Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-45 (continued-3)

Activity-based costing provides ADA with more detailed and better

estimates of product costs. For example by using ABC, ADA becomes

aware that the cost of Diomycin is lower ($0.4818 per capsule compared

From the schedule, activity-based costing assigns more overhead to

the lower-volume Addolin because the production of Addolin requires

more setups, inspection, supervision, formulation and management. The

current direct-labor-hours based costing system failed to assign costs of

all activities. As a result, Diomycin and Homycin subsidized Addolin.

The production department at ADA also benefits under ABC. ABC

provides better costing information on the cost of each of the activities

and identifies cost drivers and the activities that consume resources and

raise cost. The additional information enables production mangers to

manage cost by managing activities and cost drivers.

Adopting the ABC method is strategically important for ADA.

Because the ABC method provides ADA with a more accurate product

5-41

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-45 (continued-4)

4. Among major uses of ABC in the Pharmaceutical Industry are:

a. Strategic Use of ABC to Reduce Costs

One of the important ways companies develop competitive advantages

is to become a low-cost producer. Many companies in the

b. Use of ABC to Eliminate Low-Value-Added Costs

ABC can be used to identify and eliminate activities that add costs but

not value to the products in the pharmaceutical industry. A company

can eliminate low-value added activities and costs without reducing

c. Use of ABC in Marketing and Distribution

In the pharmaceutical industry, ABC can be applied to marketing or

administrative activities. The cost of performing marketing services

such as distributing products through different distribution channels can

be computed and the information used in making informed decisions.

For example, some of the different channels of distribution in the

who make decisions about which channel to use.

d. Use of ABC to Make Better Pricing Decisions

ABC enables managers to make better pricing decisions by providing

managers with more accurate product cost data for pricing decisions.

e. Use of ABC to Make Better Product Mix Decisions

ABC provides a firm with more detailed and better estimation of

5-42

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-46 Time-Driven Activity-Based Costing (TDABC) in a Call Center

(20min)

1. The TDABC rate per minute for MMI is determined as follows:

Total Projected Costs ÷ Practical Capacity

= $9,515,500 ÷ 12,045,000 = $0.79 per minute

The charge to AS should be estimated as follows:

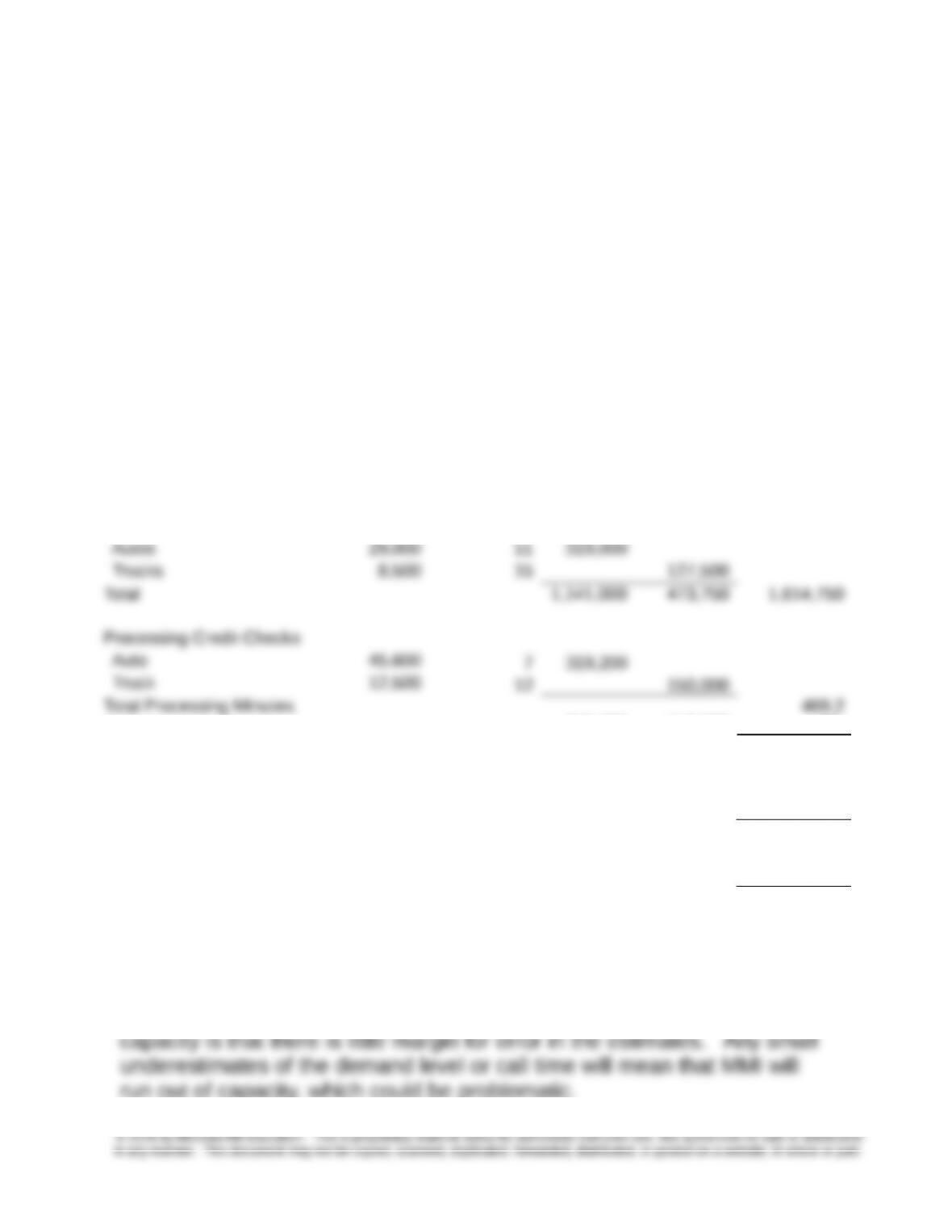

2. The total time for each type of loan is determined as follows:

Total Calls

Answered

Avg. No. of

Minutes/C

all

Total Time (minutes)

Inquiries Autos Trucks

Inquire re: Rates and Terms

Autos 80,000 6 480,000

Trucks 32,000 7 224,000

Inquire re: Loan App Status

Autos 45,000 5 225,000

Trucks 6,750 11 74,250

Inquire re: Payment Status

Autos 39,000 3 117,000

5-43

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-46 (continued)

The revised proposal would show:

Cost for Autos (1,141,000 x $.79) $901,390

Cost for Trucks (473,750 x $.79) $374,263

Total Cost $1,275,653

Note: For further information on TDABC and call centers, see Robert S.

Kaplan and Steven R. Anderson, Time-Driven Activity-Based Costing, Harvard

Business School Press, 2007; and Bilbert Y. Uang and Roger C Wu, “Strategic

Costing & ABC,” Management Accounting, May 1993, pp 33-37.

5-44

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-47 TDABC; Continuation of Problem 5-46 (20 min)

1. The amount of unused capacity is determined as follows.

Total Calls

Answered

Avg. No. of

Minutes/Call Total

Platinum Regional Bank 234,000 6.0 1,404,000

Healthwise Software Inc. 66,788 5.0 333,940

Johnson Manufacturing 122,665 4.0 490,660

Lesco Online Shopping 233,756 6.0 1,402,536

Babcock Insurance Service 55,455 5.5 305,003

Garcia Electric Supply and Service 38,956 3.4 132,450

Gilbert’s Online Garden Supplies 145,902 4.5 656,559

Unused Capacity 2,088,904

Call Center Practical Capacity 12,045,000

Total minutes used with the AS engagement (9,956,096

+ 1,614,750) 11,570,846

Unused capacity with the AS engagement 474,154

The 2,088,904 minutes of unused capacity is relatively large (17.3% of total

capacity) and has important implications for MMI’s operating and marketing

strategy. First, it indicates the importance of getting the AS engagement,

which would reduce unused capacity to 3.9%, a substantial improvement.

5-45

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-47 (continued -1)

2. The additional business with AS would leave very little unused

capacity(less than 0.1%) as shown below:

Total Calls

Answered

Avg. No. of

Minutes/

Call

Total Time (minutes)

Inquiries Autos Trucks Total

Inquire re: Rates and

Terms

Autos 80,000 6 480,000

Trucks 32,000 7 224,000

Inquire re: Loan App Status

Autos 45,000 5 225,000

Trucks 6,750 11 74,250

Inquire re: Payment Status

Autos 39,000 3 117,000

Trucks 12,000 4 48,000

Inquire re: Other Matter

319,200 150,000

00

Total Minutes for the Combined

Engagement 2,083,950

Minutes for other Clients 9,956,096

Total Minutes 12,040,046

Unused Capacity 4,954

Call Center Capacity 12,045,000

The cost of the unused capacity could be determined as follows:

$.79/min × 4,954 minutes = $3,914

One significant concern with such a small level of planned unused

run out of capacity, which could be problematic.

5-46

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-47