Chapter 11 – Decision Making with a Strategic Emphasis

Chapter 11

Decision Making with a Strategic Emphasis

Learning Objectives

LO 11-1 Define the decision-making process and identify the types of cost information relevant for

decision making.

LO 11-2 Use relevant cost analysis and strategic analysis to make special-order decisions.

LO 11-3 Use relevant cost analysis and strategic analysis in the make, lease, or buy decision.

LO 11-4 Use relevant cost analysis and strategic analysis in the decision to sell before or after additional

processing.

LO 11-5 Use relevant cost analysis and strategic analysis in the decision to keep or drop products or

services.

LO 11-6 Use relevant cost analysis and strategic analysis to evaluate service and not-for-profit

organizations.

LO 11-7 Analyze the short-run product-mix decision.

LO 11-8 Discuss behavioral, implementation, and legal issues in decision making.

LO 11-9 Set up and solve in Excel a simple product-mix problem (appendix).

New in this Edition

One updated Real-World Focus (RWF) item, dealing with distortions and deceptions in decision-making

Three (3) new Real-World Focus (RWF) items: Sustainability—The Decision to Install Solar;

Amzaon.com—Insourcing of Retail Delivery Service; and, Sustainability—Choice of a New Auto

Increased use of Excel’s “Goal Seek” function for end-of-chapter exercises and problems

Shorter, crisper discussion of Predatory Pricing Practices

Teaching Suggestions

A key teaching point for this chapter is that the strategic issues can be more important than the calculation of

contribution margin or relevant cost to determine a preferred decision alternative. The approach I take is to first

introduce the concepts of relevant costs and decision making, and then to bring in the importance of the firm’s

strategy in determining the correct decision.

I typically cover Chapter 11 in two days. In the first day I present the fundamental concepts of

contribution/relevant cost decision making and cover one or more assignments from the following areas:

1. the special-order decision

2. the make, lease, or buy decision

3. the decision to sell at split-off or after additional processing

4. the decision to keep or drop a product line

5. evaluating programs, including not-for-profit programs

I do not stress the strategic approach on the first day, but concentrate instead on the fundamentals and problem

solving. The first day is mostly drill and practice in problem solving. I explain to the students that in this chapter

the concepts are simple but the application is sometimes difficultthat many students find they can understand the

chapter but have difficulty with some of the homework (and exam) problems. I tell them a key approach in this

11-1

Education.

Chapter 11 – Decision Making with a Strategic Emphasis

chapter has to be practice, so that they see how to work a variety of different problems and develop confidence in

working these problems.

On the second day I focus on developing the strategic approach to decision making. I use one or more

exercises/problems to reinforce the point that relevant information for decision making includes both quantitative

(financial and non-financial) data as well as qualitative/strategic considerations. My main objective for the second

day is to leave the students with the idea that relevant cost/contribution margin decision analysis is only a part of

decision making, and that strategic considerations play an important part. Time permitting, and in the advanced

course, I present linear programming for the short-term product-mix decision; the Appendix to Chapter 11 shows

how to use the Solver Routine in Excel 2010 for this purpose.

Assignment Matrix

End-of-Chapter Exercises and Problems Chapter Learning Objectives Text Features

7th ed.

EOC

6th ed.

