Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18-50 (continued -1)

Other GAAP issues include differences between profit centers in:

a) Judgments of the allowance for bad debts

g) The effect of judgment in choosing the method for cost allocation

when profit centers share a common resource or service

h) Accounting for leases

The use of a contribution type of income statement as explained in

the chapter can provide an improvement over full cost-based profit

since it incorporates the concepts of traceability and controllability.

If the instructor wishes, this problem provides a good opportunity to

discuss the relationship between GAAP and IFRS and the potential

impact of the convergence of GAAP to IFRS on performance

measurement, particularly of profit centers. As noted in the chapter,

18-51

Education.

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18-50 (continued -2)

2. The proposals fit solidly within the range of proposals made by many

authors in performance management (management control systems),

financial statement analysis, and cost management. In particular the

proposal for combination of measures is widely accepted, and

and urgency to the proposal for a market oriented approach for

performance measurement is the on-going consideration at the SEC

of the convergence of U.S. GAAP and International Financial

Reporting Standards. International reporting standards have a much

stronger focus on market value, allowing under certain conditions for

long-lived assets to be measured at market value, and for research

and development costs to be capitalized, in contrast to the more

conservative cost-based approach for long-lived assets and expense-

based approach to R&D in U.S. GAAP.

18-52

Education.

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

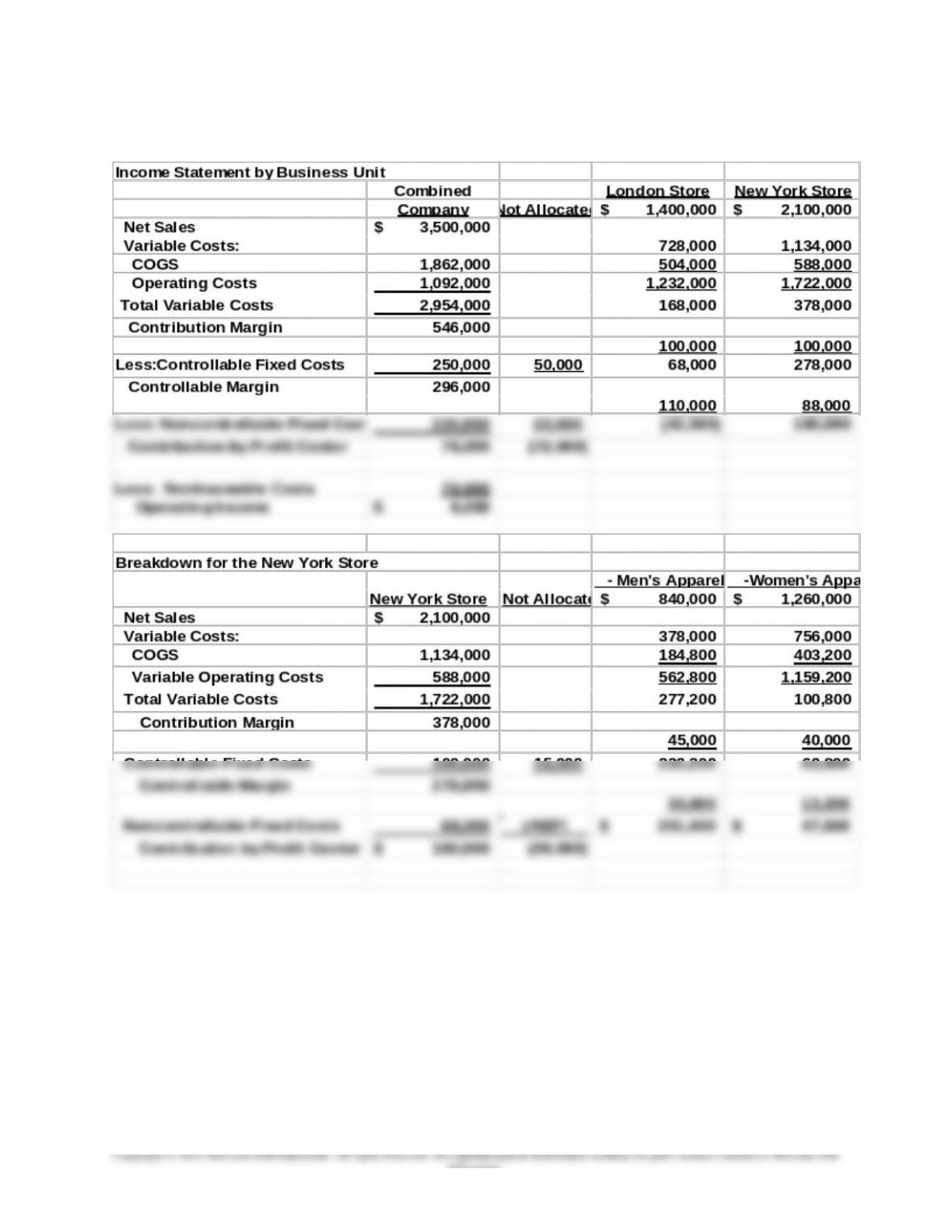

18-51 Contribution Income Statement; Spreadsheet

Application(25 min)

Data (in thousands)

Total Net Sales $ 3,500,000

Fixed Costs

Partly Traceable and Controllable 250,000

New York Store 60%

New York – Men’s Apparel 40%

New York – Women’s Apparel 60%

Cost of Goods Sold (Variable) Percent of Sales

London Store 52%

New York – Men’s Apparel 45%

-Women’s Apparel 40%

-Could not be Traced to Men’s or Women’s Apparel 15%

Could not be Traced to London or New York 20%

Fixed Noncontrollable Costs (Partly traceable) Percent of Total

London Store 50%

New York Total 40%

-Men’s Apparel 35%

-Women’s Apparel 15%

-Could not be Traced to Men or Women’s Apparel 50%

Could not be Traced to London or New York stores 10%

18-51 (continued -1)

18-53

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18-54

Education.

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18-51 (continued -2)

