Chapter 16 – Operational Performance Measurement: Further Analysis of Productivity and Sales

16-45 Partial Operational and Financial Productivity; Total

Productivity (30 min)

1. Operational Partial Productivity

MF LI Difference

* The direction of variances denotes the advantage of LI over MF.

materials while MF yields a higher direct labor productivity.

2. Manufacturing Cost

MF LI

DM 240,000 x $ 10 = $2,400,000 180,000 x $10 = $1,800,000

DL 100,000 x $26 = 2,600,000 120,000 x $26 = 3,120,000

The financial partial productivity also shows mixed results. There is not a

clear advantage of one manufacturing alternative over the other.

3. Total Productivity

MF: 20,000 /$5,000,000 = 0.0040

LI: 20,000 /$4,920,000 = 0.0041

16-31

Education.

Chapter 16 – Operational Performance Measurement: Further Analysis of Productivity and Sales

16-46 Direct Labor Variances, Productivity Measures, and Standard

Costs (30 min)

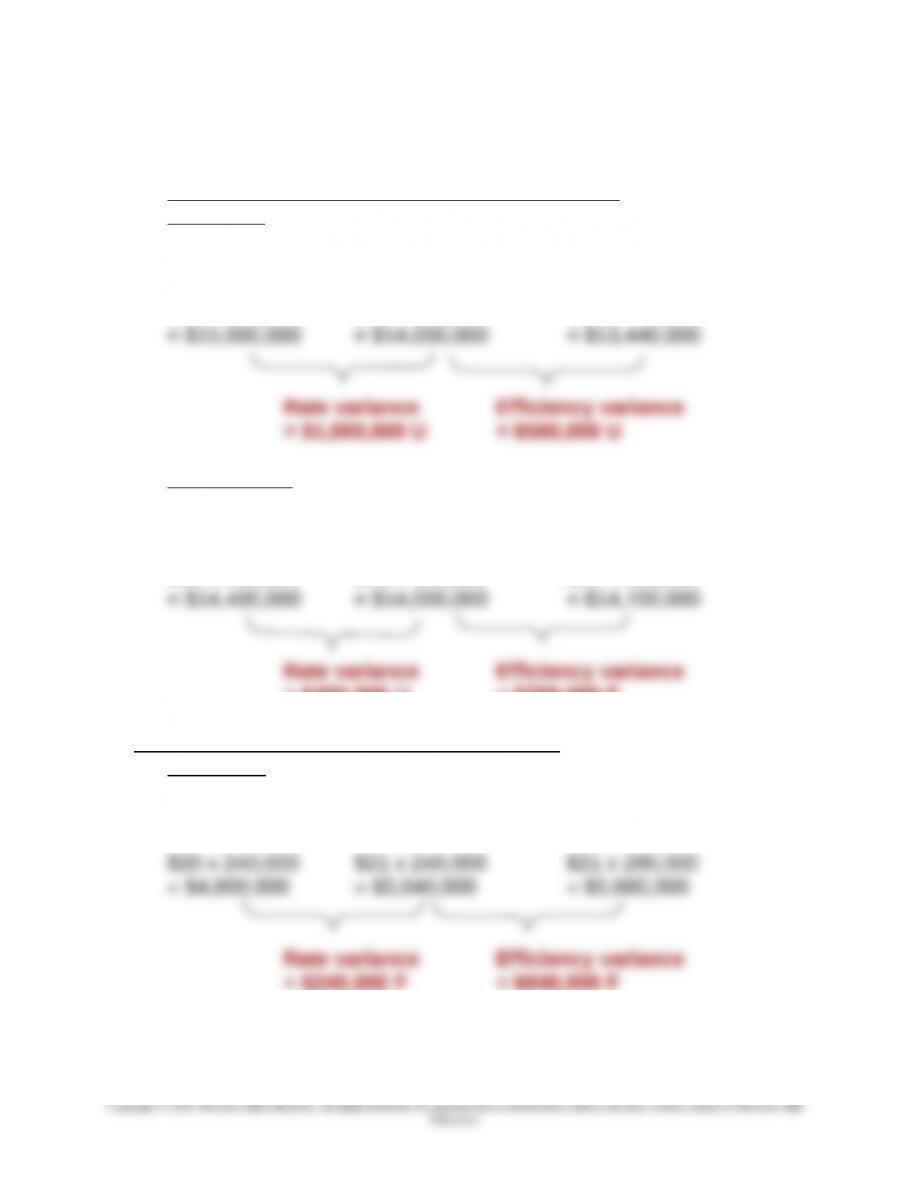

1. Assembly Department Direct Labor Variances

Prior year:

Total actual direct labor hours: 25 x 20,000 = 500,000

Total standard direct labor hours: 24 x 20,000 = 480,000

$30 x 500,000 $28 x 500,000 $28 x 480,000

Current Year:

Total actual direct labor hours: 20 x 20,000 = 400,000

Total standard direct labor hours: 21 x 20,000 = 420,000

$36 x 400,000 $35 x 400,000 $35 x 420,000

= $400,000 U = $700,000 F

Testing Department Direct Labor Variances

