Chapter 16 – Operational Performance Measurement: Further Analysis of Productivity and Sales

16-

40 Sales Variances; Quarter to Quarter (20 min)

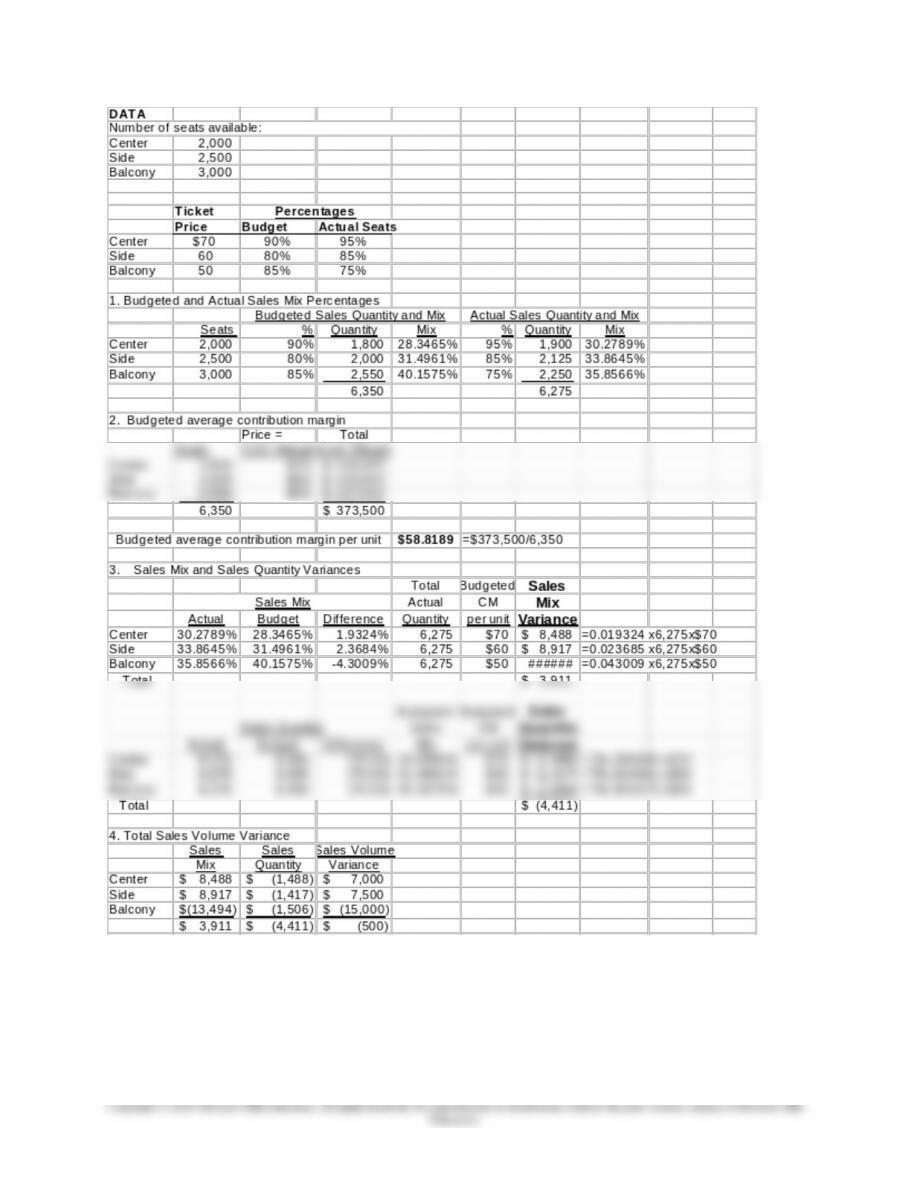

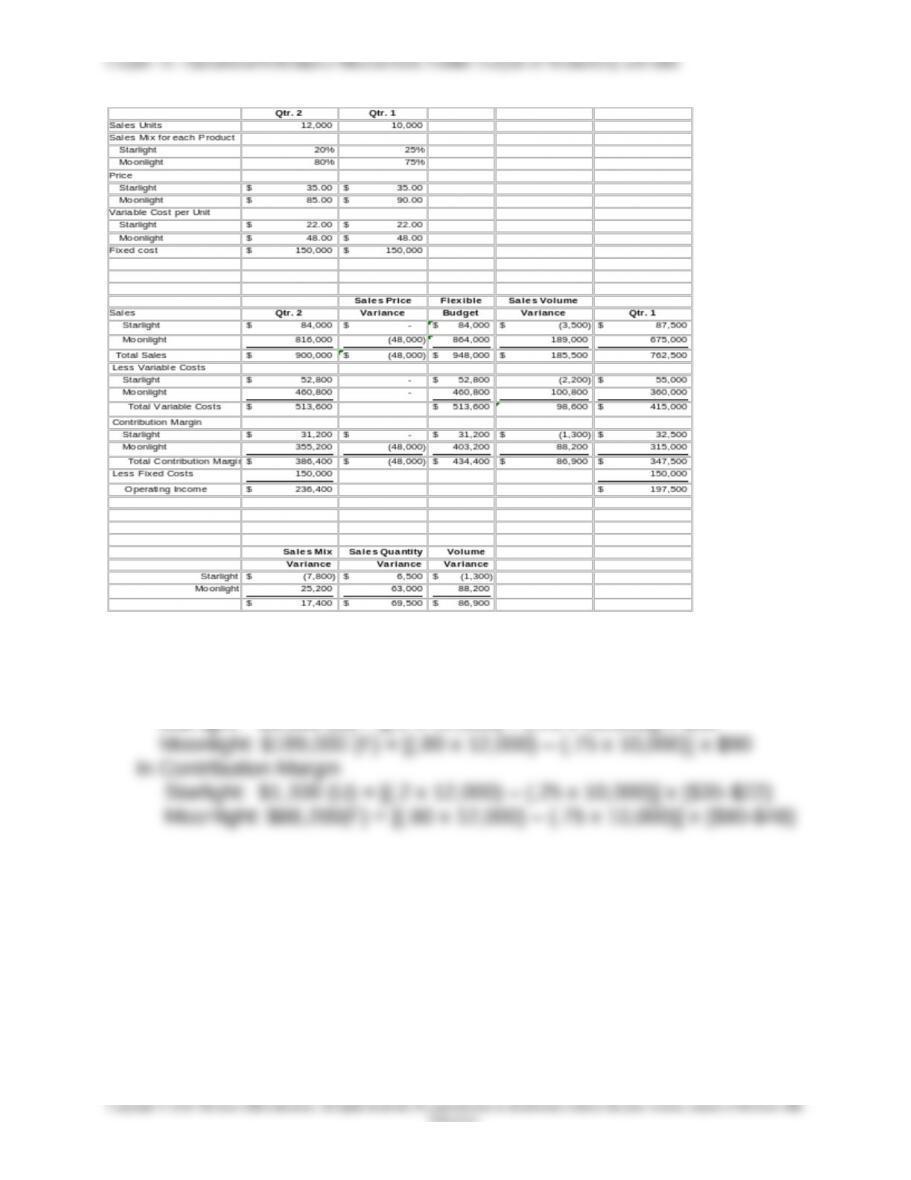

1. Contribution Income Statement for Hathaway

16-21

2. The volume variances for each product are shown above:

In Sales Dollars:

Starlight: $3,500 (U) = [(.2 x 12,000) – (.25 x 10,000)] x $35

16-22

Education.

Chapter 16 – Operational Performance Measurement: Further Analysis of Productivity and Sales

16-40 (continued -1)

3. The mix and quantity variances for each product are shown below;

note that the total of the sales mix and quantity variance equals the volume

variance

Sales Mix Variances

16-23

Education.

Sales Mix Sales Quantity Volume

Contribution Margin

Variance Variance Variance

Starlight (7,800)$ 6,500$ (1,300)$

Moonlight 25,200 63,000 88,200

Total 17,400$ 69,500$ 86,900$

Chapter 16 – Operational Performance Measurement: Further Analysis of Productivity and Sales

