Chapter 09 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-40 (Continued-1)

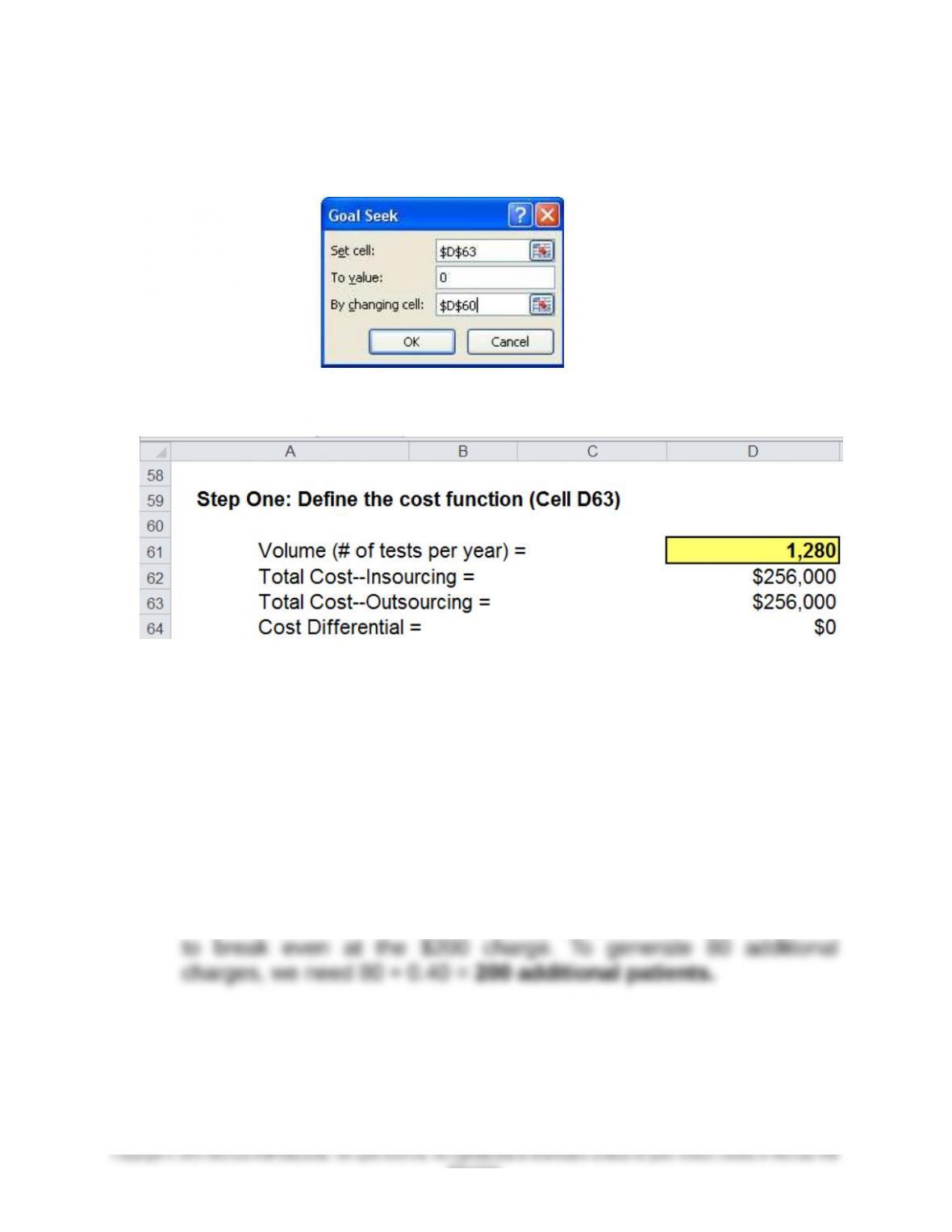

Step Two: Run Goal Seek

Step Three: Results

Thus, at 1,280 tests per year, the total cost under each of the two

decision alternatives would be the same: $256,000.

3. Current number of patients per year needing analysis = 3,000

# needing blood-gas analysis = 3,000 × 40% = 1,200

The difference = 1,280 − 1,200 = 80 tests per year

80 is the additional number of blood gas samples (per year) needed

9-40

Education.

Chapter 09 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-40 (Continued-2)

4. Indifference point—external price/test that would make the lab

indifferent between the two decision alternatives (i.e., insource vs.

outsource):

Let p = required charge (external service fee)

Current # of tests performed per year = 3,000 × 0.40 = 1,200

To solve for the breakeven charge rate (per test):

Outsourcing Insourcing

Note: the above result could have been obtained, as well, through

the use of Goal Seek.

5. Additional factors to be considered:

a. time-value-of-money (opportunity cost of capital)—the decision at

hand is really a capital budgeting problem

b. quality and reliability of the in-house testing alternative versus

leverage is more sensitive to changes in volume.

e. would the purchase of the machine now provide a disincentive to

invest in this area in the future?

