Chapter 10 – Strategy and the Master Budget

10-42 Activity-Based Budgeting (ABB) with Continuous Improvement (40 Minutes)

1. Unit-Level: Pick packing, Data entry—Lines

Batch-Level: Requisition handling, Data entry—Requisitions,

Desktop delivery

2. Budgeted cost for each activity and for the division as a whole, February &

March:

Budgeted cost-driver rates:

Cost-Reduction Cost-Driver Rates

Activity Rate (per month) January February March

Requisition Handling 98% $12.50 $12.250 $12.0050

Pick Packing 99% $ 1.50 $ 1.485 $ 1.4702

Budgeted Costs by Activity and for the Division as a whole, February and March:

Activity

Activity Volume February March

Requisition Handling 30,000 $ 367,500 $ 360,150

Pick Packing 800,000 $1,188,000 $1,176,120

Data Entry—Lines 800,000 $ 633,600 $ 627,264

3. Factors that may influence the success of a continuous-improvement (Kaizen)

program include:

Reasonable or achievable cost reductions.

Awareness of all employees on the expected (scheduled) cost

improvements over at least the immediate future periods.

10-40

Education.

Chapter 10 – Strategy and the Master Budget

10-42 (Continued)

4. Primary criticisms of Kaizen (continuous-improvement) budgets include the

following:

The budgeting process tends to place enormous pressure on employees

to reduce all costs, which can lead to employee “burnout.”

10-41

Education.

Chapter 10 – Strategy and the Master Budget

10-43 Time-Driven Activity-Based Budgeting (TDABB) (60 minutes)

