Chapter 19 – Strategic Performance Measurement—Investment Centers

19-31 (Continued-1)

In the current situation, we have:

Transfer Price:

Incremental Cost per unit = $500

the use of this transfer-pricing rule (a) maintained divisional autonomy,

and (b) provided the appropriate “signal” to internal decision-makers (i.e.,

buyers and sellers).

3. If the Fabrication (i.e., producing) Division had excess capacity, this

means that the opportunity cost associated with any internal transfers

would be zero. Thus, the transfer price, as specified by the general

transfer-pricing rule, would be:

Transfer Price = Incremental Cost per Unit + Opportunity Cost per Unit

situation that we state that the general transfer-pricing rule provides the

minimum transfer price, from the selling division’s standpoint.

4. As might be expected, the general transfer-pricing rule “works” in the

the rule is requirement to estimate opportunity costs. Under a perfectly

19-31 (Continued-2)

19-21

Education.

Chapter 19 – Strategic Performance Measurement—Investment Centers

competitive market (as was assumed in this assignment), this may not be

much of a problem. However, under other market conditions, we know

that demand is partly a function of the quantity sold, both internally and

externally. (In other words, there are demand interactions that complicate

the chapter.

19-22

Chapter 19 – Strategic Performance Measurement—Investment Centers

19-32 Transfer Pricing; Decision-Making (25 minutes)

1. Division A’s purchase decision from the overall firm perspective:

Purchase costs from outside 10,000 × $150 = $1,500,000

fixed costs are not affected by the decision, Division A should buy

inside from Division B for the benefit of the entire firm.

2. As above, but in addition, if Division A buys outside, Division B saves

an additional $200,000:

Purchase costs from outside 10,000 × $150 = $1,500,000

3. Assuming the outside price drops from $150 to $130:

Purchase costs from outside 10,000 × $130 = $1,300,000

Chapter 19 – Strategic Performance Measurement—Investment Centers

19-32 (continued)

