Chapter 17 – The Management and Control of Quality

17-48 (Continued)

3. There are likely opposing points of view. Companies that are included in

portfolios of high performance in the environmental (or social) area are certainly

likely to favor such disclosures. Stockholders (and potential investors) may favor

such disclosures, particularly since the external failure costs that some

companies face can have devastating effects on the ability of an organization to

17-32

Education.

Chapter 17 – The Management and Control of Quality

17-49 Cost-of-Quality (COQ) Report: Environmental Management (30 Minutes)

1. Sample Cost of Environmental Quality Report:

% of Total

Operating

Amounts Subtotals Cost

Prevention Costs:

Employee training $100,000

Product design 140,000

Supplier certification 40,000 $280,000 2.8%

Appraisal Costs:

Process inspection $320,000 3.2%

Internal Failure Costs:

2. With only a single year of data, it is difficult to draw any meaningful conclusions.

3. Some qualities (attributes) of an effective (“good”) environmental quality cost

system:

Collect environmental quality-cost data from across the value chain (i.e., the

scope of data collection should be broad).

If possible, utilize activity-based cost (ABC) data, which could be used to

17-33

Education.

Chapter 17 – The Management and Control of Quality

17-50 Cost-of-Quality (COQ) Improvement—Relevant Cost Analysis (30 Minutes)

1. Relevant cost analysis (short-term impact on annual operating profit):

Annual Cost of Lighting:

Cost of a new lighting system: $100,000 5 years = $20,000

Additional operating cost per year 5,000

Incremental cost per year $25,000

Annual Cost Savings:

2. Some additional factors that might bear on this decision:

Time-value-of money (this type of problem is an example of a capital budgeting

decision; as such, the time-value-of-money should be taken into consideration).

The reduction in waste/scrapped products produced effectively increases the

might be realized because of the reduction in scrap costs?

3. As indicated in Exhibit 17.3 and the accompanying text discussion, the

management accountant plays a pervasive role in a comprehensive quality

management and control system. Fundamentally, the management accountant is

17-35

Education.

17-51 Relevant Cost Analysis—Conversion to JIT; Spreadsheet Application (25

Minutes)

Current After

Income Statement Items Situation JIT

Sales $1,350,000a$1,650,000g$300,000

Less: Costs

Direct materials 405,000b330,000h(75,000)

Direct labor 297,000c247,500i(49,500)

Notes:

aGiven

bSales × 30% = $1,350,000 × 30% = $405,000

cSales × 22% = $1,350,000 × 22% = $297,000

gGiven

hSales × 20% = $1,650,000 × 20% = $330,000

iSales × 15% = $1,650,000 × 15% = $247,500

Note to Instructor: An Excel spreadsheet solution file for this exercise is embedded

in this document. You can open the spreadsheet “object” that follows by doing the

following:

1. Right click anywhere in the worksheet area below.

2. Select “worksheet object” and then select “Open.”

3. To return to the Word document, select “File” and then “Close and return

to…” while you are in the spreadsheet mode. The screen should then return

you to the Word document.

Ex. 17-51 7e.xlsx

17-36

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Chapter 17 – The Management and Control of Quality

17-52 Relevant Cost Analysis: Decision Making (30 Minutes)

1. Net Annual Financial Beneit of Implemening the New Technology

Incremental Revenue from Improvement in On-Time Delivery Rate:

Improvement in On-Time Delivery Rate = 95% − 80% = 15%

Incremental Costs:

Annual cost of new technology $80,000

Therefore, based on assumed changes the proposed investment in the new technology is not jusiied.

Minimum Increase in Sales to Jusify Investment in New Technology

Annual cost of new technology (given) = $80,000

Minus: decrease in variable costs because of reducion in lost/damaged packages = $6,000

Required increase in annual contribuion margin to jusify new technology = $74,000

Conversion of required contribuion margin to required sales dollars:

X

17-37

Chapter 17 – The Management and Control of Quality

17-53 Cost of Quality (COQ) Reporting (40 minutes)

1.

$ Amount % of Total % of Sales

Prevenion Costs:

Quality training $12,000

New vendor veriicaion and faciliies inspecion $25,000

Technical support provided to vendors $ 4,000

Subtotal $41,000 13.40% 0.98%

Appraisal Costs:

Field test of new computer $74,000

Equipment inspecion $20,000

Test and inspecion of purchased parts $32,000

Internal Failure Costs:

Spoiled work-in-process inventory disposal $28,000

Downime, due to quality problems $24,000

Re-inspecion $13,000

Rework (labor and overhead) $8,000

Subtotal $73,000 23.86% 1.74%

External Failure Costs:

2. The mix between conformance costs (Prevention and Appraisal) versus nonconformance

costs (Internal Failure and External Failure) seems reasonable. As well, the total COQ as a

percentage of sales seems reasonable, or at least not significantly out of line. Benchmarking the

results of this company to a relevant standard would be desirable.

3. There are at least three primary limitations to the COQ report illustrated in the present

exercise: (a) the COQ report provides data for only a single period; time-series data (multiple

observations over time) would be more informative (in part this is because there is typically a

17-38

Education.