1. Calculation of budgeted resource costs per hour (at practical capacity):

Practical Budgeted

Budgeted

Capacit

y Cost per

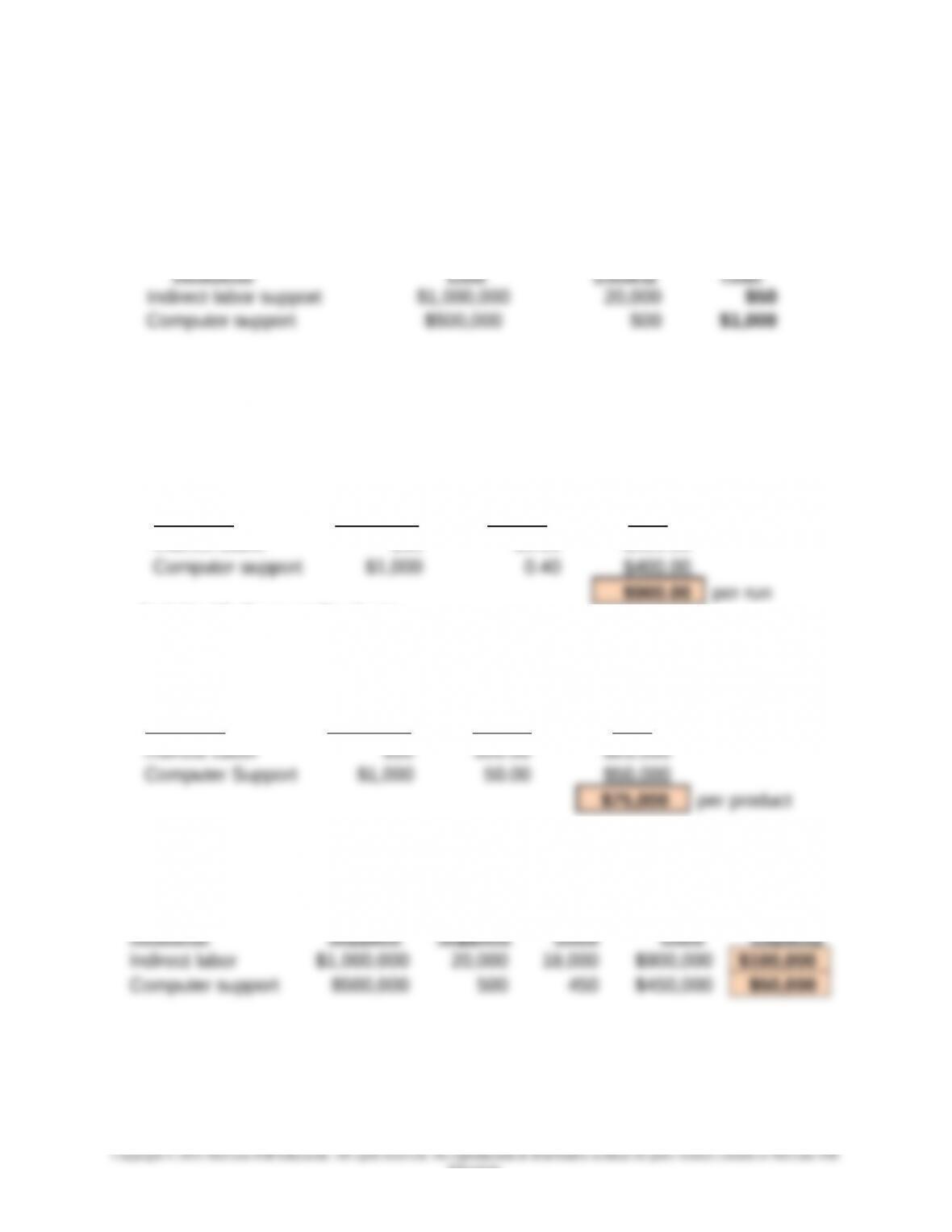

2. Cost-driver rates for each activity (handle production runs, and support product):

Activity #1: Handle Production Runs

(From 1

above) Unit Budgeted

Budgeted Times Cost-Driver

Resource Cost/Hour (hours) Rate

Indirect Labor $50 10.00 $500.00

Activity #2: Support Products

(From 1

above) Unit Budgeted

Budgeted Times Cost-Driver

Resource Cost/Hour (hours) Rate

3. Cost of unused capacity for the quarter, by resource:

Cost of Resource Resource Cost of Cost of

Resource Units Units Resources Unused

10-42

Education.

Chapter 10 – Strategy and the Master Budget

10-43 (Continued)

Generally speaking, the cost of unused capacity should not be assigned to

actual units produced or customers served during the period. However, the cost

of unused capacity should not be ignored–it is someone’s responsibility in the

organization. That is, the cost of unused capacity for a period should be

4. After implementing a TQM program, the company was able to implement process-

efficiency changes, the end result of which was a 10% reduction in the indirect labor

time associated with the activity “handling production runs.” Re-estimate the indirect

labor cost component of the cost to handle a production run. Also, recalculate the

Revised Budgeted Cost-Driver Rate: Indirect labor support for “handling a production

run”:

Unit Budgeted

Budgeted Times Cost-Driver

Revised Cost of Unused Capacity–Indirect Labor Support Cost:

Cost of

Resourc

e

Resourc

e Cost of Cost of

Resource Units Units Resources Unused

Resourc

As can be seen, the efficiency gain resulted in “freed-up” indirect labor resources,

which are now available for use elsewhere in the company. In the event that

alternative uses for this labor cannot be found, then management faces the issue

10-43

Education.

Chapter 10 – Strategy and the Master Budget

of whether to reduce its workforce. Also, the reduced cost-driver rate ($50

reduction) would be of potential strategic use to management, for pricing and

product promotion purposes.

10-44 Rolling Financial Forecasts (25 minutes)

1. “Rolling forecasts” of sales:

Month of Forecast for Month of

Forecast January February March April May June

December 100 95 100 110 120 125

January 90 100 105 110 120

2. Three-month forecast error rates, March through June. (Note: Error rate = 1 –

absolute forecast error.) For example, the forecast error rate for March’s sales is

found by dividing the absolute value of the forecast error for this month by the actual

volume for that month provided three months earlier (i.e., December).

January February ___March April May June

Actual Sales 98 95 92 108 98 100

Forecast error rate – – 8.70%11.85% 22.45% 25.00%

Direction of error – – Below Below Below Below

10-44

Education.

