Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products

7-47 (continued -1)

2. Quality Chemical should not sell H-35 after additional processing

as the incremental revenue of the sales beyond the split-off point is

less than the incremental cost of further processing.

Per gallon sales value after additional processing $6.25

Per gallon sales value at the split-off point 4.00

3. There is a clear ethical issue here, as the pesticide, J-23, may

have contaminated the food products chemical, S-210, thus

representing a health hazard to humans. The first step for the

production supervisor is to notify plant management. An appropriate

response by plant managers would be to immediately determine

whether there is a health risk, and if so, to notify immediately all users

of the swimming pool chemical and to put in place production

7-71

Education.

Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products

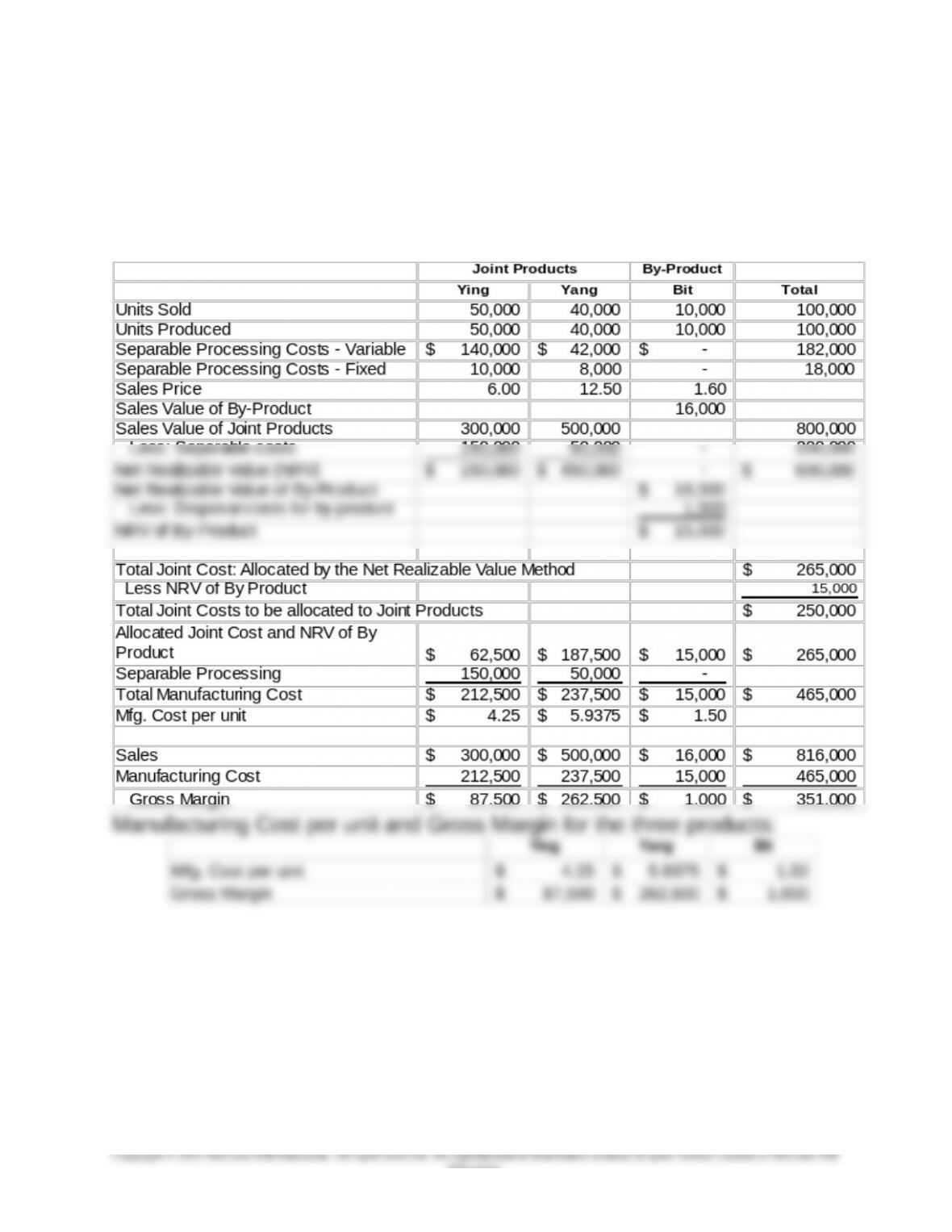

7-48 Joint Products; By-Products; Appendix (40 min)

1.,2. Note that the distinction between variable and fixed separable

processing costs is irrelevant for the solution of the problem. The total

separable processing cost is used to solve for NRV.