EOC

Transition

6e to 7e

X = included in Connect

Est. Time

1. Decision-making process

2. Special-order decisions

3. Make, lease, or buy decisions

4. Sell before or after processing

5. Keep or drop decision

6. Service/NFP Programs Anal.

7. Short-term Product/Service Mix

8. Behavioral and legal issues

9. Using Excel: Product-Mix Prob.

Strategy

Service

International

Ethics

Sustainability

Brief Exercises

11-11 11-14 – X 10 min X

11-12 11-17 – X 5 min X

11-13 11-18 – X 5 min X

11-14 11-20 – X 10 min X

11-15 11-19 – X 10 min X

11-16 11-16 – X 10 min X

11-17 11-12 – X 10 min X

11-18 11-13 – X 5 min X

11-19 11-11 – X 5 min X

11-20 11-15 – – 5 min X

Exercises

11-21 11-29 – – 60 min X X X

11-22 11-21 – X 30 min X

11-23 11-22 – X 50 min. X

11-24 11-23 – X 30 min X X

11-25 11-24 – X 25 min X X

11-26 11-25 Revised X 50 min X

11-27 11-27 – X 45 min. X X

Continued on next page…

Chapter 11 Assignment Matrix—Continued

End-of-Chapter Exercises and Problems Chapter Learning Objectives Text Features

11-2

Chapter 11 – Decision Making with a Strategic Emphasis

7th ed.

EOC

6th ed.