9-41

Education.

Chapter 09 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-41 CVP Analysis in a Professional Service Firm (30 min)

1. If operating profit is to increase, the contribution margin (i.e., revenue

less variable costs) of the new business must exceed any incremental

fixed costs.

For a breakeven situation, incremental revenue (billings, both from the

county audits and from any new business) must equal incremental

costs (both variable and fixed).

Let Y = the minimum revenue that must be earned from the county

work in order to insure that operating profit of the firm does not

decrease. Thus, looking at this new business proposal in its entirety:

Incremental Profit = Incremental Revenue – Incremental Variable

Clearly, the key to the bidding strategy is the desirability of bringing in

2. At breakeven point for the total new business (county audit job +

additional new business), incremental revenue (billings) in total would

equal incremental costs (both variable and fixed).

incremental profit = incremental revenues (billings) − incremental

variable costs − incremental fixed costs

9-42

Education.

Chapter 09 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-41 (Continued)

Alternatively, at breakeven:

Incremental revenues (billings) = incremental costs (variable + fixed)

Let X equal the minimum number of hours of additional new business

required to breakeven. At breakeven, we have:

Note that the managing partner’s estimate of 750 hours of new

9-43

Education.

Chapter 09 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-42 CVP Analysis; Sensitivity Analysis; Multiple Products (50-60 min)

1. GoGo Juice’s profit (loss) before tax from implementing the promotional

coupon with no change in sales volume and sales mix is ($6,500)

Gasoline

Food &

Beverage Other Total

Sales Revenue $100,000 $60,000 $40,000 $200,000

Coupons redeemed

(note 1)

(15,000) (15,000)

Cost of Sales (note

2)

(75,000) (36,000) =

0.6 × 60,000

(20,000) =

0.5 × 40,000

(131,000)

Contribution Margin $10,000 $24,000 $20,000 54,000

Fixed costs (note 3) 60,500

Loss before tax $(6,500)

Note 1: Coupons redeemed: total sales of ($200,000 × 75%) ÷ 10 ($1 per

gallons; 40,000 gallons × $1.875/gallon = $75,000

Note 3: Fixed costs:

Labor ($10,000 + $2,500) $12,500

Rent, power, supplies, etc. 40,000

Depreciation 7,500

2. The breakeven point in sales dollars for GoGo, based on the weighted-

average contribution margin ratio (CMR) approach:

Weighted-average contribution margin ratio = total contribution

margin ÷ total sales dollars

9-44

Education.

Chapter 09 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-42 (continued-1)

3. Allocation of total breakeven sales dollars across the three product lines

(based on sales mix determined on the basis of relative sales dollars, not

units, of the three products):

Total breakeven sales dollars (#2 above) = $224,074

Sales mix percentages, based on relative sales dollars:

Gasoline: $100,000 ÷ $200,000 = 0.50

Other: $40,000 ÷ $200,000 = 0.20

Breakdown of total breakeven sales dollars ($224,074):

4.

Sales revenue ($200,000 × 1.2) $240,000

Variable costs (sales − CM) 156,000

Contribution margin ($240,000 × 35%) 84,000

5. Sensitivity analysis is used to deal more effectively with uncertainty or

risk. Sensitivity analysis is a “what-if’ type of analysis used to determine the

outcomes if any parameters change from the initial assumptions. For

example, revenues or costs could be changed from the initial assumptions

and a new break-even sales volume calculated.

At least three factors that make sensitivity analysis prevalent in decision-

making today include the following:

9-45

Education.

Chapter 09 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-42 (Continued-2)

As the business environment is becoming more dynamic and

competitive, sensitivity analysis provides management with an

understanding of the impact of changes in the environment. The

Sensitivity analysis aids management in identifying the key variables

6. As discussed in the chapter, the following methods that can be used to

address uncertainty in the profit-planning process:

Conventional measures associated with CVP analysis:

oDegree of operating leverage (DOL)

oMargin of safety (MOS) and margin of safety ratio (MOS%)

Sensitivity analysis:

oSimple “what-if” analysis/analyses

9-46

Education.

Chapter 09 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-43 CVP Analysis; Commissions; Ethics (50 min)