7-72

Education.

Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products

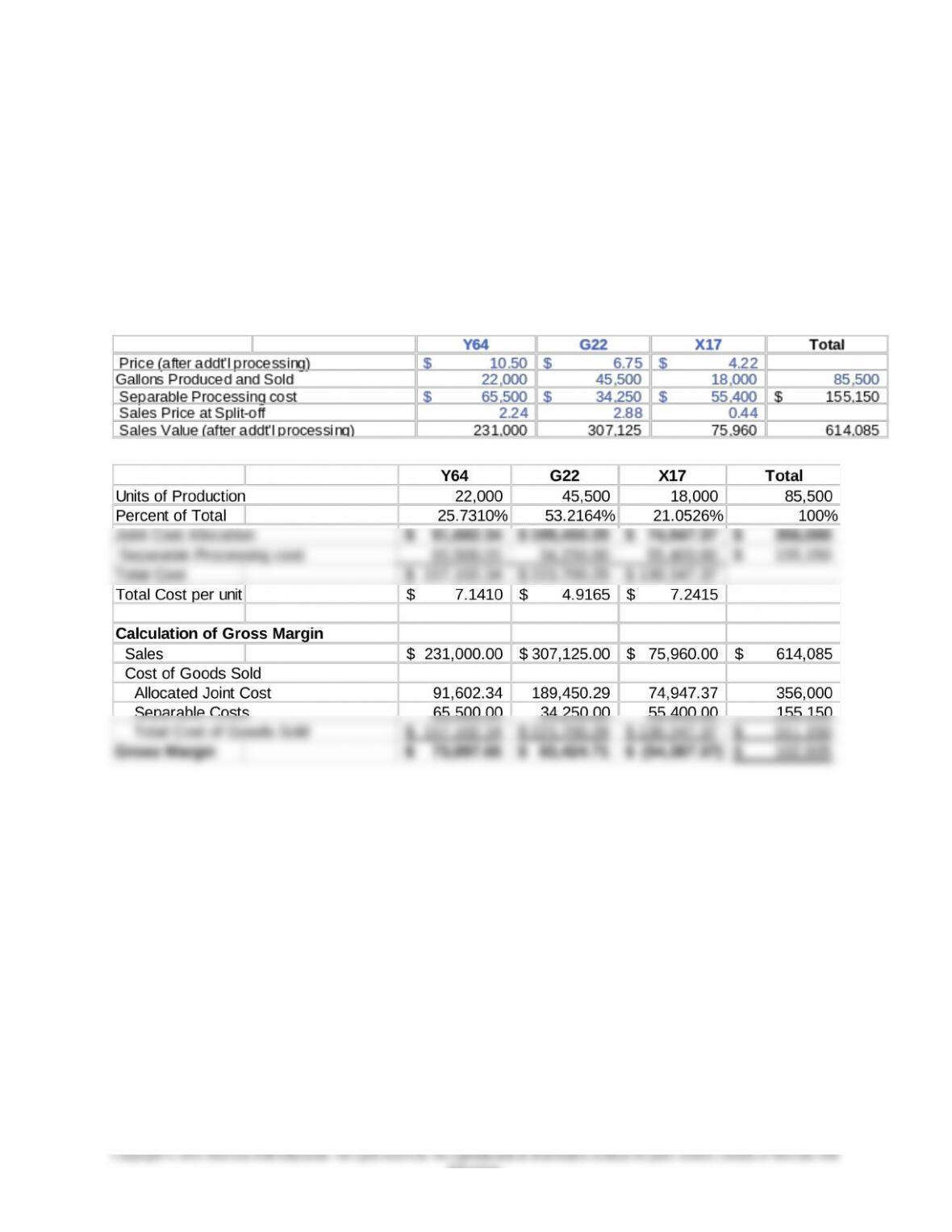

7-49 Joint Products (35 min)

Note: the information on number of customers is irrelevant

1.a. The Physical Unit Method

First, summarize the data and determine sales value:

Next, determine the cost allocation and gross margin:

7-73

Education.

Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products

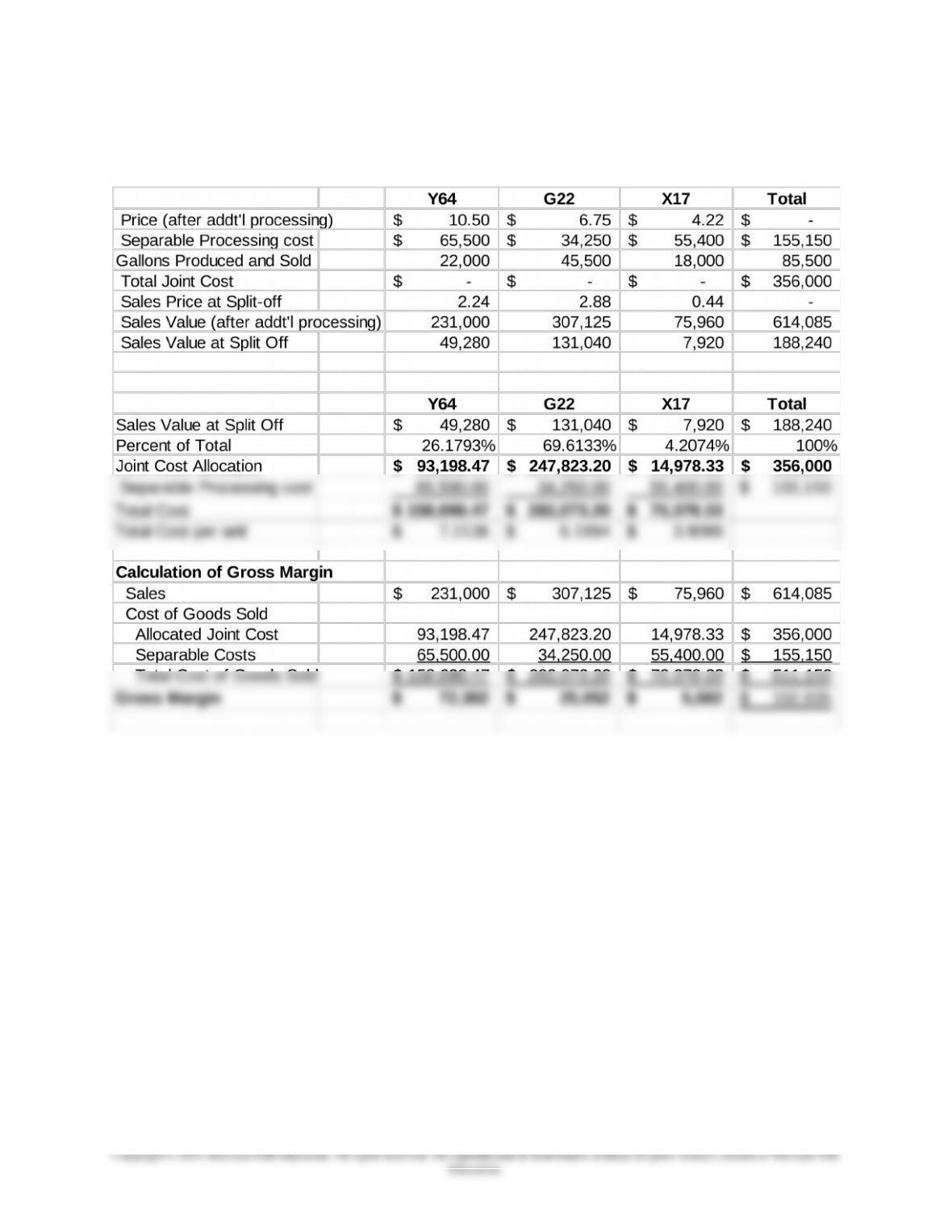

7-49 (continued -1)