EOC

Transition

6e to 7e

X = included in Connect

Est. Time

1. Decision-making process

2. Special-order decisions

3. Make, lease, or buy decisions

4. Sell before or after processing

5. Keep or drop decision

6. Service/NFP Programs Anal.

7. Short-term Product/Service Mix

8. Behavioral and legal issues

9. Using Excel: Product-Mix Prob.

Strategy

Service

International

Ethics

Sustainability

11-28 11-26 – – 50 min. X X

11-29 11-28 – – 50 min X

11-30 11-30 Revised X 90 min X X X X X X

Problems

P11-31 P11-39 – – 90 min. X X X X X X

P11-32 P11-32 Revised – 45 min. X X X X

P11-33 P11-33 Revised – 60 min. X X X

P11-34 P11-34 Revised – 45 min X

P11-35 P11-31 – – 90 min X X X

P11-36 P11-35 – – 60 min X X X

P11-37 P11-37 Revised – 45 min X X X

P11-38 P11-38 – – 45 min X X X X X X

P11-39 P11-42 – – 60 min X X X

P11-40 P11-43 – – 75 min X X X

P11-41 P11-44 Revised – 60 min X X

P11-42 P11-46 – – 75 min X X X X

P11-43 P11-47 – – 45 min X X

P11-44 P11-36 – – 45 min X X X X X

P11-45 P11-48 – – 60 min X X X

P11-46 P11-40 – – 75 min X X X

P11-47 P11-41 – – 45 min X X

P11-48 P11-45 – – 60 min X X

Lecture Notes

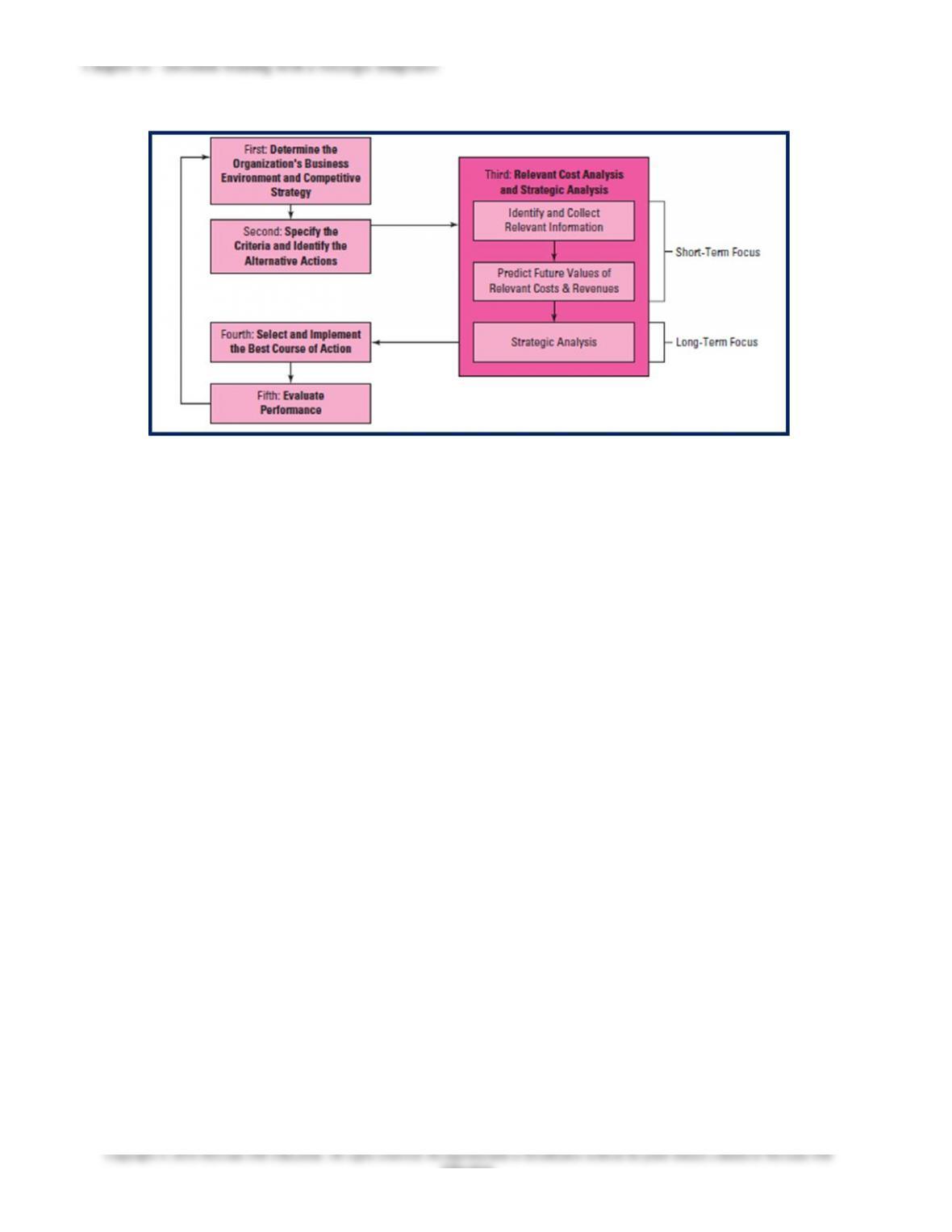

A. The Decision-Making Process—see Text Exhibit 11.1. In deciding among alternative choices for a given

situation, managers employ the following five-step process. The first, and probably most important, step is to

consider the strategic issues regarding the decision context. This helps focus the decision maker on answering the

right question. The second step is to specify the criteria by which the decision is to be made. Often, a manager is

forced to think of multiple objectives, both the quantifiable short-term goals, and the more strategic long-term

goals. In the third step, a manager performs an analysis in which the relevant information is developed and

analyzed, using relevant cost analysis and strategic analysis. This step involves three sequential steps, the manager

identifies and collects relevant information about the decision, makes predictions about the relevant information,

and considers the strategic issues involved in the decision. Fourth, based on the cost analysis, the manager selects

the best alternative and implements it. In the fifth step, the manager evaluates the performance of the implemented

decision as it relates to future decisions.

11-3

Education.

B. Relevant Cost Analysis—Basic Considerations:

1. Relevant Cost Information. Relevant costs are costs that will be incurred at some future time and

that differ for each option available to the decision maker. A relevant cost can either be variable or

fixed. Generally, variable costs are relevant for decision making because they differ for each

option and have not been committed. In contrast, fixed costs are often irrelevant, since typically

they do not differ for the options. Occasionally, some variable costs are not relevant and

sometimes, fixed costs can be relevant. However, there is more to the decision process than the

discovery of relevant costs. The manager must also consider the long-term, strategic issues.

2. Batch-Level Cost Drivers. Although most relevant costs for many decisions are variable, the

concept of variable costs does not mean only a cost tied to changes in the output level. A variable

cost varies directly with changes in a given cost driver, whether it is the number of products

produced, or the number of batches of product produced. In determining the costs that differ for

options, managers must consider variable costs in the broadest possible sense as those that might

vary at any level of manufacture (units of output, batches, and products).

