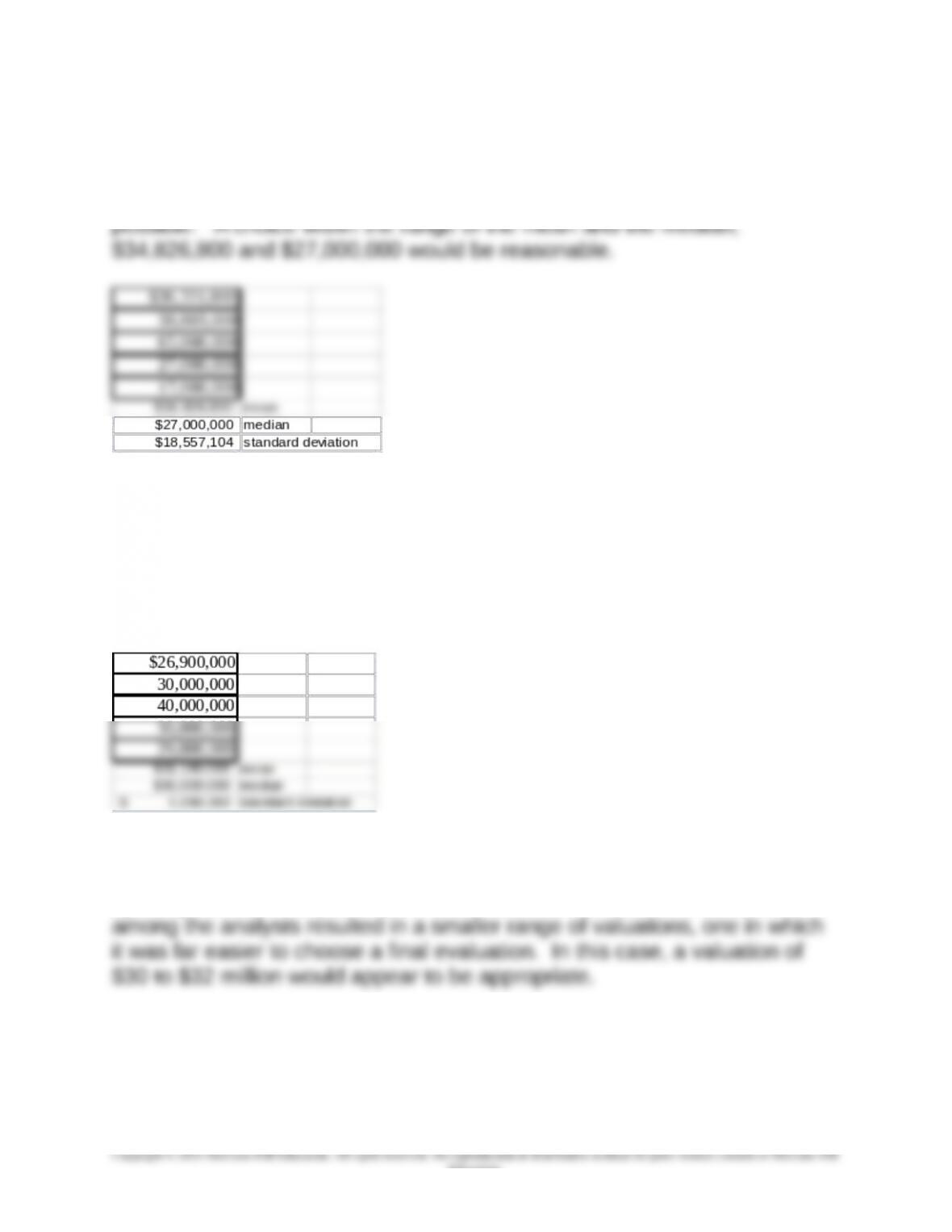

The simple mean and median for the data are shown below; the standard

deviation is $18,557,104. A number of choices for the final valuation are

The analysts who participated in the valuation described here also

participated in a market valuation approach in which the analysts could

confer, and change valuations over a period of time, utilizing a specially

designed web site. The valuations shown in the problem are the opening

valuations in this approach; later adjustments by each analyst, through

participation in the web site, resulted in a much smaller range of valuations:

The standard deviation of the final round of evaluation, shown above, was

$5,090,383, much smaller than the $18,557,104 standard deviation of the

opening round. The point of the article is to show that communication

Source: Peter Leitner, “Measure Twice, Cut Once,” Strategic Finance,

September 2005, pp. 27-32.