Prior Year:

Total actual direct labor hours: 12 x 20,000 = 240,000

Total standard direct labor hours: 14 x 20,000 = 280,000

16-32

Chapter 16 – Operational Performance Measurement: Further Analysis of Productivity and Sales

16-46 (continued -1)

Testing Department Direct Labor Variances (continued)

Current Year:

Total actual direct labor hours: 10 x 20,000 = 200,000

Total standard direct labor hours: 11 x 20,000 = 220,000

2. Assembly Department Operational Partial Productivity

Prior year: 20,000 ÷ 500,000 = 0.04

3. Assembly Department Financial Partial Productivity

Prior year: 20,000 ÷ $15,000,000 = 0.001333

Current Year: 20,000 ÷ $14,400,000 = 0.001389

16-33

Education.

Chapter 16 – Operational Performance Measurement: Further Analysis of Productivity and Sales

16-46 (continued -2)

4. Recap:

Operational partial productivity

Prior Current

Year Year Change

Assembly 0.04 0.05 0.01 F

Testing 0.083333 0.1 0.016667 F

5. The standards in a standard costing system often are determined

independently and incorporate changes in operating factors. The

standard for the operation of a year may change because of changes in,

for example, technology, quality of materials, experience of production

16-34

Education.

Chapter 16 – Operational Performance Measurement: Further Analysis of Productivity and Sales

16-47 Productivity and Market Share in the Auto Industry; Internet

Exercise (20 min)