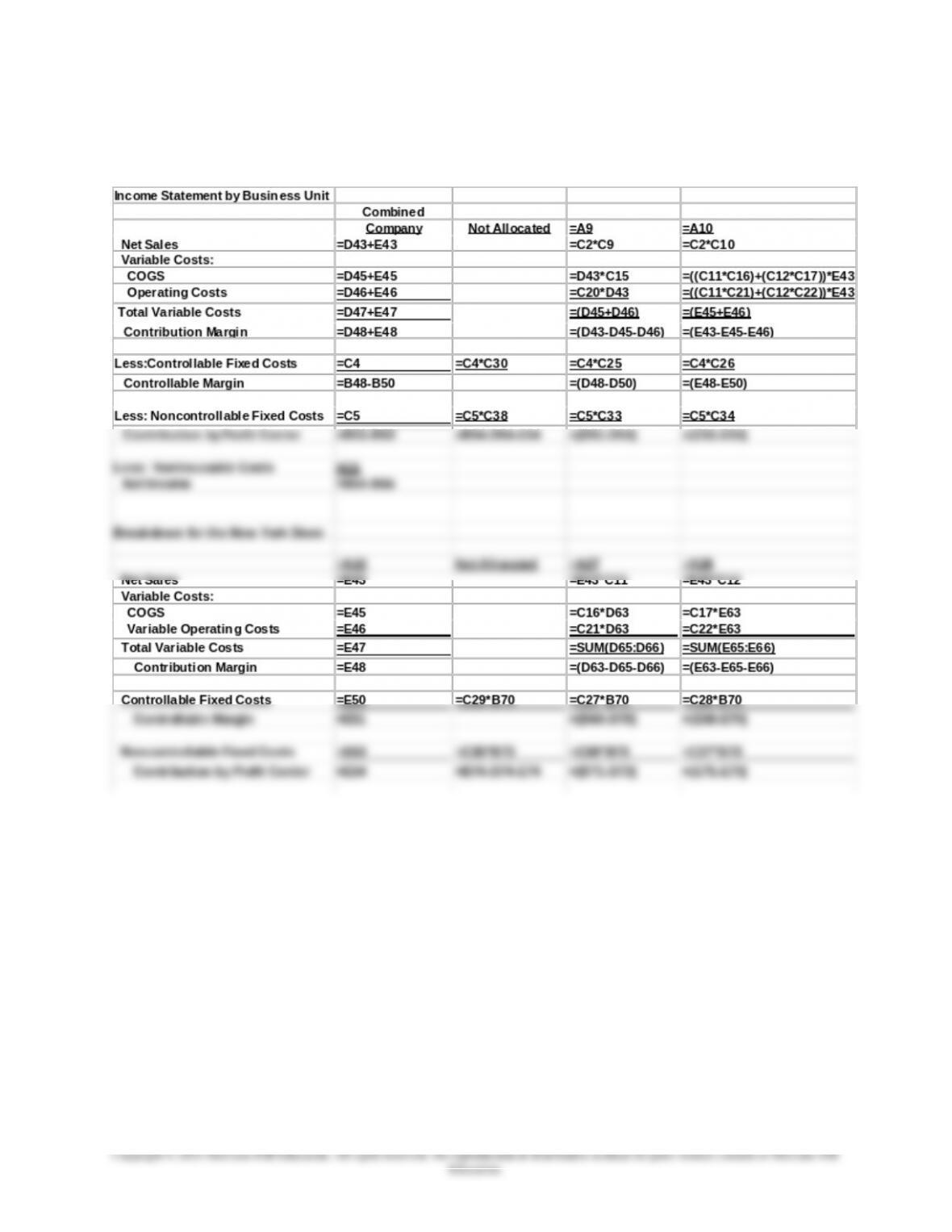

The formulas for the above spreadsheet are as follows:

18-55

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18-51 (continued – 3)

2. The global issues for High Fashion include foreign currency

translation, as the U.S. dollar fluctuates relative the U.K. pound. For

example, the U.S. dollar increased in value approximately 25%

relative to the pound during 2008 and then the two currencies were

been relatively stable into 2013. The dollar then began losing value,

reaching a low in late November, 2014, before a new phase of

increase began and it reached a high as of April 2015. The higher

value of the dollar in 2008 meant that the company’s sales in the U.K.

would be at higher prices, with the probable effect of reducing those

Other global issues include the state of the economies of the

different countries where Fashionisto is doing business. For

example, in 2011, the economies of both the U.S. and the U.K. were

in recession. Economists in mid-2011 had not stated clearly when

the global recession and debt crisis might abate, so the company

needs to adjust its strategy to effectively deal with a radically different

sales outlook. The economies did not emerge from this recession as

the same time, and this could mean significant changes in the types

of clothing carried at the various locations, the hours the stores are

open, and new product offerings, among other measures. In keeping

structure this type of broadened evaluation.

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18-52 Validating the Balanced Scorecard; Spreadsheet Application

(35 min)

1. The balanced scorecard is a more comprehensive approach to

strategic performance measurement. In addition to profit, it includes

2. The correlation matrix for the data are shown below. Some

observations are as follows:

There is a high correlation (r= .89) on the customer survey data with

the sales increase variable, indicating that the survey is a valuable

on this measure.

Training hours appears to have no effect on store success. This is a

surprising result which should be examined by store managers and

district managers to determine the cause. Are the in-house training

sessions properly focused and of the desired quality?

Note that there is a high negative correlation between wait time and

18-57

Education.

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18-52 (continued -1)

The change in sales at each of the stores is driven by a number of factors

in addition to those in the analysis shown here. For example, the

economic environment at each store could be changing for better or worse.

Also, a given store might be impacted by the opening or closing of a

competitive store in its area. A full validation study would attempt to

capture as many of these additional variable as possible.

The correlations results for the data:

Sales Survey Review Wait Time Hours

Sales 1.000000000

Survey 0.887385586 1.000000000

Note: correlations greater than .5 are significant at p < .05

18-58

Education.