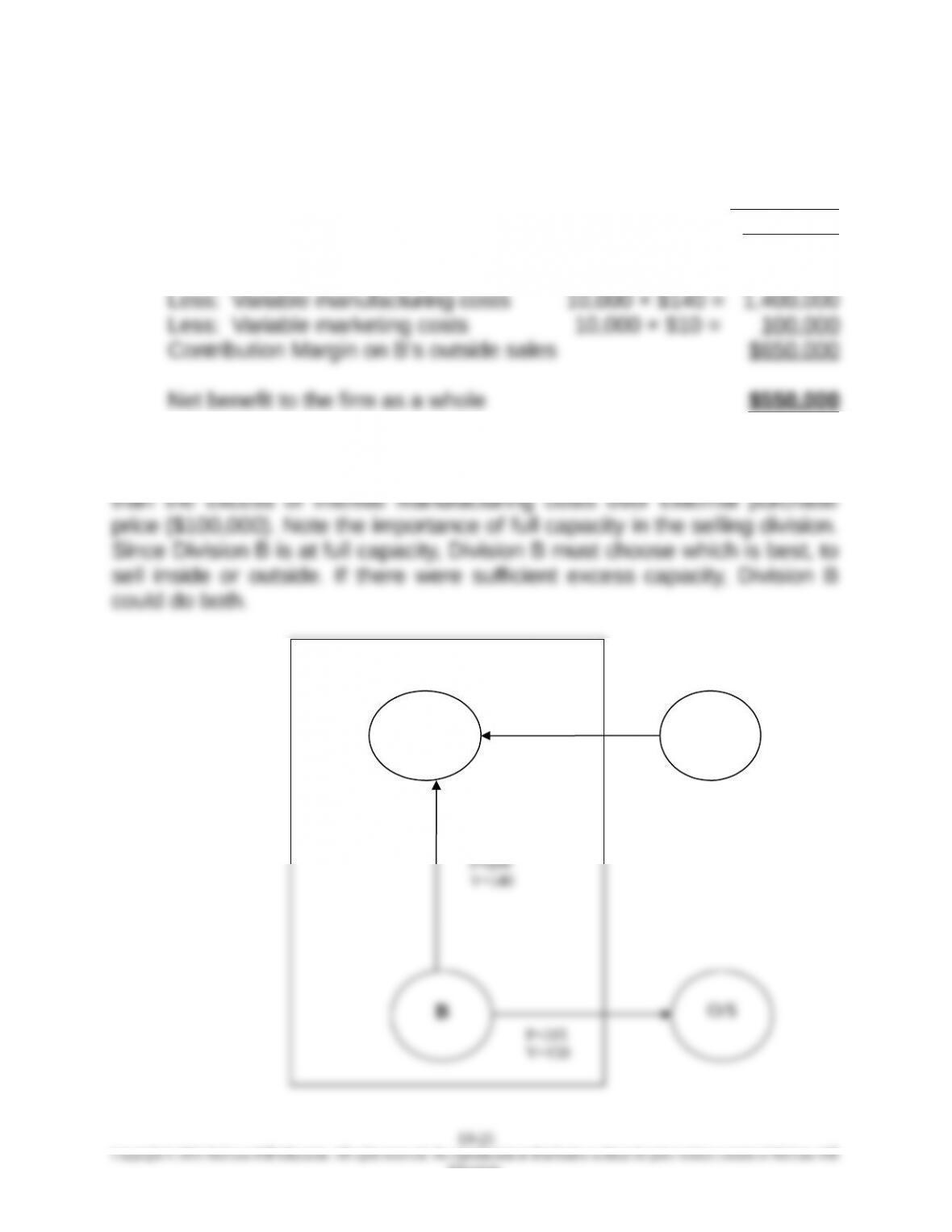

19-24

P=150

P=200

V=140

O/S

A

B

B is at 100% capacity

Chapter 19 – Strategic Performance Measurement—Investment Centers

19-33 Transfer Pricing; Decision-Making (20 minutes)

Purchase costs from outside 10,000 × $150 = $1,500,000

Less: Savings in variable costs 10,000 × $140 = 1,400,000

Net Cost (Benefit) of External Purchase $ 100,000

B sales to other customers 10,000 × $215 = $2,150,000

The firm as a whole is better off (by $550,000) if Division A buys outside

since the contribution of Division B’s outside sales ($650,000) is greater

Education.

Chapter 19 – Strategic Performance Measurement—Investment Centers

19-34 Transfer Pricing; International Taxation (25 minutes)

The change in transfer price would simultaneously increase the

profitability of the foreign subsidiary where taxes are lower and reduce

Singapore

Subsidiary

United States

Subsidiary Total

INCOME PRIOR TO INCREASE IN TRANSFER PRICE

Revenues $2,500,000 $3,500,000 $6,000,000

Mfg. Costs 1,500,000 2,500,000 4,000,000

INCOME AFTER INCREASE IN TRANSFER PRICE

Revenues $3,000,000 $3,500,000 $6,500,000

Mfg. Costs 1,500,000 3,000,000 4,500,000

Gen. & Adm. Costs 350,000 200,000 550,000

Note: An equivalent, short-cut calculation would be:

19-26

Education.

Chapter 19 – Strategic Performance Measurement—Investment Centers

PROBLEMS

19-35 Return on Investment (ROI); Different Measures for Total Assets (50

minutes)

1. Net book value (NBV) of fixed assets for each division (000s):

HEALTHCARE: $70 × 11 years remaining useful life = $770

COSMETICS: $70 × 9 years remaining useful life = $630

ROI using historical cost of divisional assets:

The COSMETICS Division is more profitable than the HEALTHCARE

Division, based on ROI calculated using net book value (NBV) of

divisional fixed assets (plus the current balance sheet value of current

assets).

2. a.

Gross Book Value (GBV) for each division:

ROI:

b. (GBV at historical cost) × (construction cost index in 2016 ÷

construction cost in year of construction):

19-27

Education.

Chapter 19 – Strategic Performance Measurement—Investment Centers

19-35 (continued-1)

c. (Current NBV of fixed assets) ×(construction cost index in 2016 ÷

construction cost in year of construction)

d. ROI Based on Current Replacement Cost of Fixed Assets (plus

current book value of current assets):

3. a. The best measure for evaluating the manager is replacement cost, as

it corresponds to the “going-concern” value of the investment. The

objective is to identify a measure of investment that fairly reflects the

productive capacity of the assets. Often, net book value falls much

faster than the productive capability of the assets, and thus, the ROI

with the older assets overstates the profitability of the unit. The use of

19-28

Chapter 19 – Strategic Performance Measurement—Investment Centers

19-35 (continued-2)

The advantages of the replacement cost measure are fairness, since it

avoids the age bias issues associated with the net book value

measure, and motivation, since it reflects the current value of the

b. The evaluation of the division should use replacement cost for the

same reasons as explained in (a) above. The only difference here is

when either division might be sold or relocated, in which case the

liquidation value is relevant. Top management can also look at the

19-29

Education.