Chapter 10 – Strategy and the Master Budget

10-45 Resource Capacity Planning/ABC (25 minutes)

1. Likely result of the decision to raise prices?

Recalculated fixed operating cost per meal, based on available capacity (meals per

If demand (e.g., because of competitive pressures) should drop even further and the

daily fixed operating cost per meal recalculated again, based on the lower demand,

then the average fixed cost per meal (and total cost per meal) would increase even

further. Perhaps the owners would be tempted to raise prices once again, in an

attempt to recover “cost.” In all likelihood, however, the rising prices of meals would

exacerbate the situation, leading the business to a downward (or what some refer to

as “death”) spiral.

2. Alternative approach for allocating daily fixed operating cost to each meal:

The owners of this business should consider calculating the fixed operating cost per

meal based on “practical capacity.” This practice would avoid the downward business

spiral referred to above and attributable to an escalating “cost” per meal. In fact,

using some notion of capacity would allow the owners to make an assessment of the

10-45

Education.

Chapter 10 – Strategy and the Master Budget

10-46 Kaizen Budgeting (50 minutes)

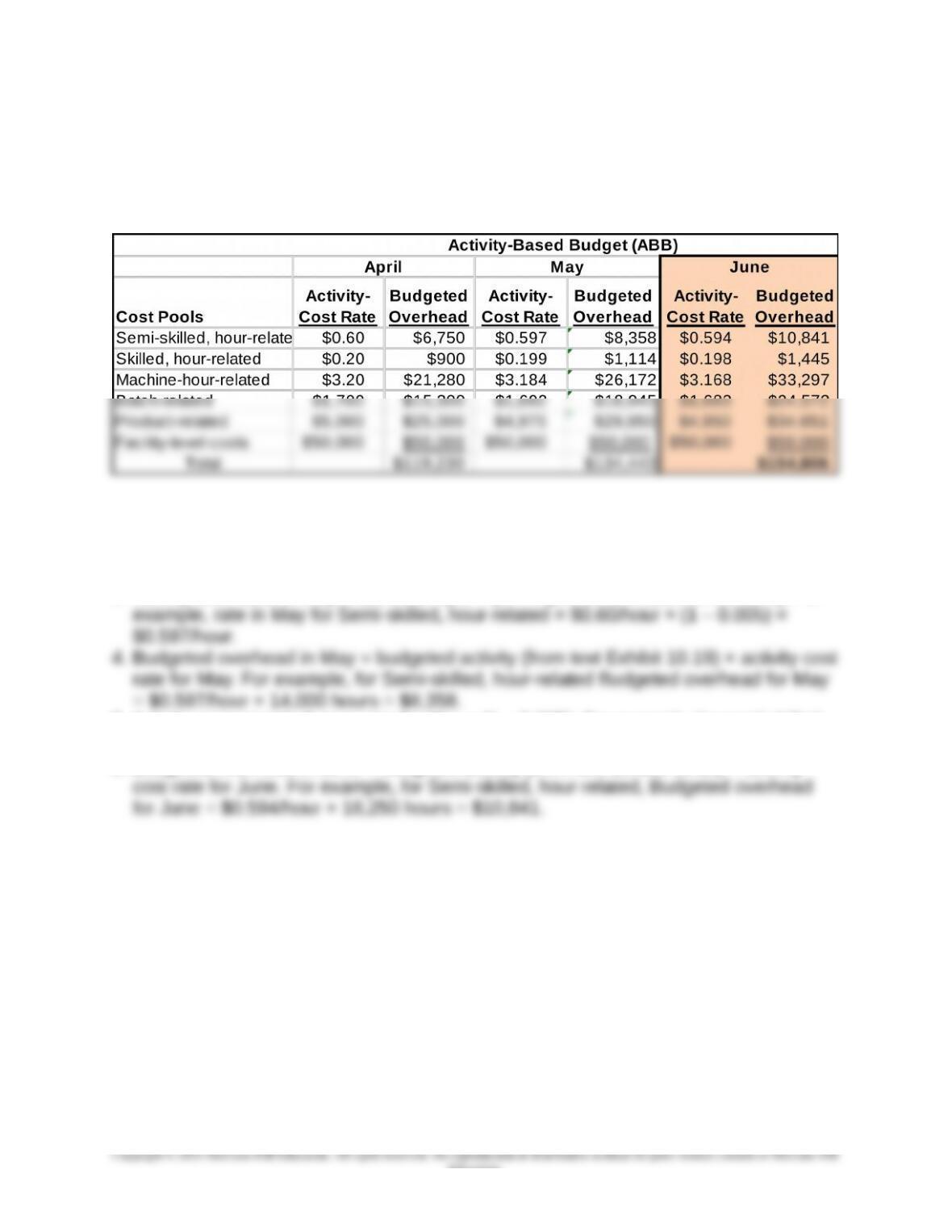

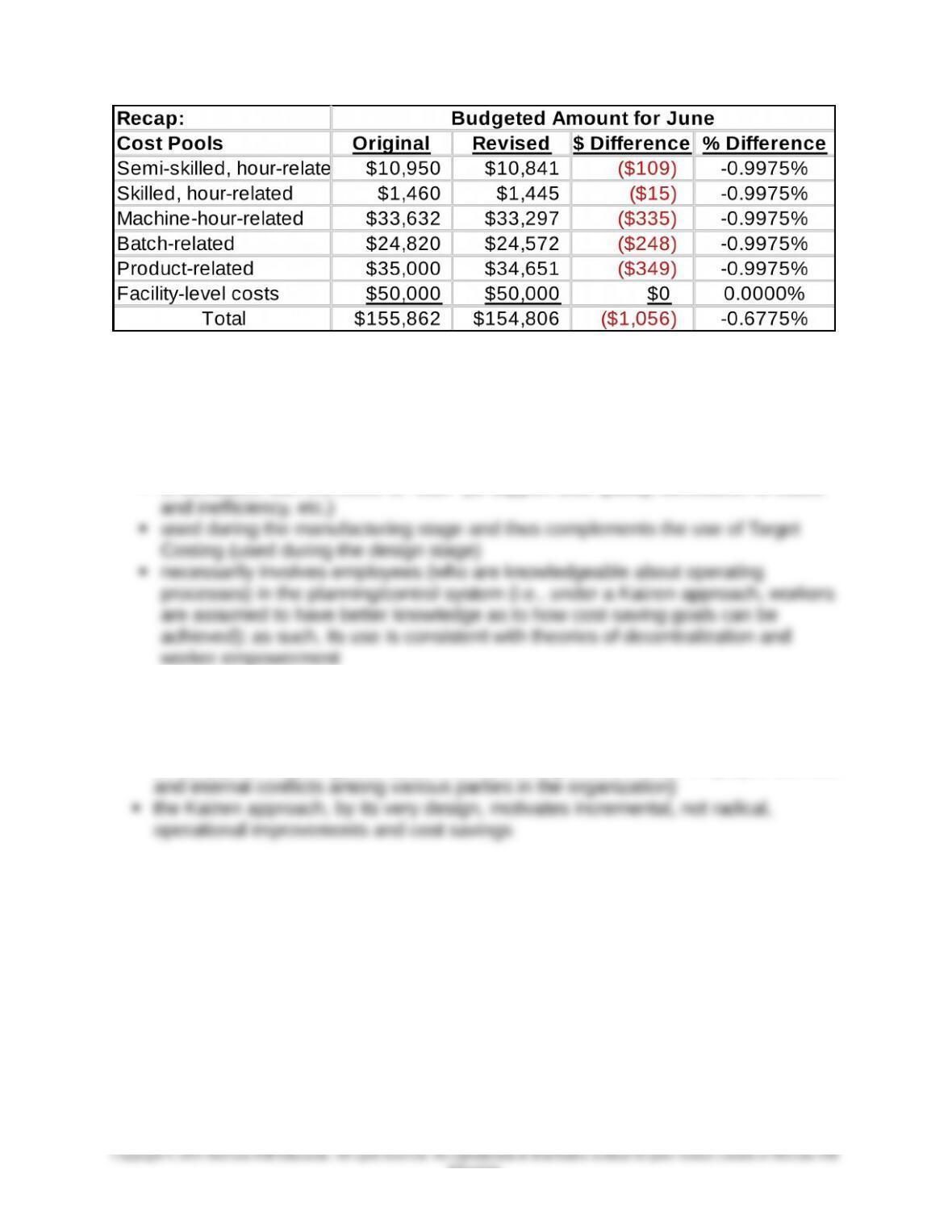

1. Recalculated budgeted factory overhead cost for June, under the assumption that,

starting in May, each budgeted cost-driver rate decreases by 0.5% relative to the

preceding month.

Sample Calculations:

1. Activity cost rates in April: Given (text Exhibit 10.19)

2. Budgeted overhead in April: Given (text Exhibit 10.19)