18-53 Contribution Income Statement for Profit Centers; Strategy;

International (60 min)

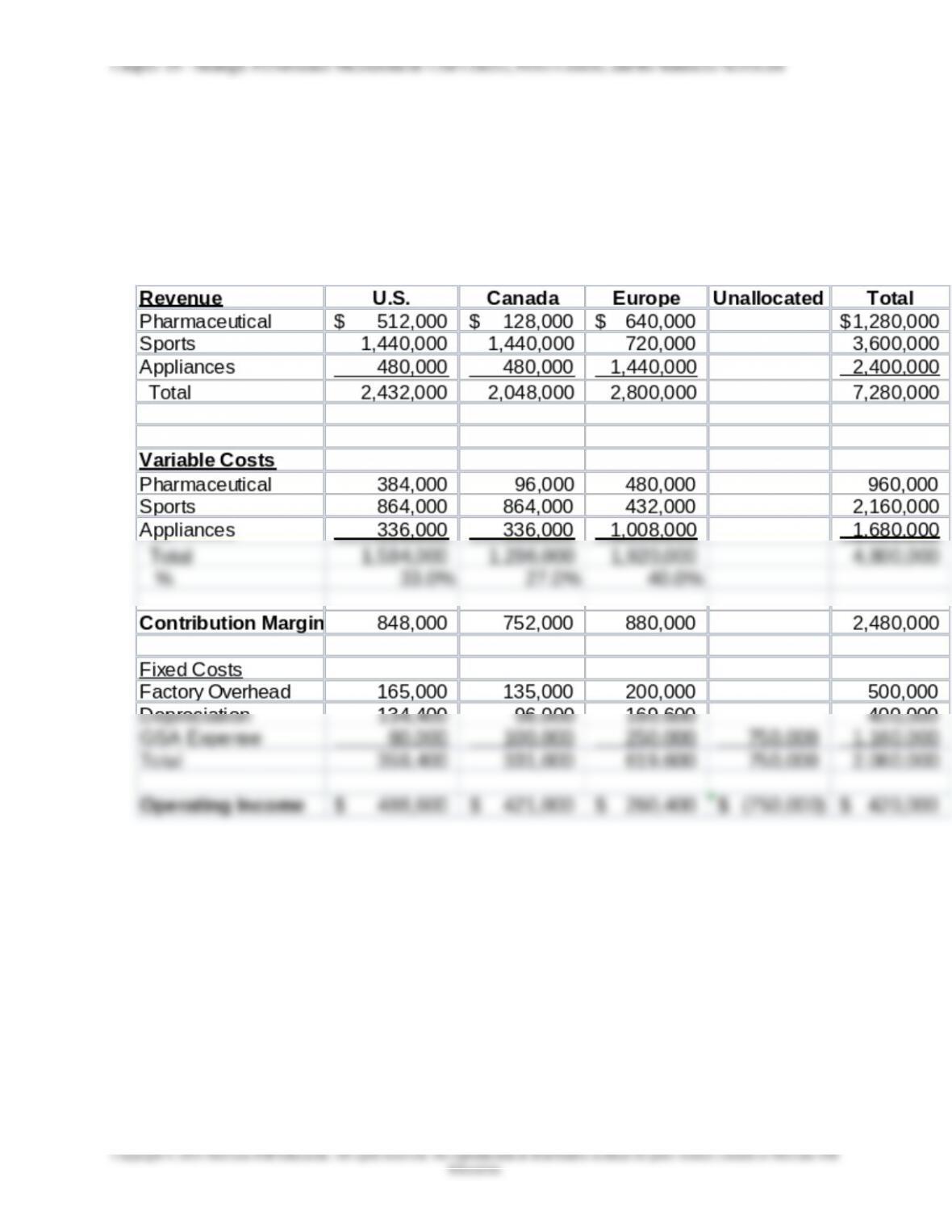

1. Stratford Corporation

Statement of Income by Geographic Area

For the Fiscal Year Ended April 30

18-59

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18-53 (continued -1)

