Chapter 06 – Process Costing

CHAPTER 6: PROCESS COSTING

QUESTIONS

6-1 A company that should use a process costing system typically has homogenous

6-2 Process costing is likely used in industries such as chemicals, oil refining,

textiles, paints, flour, canneries, rubber, steel, glass, food processing, mining,

6-3 Differences between job and process costing: (1) accumulating costs by job

versus department, (2) collecting cost data using the job cost sheet vs. the

6-4 Equivalent units are the number of completed units that could have been

6-5 If direct materials are added at the beginning of the process rather than uniformly

materials to finish the work-in-process beginning inventory.

6-6 A production cost report is a report, which summarizes the physical units and

equivalent units of a department, the costs incurred during the period, and costs

assigned to both finished goods and work-in-process inventories. The five key

computation of unit costs, and assignment of total costs.

6-7 The weighted-average method equivalent units include both the units placed into

production in the current period and the units from the prior period that are still in

production at the beginning of this period. FIFO method does not include the

6-8 The weighted-average method would be inappropriate when a firm’s beginning

6-1

Chapter 06 – Process Costing

6-9 The advantage of the weighted-average method is its simplicity.

6-10 From the standpoint of cost control, the FIFO method is superior to weighted-

average because the cost per equivalent unit under FIFO represents the cost for

6-11 Transferred-in costs are costs of work done in the prior department that are

transferred into the current department.

6-12 Work-in-Process Inventory — Second Department $50,000

6-13 Under the FIFO method of handling units transferred out, beginning inventory

6-14 Under the weighted-average method, it makes no difference when a product is

started; all units completed in the same period or in the ending inventory of that

period are treated the same. In computing the equivalent units, this method looks

6-15 Process costing uses the same manufacturing accounts as job costing. Journal

entries are essentially the same as in job costing. However, instead of tracing

departments.

6-16 Backflush costing is a simple costing system that assigns materials and

conversion costs directly to finished goods inventory, by assuming there is little or

6-17 Activity-based process costing is an extension of the basic process costing

model in which certain products require significantly more processing costs in

certain activities. Activity-based costing is used together with process costing to

approach.

6-2

Education.

Chapter 06 – Process Costing

BRIEF EXERCISES

6-18

Work-in-process inventory, February 28 65,000

Learning Objective: 06-04

Topic: Illustration of Process Costing

Category:

Blooms: Apply

AACSB: Analytic

AICPA FN: Measurement

AICPA BB:

Difficulty: Easy

Feedback

6-19

Work-in-process Inventory, June 1 63,000

Learning Objective: 06-04

Topic: Illustration of Process Costing

Category:

Blooms: Apply

AACSB: Analytic

AICPA FN: Measurement

AICPA BB:

Difficulty: Easy

Feedback

6-20

Units started 5,200

Learning Objective: 06-04

Topic: Illustration of Process Costing

Category:

6-3

Education.

Chapter 06 – Process Costing

Blooms: Apply

AACSB: Analytic

AICPA FN: Measurement

AICPA BB:

Difficulty: Easy

Feedback

Units completed 7,300

6-21

Units completed 79,000

Learning Objective: 06-04

Topic: Illustration of Process Costing

Category:

Blooms: Apply

AACSB: Analytic

AICPA FN: Measurement

AICPA BB:

Difficulty: Easy

Feedback

6-22

a) Weighted Average

Materials: 47,000

Conversion: 45,500

b) FIFO

Materials: 45,000

Conversion: 44,500

Learning Objective: 06-04

Topic: Illustration of Process Costing

Category:

Blooms: Apply

AACSB: Analytic

6-4

Chapter 06 – Process Costing

AICPA FN: Measurement

AICPA BB:

Difficulty: Easy

Feedback:

a) Weighted Average

Materials: 47,000 = 44,000 + 1.0 x 3,000

6-23

Cost of Goods Completed: $50,000

Learning Objective: 06-04

Topic: Illustration of Process Costing

Category:

Blooms: Apply

AACSB: Analytic

AICPA FN: Measurement

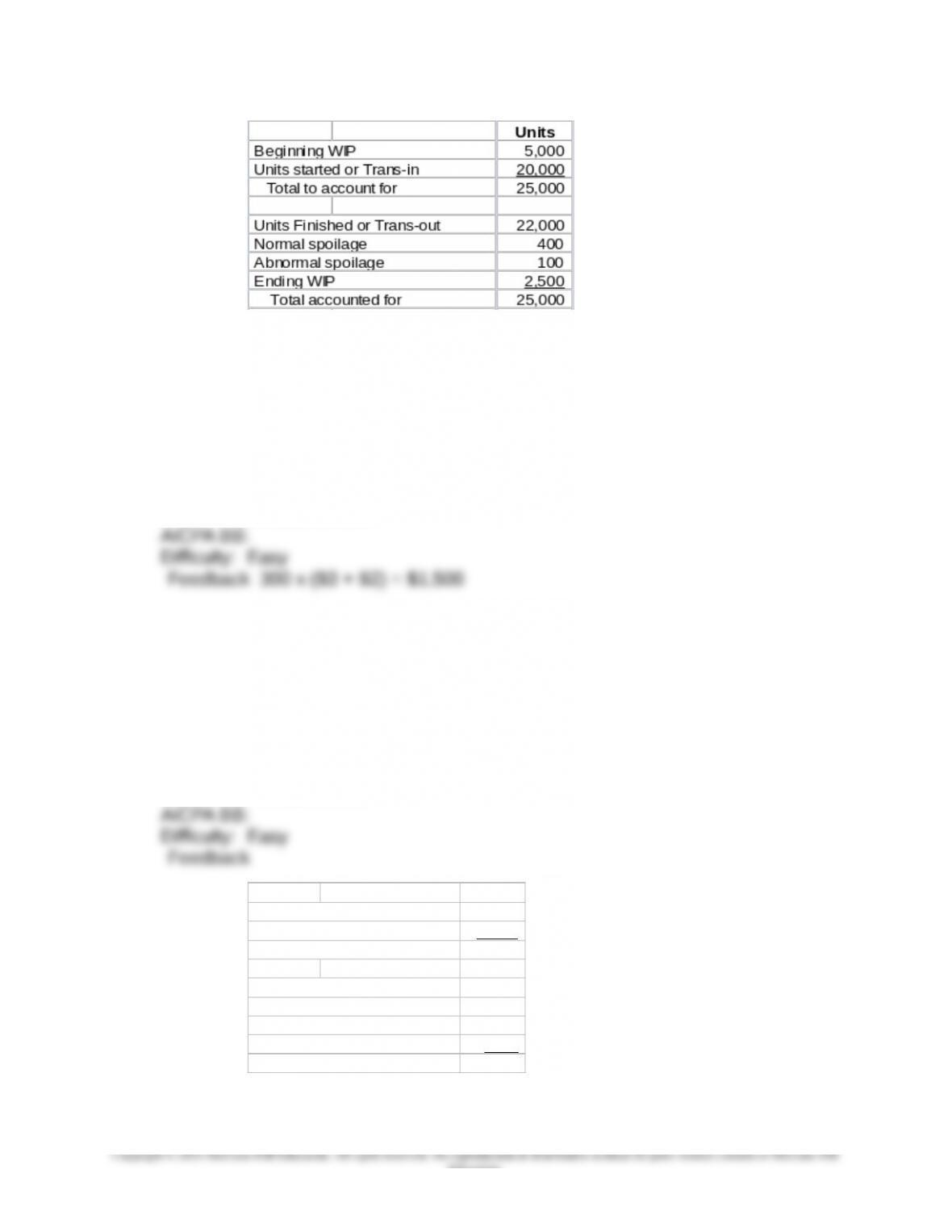

6-24 Ending WIP: 2,500 units

Learning Objective: 06-04

Topic: Illustration of Process Costing

Category:

Blooms: Apply

AACSB: Analytic

6-5

Education.

