Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18-56 (continued -1)

There are at least two possible approaches:

1. develop a charge-back system for printing and duplicating,

so that each of the users of this service will be directly charged for the

service. The effect will be to reduce demand of printing and

2. make the printing and duplicating department a profit center.

Allow users to purchase printing and duplicating services outside the

firm. This will take the charge-back idea in (1) above one step further.

Now, in addition to reducing demand, there is an incentive for the

printing and duplicating department to recruit services from the other

18-71

Education.

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18-57 Design of Strategic Business Unit (30 min)

This short case is intended to provide a basis for discussion of

the situation where a support function might be viewed as simply an

important resource, or alternatively, it might be viewed as having a

critical strategic role in the bank. Cost centers are more often viewed

as resources, while profit centers are more often viewed as having a

strategic role in the success of the firm. This discussion is played out

in the context of an information services department.

The information services department is a cost center, and the

case description suggests that management is principally concerned

about the costs incurred in that department. Information services is

viewed as a critical resource to support the growth of the firm. The

wider and more extensive use of information services, to provide the

desired integration of information services into the firm. Alternatively,

information services might be viewed as a profit center, to enhance its

role in the firm, and to more clearly define the benefits obtained. The

profit center also sets out a higher expectation for the unit. Can it

compete with services provided outside the firm? Can it develop

internal (and external) customers on the basis of quality service and

low cost?

Another way to use the case is to develop a discussion of the

appropriate allocation method, based on the assumption that

information services will be a cost center. Here the discussion should

be much like that for 18-55 above. The only difference is we are now

talking about information services instead of maintenance.

18-72

Education.

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18-58 Profit Centers: Hospitals (20 min)

If all of the service lines are charged the same percentage for

Guest Services, then managers and employees will not really monitor

their use of Guest Services and may even tend to overuse the

service. However, this method may help the most in improving

patient relations and customer service because these objectives will

be supported by all of the service lines utilizing this department. If

18-59 Performance Measurement; Balanced Scorecard; Hospital (20

min)

1. The number of perspectives was likely reduced to further refine the

focus of the scorecard and the performance measurement system. Too

many perspectives and critical success factors could reduce the desired

through improved operations, and the combination of the two provide

greater focus on operational improvement. The remaining four

perspectives could be related to the conventional balanced scorecard in the

following way:

Perspectives in the BHHS and Conventional Balanced Scorecard:

BHHS Scorecard (2001) Balanced Scorecard

Organizational Health Learning and Innovation

18-73

Education.

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18-59 (continued -1)

2. The CSFs used by BHHS in the 2000 BSC include the following:

Organizational

Health

percentage of employee development plans in

place, number of employee survey action plans, job

vacancy rates, turnover rates

Process

Improvement

operating room turnaround time, number of

physicians using online hospital clinical information

systems

cost per discharge

3. The scorecard perspectives appear to be correctly aligned with the

mission statement which has goals for improvement in terms of patient

care, physician satisfaction, and overall staff satisfaction. The

perspectives of process and quality improvement should support the

satisfaction of patients, while the focus on the organizational health

18-74

Education.

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18-59 (continued -2)

4. The strategy map is likely to follow the sequence of perspectives

provided in the article.

Organization Health, as the foundation of the

strategy map, supports…

5. It is unlikely that a profit center approach alone would be able to

capture the breadth of goals that BHHS has. In this case, because of the

Source: “Journey to Destination 2005,” by Andra Gumbus, Bridget Lyons,

and Dorothy E. Bellhouse, Strategic Finance, August 2002, pp. 46-50.

18-75

Education.