3. Fixed Costs and Depreciation. A common misperception is that depreciation of existing facilities

is a relevant cost. Depreciation is a portion of a committed cost; therefore, it is sunk and irrelevant.

There is an exception to this rule: when tax effects are considered in decision-making. In this case,

depreciation has a positive value, since it’s an expense and it reduces taxable income.

4. Other Relevant Information: Opportunity Costs. Managers should include in their decision

process information such as the capacity usage of the plant. Capacity usage information is a

critical signal of the potential relevance of opportunity costs, the benefit lost when one chosen

option precludes the benefits from an alternative option. When opportunity costs are relevant, the

manager must consider the value of lost sales as well as the contribution form the new order or

new product. Another important factor is the time value of money that is relevant when deciding

among alternatives with cash flows over two years or more.

C. Strategic Analysis. Strategic information keeps the decision maker’s attention focused on the firm’s crucial

strategic goal. Failing to attend to the long-term, strategic factors could cause the firm to be less competitive in

the future. By identifying only relevant costs, the decision maker might fail to link the decision to the firm’s

11-4

Education.

Chapter 11 – Decision Making with a Strategic Emphasis

strategy. A good indication of a manager’s failing to take a strategic approach is that the analysis will have a

product cost focus, while a strategic relevant cost analysis also addresses broad and difficult-to-measure strategic

issues.

D. Special-Order Decisions: Cost Analysis. The special-order decision occurs when a firm has a one-time

opportunity to sell a specific quantity of its product or service. It is called “special order” because it is typically

unexpected and non-recurring in nature. To make this special order decision, managers need critical information

about relevant costs, revenues, and any opportunity costs.

E. Special-Order Decisions: Strategic Analysis. The relevant cost analysis described in the previous section

provides a useful decision regarding the order’s profitability. However, for a full decision analysis, the firm

should also consider the strategic factors of capacity use, short-term vs. long-term pricing, the trend in variable

costs, and the use of activity-based costing. The relevant cost decision rule for special orders is intended only for

those infrequent situations when a special order can increase income. Done on a regular basis, relevant cost

pricing can erode normal pricing policies and lead to a loss on profitability for firms. Special order decisions

should not become the centerpiece of a firm’s strategy.

F. Make, Lease, or Buy Decisions: Cost Issues. The relevant cost information for the make-or-buy decision is

developed in a manner similar to that of the special order decision. The relevant cost information for making the

component consist of the short-term costs to manufacture it, ordinarily the variable manufacturing costs, which

would be saved if the part was purchased. These costs are compared to the purchase price for the part to determine

the appropriate decision. A similar question arises when a firm must choose between leasing or purchasing a piece

of equipment. Such decisions become ever more frequent as the cost and terms of the lease agreement become

more favorable.

G. Make, Lease, or Buy Decisions: Strategic Analysis. The make, lease, or buy decision often raises strategic

issues. Make, lease, or buy analysis has a key role in the decision to outsource by providing an analysis of the

relevant costs. Certain firms have taken the idea of outsourcing one step further, to what is called contract

manufacturing, in which another firm manufactures a portion of the first firm’s products. When one firm has

more capacity or expertise than another firm, contract manufacturing can be a cost-effective strategy for both

firms.