PROBLEMS

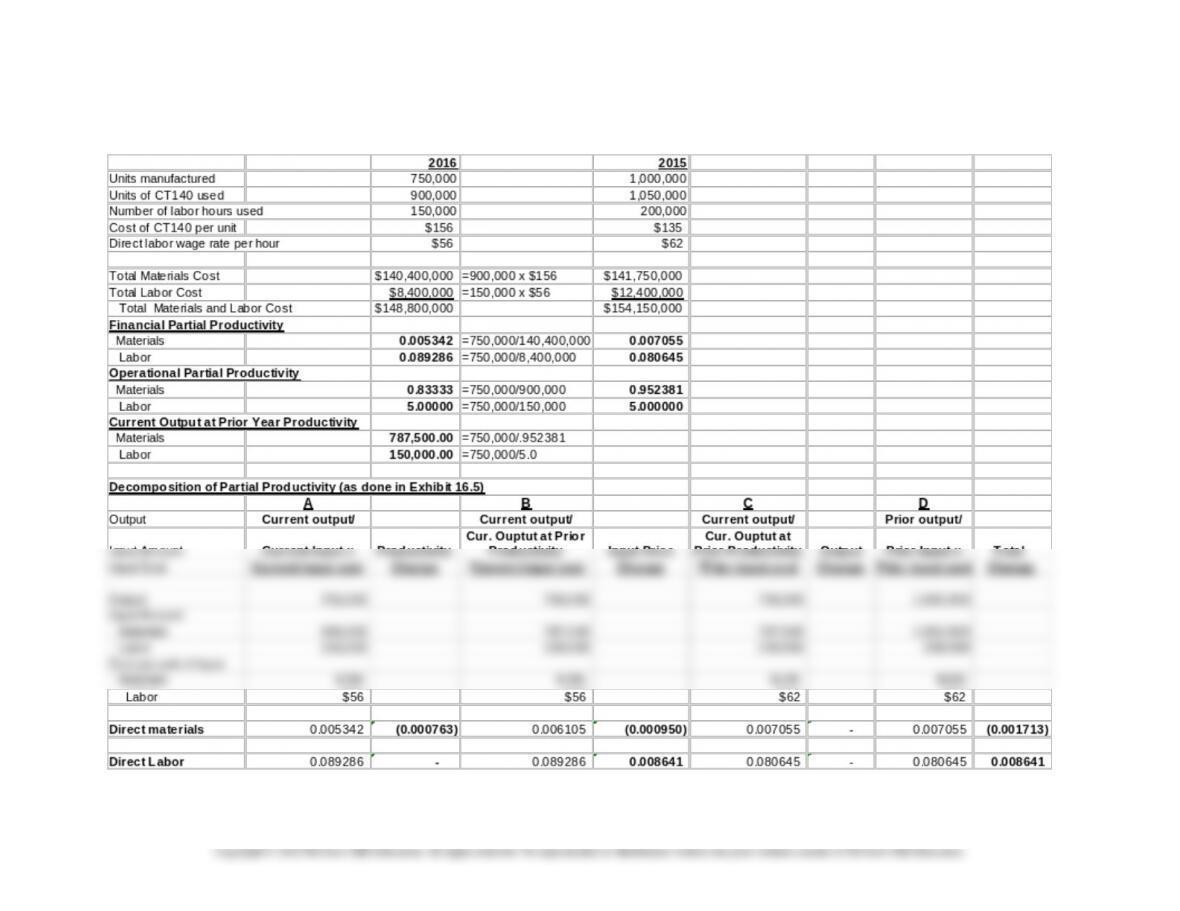

16-41 Partial Operational Productivity (15 min)

1. Operational Partial Productivity

2. Productivity of direct material, CT140, deteriorated from 0.9524 in

2015 to 0.833 in 2016. Productivity of direct labor, however,

remained the same for 2015 and 2016. Note however that, while

16-24

Education.

Chapter 16 – Operational Performance Measurement: Further Analysis of Productivity and Sales

16-42 Partial Financial Productivity (30 min)

1.,2.,3. See spreadsheet solution below:

16-25

Chapter 16 – Operational Performance Measurement: Further Analysis of Productivity and Sales

16-42 (continued-1)

1.

2. Direct material productivity financial partial productivity deteriorated

3. The partial financial productivity ratios are calculated and compared

in the spreadsheet above.

4. The decompositions suggest that changes in financial productivity

16-26

Education.

Chapter 16 – Operational Performance Measurement: Further Analysis of Productivity and Sales

16-43 Total Productivity (15 min)

1. Total productivity in units

2016 2015

(a) Total units manufactured: 750,000 1,000,000

(b) Total variable manufacturing

costs incurred (see 16-42):

(c) Total productivity: (a) / (b) 0.005040 0.006487

(d) Change in productivity:

2. Financial partial productivity measures indicate that the changes in

productivity for direct materials and direct labor are in opposite

directions. The firm maintained its direct labor productivity while its direct

Chapter 16 – Operational Performance Measurement: Further Analysis of Productivity and Sales