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

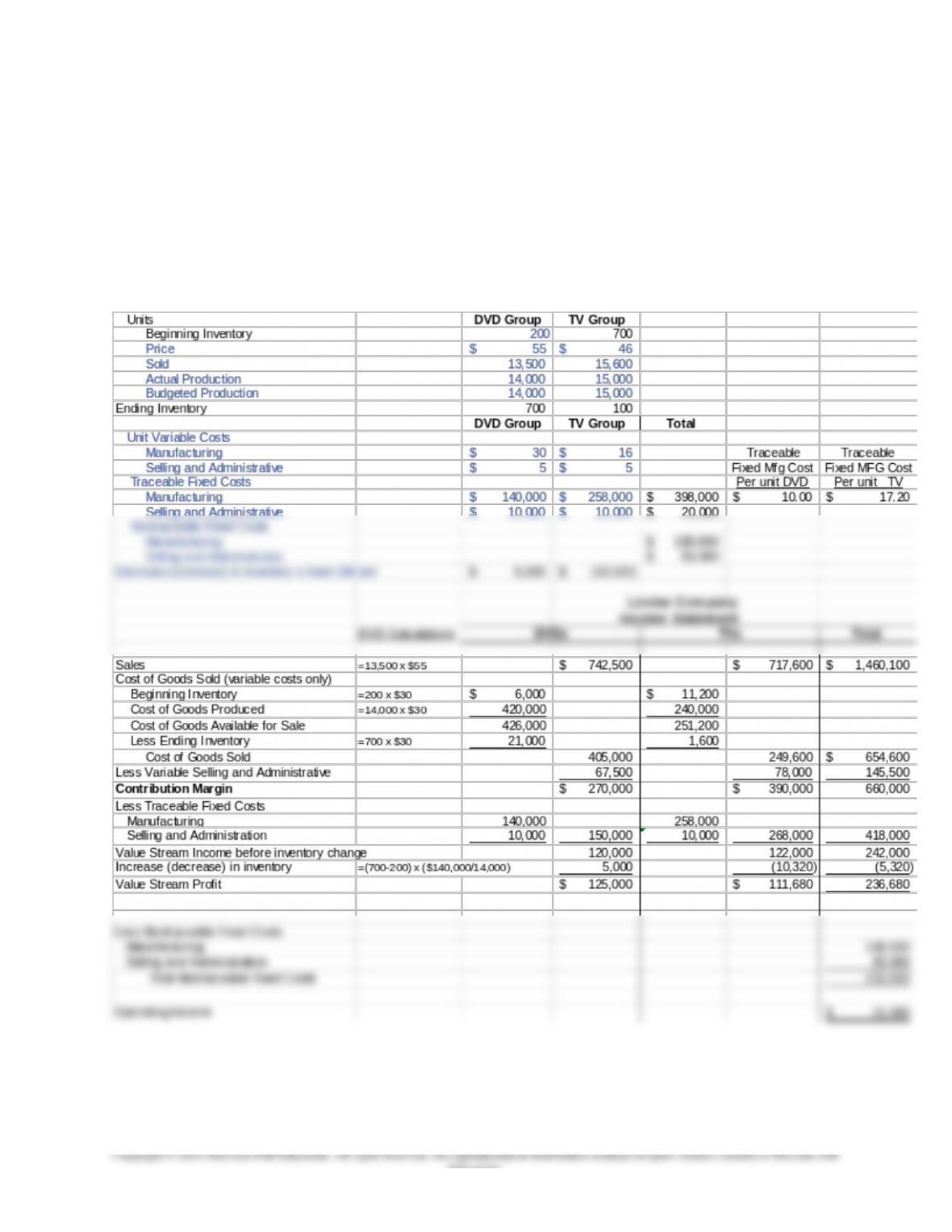

18-60 Value Streams and Profit Centers (30 min)

1. The value stream income statements for the two value streams of

Levine Company is shown below. The value stream income

statement is based on a contribution type income statement (variable

costing-based) to which is added the effect of a change in inventory

level on income, thereby converting the variable costing income

statement to a full cost statement.

18-76

Education.

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18-60 (continued -1)

Note that the effect on value stream income of a change in inventory

is displayed separately in the income statement; there is a $5,000

increase in income for the DVD group (because of an increase in

that nontraceable fixed costs are not allocated to the value streams

but are subtracted from total company profit to produce a total

2. The value stream income statements show that both value streams

are profitable though the DVD value stream has a higher value

Levine is in.

3. The value stream income statement is a combination of the variable

costing and full costing income statement that shows as a separate

line item in the statement the effect of inventory change on income.

For a useful reference on lean accounting and value streams, see:

Frances A. Kennedy and Peter C. Brewer, “Lean Accounting: What’s it All

About,” Strategic Finance, November 2005, pp. 27-34.

18-77

Education.

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18-61 Cost Centers; The Finance Function; Spreadsheet Application

(25 min)

The data are for selected countries from the A.T. Kearney 2007 survey.

1. There are a large number of strategies for ranking the countries, so there

are a number of possible rankings. Here are a few ways to develop the

ranking:

1. Sum the three criteria and then rank the countries on this number;

this would be useful if the criteria are equally weighted, though the

weight since it is scored on the range 0-4 while the other two are

scored on a smaller range, 0-3.

2. Weight the three criteria; for example, if the firm is interested

could be given higher weight.

3. One or more of the measures could be required to achieve a

certain level (for example, skills availability must be above 1.0);

A variety of different ranking methods are possible. The following ranking is

developed using the approach that is similar to the third approach above.

A country is deleted if business environment is less than 1.5 or skills

are shown below.

18-78

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18-61 (continued -1)

The results show that China is the most highly ranked and Thailand,

Bulgaria and Malaysia are a close second. China’s relatively low scores on

financial attractiveness and business environment are more than made up

for by the highest score on skills availability. A firm should carefully

brought new (opposition) leadership to the country that is civilian and

democratically-elected. Also, in 2011 Thailand is suffering from disastrous

flooding. The 2011 measure of business environment might be somewhat

lower than for 2007.

2.

Strategic issues to consider in the potential outsourcing of the finance

function include:

Before choosing to outsource, the firm must first determine if the finance

function is strategically critical in day-to-day decision making. This would

be true for example if the firm operated in a dynamic, differentiated market,

18-79

Education.

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18-61 (continued -2)

function is to pay the bills and record customer payments and the like, then

outsourcing to a reliable, low cost provider makes sense.

If the decision is made to outsource, then additional measures of the

country’s suitability should be considered. These could include political

Reference: Kate O’Sullivan, “Where in the World is Your Offshore Finance

Team?” CFO.com, January 31, 2008. Source cited: A. T. Kearney Global

Services Location Index.

18-80

Education.