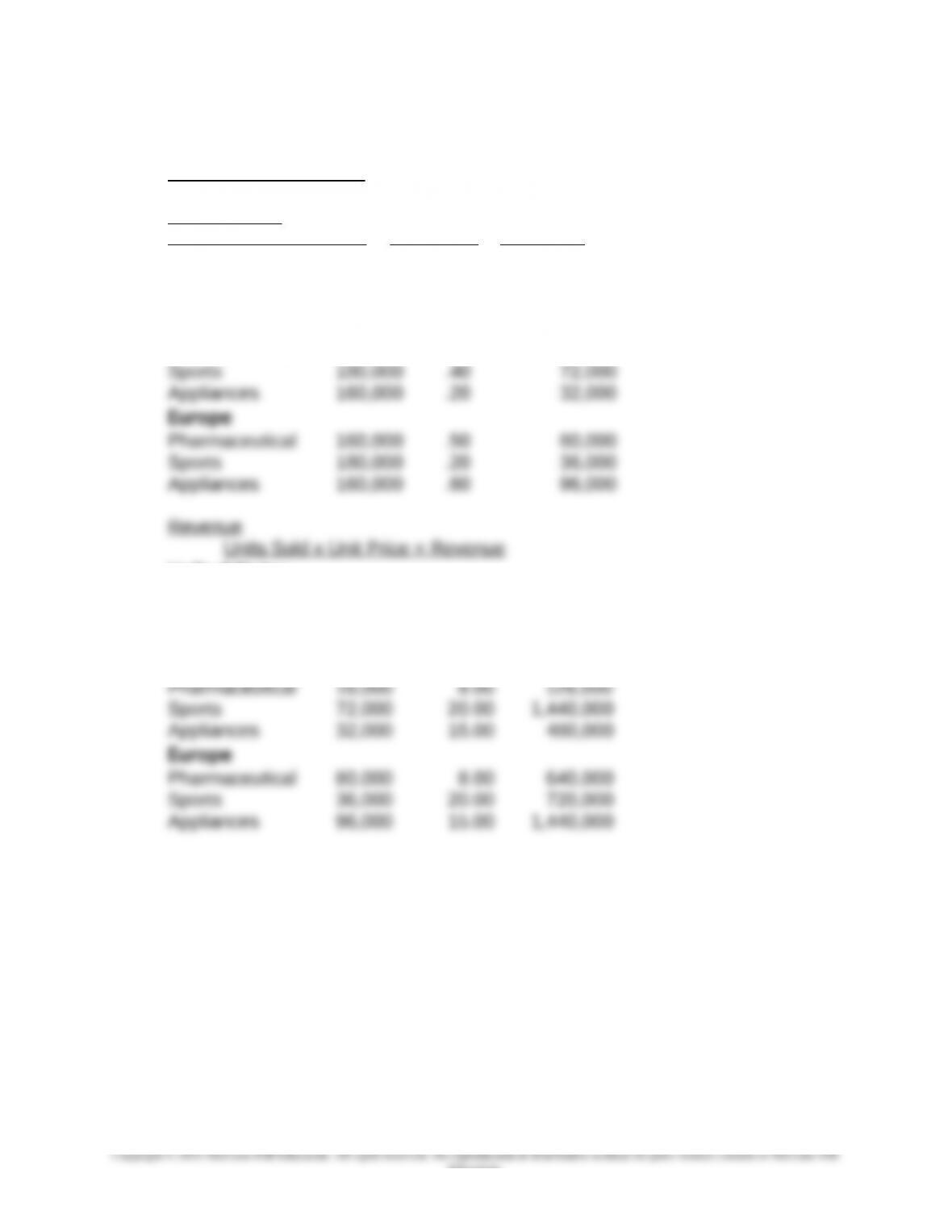

Supporting Calculations

Sales in Units

United StatesTotal Units X % of Sales = Units Sold

Pharmaceutical 160,000 .40 64,000

Sports 180,000 .40 72,000

Appliances 160,000 .20 32,000

Canada

Pharmaceutical 160,000 .10 16,000

United States

Pharmaceutical 64,000 $8.00 $512,000

Sports 72,000 20.00 1,440,000

Appliances 32,000 15.00 480,000

Canada

18-60

Education.