H. Sell Before or After Additional Processing: Cost Analysis. Another common decision concerns the option to

sell a product or service before an intermediate processing step or to add further processing and then selling the

product or service for a higher price. The analysis of features also is important for manufactures in determining

what to do with defective parts. The decision is whether the product should be sold with or without additional

processing. I use class time to distinguish between financial reporting uses of cost information (here, the need to

allocate joint production costs to outputs, so that the accountant can prepare financial statements—inventory on

the Balance Sheet, and Cost of Goods Sold on the Income Statement) versus the decision-use of cost information

(here, whether certain products should be sold at the spilt-off point or processed further and then sold). Again, the

decision process should begin (but not end) with a relevant cost analysis: which costs in the decision are

avoidable, and which are not? Added in the 6th edition was a discussion of the following terms:

joint production process

split-off point

joint production costs, and

separable processing costs

I. Sell Before or After Additional Processing: Strategic Analysis. Strategic concerns arise when considering

selling to discount stores, and whether doing so will affect sales in our markets.

11-5

Education.

Chapter 11 – Decision Making with a Strategic Emphasis

J. Profitability Analysis: Keep or Drop a Line—Cost Issues. An important aspect of management is the

regular review of product profitability. This review should address the following issues:

Which products are most profitable?

Are these products properly prices?

Which products should be promoted and advertised more aggressively?

Which product managers should rewarded?

K. Profitability Analysis: Keep or Drop a Line—Strategic Issues. In addition to the relevant cost analysis, the

decision to keep or drop a product line should include relevant strategic factors, such as the potential effects of the

loss of one product line on the sales of another. Other important factors include the potential effect on overall

employee morale and organizational effectiveness if a product line is dropped. Moreover, managers should

consider the sale growth potential of each product. A particularly important consideration is the extent of available

production capacity.

L. Profitability Analysis: Evaluating Programs—Cost Issues. Managers use the concept of relevant cost

analysis to measure the financial effectiveness of programs or projects sponsored by government and non-profit

organizations.

M. Multiple Products and Limited Resources. The preceding relevant cost analyses were simplified by using a

single product and assuming sufficient resources to meet all the demands. The analysis changes significantly with

two or more products and limited resources. A key element of the relevant cost analysis is the most profitable

sales mix for the two products. If there are no production constraints, the answer is clear, we manufacture what is

needed to meet demand for both products. However, when demand exceeds production capacity, management

must make some trade-offs about the quantity of each product to manufacture, and therefore, what demand is

unmet.

1. One Resource Constraint. When there is only one production constraint and excess demand, it is

generally best to focus production and sales on the product with the highest contribution per unit of scarce

resource. Of course, it is unlikely in a practical situation that a firm would be able to adopt the extreme

position of deleting one product and focusing entirely on the other. An optimal solution in this simplified

case can be determined graphically (that is, by determining the total contribution margin associated with

the “corner points” on a graph similar to the one depicted in Exhibit 11.19).

2. Two Resource Constraints. When the production process requires two or more production constraints, the

choice of sales mix involves a more complex analysis, and in contrast to one production constraint, the

solution can include both products. The analysis of sales mix and production constraints is a useful way

for managers to understand both how a difference in sales mix affects income and how production

limitations and capacities can significantly affect the proper determination of the most profitable sales mix.

When there are only two products, the optimal solution can be determined graphically (see text Exhibit

11.21, by choosing one of the “corner points” from the “feasible region”).

3. Using the Solver Routine in Excel: See the Appendix to the chapter for setting up and solving a

“constrained optimization” problem, similar to the product-mix problem discussed in the chapter. Of

particular interest is the “Sensitivity Report” that accompanies the optimal solution generated by Excel.

(See Exhibit 11A.4 for a sample report.)

N. Behavioral and Implementation Issues:

1. Consideration of Strategic Objectives. A well-known problem in business today is the tendency of

managers to focus on short-term goals and neglect the long-term strategic goals because their

11-6

Chapter 11 – Decision Making with a Strategic Emphasis

compensation is based on short-term accounting measures. It is critical that relevant cost analysis be

supplemented by a careful consideration of the firm’s long-term strategic concerns. Without strategic

considerations, management could improperly use relevant cost analysis to achieve a short-term benefit

and potentially suffer a significant long-term loss.