Chapter 06 – Process Costing

6-25

Cost of Spoilage $1,500

Learning Objective: 06-04

Topic: Illustration of Process Costing

Category:

Blooms: Apply

AACSB: Analytic

AICPA FN: Measurement

6-26 The number of units transferred-in is 33,000 units

Learning Objective: 06-04

Topic: Illustration of Process Costing

Category:

Blooms: Apply

AACSB: Analytic

AICPA FN: Measurement

6-6

Education.

Units

Beginning WIP 6,000

Units started or Trans-in 33,000

Total to account for 39,000

Units Finished or Trans-out 35,000

Normal spoilage 0

Abnormal spoilage 0

Ending WIP 4,000

Total accounted for 39,000

Chapter 06 – Process Costing

EXERCISES

6-27 Process Costing in Process Industries (10 min)

There are a number of possible answers here. Some examples are given

in the chapter, as well as exercises 4-29 and 4-30 from chapter 4. The

exercise is intended for class discussion. The goals is to have the

students able to identify process-oriented companies in industries such as

chemicals, food processing, beverages, etc. The instructor may choose

to follow up this short question with a more substantive one such as 6-29

which gets into the details of one type of process industry, sugar

manufacturing.

6-7

Education.

Chapter 06 – Process Costing

6-28 Equivalent Units; Weighted-Average Method (15 min)

1. Calculate the number of tons completed and transferred out during the

2. Calculate the number of equivalent units for both materials and

conversion for the month of May, assuming that the company uses the

weighted-average method.

3. How would your answer in part 2 change if the percentage of completion

in ending inventory were as follows: materials 30%, conversion 40%?

4. Process costing is a good fit for the fish processing industry because

there is single or a small number of products that are processed through a

series of well-defined processing steps: moving, cleaning, preparation for

shipment, etc.

Learning Objective: 06-04

Topic: Illustration of Process Costing

Category:

Blooms: Apply

AACSB: Analytic

AICPA FN: Measurement

AICPA BB:

Difficulty: Easy

Feedback for parts 1, 2, and 3:

1. Work-in-process inventory, 5/1 1,000

Units started 7,000

Total units to account for 8,000

6-8

Education.

Chapter 06 – Process Costing

6-28 (continued -1)