20-25

Education.

Chapter 20 - Management Compensation, Business Analysis, and Business Valuation

20-39 (Ratio Analysis (15 min)

2016 2015

Inventory turnover

5.96 = 2,085,480 ÷ ((332,452 + 367,514) ÷ 2)

5.91 = 1,975,471 ÷ ((367,514 + 301,208) ÷ 2)

Current ratio

2.64 = 1,141,800 ÷ 432,902

3.18 = 1,287,488 ÷ 405,401

2016. If cash flow is considered crucial, then the improvement in the cash

flow ratio would be highly valued.

20-40 (Ratio Analysis 10 min)

2013 2012

Gross margin percentage 27.4% = 3,583 ÷ 13,084 27.7% = 3,780 ÷ 13,632

Return on Assets 12.3% = 1,597 ÷ ((8,695 + 9,013) ÷ 2) 17.9% = 1,597 ÷ ((9,013 + 8,834) ÷ 2)

on assets declined significantly. Stockholder equity was fairly stable, so the

decline in income caused a significant drop in return on equity

20-26

Education.

Chapter 20 - Management Compensation, Business Analysis, and Business Valuation

20-41 (Business Valuation) 15 min

a. Market capitalization

443,000,000 shares x $74 per share = $32,782 million

b. Enterprise Value

consideration would be to employ additional valuation measures (for

example, the earnings multiple) to help determine the ultimate valuation.

Another approach would be to consider how the values for stock price, free

cash flow, and earnings are trending; are the figures used in the valuation

representative of the underlying trends for earnings, cash flow, and stock

price?

20-27

Education.

Chapter 20 - Management Compensation, Business Analysis, and Business Valuation

PROBLEMS

20-42 Compensation; Net Present Value (25 min)

This problem utilizes net present value concepts from chapter 12.

1. Annuity factor for 10 years at 10% is 6.1446

Annual savings from lower net operating costs

Replacing the current packaging machine with the new machine is

desirable because of the $38,676 in present value savings. From the

firm-level viewpoint, the machine should be replaced.

2. Steve expects to be with Kate’s for two more years. Thus the

rewards to him (from his 5% bonus) of the increases in net income

caused by the lower net operating costs, including the change in

Use of deferred bonus payments that emphasize the long-run

effects on net income could remedy this situation. For example,

awarding a bonus this year that pays 1% or less of net income for

each of the next six years would change the costs incurred to Bishop.

Restricted stock options-based compensation, where the options

must be exercised in future years, would also cause Bishop to think

about the long-run effects of his decision, but with only a two-year

window for his employment, this might not be the best option. Kate’s

20-28

Education.

Chapter 20 - Management Compensation, Business Analysis, and Business Valuation

20-43 Compensation; Benefits; Ethics (20 min)

1. The multiple levels of perquisites is a common practice and one

that is well understood and accepted. However, firms are obliged in

ethics, equity and fairness to all employees and to the shareholders

to make decision regarding perquisites on a reasonable basis. The

amount of perquisites should be associated with the responsibilities

of the manager, and should not be considered an entitlement of any

given level of employment. For example, an executive who must

2. Some of the instances described in the problem are probably

within the firm’s guidelines as acceptable use of perks. Often the firm

will pay for the spouse of an executive to accompany him or her on a

trip where the presence of the spouse is appropriate and in keeping

with the executive role on that trip. Other instances may involve

ethical issues which arise when perks are involved. Each should be

20-29

Education.