3. Activity cost rates in May: Rate from April × (1 – improvement rate/month, 05%). For

5. Activity cost rates in June = rate for May x (1 – 0.005). For example, for semi-skilled,

hour-related, June’s activity cost rate = $0.597/hour × (1 – 0.005) = $0.594/hour.

6. Budgeted overhead in June = budgeted activity (from text Exhibit 10.19) × activity

10-46 (Continued-1)

10-46

Education.

Chapter 10 – Strategy and the Master Budget

2. In general, the benefits associated with a move to continuous (i.e., Kaizen) budgeting

include the following:

helps ensure that the budget is a forward-looking tool

may help the organization stave off competition or otherwise secure a competitive

advantage

is consistent with the move to “lean” (to support total quality, elimination of waste

3. Principal concerns or limitations associate with Kaizen budgeting:

a Kaizen approach places pressure on employees to meet continually revised (and

stricter) performance goals; dysfunctional consequences include employee burnout

4. Examples of how Kerry Company could realize the cost savings referenced above in

Requirement 1: the activity cost rates are calculated as budgeted spending (on

resources) divided by the practical capacity (i.e., supply) of resources acquired.

Therefore, the rate can go down either because total budgeted spending is decreased,

or the supply of activities is increased while holding spending constant. Both would

seem to rest on notions of increasing efficiency. Some examples, referenced to text

Exhibit 10.19 might include the following:

10-47

Education.

Chapter 10 – Strategy and the Master Budget

10-46 (Continued-2)

move to a JIT production system

