Chapter 01 – Cost Management and Strategy

Chapter 1

Cost Management and Strategy

Learning Objectives

1. Explain the use of cost management information in each of the four functions of management and

in different types of organizations with emphasis on the strategic management function.

2. Explain the contemporary business environment and how it has influenced cost management.

3. Explain the contemporary management techniques and how they are used in cost management to

respond to the contemporary business environment.

4. Explain the different types of competitive strategies.

5. Describe the professional environment of the management accountant, including professional

organizations, professional certifications, and professional ethics.

6. Understand the principles and rules of professional ethics and explain how to apply them.

New in this Edition

Update of content in all Real World Focus items, one new Real World Focus item, and

update of Cost Management in Action item; updated surveys on strategy and ethics;

updated content on real world information used throughout the chapter

Replaced Sara Lee company example with Tyson Foods (Sara Lee in North American

became Hilshire Brands, Inc. in 2012 and Hillshire Brands became a subsidiary of Tyson

Foods on August 29, 2014)

Twelve new exercises added; several revised problems and five all-new problems with a

focus on strategy and ethics

Teaching Suggestions

Most instructors will choose to assign this chapter for the first one or two class meetings, but to

spend little, if any, class time on it. Some instructors will choose to spend more time if a more thorough

coverage of strategic positioning is desired. The main topic areas, except for strategic positioning and

professional ethics, do not require class discussion and exercise. The presentation for these other topics is

factual and informative, covering some of the basic concepts of management organization and of the

contemporary business environment. The instructor might choose to explain each of the management

techniques identified in the chapter, and to also explain that these techniques will be covered in later

chapters.

The material on professional ethics is best introduced briefly at this time, with the reminder that

the topic will come up in each of the subsequent chapters. Going through a few problems in Chapter 1 on

ethics would provide a useful framework for them to remember in answering the ethics questions coming

up in later chapters. Remind them to not forget the IMA code of ethics and the four step process for

applying the code.

The important points to convey in the first class session are that the course will have four main

themes: strategy, globalization of business, service firms, and ethics. Strategy is the most important

1-1

Chapter 01 – Cost Management and Strategy

theme, that is, the use of cost management methods and practices to help the firm succeed at its business

strategy. Strategy can be described to the students as the umbrella concept which ties the topics of the

course togethereach topic is covered because it contributes in some way to the success of the firm. All

four themes are covered in each chapter. The students should understand that each topic covered in the

course will be strongly influenced by:

1. Cost and management accounting have changed from what was once a focus on financial record

keeping to a strategic focus, one in which the management accountant becomes a business partner

with management, to help the firm to succeed. To be an effective business partner, the management

accountant must understand business and contemporary business issues and management techniques.

He or she must go beyond an expertise in financial matters only, but also be able to integrate

important factors in operations, marketing, and human resources to come up with solutions which are

good for the firm, not just good accounting.

2. The strategic focus is a very important theme of the course, and is forcefully present in each of the

chapters. The strategic focus is included in the text, class discussion and exercise problems. Strategic

issues may even appear as a part of an exam question.

3. The demands on management and the management accountant are increasing due to the changing

business environment and to the globalization of business. Contemporary business topics are covered

throughout the book, and global issues are touched on in each chapter.

4. As the demands on cost management change, so have the responsibilities of the management

accountant. Each topic covered in the course will include professional and ethical issues.

Welcome to Students

(The following is in the front pages of the book, and can be used to help motivate the first day of

class. Also, for a description of how the first two chapters of the text can be used in the first days of

class, see the article by Edward J. Blocher, “Teaching Cost Management: A Strategic Emphasis,”

Issues in Accounting Education, February, 2009, pp 1-12.

To the student:

We have written this book to help you understand the role of cost management in helping an organization

succeed. Unlike many books that aim to teach you about accounting, we aim to show you how an

important area of accounting, cost management, is used by managers to help organizations achieve their

goals.

An important aspect of cost management in our text is the strategic focus. By strategy we mean

the long-term plan the organization has developed to compete successfully

Most organizations strive to achieve a competitive edge through the execution of a specific strategy. For

some firms it is low cost, and for other it might be high quality, customer service, or some unique feature

or attributes of its product or service. We know in these competitive times that an organization does not

succeed by being ordinary. In contrast, it develops a strategy that will set it apart from competitors and

assure its attractiveness to customers and other stakeholders into the future. The role of cost management

is to help management of the organization attain and maintain success through strategy implementation.