2. Predatory Pricing Practices. The Robinson-Patman Act, administered by the FTC, addresses pricing that

could substantially damage the competition in an industry. This is called predatory pricing, and it occurs

when a company has set prices below cost and planned later to raise prices to recover the losses from lower

prices. This law is relevant for short-term and long-term pricing since it could require a firm to justify

significant price cuts.

3. Replacement of Variable Costs with Fixed Costs. Another potential incentive associated with relevant

cost analysis is for managers to replace variable costs with fixed costs. This might happen if mid-level

managers realize that because they rely on relevant cost analysis, upper management tends to overlook

fixed costs. Management’s proper goal is to maximize contribution margin and to minimize fixed operating

costs at the same time. Managers must not forget to develop methods to manage fixed costs.

4. Proper Identification of Relevant Factors. Another possible problem area of cost analysis is that

managers can fail to properly identify relevant costs. In particular, untrained managers commonly include

irrelevant, sunk costs into their decision-making. Similarly, many managers fail to see that allocated fixed

costs are irrelevant. It is easier for these managers to see the fixed cost as irrelevant when it is given in a

single sum.

Advanced Lecture Notes

The illustrations developed in this chapter have assumed that each of the cost and revenue factors in the relevant

cost analysis is known with certainty. In some situations this can be a very unrealistic assumption, as for example,

for new companies, new products, seasonal products, and so on. Rather than to simply calculate the cost and/or

income under each decision alternative based on approximated values, managers often prefer to incorporate the

uncertainty directly into the analysis. Techniques have been developed to deal with this matter; they include

simulation and analytical modeling, which are explained in the teaching notes at the end of Chapter 9 (CVP

analysis) in this guide.

Another technique for handling uncertainty is to use a probability modeling approach, as explained in the note

below. This approach is also used in Chapter 12 (Capital Budgeting) and in the appendix of Chapter 15 to

illustrate the application of the method for investigating standard cost variances under conditions of uncertainty.