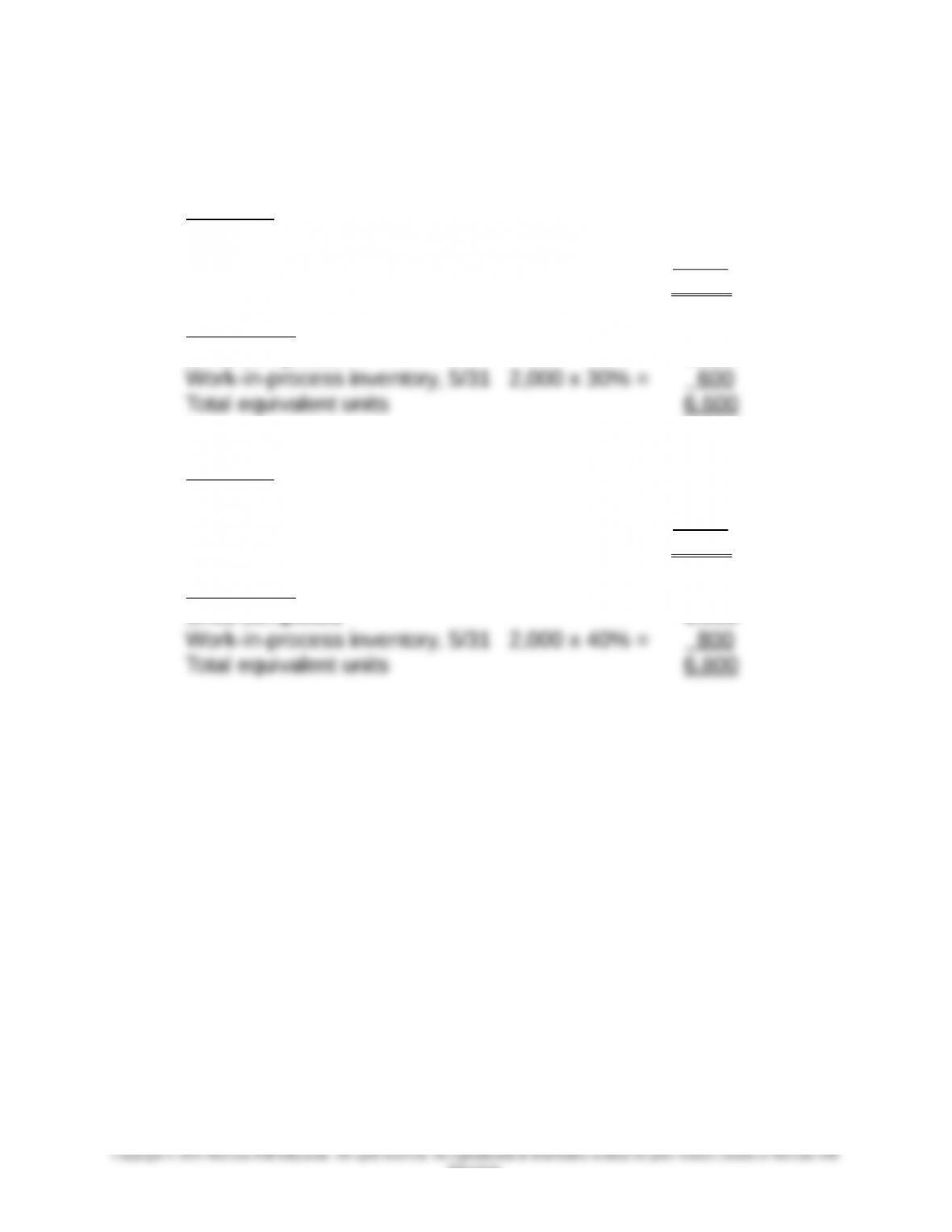

2. Equivalent units — Weighted-Average Method

Materials:

Units completed 6,000

Work-in-process inventory, 5/31 2,000 x 50% = 1,000

Total equivalent units 7,000

Conversion:

Units completed 6,000

3. Equivalent units — Weighted-Average Method

Materials:

Units completed 6,000

Work-in-process inventory, 5/31 2,000 x 30% = 600

Total equivalent units 6,600

Conversion:

Units completed 6,000

6-9

Education.

Chapter 06 – Process Costing

6-29 Process Costing in Sugar Manufacturing (20 min)

1. There are very likely to be transferred in costs in sugar

manufacturing, as there are a number of processes, each of which

could be a separate manufacturing department with its own process

cost report. There are seven steps in the manufacturing process so

there are possibly as many as seven departments, each with its own

cost report. The reason for multiple cost reports is to monitor the flow

of costs throughout the manufacturing process start to finish, and to

be able to control costs in each department. The individual cost

reports provide a means for tracking cost management performance

of each department over time. For example, it would be possible to

next chapter, Chapter 7.

2. As noted in the problem, the raw material for sugar production (sugar

cane) goes through periods of very volatile changes in price. This

means the cost of sugar can fluctuate greatly, and the production

costs may be given greater attention, especially in periods when

prices are low and sugar manufacturers compete on cost leadership

since sugar is a commodity. One could argue that FIFO provides a

better means to analyze costs since it separates costs from period to

period. Alternatively, one could argue that an advantage of the

weighted average method is that it would tend to smooth the changes

6-10

Education.