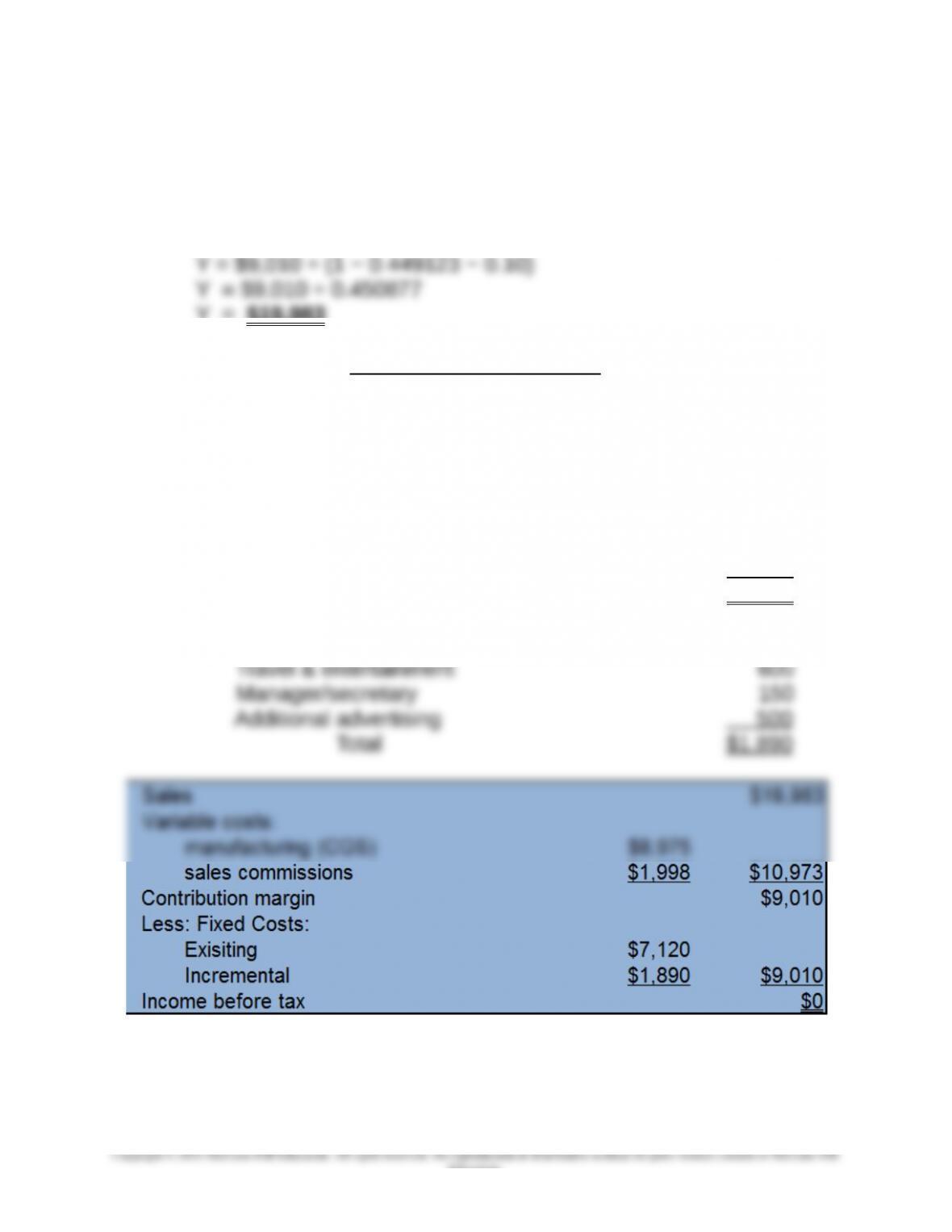

1. Breakeven dollars (dollars in thousands), Y:

Y = total fixed costs ÷ contribution margin ratio

Y = ($7,120 + $1,890) ÷ (1 − VCGS rate − commissions rate)

Y = $19,983

Supporting Calculations

Variable cost of goods sold (VCGS) rate (dollars in thousands):

$12,800 ÷ $28,500 = 44.9123%

Current fixed costs ($ thousands):

Fixed cost of goods sold $3,500

Fixed advertising cost 770

Fixed administrative cost 2,150

Fixed interest expense 700

Total $7,120

Incremental fixed costs ($ thousands):

Sales people (8 × $80) $ 640

9-47

Education.

Chapter 09 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-43(Continued-1)

2. Required sales (to maintain current level of pre-tax income, $3,450,

while paying the requested increase in commission):

Let Y = required sales level:

$3,450 = Total sales − total variable costs − total fixed costs

$3,450 = Y − (0.449123Y + 0.23Y) − $7,120

3. The general assumptions underlying breakeven analysis that may limit

its usefulness include the following:

All costs can be divided into fixed and variable elements.

Variable costs vary proportionally to volume (thus, the variable cost

function is linear)—there are no efficiency changes as output

changes

certainty

4. Let sales (in 000s) at the indifference point be Y.

Since the two decision alternatives do not affect the selling price per

unit, we can define the indifference point as the volume level that

results in equal total cost between the two decision alternatives:

9-48

Education.

Chapter 09 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-43 (Continued-2)

Cost Under Alternative #1 = Cost Under Alternative #2

0.4491Y + 0.23Y + $7,120 = 0.4491Y + $7,120 + $1,890 + 0.10Y

5. Alan Chen should consider the firm’s ethical responsibility to its

shareholders, employees and agents. The new plan would be a

savings for the firm and thus would have an upward effect on stock

price and thus benefit the shareholders. However, the plan would be

a blow to the sales agents, many of whom may be depend on Lionel

Corporation for a significant portion (or perhaps all of) their income.

9-49

Education.