Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

6. Identify the activity drivers for overheads activity-cost pools identified in this study and explain the

reasons for the selection?

Gasoline Sales Attendants (Labor): Volume of gasoline sold (a unit-level activity driver).

The principal responsibility of a kiosk attendant is to receive payments from customers for gasoline

purchases, which is a batch-level activity. Given that the average volume of gasoline sold to each

benefits payments.

Kiosk Facility: Volume of gasoline sold.

The entire purpose of the kiosk facility is to house the attendants who receive payments from

customers for gasoline purchases.

grade of gasoline irrespective of the volume of gasoline sold (for example, the gasoline tanks).

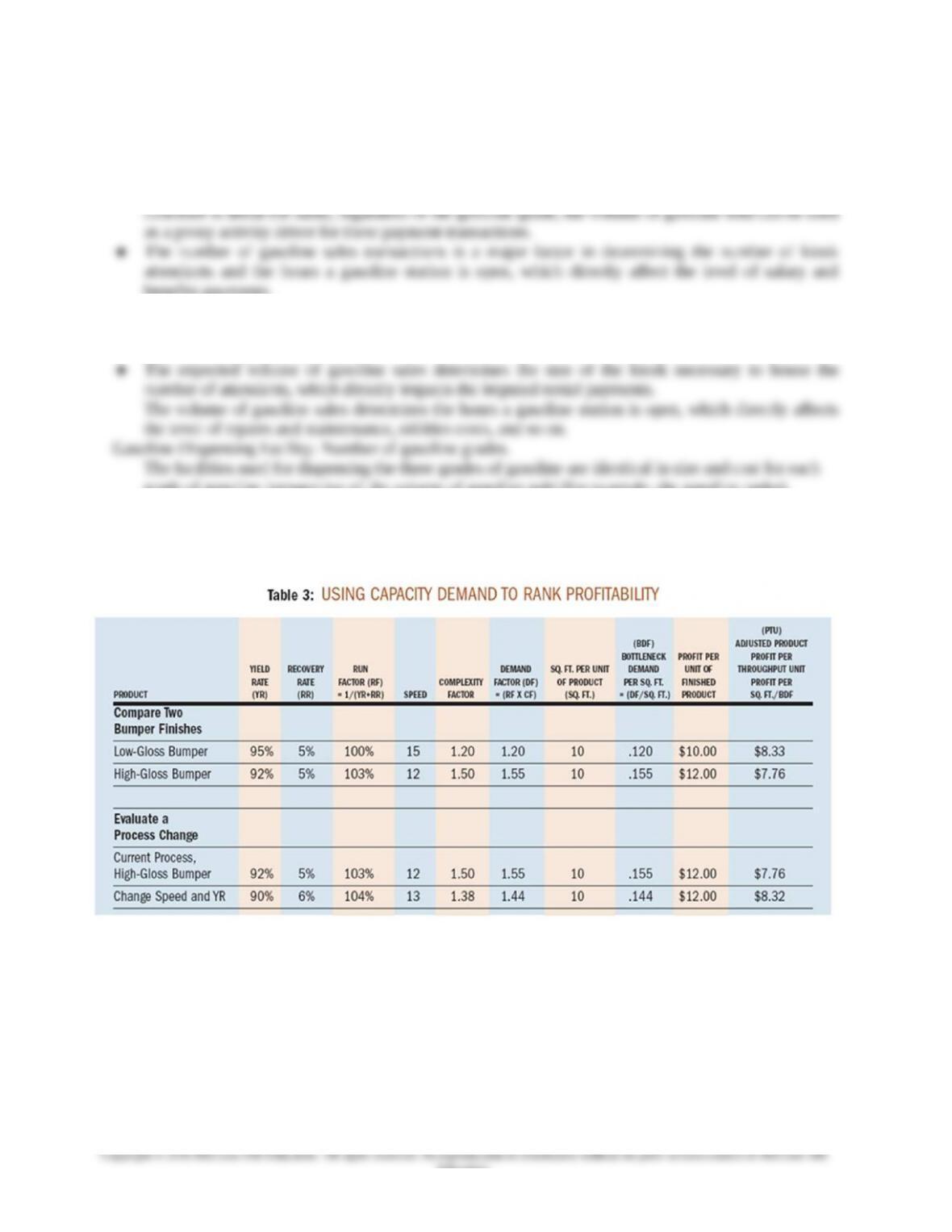

7. List examples of gasoline-dispensing facilities for a gasoline service center and identify whether each of

the facilities is a common or a gasoline grade-specific asset. (Please refer to Table 3 below for the

answer).