19-36 Return on Investment (ROI) and Incentive/Goal-Congruency Issues;

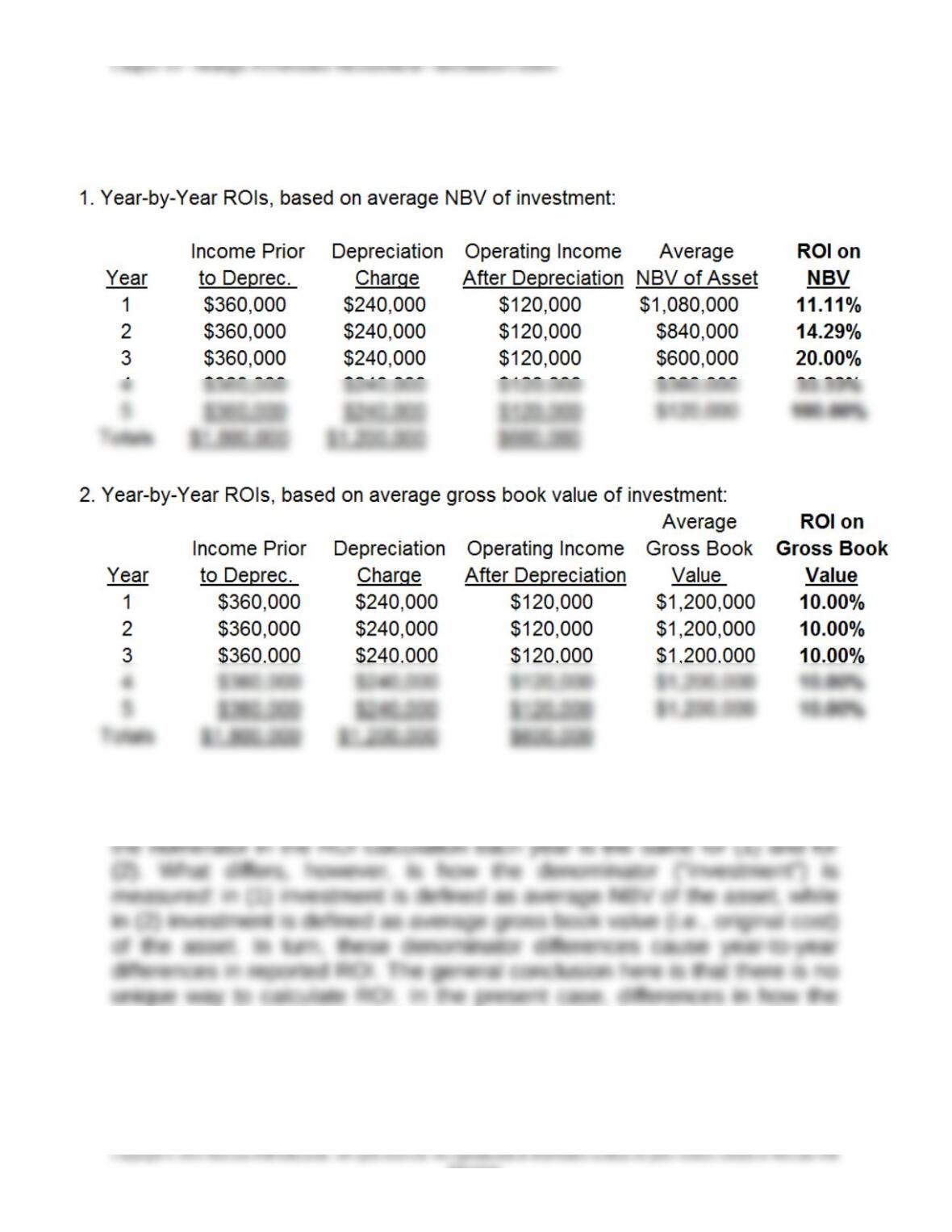

Spreadsheet Application (60-75 Minutes)

3. The depreciation calculation, and therefore the year-by-year operating

incomes for the proposed investment, are identical in (1) and in (2). That is,

asset base (level of investment) was measured results in vastly different

year-to-year ROIs for the two specified alternatives. These differences

introduce ambiguity in the decision-making process (unlike the use of the

NPV criterion).

19-30

Education.