incorporate technology into (i.e., automate) the order-processing system used by

effecting changes in the layout of the facility (e.g., to reduce movement and

storage of inventory

Notice, too, that in order to reduce spending (on resources), management has to take

direct and deliberate action to do so. This is due in large part because some of the

activity costs in an ABC model are considered short-term fixed costs. As such, the only

10-48

Chapter 10 – Strategy and the Master Budget

10-47 Budgetary Slack and Zero-Based Budgeting (ZBB) (30 minutes)

1. Budgetary slack is a planned difference between budgeted revenue and expected

revenue, and/or budgeted expenditures and expected expenditures. Budgetary

slack describes the tendency of managers to under-estimate revenues and over-

2. a. From the point of view of the business unit manager, budgetary slack provides:

performance that will “look better” in the eyes of their superiors

evaluate the performance of subordinates and to use the budget as a control

mechanism over subordinate performance.

b. From the perspective of corporate management, the use of budgetary slack

increases the probability that budgets will be achieved. This increased

probability facilitates the overall corporate budgeting process. Corporate

management may also allow budgetary slack as a form of reward to managers

for previous good performance.

However, from the point of view of corporate management, the use of budgetary

3. a. Zero-based budgeting (ZBB) is a budgeting technique that evaluates all

proposed operating and administrative expenditures as though they were being

b. Atlantis Laboratories could benefit from ZBB as each of the business unit

10-49

Education.