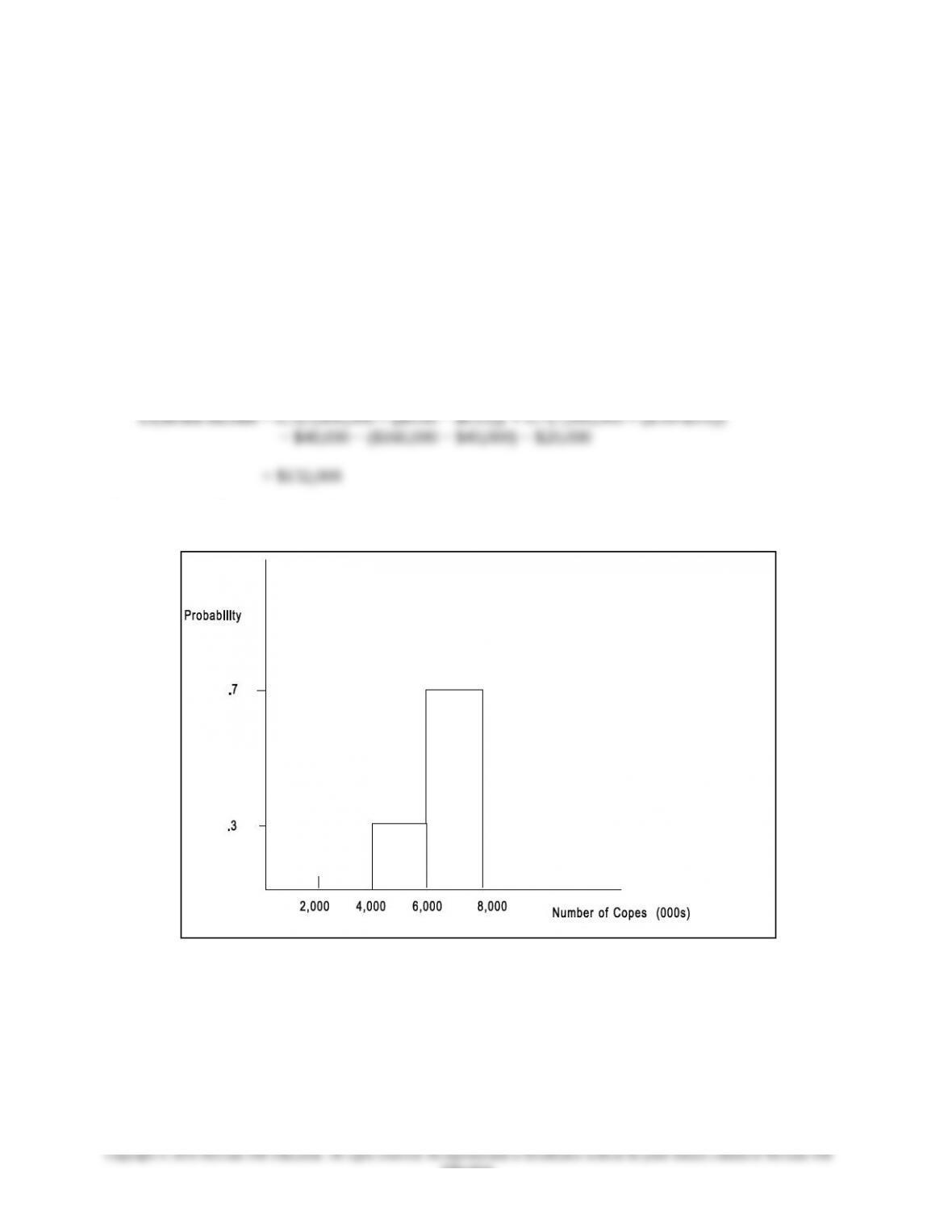

Modeling of Uncertainty in Relevant Cost Analysis

To illustrate the application of probability modeling, we consider again the example of the QUICK COPY lease or

buy decision developed in this chapter. Now suppose QUICK COPY is uncertain that the annual demand will be

6,000,000 copies, and wants to formally include this uncertainty in the analysis. The first step is to have

management describe their uncertainty in a graph; suppose what you get from this is shown in Exhibit 1. The

graph shows that management expects the number of copies will be between 4,000,000 and 8,000,000 copies and

there is a 30% chance it will be between four and six million, and a 70% chance it will be between six and eight

million copies.

Since we know from the analysis in the chapter that QUICK COPY should purchase rather than lease the copy

machine if the demand for the number of copies exceeds the indifference point of 5,000,000 copies, and since

11-7

Education.

Chapter 11 – Decision Making with a Strategic Emphasis

there is a 70% probability that the demand for copies will exceed six million copies, we can say that the

probability is at least 70% that QUICK COPY will have less cost if it purchases the new machine.

We can also give the manager a pretty good idea of expected income assuming the purchase of the machine, as

follows. First, we assume that the average price per copy is $.06, the average cost of paper per copy is $.01, and

the expected labor and other operating costs are expected to be $48,000. (Note that this information was irrelevant

for the decision about lease or purchase, since the decision would not affect price, paper cost or operating costs).

Second, with the idea that since the probability is 30% that sales will be between four and six million copies, we

say the probability is 30% that sales will be exactly five million copies (the mid-point) to simplify the analysis

(and similarly, the probability is 70% that sales will be seven million copies). Then, expected income can be found

by calculating the expected value for each of the two possible outcomes (5 or 7 million sales of copies).

Expected Income = Expected contribution less Fixed Operating Costs (Labor, Service

Contract, Depreciation)

Exhibit 1: Probabilities for QUICK COPY

This expected value calculation shows that QUICK COPY can expect income of $132,000, assuming the purchase

of the copier and given management’s probabilistic estimate of demand. This information can be used by

management in choosing whether to lease or to buy the new machine, in planning expenditures for the coming

year, and in obtaining financing for the new machine.

11-8

Education.