11-33 Special Order (45-60 min)

1. In general, relevant cost equals the sum of out-of-pocket costs (variable

+ fixed), plus opportunity cost (if any). In the present case, these costs

total $147,500, as follows:

Out-of-Pocket Costs:

Variable costs:

Manufacturing cost (@ $17 per unit) $85,000

Opportunity Cost:

No. of lost unit sales (if any) 3,000

CM per unit, regular sales:

Selling price, per unit $40.00

Variable manufacturing cost $17.00

2. Operating income with the special order will decrease by $17,500. The

only relevant variable cost is the $17 variable manufacturing cost per

full. Thus, if the special order is accepted, there would be a sales loss of

3,000 units to regular customers.

Contribution margin lost (foregone) on 3,000 units of lost sales

= (price – variable manufacturing cost – variable selling cost) × # lost

units

= ($40 − $17 − $3) × 3,000 units = $60,000

Summary of relevant costs:

Variable manufacturing costs ($17 × 5,000) $ 85,000

One-time (fixed) delivery costs 2,500

11-33 (Continued-1)

Note that if GGI had available capacity, the only relevant cost would be

the variable manufacturing cost and the delivery cost, which would total

3. The breakeven selling price is the price that just equals total relevant

cost of the special sales order. Put another way, the breakeven price is

the selling price per unit that would leave operating income unchanged.