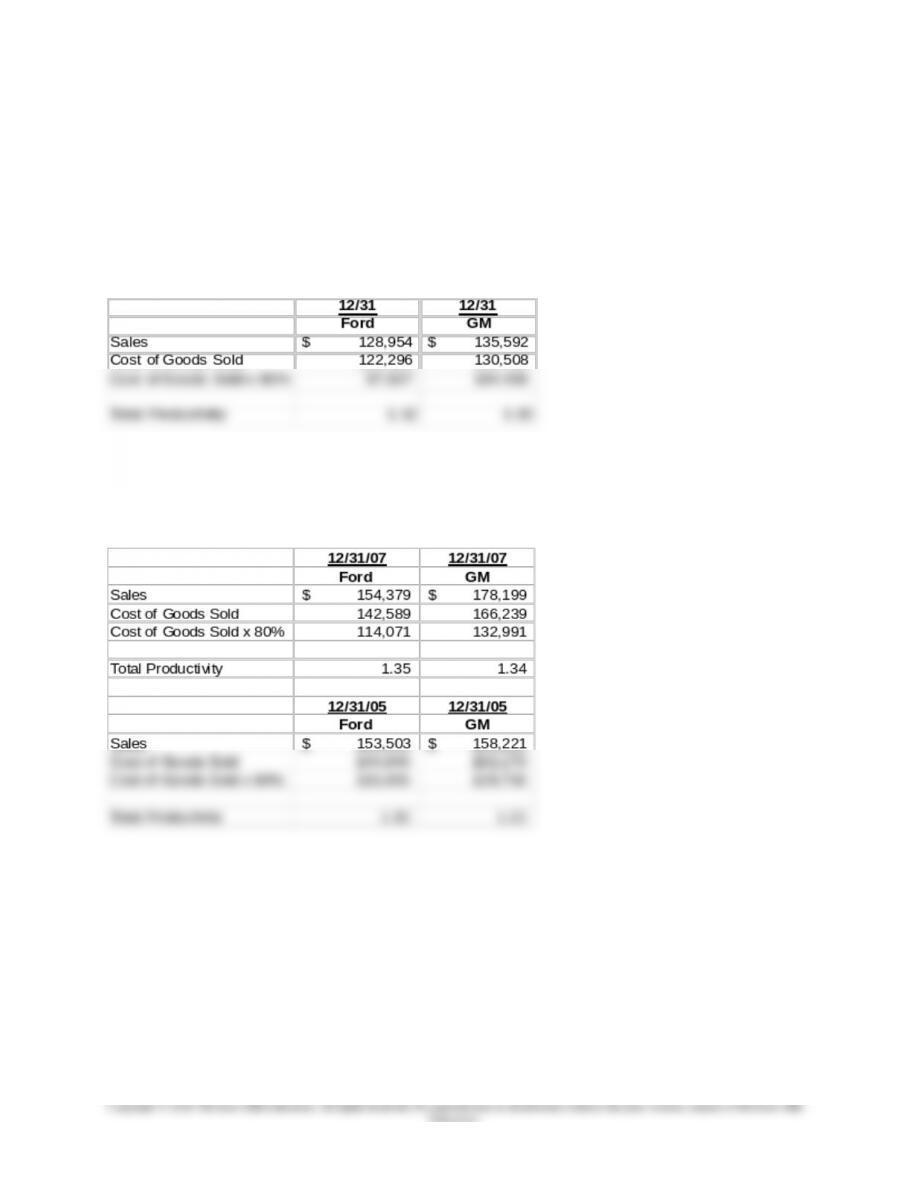

1.

The total productivity for the auto makers is shown below for the given

data. Also, while not required, the results for 2007 and 2005 are also

shown for comparison.

For contrast, the productivity calculations for the two companies in 2007

and 2005 are as follows:

The objective of this question is to make the students aware that total

productivity can be at least approximated for a company the student is

interested in by obtaining basic financial data from the firm’s annual report.

16-35

Education.

Chapter 16 – Operational Performance Measurement: Further Analysis of Productivity and Sales

16-47 (continued -1)