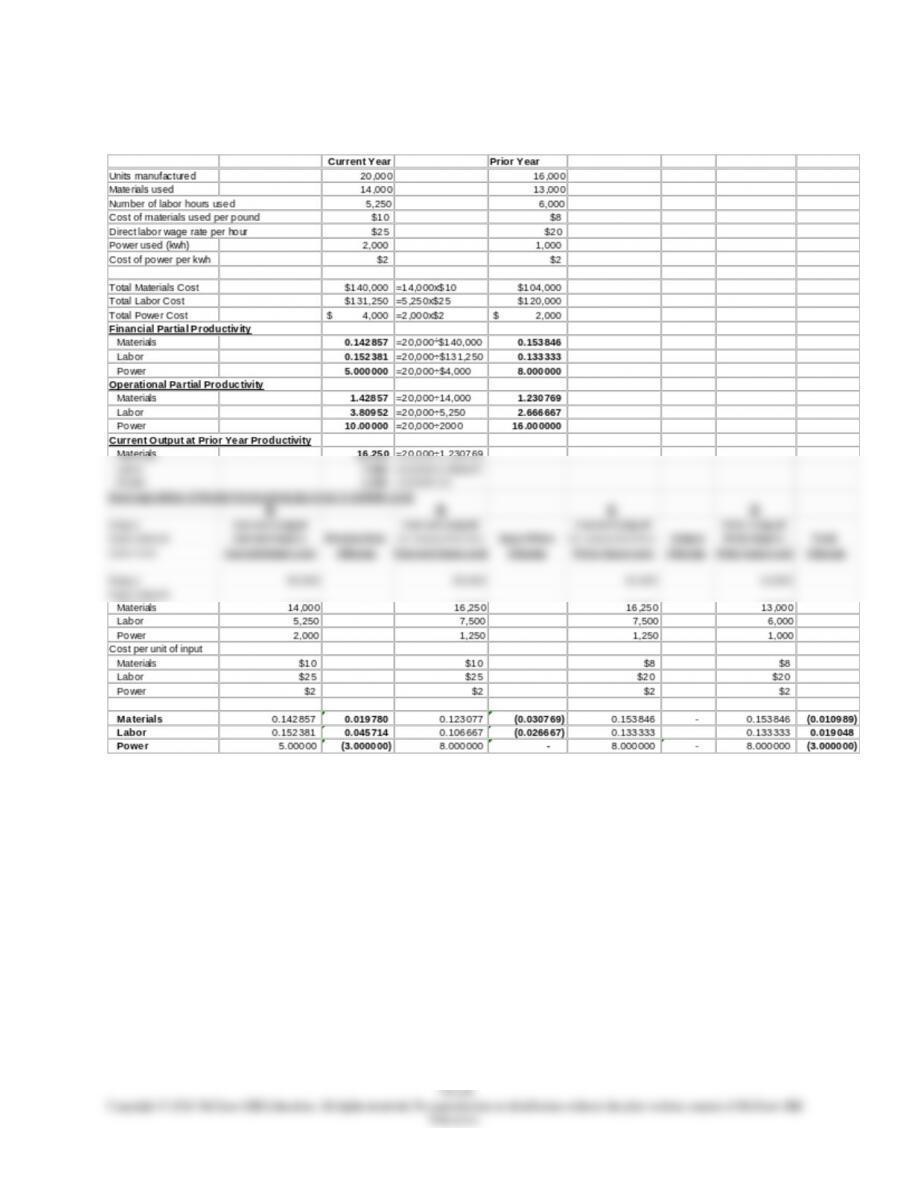

16-44 Operational and Financial Partial Productivity (45 min)

1. Colditz Company

Comparative Income Statement

For the years ended

Current year Prior year

Sales 20,000 x $40 = $800,000 16,000 x $40 =$640,000

Variable cost of sales:

Materials 14,000 x $10 = $140,000 13,000 x $8 = $104,000

Labor 5,250 x $25 =131,250 6,000 x $20 = 120,000

Power 2,000 x $2 = 4,000 1,000 x $2 = 2,000

2.3., See spreadsheet on following sheet.

4. Both direct materials and direct labor operational partial productivity

improved from the prior year to the current year. In the current year the

firm was able to manufacture more output units for each unit of materials

placed into production and for each hour spent on production. The

operational productivity of power in the current year deteriorated from

that of the prior year. It is likely that the firm used more equipment in

production in the current year that reduced consumption of materials

16-28

Education.

Chapter 16 – Operational Performance Measurement: Further Analysis of Productivity and Sales

16-44 (continued -1)

Chapter 16 – Operational Performance Measurement: Further Analysis of Productivity and Sales

16-44 (continued -2)

5. See spreadsheet above.

6. Productivity for both direct materials and direct labor improved in the

current year. The percentages of improvements in productivity are

16-30

Education.