Thus, in every chapter, and in every problem and case in the text, there is a larger issue, which is: “How

does this organization compete? What type of cost-management information does it need?” We do not

cover a cost-management method simply to become proficient at it. We want you to know why, when, and

how the technique is used to help the organization succeed.

A strategic understanding of cost management is so important that many senior financial

managers are coming back to school to learn more about strategy, competitive analysis, and new

1-2

Chapter 01 – Cost Management and Strategy

cost-management techniques. Knowing how to do the accounting alone, no matter how well you

do it, is by itself no longer sufficient. Cost management with a strategic emphasis is one way to

enhance your career and to add value to your employer, whatever type of organization it might

be.

A Motivator

To help the students see the importance of cost management, the instructor can periodically use a

short case with an issue the student may have some difficulty seeing initially, but which can be easily

explained. The Bloomberg Business week stories which start each chapter can be used for this purpose.

As an example, you can use the following question: You are a domestic appliance manufacturer and a

Japanese competitor has entered the market with a product that has better quality, features, and a lower

price. What do you do? How can the management accountant help? The question is a very broad but

engaging question, which should have the students to begin to realize that the course is about business

and being an effective competitorwe are looking to see how cost management can help. Some students

will suggest one or more of the contemporary management techniques. If the discussion doesn’t get there

pretty quickly, ask them to think which of the contemporary management techniques might help. A

variety of answers is possible. I would make sure that a discussion of target costing is coveredto explain

the role of target costing in managing the firm’s competitive tradeoffs between costs, features, and quality

of product.

The Four Management Functions

In management and accounting, different authors describe a variety of different concepts about

the functions of management. We have chosen to focus on the four functions:

1) strategic management

2) planning and decision making

3) management and operational control, and

4) preparation of financial statements.

These four functions are a useful way to view management’s responsibility from a cost management

perspective, and are helpful to provide an organizing structure for the book. However, sometimes a

human resources perspective or alternative perspective is taken, and the functions are described

differently. For example, a common listing of the functions of management would look as follows: (1)

planning, (2) leading, (3) organizing, and (4) controlling.

1-3

Education.

Chapter 01 – Cost Management and Strategy

The New Definition of Management Accounting

The strategic role of the management accountant in an organization is explained in the definition of

management accounting provided by the Institute of Management Accountants (IMA); relevant

additional information on the definition can be found in the Statement on Management Accounting:

Management accounting is a profession that involves partnering in management decision

making, devising planning and performance management systems, and providing expertise

in financial reporting and control to assist management in the formulation and

implementation of an organization’s strategy.

Management accountants use their unique expertise (decision making, planning, performance

management, and more), working with the organization’s managers, to help the organization