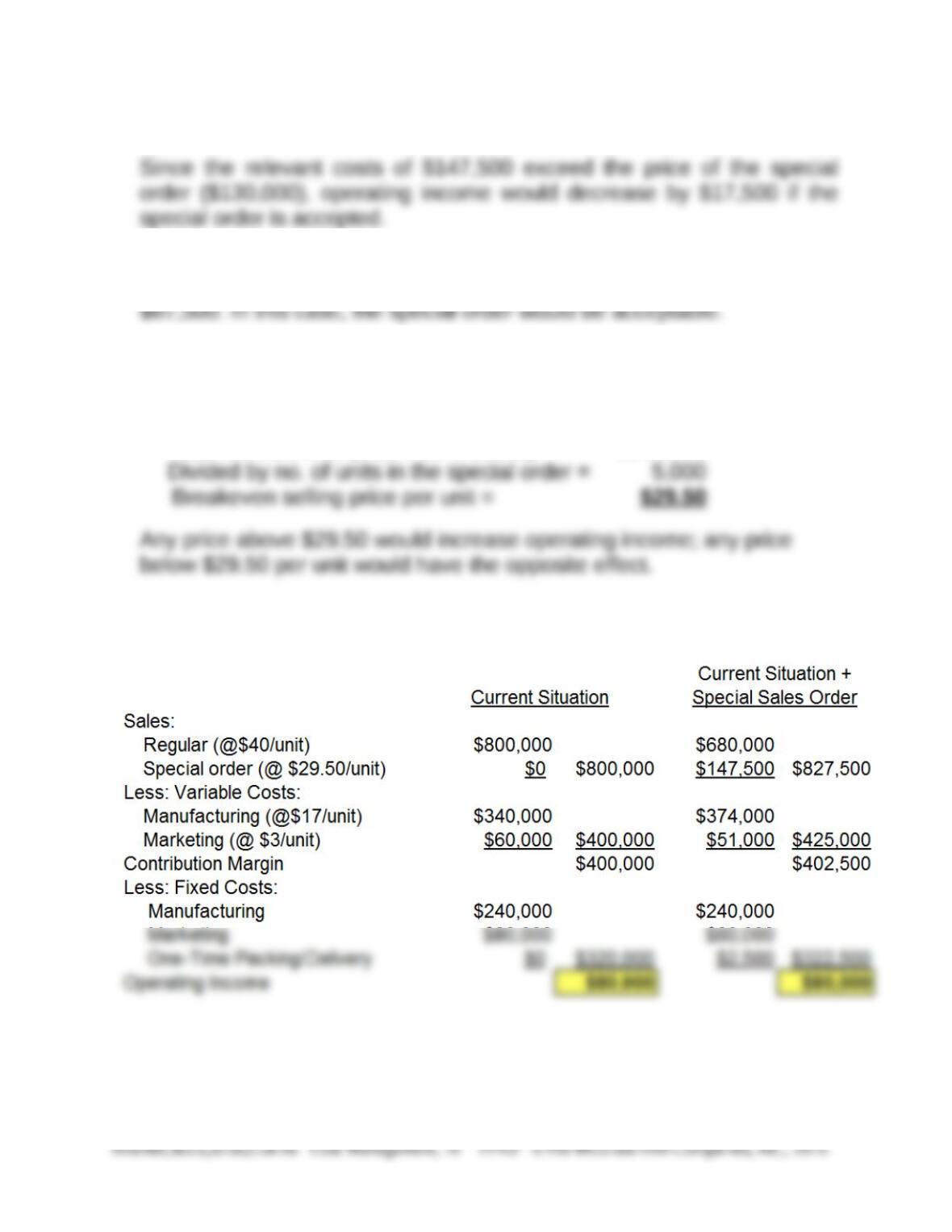

Total relevant cost (from Part 1 above) = $147,500

4. Comparative income statements (contribution format), with and without

special order:

Note: Variable selling costs ($3/unit) are not incurred on the special

sale units. Thus, if the special sales units are sold at $29.50 per

unit, operating income is left unchanged.

5. There are both ethical and strategic issues for GGI. From a strategic

view, GGI would suffer severe damage to its reputation if APAC were to

have any problems with the purity of the special order. One of the

reasons APAC has requested the special order from GGI is because of

11-34 Special Order; ABC Costing (continuation of Pr. 11-33) (30-45 min)