Chapter 17 – The Management and Control of Quality

17-54 Relevant Cost Analysis—Quality Improvements (25 Minutes)

Estimated cost savings resulting from the recently enacted quality program come

from two sources:

1. Manufacturing cost savings associated with the reduction in rework costs:

= (reduction in reject rate) × (annual volume of output) × (total rework cost per

2. Financing cost savings associated with the reduction in inventory holdings:

Reduction in Inventory Holdings = $400,000 − $250,000 = $150,000

3. Total estimated savings due to quality improvement program

= rework cost savings + inventory financing cost savings

17-39

Chapter 17 – The Management and Control of Quality

17-55 Nonfinancial (Operational) Control Measures: Environmental Performance (25

Minutes)

The purpose of this exercise is to get students to think about the process of

developing nonfinancial quality indicators, based on specified Environmental

Objectives (five in the present case). The purpose of these indicators is to gauge

progress in accomplishing the specified Environmental Objectives and, as such, to

motivate improved quality in environmental performance. The following answers are

suggestive only:

Minimize Hazardous Materials:

Types and quantities of hazardous materials produced (in total,

Minimize Energy Requirements:

Types and quantities of energy consumed

Productivity measures (energy consumption per unit produced, etc.)

Minimize Release of Residues into the Environment:

17-40

Education.

Chapter 17 – The Management and Control of Quality

17-55 (Continued-1)

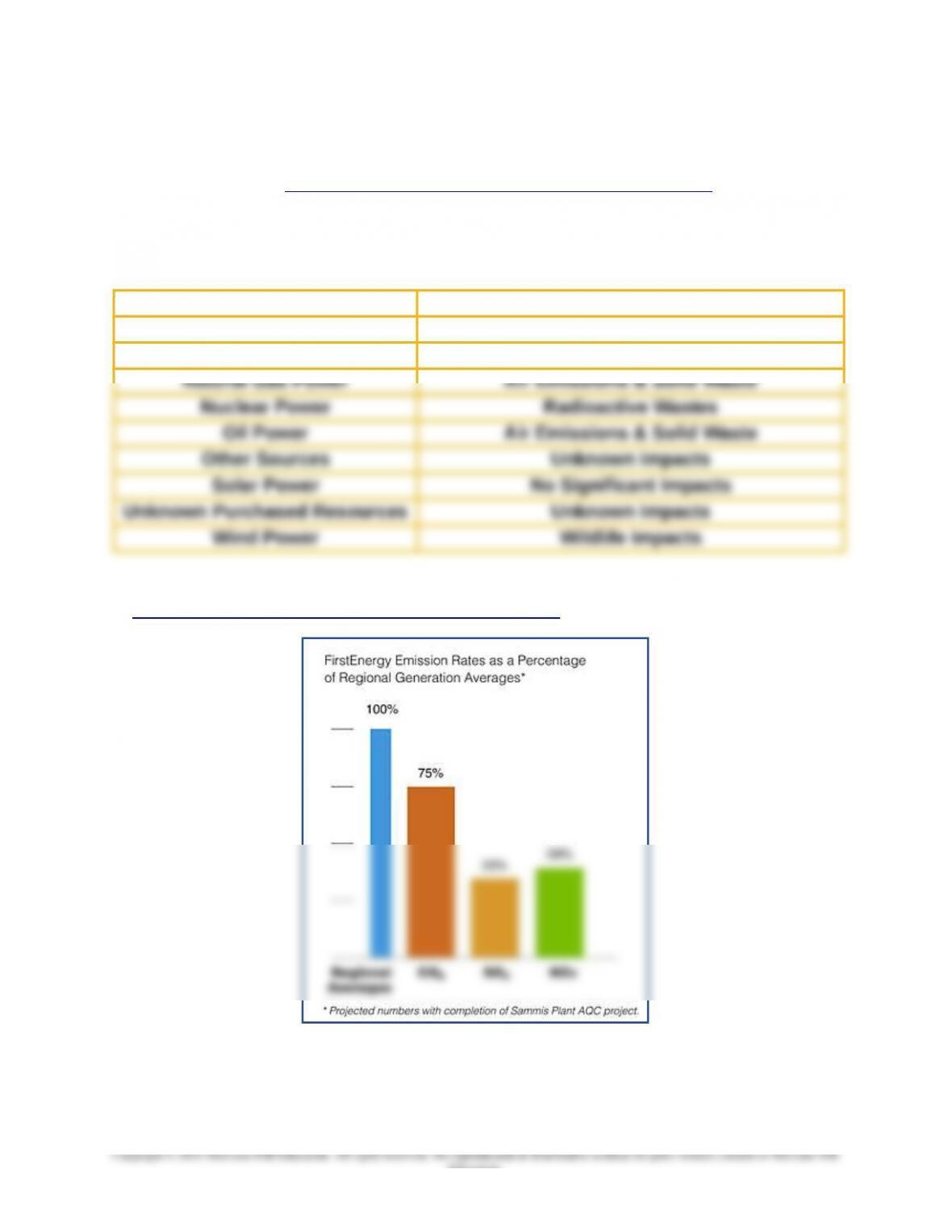

The instructor might want to use some of the following example disclosures from First

Energy Corporation (https://www.firstenergycorp.com/environmental.html) for illustrative

purposes:

Environmental Characteristics Associated with Various

Sources of Power Generation

Biomass Power Air Emissions & Solid Waste

Coal Power Air Emissions & Solid Waste

Hydro Power Wildlife Impacts

Air Emission Disclosure: First Energy Corporation, 2011

(https://www.firstenergycorp.com/environmental.html, accessed 25 November 2011)

Website updated: 08 September 2011

17-41

Education.