Chapter 17 – The Management and Control of Quality

17-66 (Continued-2)

Since JIT involves smooth and efficient flows throughout the entire value chain,

have suppliers and customers been consulted and included in any planning

17-62

Education.

Chapter 17 – The Management and Control of Quality

17-67 Assessing the Use and Role of Nonfinancial Performance Indicators (60

Minutes)

1. Nonfinancial performance indicators pertain to areas such as customer loyalty and

employee satisfaction. The authors of this cited article argue that monitoring and

reporting such measures as part of a comprehensive management accounting and

control system is important because:

as represented by the framework known as The Balanced Scorecard (BSC),

performance in these areas represents a precursor to financial performance

managers, etc.)

these indicators can, if appropriately developed, be used to assess

managerial performance

2. The authors hypothesize that many organizations are not able to reap the benefits of

including nonfinancial performance indicators in their management accounting and

control systems because:

haphazard selection of the set of nonfinancial performance indicators—many

organizations simply fail to choose and act on the right measures; in short,

and consistent with arguments that underlie the construction of an

Chapter 17 – The Management and Control of Quality

17-67 (Continued)

there is a natural tendency (i.e., bias) for managers to choose performance

indicators.

measurement errors—that is, companies choose performance indicators that

are not psychometrically sound (i.e., evidence regarding the validity of the

measures is not established)

3. The Institute of Management Accountants (IMA) has recently (December 11, 2008) a

revised its definition of “management accounting” (http://www.imanet.org [requires

log-in name and password]). This statement indicates that management accounting:

… is a profession that involves partnering in management decision-

making, devising planning and performance-management systems, and

providing expertise in financial reporting and control to assist management

in the formulation and implementation of an organization’s strategy.

Source: Christopher D. Ittner and David F. Larker, “Coming Up Short on Nonfinancial

Performance Measurement,” Harvard Business Review (November 2003), pp. 88-95.

17-64

Education.

Chapter 17 – The Management and Control of Quality

17-68 Relevant Costs and Quality Improvement (25 minutes)

1.

Lightening Bulk Company

Cost and Benefit Analysis of the Proposed

Scheduling and Tracking System

Cost of the new system (per year) $ 125,000

Expected benefits each year from the new system:

Contribution margin from sales increase:

(6,000 × 10%) × $200 × 37.5% = $ 45,000

Cost savings from decrease in misplaced

items—existing sales: 6,000 × (13% − 1.0%) × $65 = 46,800

Savings foregone from decrease in lost items—existing

2. Among other factors the manager needs to consider are: reliability and accuracy of

the estimates, including contribution margins, cost of tracking misplaced and lost

items (and their behavior patterns), and the estimated decreases in misplaced and

3. Cost to handle lost or misplaced items in the country in question:

Misplaced items: 6,000 × 13.0% × 0.8 × $65 = $40,560

Lost items: 6,000 × 2.0% × 0.8 × $300 = + 28,800

Total cost of handling lost/misplaced items $69,360

17-65

Education.

Chapter 17 – The Management and Control of Quality

17-69 Relevant Costs and Quality Improvement (50 Minutes)

1. Cost of new equipment and installation $12,000,000

Training 3,000,000

2. Quality cost if no change is made:

Rework (3,000 × 40%) × $2,000/unit = $ 2,400,000

Repair (3,000 × 15%) × $2,500/unit = 1,125,000

Appraisal 600,000

Inspection 3,000 × $50 = 150,000

Foregone contribution from lost sales:

Contribution margin per unit:

($12,000 × 85%) − $2,500 = $7,700

Quality cost of the new process:

Warranty repairs (3,000 0.8) × 5.0% × $1,000/unit = (187,500)

Savings from the new process each year $ 9,862,500

Years effective × 3

Savings over Three-Year Period $29,587,500

Appraisal and inspection cost, Year 1 ($600,000 +

3. Yes. The cost of the new process is $15,000,000 and the expected benefits total

$28,837,500 over three years. The pattern of pre-tax cash flows for this investment

opportunity is as follows:

Year 0 = ($15,000,000)

Year 2 = $9,862,500

Year 3 = $9,862,500

Thus, the payback period for this proposed investment is less than two years. Its

internal rate of return (IRR) is approximately 41%, as shown in the following screen

shot from Excel:

17-66

Education.

Chapter 17 – The Management and Control of Quality

17-69 (Continued)

4. The following factors should be considered before making the final decision:

a. Accuracy of cost estimates, including:

contribution margin per unit

costs of current repair and rework

cost of the new process

b. Reliability of estimations of

rates of rework and repair

making

5. The member of the board would be right if we ignore the financial payoff of the new

process and if the company is going to be in business for only three years. Having

17-67

Education.