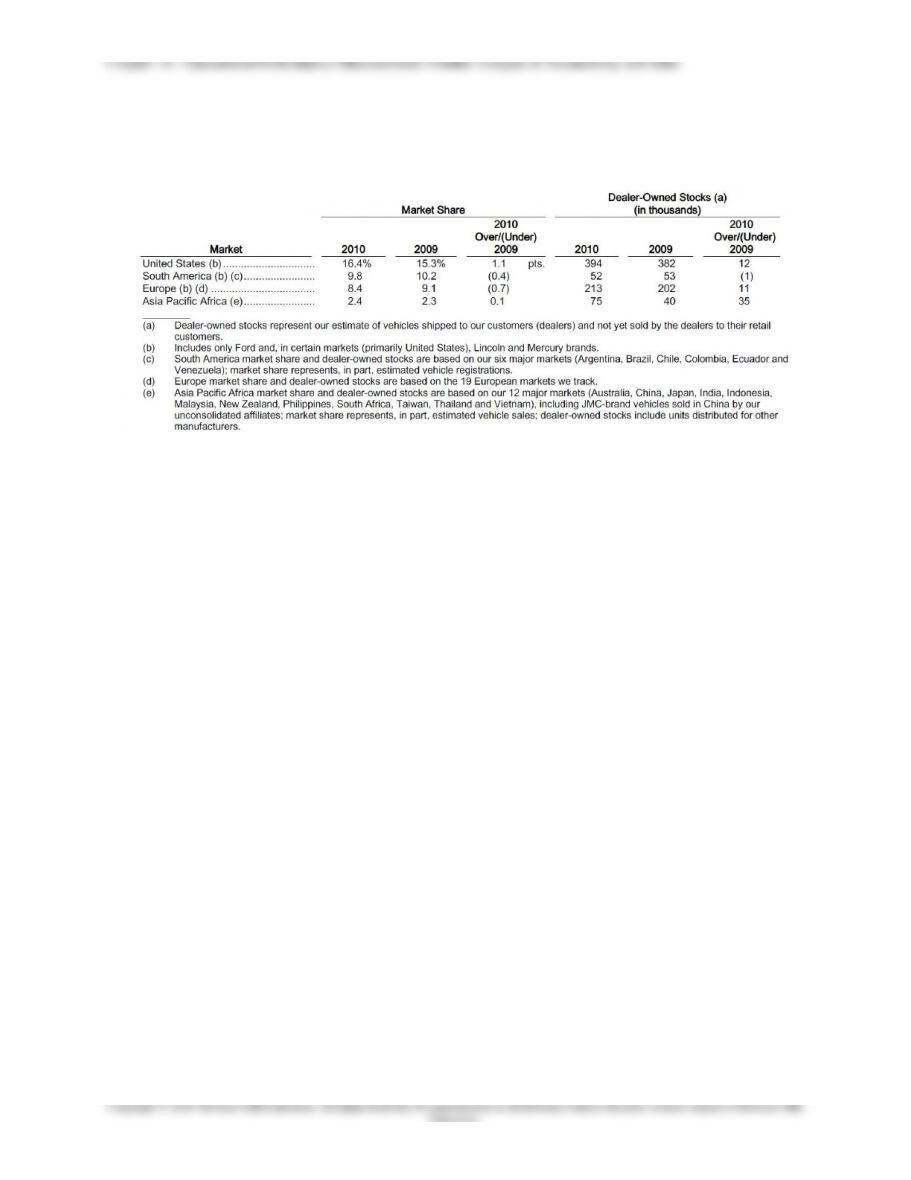

Note there are no significant differences between the auto makers or

between the productivity measures for the three years. Note that this is in

contrast to the Harbour Report data on auto firm productivity in 2008, cited

in Problem 16-35, which reports an increase in productivity (measured as

labor hours per vehicle) for Ford. The two measures of productivity do not

measure the same thing, so that these differences arise.

While the measures computed here are limited by the amount of

information available, they can provide a starting point for looking at other

measures of performance, and looking for more detailed information about

(in billions of dollars).

From Ford’s 2010 Annual Report:

“…Total costs and expenses for our Automotive sector for 2010 and 2009

2010(Over)/Under2009

Explanation of Change:

Volume and Mix, and Exchange (11.6)

Material Costs Excluding Commodity Costs 1.1

Commodity Costs (1.0)

Structural Costs (1.2)

Warranty / Other 0.1

16-36

Education.

Chapter 16 – Operational Performance Measurement: Further Analysis of Productivity and Sales

16-47 (continued -2)

Ford’s 2005 Annual Report has a similar analysis

Increase (decrease)

Supplier related cost $1

Pension and health care .8

Warranty costs .4

Depreciation and amortization (investments

in new equipment and faster depreciation) .3

2. This requirement can be assigned for class discussion, and answers will

likely vary, depending on what portion of the financial statement is used

and which year’s annual report is used. The discussion here can focus on

some of the following (all these points are based on the 2010, 2007 and

2005 annual reports of GM and Ford)

Alternatively, the instructor can assign requirement 1 only, and then discuss

some of the observations about requirement 2, as noted below.

16-37

Education.

16-47 (continued -3)

16-38

Education.

Chapter 16 – Operational Performance Measurement: Further Analysis of Productivity and Sales

16-48 Productivity and Ethics (15 min)

1. The operational partial productivity deteriorates slightly from 0.0051 in

the prior year (500÷99,000) to 0.005 in the current year (560÷112,000).