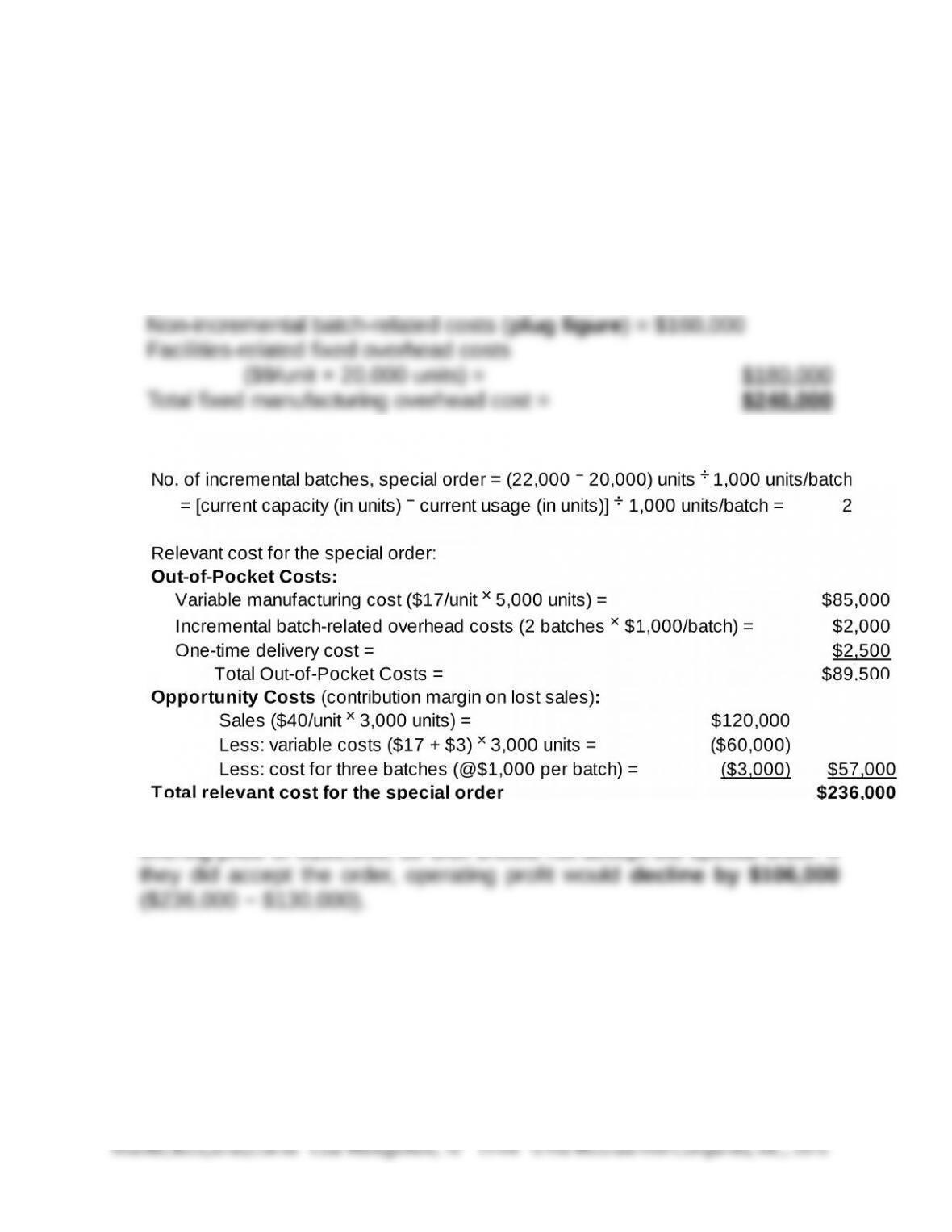

1. Total Fixed Manufacturing Cost and Breakdown into Components:

Total fixed manufacturing costs are $12/unit × 20,000 units = $240,000:

Total batch-related costs ($3/unit × 20,000 units) = $ 60,000

Incremental costs ($1,000/batch × 20 batches) = $20,000

2.

3. The

total relevant cost of $236,000 is much greater than the special order

11-35 Special Order; Strategy; International (75-90 min)

1. The standard direct labor hour (DLH) per finished valve is ½ hour.

2. The analysis of accepting the Glasgow proposal is presented below.

Totals for

Per unit 120,000 units

Incremental revenue $21.00 $2,520,000

Incremental costs

Variable costs:

Direct materials 6.00 720,000

Direct labor 8.00 960,000

Variable overhead 3.00 360,000

Total variable costs $17.00 $2,040,000

Fixed overhead:

Supervisory and clerical costs

3. The minimum unit price that Williams could accept without reducing

operating income must cover variable costs plus the additional fixed

costs; in this case, there are no opportunity costs. The $30 suggested

selling price is irrelevant for the special order:

Incremental variable costs, per unit:

Direct materials $6.00

Direct labor $8.00

Problem 11-35 (continued-1)