5-37

Education.

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-2 Activity-Based Benchmarking and Process Management - Managing the Case of Cardiac

Surgery

1. Describe briefly the hospital’s costing system.

Generally, the hospital’s costing system begins with the division of each general ledger account into

cost types: variable direct cost, fixed direct cost, and fixed indirect cost.

At the cost center or department level, each indirect cost center is assigned an allocation base (such as

total cost, square feet, or gross revenue) to be used to spread the indirect costs to the direct cost centers.

budgeted volume. The standard unit costs for primary products/services are then summed up into

intermediate products, such as a surgical procedure and rolled up into final product/service, such as

inpatient days or admissions.

2. Describe steps in activity-based benchmarking for medical-care processes.

5-38

Education.

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-3 Using ABC to Asses Channel/Customer Profitability

This article explains how ABC was used by a firm (TEC) in the temporary employment industry to better

identify the profitability of its service distribution channels and individual customers.

Discussion Questions:

1. What are the four steps used in implementing ABC costing at TEC?

Step 1. Develop the activity dictionary.

Step 2. Determine how much the organization is spending on each of its activities.

2. What are the activity consumption drivers that TEC has chosen for each of the three activities: filling

work orders, hiring temporaries, and processing payroll?

From Table 2:

3. Which customer channel is most profitable, clerical or industrial, and why?

demand lower rates and have significantly higher worker’s compensation rates.

4. Within the industrial channel, which class of customers is most profitable and why?

5. In the study of the four largest customers, which is the most profitable and why?

The newspaper publisher and the food processing company had negative contributions, while the

trailer manufacturer has a modest contribution. The highest contribution was for the chemical company

5-39

Education.

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-4 Cost System Redesign at a Medium-Sized Company

This article looks at a company that was experiencing unprofitable growth and weak cash-flow activity. The

authors examine how an ABC method allowed the company to become more competitive, to look at their

current product mix and product lines, and ultimately, to improve cash flow and product profitability.

Discussion Questions

1. Why for any manufacturer is proper inventory management important?

For virtually any manufacturer, proper inventory management ensures the availability of the right items at the

productivity, profit, and return on investment (ROI).

2. What are the elements of an ABC system?

3. What is a cost objective?

4. Why are duration drives used in an ABC system?

5. What internal factors limit the ABC model’s ability to influence the decision-making process in a

company?

Many internal factors, including corporate culture, available information systems, and current financial

process.

5-40

Education.

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-5 Implementing Time-Driven Activity-Based Costing at a Medium-Sized Electronics

Company

This article revisits the company described in reading 5-4, which has now adopted a traditional ABC system.

In this article the authors examine how a time-driven ABC (TDABC) system might overcome some of the

drawbacks of the traditional ABC system while provide more insightful information about the demand that

products put on the available resources.

Discussion Questions

1. What are the goals of an ABC system?

At one level, the goal of an ABC system is to allocate indirect (support) costs in such a way that the

resulting cost information reflects more accurately the resource demands/resource consumption of an

and ABC system is to provide better information for management decision making.

2. What are the potential drawbacks of a traditional ABC system?

The issues faced by XYZ are representative of a major drawback of a traditional ABC system. First is

the complexity of the implementation. A traditional ABC system is very data intensive and collecting

and analyzing the data can prove to be overwhelming for a small to medium sized firm. Additionally,

there is the difficulty in keeping all the data current in order for management to be able to rely on the

3. What benefits does a TDABC system offer over a traditional ABC system?

Advocates of time-driven activity-based costing maintain that this system is an improvement on

traditional ABC systems in the following respects:

TDABC eliminates the need for the time consuming, subjective, interview-and-survey process to

define resource pools. Rather, TDABC relies only on simple time estimates that, for example, can be

established based on direct observation of processes.

TDABC accurately accounts for the complexities of business transactions (such as variations of

operational transactions) by using time equations. These equations more accurately reflect the time

5-41

Education.