Chapter 17 – The Management and Control of Quality

17-70 Cost-of-Quality (COQ) Analysis; Nonfinancial Performance Measures (60

Minutes)

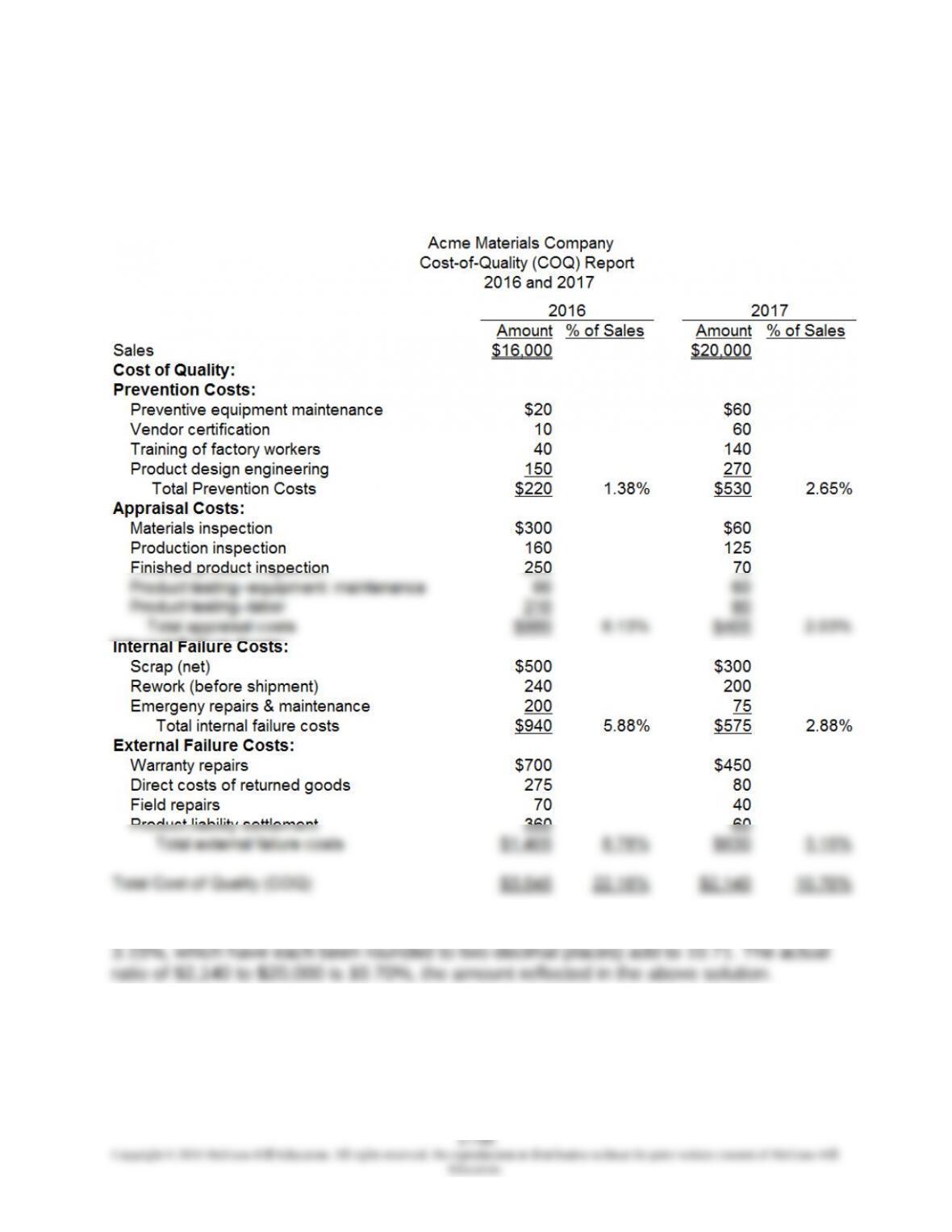

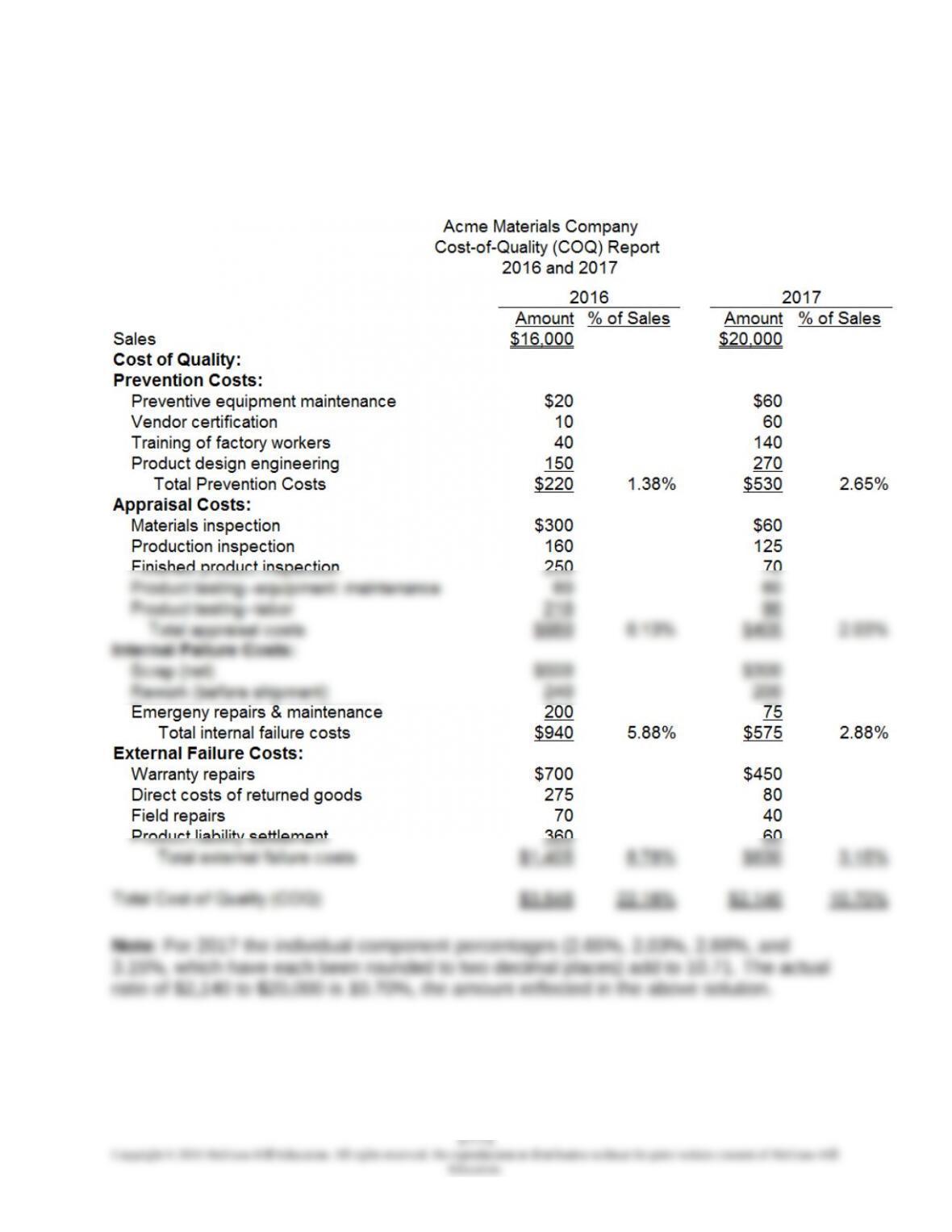

1. and 2. Cost-of-Quality (COQ) Report

Note: For 2017 the individual component percentages (2.65%, 2.03%, 2.88%, and

Chapter 17 – The Management and Control of Quality

17-70 (Continued-1)

3. Decrease in total Cost of Quality (COQ) as a percentage of sales, from 2016 to

2017, is approximately 11%:

2016 COQ, as a percentage of sales = 22.16%

sales in 2017 compared to 2016. However, even without the sales dollar increase,

the total COQ has decreased, both in absolute and in relative terms:

Acme increased spending in 2017 on prevention (141% of the 2016 amount). As a

result, each of the other three categories of COQ (viz., appraisal, internal failure,

and external failure) decreased in 2017, both in absolute dollars and as a

percentage of sales dollars:

XPrevention Costs:

2017 Amount = $530

2016 Amount = $220

4. To complement the COQ data, the company may want to collect both internal and

external nonfinancial measures of quality, such as the following:

Internal Measures of Quality

The number of defects per period

Throughput (or, throughput efficiency)

17-70 (Continued-2)

17-69

Education.

Chapter 17 – The Management and Control of Quality

External Measures of Quality

The number of customer complaints

5. As should be obvious from an examination of Exhibit 17.3, there is a role for

both financial and nonfinancial quality data (metrics) in a comprehensive

framework for managing and controlling quality. COQ (i.e., financial) data are

reported only periodically. As such, they are likely of greater interest/value to

managers. After all, these are the individuals who ultimately have responsibility

over financial performance and who make spending and investment decisions

regarding quality costs.

Operating personnel, on the other hand, are likely to find nonfinancial quality

data to be more useful. For one thing, such data are expressed in terms that are

17-70

Education.

Chapter 17 – The Management and Control of Quality

17-71 Cost-of-Quality (COQ) Analysis—Spreadsheet Application (60 Minutes)

1-4: Cost of Quality (COQ)—Excel-Generated Report