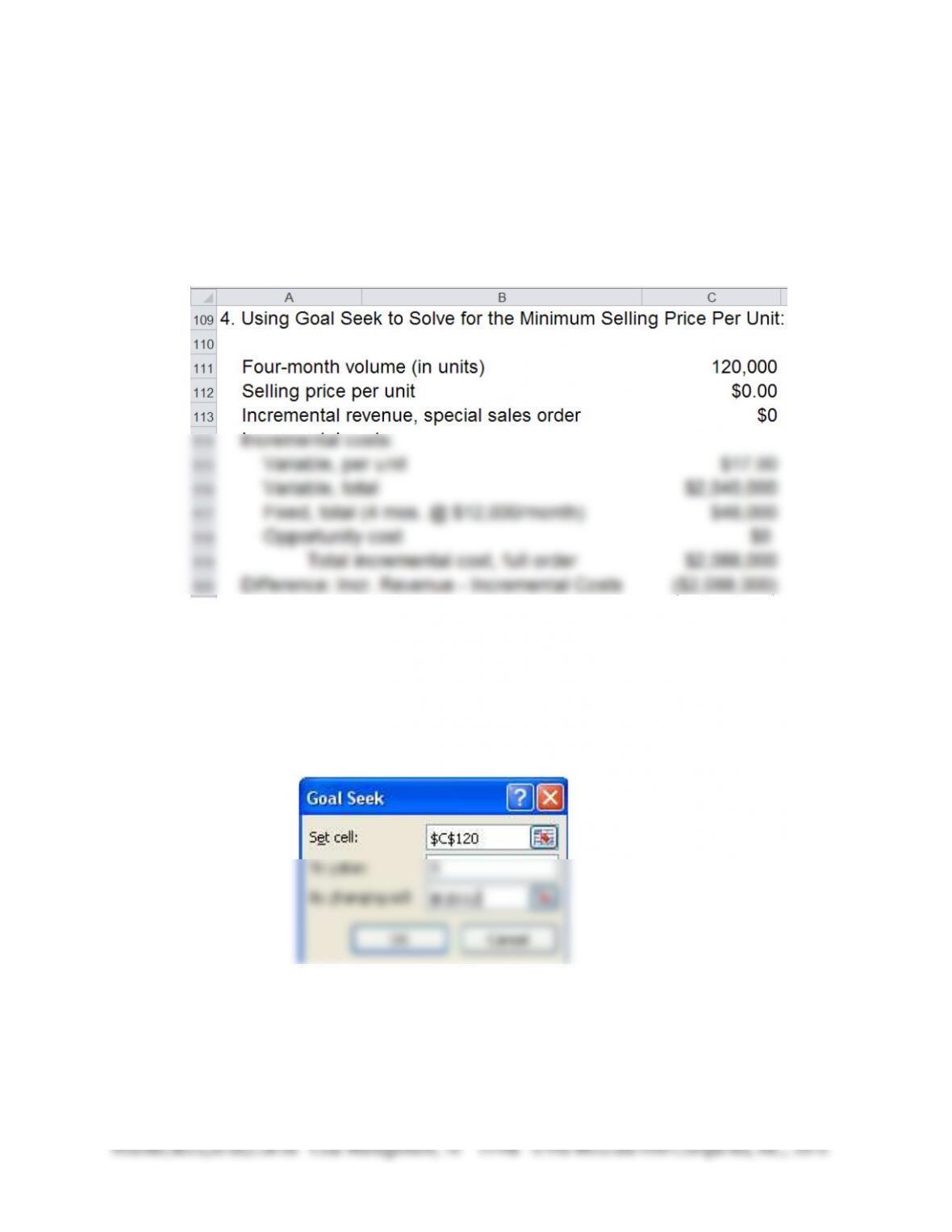

4. Use the Goal Seek option in Excel to solve for the minimum unit price

determined in 3 above.

Step #1: Define the Appropriate Equation to Be Solved

Note: the decision cell (to be solved) is C112; Cell C113 =

C111*C112; cell C115 = SUM(C85:C87); Cell C119 = C116

+ C117 + C118; Cell C120 = C113 – C118

Step #2: Run Goal Seek (to Solve the Equation)

Note: Cell C112 contains the selling price per unit; cell C120 is the

effect on operating income (i.e., the difference between

incremental revenues and incremental costs of the special

sales order).

Problem 11-35 (continued-2)

Step #3: Results

In other words, a selling price of $17.40 exactly offsets incremental

costs of the special order, resulting in a net change of $0 in terms of

operating income.