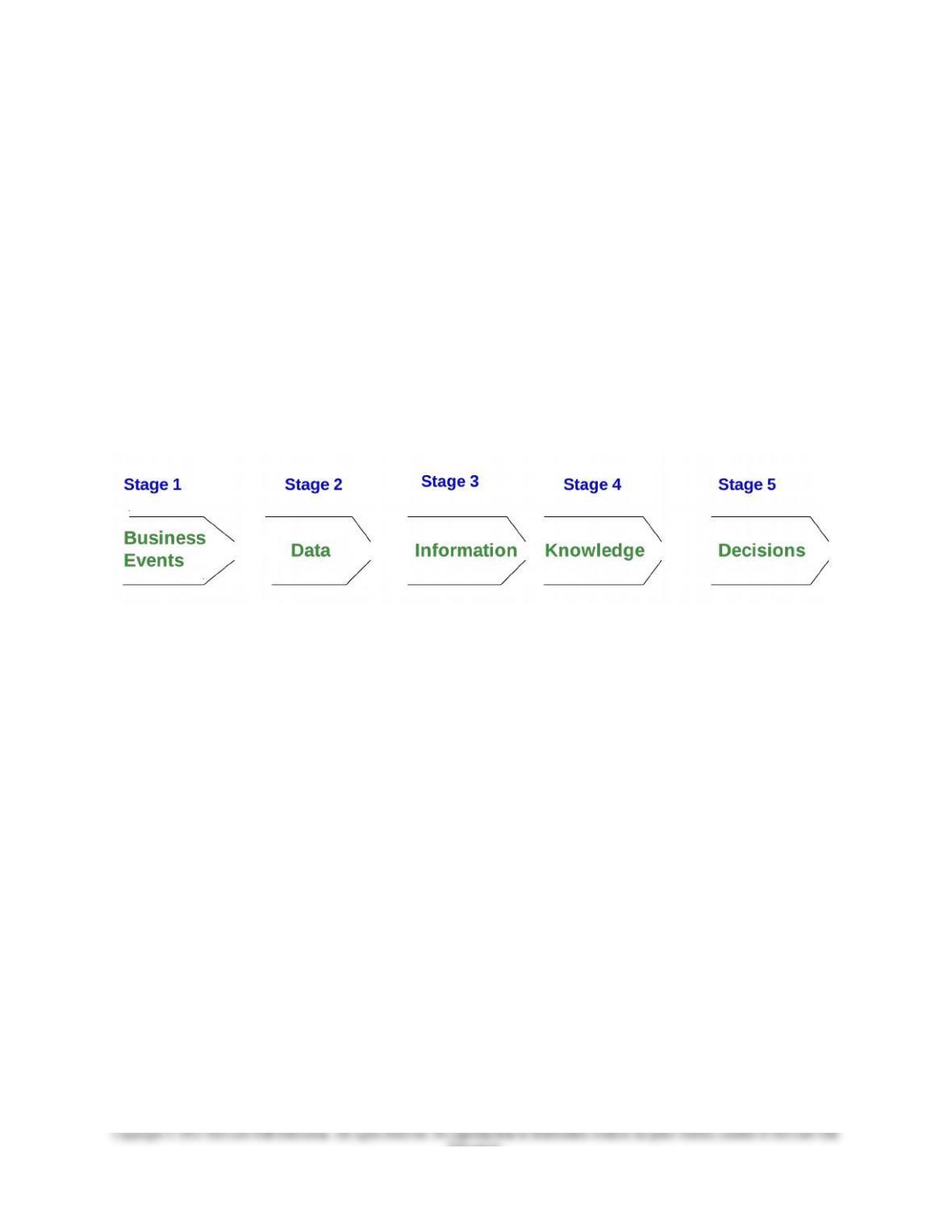

succeed in formulating and implementing its strategy. Cost management information is developed

and used within the organization’s information value chain, from stage 1 through stage 5 as shown

below:

At lower stages of the value chain, management accountants gather and summarize data (stage 2)

from business events (stage1) and then transform the data to information (stage 3) through

analysis and use of the management accountant’s expertise. At stage 4 the information is combined

with other information about the organization’s strategy and competitive environment to produce

actionable knowledge. At stage 5 management accountants use this knowledge to participate with

management teams in making strategic decisions that advance the organization’s strategy.

1-4

Education.

Chapter 01 – Cost Management and Strategy

The Contemporary Business Environment

The chapter emphasizes the six forces acting on the contemporary business environment which have

strongly influenced cost management:

The Global Business Environment: including the importance of the World Trade Organization,

other global treaties, and the integration of the European Union

Lean Manufacturing: the use of the principles of production efficiency, many developed within

Japanese manufacturers, especially Toyota

The Use of the Internet, and Enterprise Resource Management

The Focus on the Customer

Changes in Management Organizations

Social, Political, and Cultural Changes

Contemporary Management Techniques

The chapter describes 13 ways in which organizations, with the help of cost management, have

adapted to the changing business environment:

1. The Balanced Scorecard and Strategy Map

2. The Value Chain

3. Activity Based Costing and Management

4. Business Intelligence

5. Target Costing

6. Life Cycle Costing

7. Benchmarking

8. Business Process Improvement

9. Total Quality Management

10. Lean Accounting

11. The Theory of Constraints

12. Enterprise Sustainability

13. Enterprise Risk Management

Strategy and the Strategic Role of Cost Management

As a framework for the integration of strategy throughout the text, the Michael Porter model of

competitive strategy is used. This model explains that an organization succeeds either by pursuing

a cost leadership strategy or a differentiation strategy. The cost leader succeeds by providing the

lowest cost product or service to the consumer, while the differentiated organization succeeds by

providing products and services with features, quality, and innovation that draw the consumer to

these products and services.

The Five Steps for Strategic Decision Making

The five steps for decision making with a strategic emphasis are a new feature of the

fifth edition. In these segments, which appear in nearly all the chapters, the material of the

chapter is illustrated in a clear example to show the strategic role of cost management for that

topic material. For example, listed below is a short illustration of how the steps could be used

by Wal-Mart to help the company deal with the problem of rising fuel prices that affect the cost of

the firm’s use of trucks to deliver product from Wal-Mart’s warehouses to its retail stores.