2. Tomas should not follow the order without following a consistent

accounting method. If the firm believes that certain cost items should be

16-39

Education.

Chapter 16 – Operational Performance Measurement: Further Analysis of Productivity and Sales

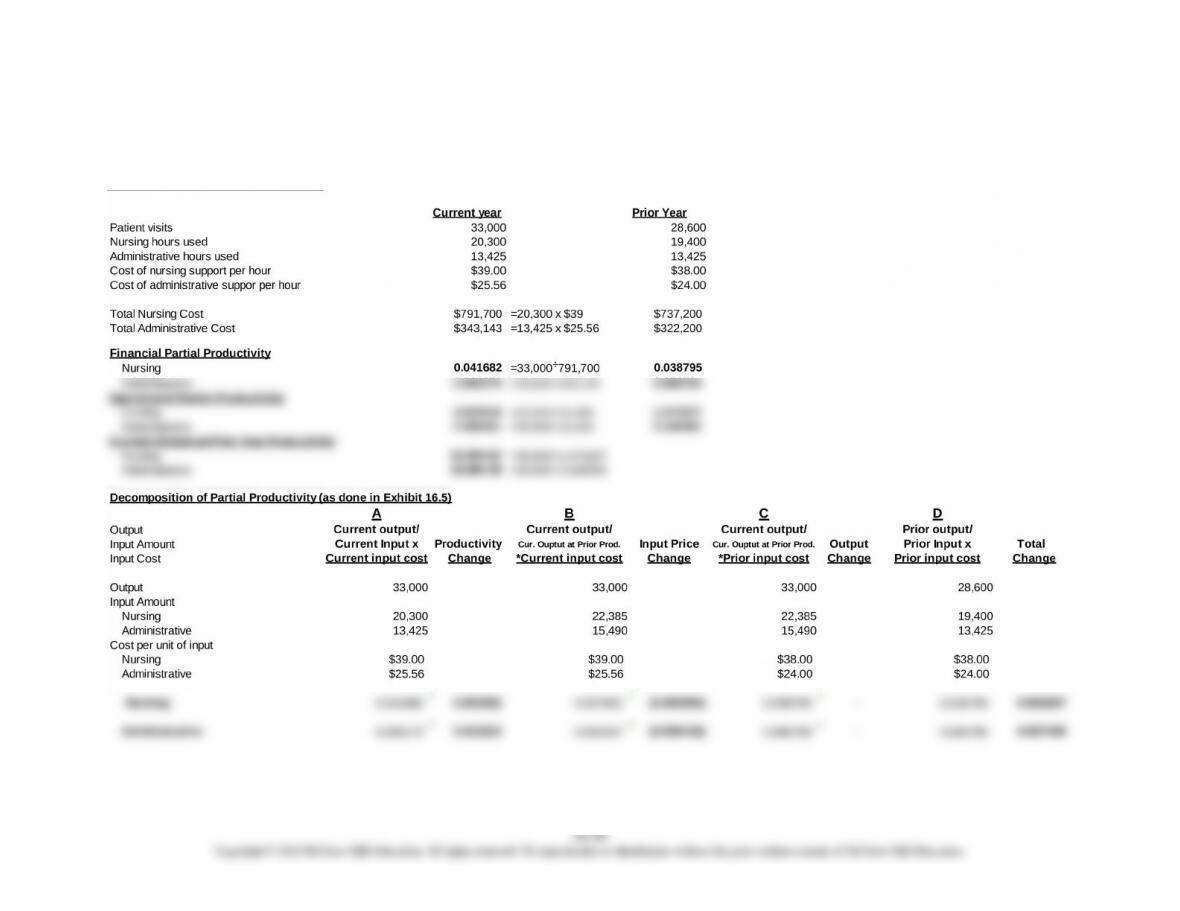

16-49 Partial Operational and Financial Productivity; Medical Practice (45 min)

1.,2. Partial operational and financial productivity and separation of partial financial productivity: