Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit Analysis

Chapter 9

Short-Term Profit Planning: Cost-Volume-Profit Analysis

Teaching Notes for Cases

Case 9-1: CVP Analysis; Strategy

This problem can perhaps be visualized most easily by first constructing a table that shows the effects on

pre-tax income of the various alternatives.

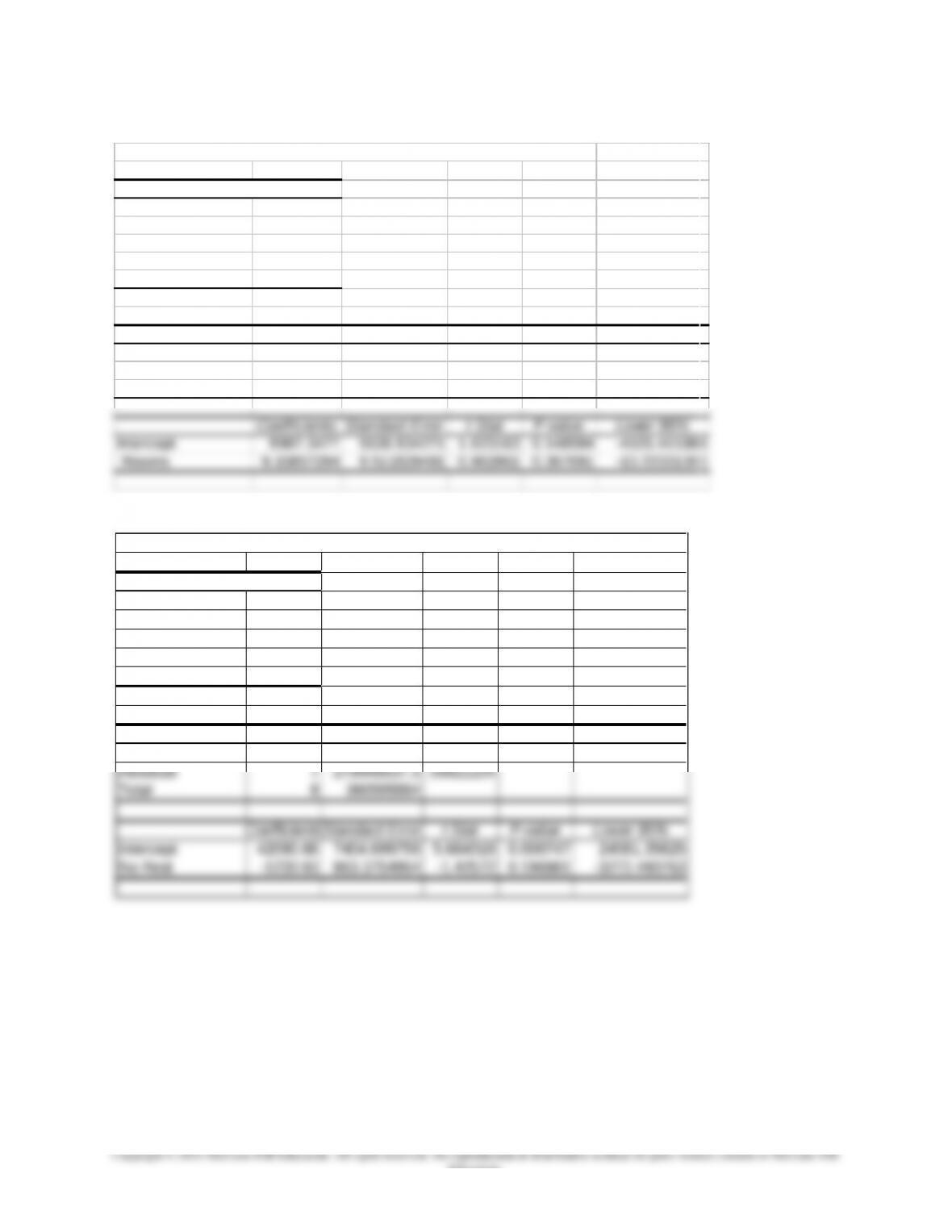

Prior Year Keep Old Use New Purchase

& Budgeted Carrier Carrier Trucks

Sales $1,500,000 $1,500,000 $1,430,000 $1,430,000

Shipping Costs 135,000 (a) 147,150 (b) 122,909 (c) 109,395

Other Variable Costs 1,095,000 1,095,000 1,043,900 1,043,900

Contribution Margin $270,000 $257,850 $263,191 $276,705

Fixed Costs 150,000 150,000 150,000 ?

1. Using the breakeven equation:

$47,050.

2. Again we use the breakeven equation, substituting for required income the expected income using the

new carrier (computed previously).

$1,430,000 = [$109,395 + $1,043,900] + [X + $2,000 + $150,000] + $113,191

9-1

Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit Analysis

3. Based on Mr. Carter’s decision, it is evident that the trucks could not be purchased for $115,000, much

less for $47,000. Using a new carrier was the economically advisable decision. Unfortunately it appears

that another variable, carrier reliability, was not taken into account. Possibly the best decision was to keep

using the old carrier. The so-called “safety margin” can be computed as follows:

4. Simmons is best characterized as a differentiator because of its emphasis on service and on-time

delivery. However, the fact that the increase in shipping rates would mean that Carter would not meet his

profit goals suggests that the market is also somewhat price sensitive. It is likely that on balance, Carter

5. Value chain analysis is useful for identifying the critical value-adding activities in the firm, and for

analyzing the effect of these activities upstream and downstream in the firm. For example, the value chain

can be used by Carter to help determine whether insourcing the shipping function might have the effect of

9-2

Education.

Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit Analysis

Case 9-2: CVP Analysis; Review of Cost Estimation

1. Note that the data for competitor 9 must be discarded as it represents a partial year and is therefore not

comparable with the remaining data. For the first question, a regression on net income (dependent

variable) against total revenue (independent variable) is shown in Exhibit 1:

The regression equation is:

The above equation has an R2 of 0.45, the standard error of the estimate is $19,022,030, and the t-value is

2.40. That is a good fit considering that we would expect the fit to be affected by a variety of factors

affecting revenue. On average it appears a casino must generate revenues of $169,396,875 (= $48,955,697

÷ 0.289) to breakeven.

2. Regress casino revenues (dependent variable) against square footage of casino space (independent

variable).The resulting equation is shown in Exhibit 2.

space. But an even more important issue is: if the two variables are related, which causes which? It is

more plausible that higher revenues lead to the construction of more space, rather than more space

generating higher revenues. Thus any relationship found to hold must be used cautiously in making

revenue predictions.

3. The results are shown below. The fit of both models is extremely poor, with R-squared values of less

9-3

Education.

Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit Analysis

9-4

Education.

Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit Analysis

Regression Using Number of Rooms to Predict Room Revenue

Regression Statistics

Multiple R 0.34198458

R Square 0.11695346

Adjusted R Square -0.0091961

Standard Error 2800.47961

Observations 9

ANOVA

df SS MS F Significance F

Regression 1 7270969.691 7270970 0.927102 0.367691352

Residual 7 54898802.31 7842686

Total 8 62169772

Coefficients Standard Error t Stat P–value Lower 95%

Intercept 8987.3477 5536.934271 1.623163 0.148584 -4105.411988

Rooms 9.15857294 9.511829491 0.962861 0.367691 –13.33331366

Regression Using Number of Restaurants to Predict Food and Beverage Revenue

Regression Statistics

Multiple R 0.47438

R Square 0.225037

Adjusted R Square 0.114327

Standard Error 6318.325

Observations 9

ANOVA

df SS MS F Significance F

Regression 1 81147246.68 81147247 2.032684 0.196980598

Residual 7 279448637.3 39921234

Total 8 360595884

Coefficients

Standard Error

t Stat P-value Lower 95%

Intercept 42090.68 7404.699759 5.684319 0.000747 24581.35625

No Rest -1230.93 863.3754864 -1.42572 0.196981 -3272.490763

Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit Analysis

Case 9-3: CVP Analysis; Service (Hospital); Strategy

1. The strategic role of CVP Analysis for Melford Hospital is to provide a basis for understanding

the relationships between costs, revenues, profits and the level of output for the hospital’s