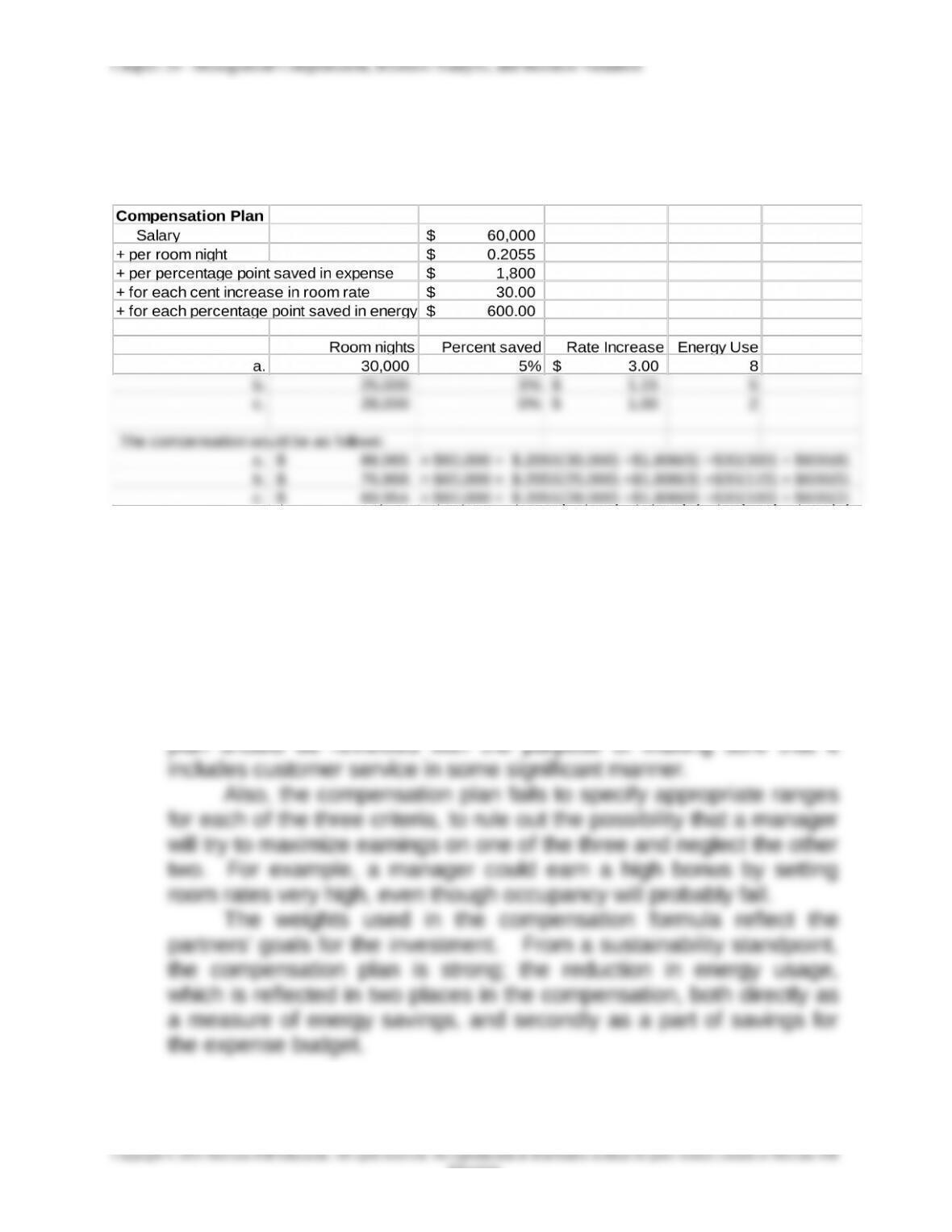

20-44 Incentive Pay in the Hotel Industry (20 min)

1. The compensation would be as follows:

2. The compensation plan appears to be an effective one, as it

includes all the key factors of success which the partners are

interested in. However, a key success factor for hotels, as for any

service firm, is to provide effective customer service, and none of the

quantitative measures includes customer service or satisfaction

(though the occupancy goal is said to include service quality, it is not

quantitatively included in compensation). Thus, the compensation

20-30

Education.