1.b The Sales Value at Split Off Method

7-74

Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products

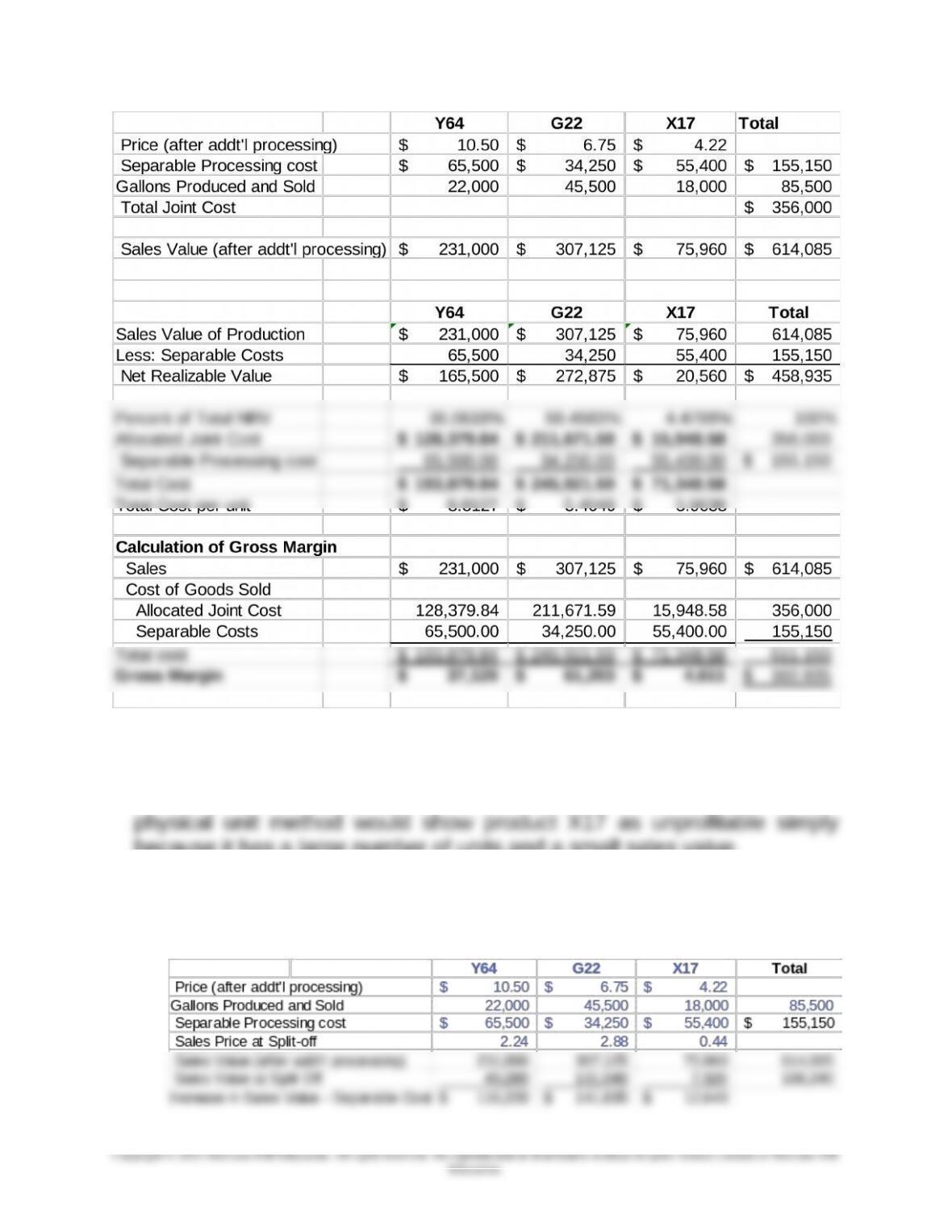

7-49 (continued -2)

1.c. The Net Realizable Value Method

7-75

Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products

7-49 (continued-3)

2. The Net Realizable Value Method is preferred because it takes into

account the value of the product after separable costs. Note that the

because it has a large number of units and a small sales value.

3. The increase in sales value after additional processing cost is greater

than the additional processing costs for all three products, so that Yonica

has the correct policy in processing all products to the final sales value.

7-76

Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products

Also, note that G22 has far fewer customers than the other two products

and G22 also has the highest sales value and gross margin of all the

products irrespective of the allocation method chosen. This suggests

4. Yonica’s strategy is based on environmentally friendly policies, and the

odds are that the company’s customers will increasingly seek out

companies, like Yonica, that produce environmentally friendly products.

Consumers are aware of the environmental costs of certain products,

especially those in the chemical industry, so that this is likely to

positively affect the demand for Yonica’s products over time. Also,

7-49 (continued – 4)

5. The key global issues for Yonica include the strategic decisions

regarding the sourcing of its raw materials, the purchase and

transportation costs of the raw materials, together with the potential

purchase transactions in foreign currencies.

6. Yonica has a good position in sustainability because the company’s

business model it based on recycling waste chemicals. To improve this

position, Yonica should look for ways to reduce the energy use and

environmental impact of the waste chemicals the firm purchases.

7-77

Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products

7-78

Education.

Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products

7-50 Joint Cost Allocation: Managerial Incentives (15 min)

The use of total production to allocate the cost of the insurance does satisfy

the objective of fairness – the larger plants pay more. But it does not

provide much of a desired incentive – to reduce accidents, as Mike points

out. However, his suggestion is simply another measure of size, in this

case number of personnel, and it would probably have very nearly the

same effect on allocation as the use of total output.

Alternatively, the allocation could be based on the number of accidents –

those plants with more accidents pay more of the insurance bill. This basis

could also be adjusted for size, by using for example, the number of

7-79

Education.