services. In this case, the hospital needs to be able to analyze the alternative uses of its space for

rental. Will the space be more profitably used by activities within the hospital? What is the proper

2. The breakeven point is determined as follows:

Total Fixed costs:

Melford Hospital charges $2,900,000

Supervising nurses ($25,000 × 4) 100,000

Nurses ($20,000 × 10) 200,000

Aides ($9,000 × 20) 180 ,000

Total fixed costs $3,380,000

Contribution margin per patient-day:

Revenue per patient day $300

Less: Variable costs per patient-day

3. Calculation of Loss from Rental of Additional 20 Beds

Increase in revenue (20 additional beds × 90 days × $300 /day) $540,000

Increase in expenses:

Variable expense by Melford Hospital

(20 additional beds × 90 days × $100/day) 180,000

Fixed charges by Melford Hospital

($2,900,000 ÷ 60 beds = $48,333 per bed × 20 beds) 966,667

Salaries expense:

9-6

Education.

Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit Analysis

Case 9-4: ALLTEL Pavilion

1. The best description of the strategy of an entertainment business such as the ALLTEL Pavilion is

differentiation. The mission statement includes: “a concert… it’s better live.” A live concert is certainly

not the least expensive entertainment. What brings a customer to the ALLTEL Pavilion is top name acts

and the experience of enjoying previous shows. The Pavilion knows that and strives to make every

customer’s experience a pleasant one.

Some students may argue that the Pavilion employs both differentiation and low price strategies –

the differentiation strategy for nationally well-known performers and low price for local or regional

talents. Even though the ticket prices for less popular artists are relatively low, attending a concert is not

2. The determination of the breakeven point is not straight-forward. It requires the student to understand

how both types of customers contribute to the Pavilion’s profits – the paying ticket holders and the comp

ticket holders. To determine the breakeven point:

Since there are many different types of tickets, the best approach is to use total revenues and total variable

costs, rather than to use per capita figures. This means using the contribution margin ratio or the variable

cost ratio. First determine total variable costs and total fixed costs as follows.

Begin by separating parking, concession and merchandise costs into their variable (10% of revenue) and

fixed components:

Variable Fixed

Total (from

Flash Report)

Parking 0.1 × 19,767 = $1,977 $4,448 − $1,977 = $2,471 $4,448

Other

variable

costs

$14,323

Guarantee $160,635

Production 15,506

9-7

Education.

Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit Analysis

This is approximately $285,453 ÷ ($26.99 + 1.91 + 7.66 + 3.52 = $40.08) = 7,122 ticket holders, at

the $26.99 average per capita revenue from ticketing and assuming the per capita revenues for

parking, concessions, and merchandise

Alternatively,

The above approach ignores the contribution of “comp” tickets and uses only paying ticket holders.

However, comp patrons should not be ignored because the also pay for parking and buy food and

merchandise. Thus, a preferred approach would be to include directly in the analysis the fact that

“comp” ticket holders will pay for parking, food, and merchandise, as follows:

a) The contribution per paying customer is $37.03 = $42.08-$3.049

b) The contribution for each comp customer is $10.04 = $13.09 – $3.049, where $13.09 = $1.91 +

Assumptions and Discussion Points

The above analyses assumes a constant purchase mix of ticket types, as set out in Exhibit A. Also, there

are a number of other key assumptions.

1. Our solution assumes that the $1.74 of other variable expense applied to both paying ticket

holders and comp ticket holders. That is, the COGS for the concessions and insurance are applicable to

each customer, whether paying or not. Some students will note that the Flash Report provided to me by

Alltel Pavilion staff is inconsistent with this because it shows project variables expense of $1.74 × 8,251

= $14,323. The Alltel staffs’ calculation seems to imply that only paying customers cause these costs. I

decided to leave this discrepancy in the case to add some realism—I can add it to the class discussion and

use it to reinforce the importance of accuracy and consistency; depending on my goals for the class I

2. In my experience with the case, a number of students will assume the costs provided in the

Flash Report for the ancillaries (parking, food, and merchandise) are fixed costs only. I remind them of

9-8

Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit Analysis

the case information that states that the concession contractors are paid on a basis of both a fixed fee and

a percentage of revenue (and therefore a variable cost). After a question or two the class seems to then

understand this point.

3. Relatively few students attempt to account for the ancillary revenues from the comp ticket

Note that the $17.63 per ticket holder calculated in the flash report just above the facilities charges is in

error; it is apparently calculated from the total admissions of $182,479 (a correct number) by the drop

Also, note that the fact there are extensive key assumptions and a significant amount of uncertainty

involved in the case, the calculation of a breakeven point must be accompanied by a caution regarding

these uncertainties. It also argues for an explicit sensitivity analysis, as described in the answer to

question 4 below.

3. This question explores the relevance of operating leverage for the Alltel Pavilion. The breakeven

analysis is likely to be more important for a fixed fee type of performer because the fixed costs

(performer fee included) will be larger, and the risk of loss from poor attendance is greater. For this

reason, including the greater difficulty in attracting fans to the relatively weaker fixed-pay performers, the

per-capita artists are likely to be preferred.

We can also look at this question from both the Pavilion’s and the Performer’s point of view:

From the Pavilion’s Point of View:

For the more popular performers for whom we expect to fill all the seats, the Pavilion would

prefer to have a fixed pay contract, to take advantage of operating leverage–the profits to the Pavilion

would be relatively high if variable costs are low (i.e., with a fixed rather than a per capita contract) and

From the Performer’s Point of View:

The popular performer is likely to be able to insist on the type of contract that is preferable the

them, presumably either a per capita type of contract or a fixed pay contract that has a very high fixed pay

amount (the performer might calculate what the Pavilion might earn from the contract based on their

9-9

Education.

knowledge of the cost structures of Pavilions generally, and use this to negotiate with the Alltel Pavilion).

The Pavilion is likely to prefer a per capita contract with this type of performer because of the relatively

higher risk for a high fixed pay contract.

The unknown performer, in contrast, is likely to prefer a fixed pay contract to guarantee a small

or modest pay, irrespective of attendance. The Alltel Pavilion would then need to take care to make sure

that the

The Alltel Experience

Driven in part by the performer’s preferences, the Alltel Pavilion’s contracts tend to be per capita

for the most popular performers and fixed pay for the less popular performers.

4. Sensitivity analysis could be used to evaluate the risk of a potential loss on the KFBS Allstars event.

Some of the methods that might be used include spreadsheet modeling, including graphical analysis to

depict the change profits as attendance levels change and the use of spreadsheet analysis tools such as

Crystal Ball in which the user can make certain aspects of the uncertainty of the situation explicit and

then see how these risk assessments affect overall profitability.

An example of a spreadsheet model for Alltel Pavilion is shown in Exhibit TN-1. If there is sufficient

A Simulation Model of Alltel Pavilion’s Profit: Crystal Ball

As a further extension of the sensitivity analysis shown in the spreadsheet (Exhibit TN-1), and

again, if I have sufficient class time, I will demonstrate the use of the Excel Add-in Crystal Ball to

analyze the uncertainty in the case. Crystal Ball was recently acquired by Oracle, Inc., and is available for

Note: As of March 2008, the Alltel Pavilion has been renamed, and is now called the Time Warner

Cable Music Pavilion at Walnut Creek.

9-10

Education.