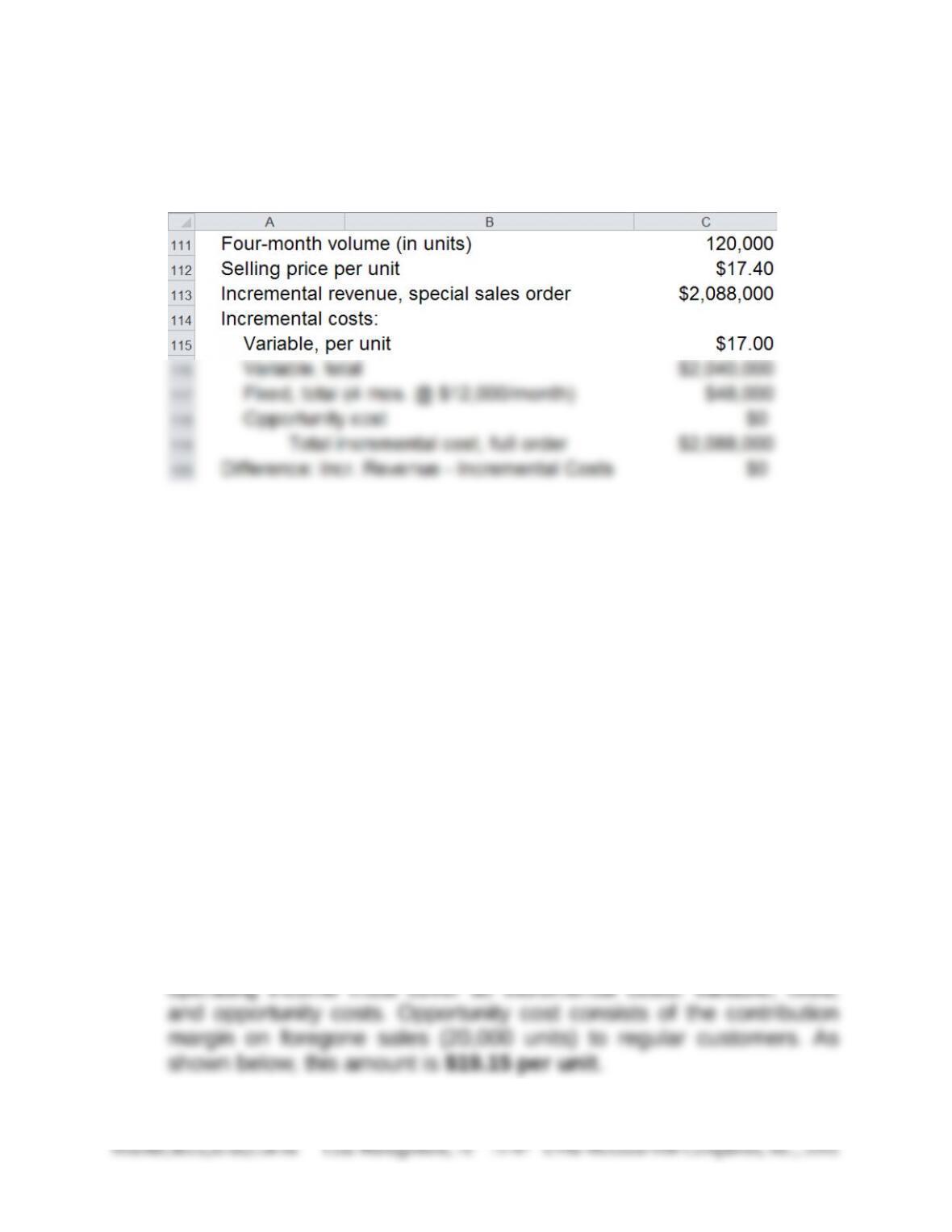

5. Determination of minimum (i.e., breakeven) selling price per unit in

the face of opportunity costs (lost sales to regular customers):

The minimum unit price that Williams could accept without reducing

Problem 11-35 (continued-3)

Incremental variable cost, per unit:

Direct materials $6.00

Direct labor $8.00

Variable overhead $3.00 $17.00

Incremental fixed costs, per unit ($48,000 ÷ 120,000 units) 0.40

Opportunity Cost:

Total lost sales (in units) (4 × 5,000 units) 20,000

Regular selling price per unit $30.00

Less: variable costs (per unit):

Direct materials $6.00

Direct labor $8.00

Variable manufacturing overhead $3.00

6. Williams Company should consider the following strategic factors before

accepting the Glasgow Industries order:

The effect of the special order on Williams’ sales at regular

prices.

The possibility of future sales to Glasgow Industries and the

effects of participating in the international marketplace.

The company’s “relevant range” of activity and whether or not

the special order will cause volume to exceed this range

Problem 11-35 (continued-4)

The ethical and competitive issues of helping a competitor in

distress.

7. The international issues Williams should consider include:

What customs duties and import/export restrictions might affect

the special order and any future business with Glasgow?

While this special order will be completed in the relatively short

time of a few months, foreign exchange rates might change

significantly in this period. What does the special order

agreement say regarding the sales price, in pounds or dollars?

Might the Glasgow special order introduce Williams to new

markets in Scotland or elsewhere in Britain or Europe? If

Williams is not now significantly involved in global sales, how

might the firm use this opportunity to increase its exposure in

foreign markets?