1-5

Education.

Chapter 01 – Cost Management and Strategy

The first step is to determine the strategic issues surrounding the problem, because the

solution of any problem must fit the organization’s strategy. A good decision is one that makes

the organization more competitive and successful. By starting with the strategic issues, we

ensure that the decision fits the organization’s strategic goals.

1. Determine the Strategic Issues Surrounding the Problem.

Fuel costs are critical to Wal-Mart because it competes on low cost and low prices. So this

problem will get close management attention. In contrast, the effect of a rise in fuel prices will

likely not be as critical for a differentiated company, such as a high-end retailer like Nordstrom.

2. Identify the Alternative Actions:

In one alternative, Wal-Mart considers the use of smaller and more fuel-efficient trucks together

with a relocation of its warehouses, to reduce travel time and fuel usage. Another option would

be to outsource all of Wal-Mart’s delivery needs to other trucking firms.

3. Obtain Information and Conduct Analyses of the Alternatives

Wal-Mart collects relevant cost information and calculates the expected cost of each alternative

and finds that the use of other truckers would provide significantly lower total fuel cost.

Considering the problem strategically, Wal-Mart projects on the one hand that it can more

effectively compete with Target by providing more rapid delivery of fast-moving items to its

stores, and that this could be accomplished with the use of smaller trucks. On the other hand,

Wal-Mart also knows that it competes on cost and that lower cost is critical to its success.

4. Based on Strategy and Analysis, Choose and Implement the Desired Alternative

After considering the options, Wal-Mart chooses to outsource the delivery function to other

trucking firms, in order to maintain or perhaps improve its low cost position. In contrast, a high-

end retailer such as Nordstrom might have chosen the option with more rapid delivery and higher

cost, because its strategy is based on quality of product and customer satisfaction. Knowing the

strategic context for the decision can make a big difference!

5. Provide an On-going Evaluation of the Effectiveness of implementation in Step 4.

To provide an on-going review of delivery costs, Wal-Mart top management instructs operational

managers in the firm to present an updated review of the decision to top management once every

quarter. In this way, changes in costs or strategic objectives will be reviewed on a regular basis.

1-6

Chapter 01 – Cost Management and Strategy

Assignment Matrix Chapter 1

Exercises and Problems

Learning Objectives Text Features

Connect

1.

Cost management information

2.

Contemporary business environment

3.

Contemporary management techniques

4.

Types of competitive strategies

5.

Professional environment

6.

Professional ethics

Strategy

Service

International

Ethics

Sustainability

Chapter 01 – Cost Management and Strategy

1-16 5 min. X X

1-17 5 min. X X

1-18 5 min. X X

1-19 5 min. X X

1-20 5 min. X X

1-21 5 min. X X

1-22 5 min. X X

1-23 5 min. X X

1-24 New to 7e 5 min. X X

1-25 New to 7e 5 min. X X X

1-26 New to 7e 5 min. X X

1-27 New to 7e 5 min. X X

1-28 New to 7e 5 min. X X X

1-29 New to 7e 5 min. X X X

1-30 New to 7e 5 min. X X

1-31 New to 7e 5 min.. X X

1-32 New to 7e 5 min. X X

1-33 New to 7e 5 min. X X X X

1-34 New to 7e 5 min. X X X

1-35 New to 7e 5 min. X X

Exercises

1-36 1-24 15 min. X X X X X

1-37 1-25 15 min X

1-38 1-26 15 min. X X

1-39 1-27 30 min. X

1-40 1-28 15 min. X

1-41 1-29 20 min. X X X X X

1-42 1-30 20 min. X X X

1-31 Deleted

1-43 1-32 20 min. X

1-44 1-33 15 min. X

1-34 Deleted .

Continued on next page…

Assignment Matrix Chapter 1

(continued)

Learning Objectives Text Features

7e 6e Transition

6e to 7e Time

Connect

1.

Cost management information

2.

Contemporary business environment

3.

Contemporary management techniques

4.

Types of competitive strategies

5.

Professional environment

6.

Professional ethics

Strategy

Service

International

Ethics

Sustainability

Problems

1-45 New in 7e 15 min. X X X

1-8

Education.