Chapter 19 – Strategic Performance Measurement—Investment Centers

19-42 Calculating Return on Investment (ROI) and Residual Income (RI);

Comparing Results (25 minutes)

1. a. ROI = Operating Income ÷ Average Assets

= $2,440,000 ÷ {[$16,000,000 + ($16,000,000 ÷ 1.06)] ÷ 2}

b. RI = Operating Income – (Avg. Assets × Min. pre-tax rate of return)

= $2,440,000 – ($15,547,170 × 0.10)

2. In this case residual income (RI) provides the desired incentive for local

managers to make investments desired by top management. Delta

performance measure.

3. Like many organizations, Blackwood Industries should benefit from a

management control system which gives explicit attention to strategic

factors. The balanced scorecard (BSC) would be a useful approach to

accomplish this objective. The BSC considers not only financial factors,

but also non-financial factors such as progress with customer relations,

improvements in operations, and improvements in capabilities of

19-51

Education.

Chapter 19 – Strategic Performance Measurement—Investment Centers

19-52

Education.

Chapter 19 – Strategic Performance Measurement—Investment Centers

19-43 Residual Income (RI); Performance Evaluation Time Horizon; Spreadsheet Application (60

Minutes)

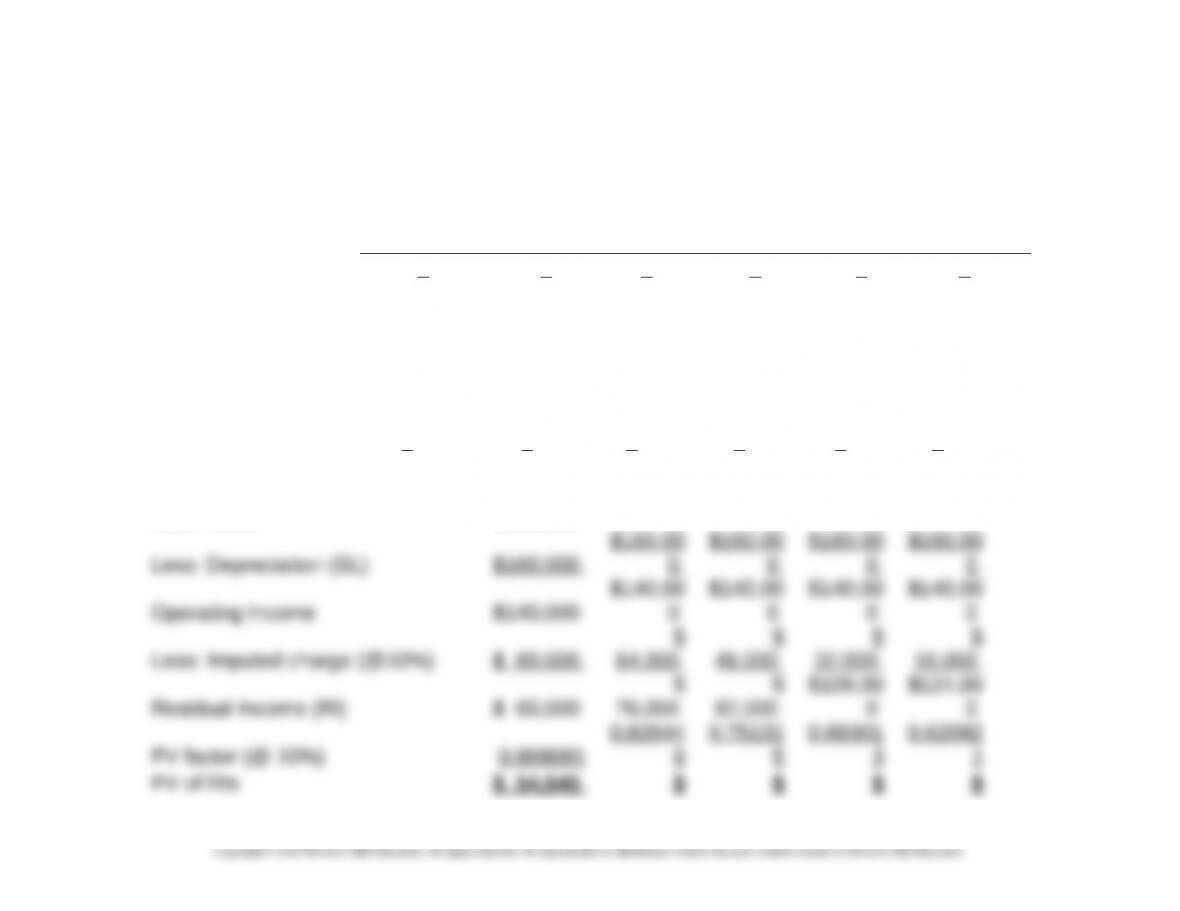

1. Estimated NPV of cash flows and estimated NPV of Residual Incomes (RI):

Time Period (Year)

0 1 2 3 4 5

Depreciation Expense =

$160,00

0 $160,000

$160,00

0 $160,000

$160,00

0

Beg.-of-Year NBV of asset =

$800,00

0 $640,000

$480,00

0 $320,000

$160,00

0

Time Period (Year)

0 1 2 3 4 5

Residual Incomes (RI):

Cash Inflow $300,000

$300,00

0

$300,00

0

$300,00

0

$300,00

0

$160,00

$160,00

$160,00

$160,00

19-53

Chapter 19 – Strategic Performance Measurement—Investment Centers

19-43 (Continued)

Time Period (Year)

2. The basic issue illustrated in the calculations presented above in (1) pertains to the incentive effects of

financial performance metrics, such as ROI and Residual Income (RI). We know from Chapter 12 that

long-term investment decisions are typically made on the basis of a discounted cash flow (DCF) basis.

On the other hand, it is more typical that subsequent financial analysis of investment projects is

conducted using accrual-based accounting data, e.g., ROI or Residual Income (RI). This divergence

presents an issue of “goal congruency” and therefore the possibility of suboptimal decisions from the

19-54

Chapter 19 – Strategic Performance Measurement—Investment Centers

budgeting decisions, then using multi-year RI to evaluate subsequent financial performance helps to

achieve goal congruency. (In this regard, see also Problem 19-37.)

Chapter 19 – Strategic Performance Measurement—Investment Centers

19-44 EVA® NOPAT and EVA® Capital; Operating Approach (60 Minutes)

Students should understand that EVA® is an approximation of an entity’s true (i.e., “economic”) profits

for a period. This measure of profitability is defined as the difference between the entity’s NOPAT (net

operating profit after tax) and an imputed capital charge. NOPAT is supposed to approximate the

entity’s actual cash yield generated for investors from recurring business activities during the period.

The amount of capital employed is supposed to represent the cash that investors have put at risk in

the firm, and upon which they expect an appropriate return. To estimate both NOPAT and the amount

of capital for a period, the analyst begins with reported financial statement amounts and then makes

adjustments. These adjustments, in the parlance of EVA®, are collectively referred to as “equity

equivalent adjustments.”

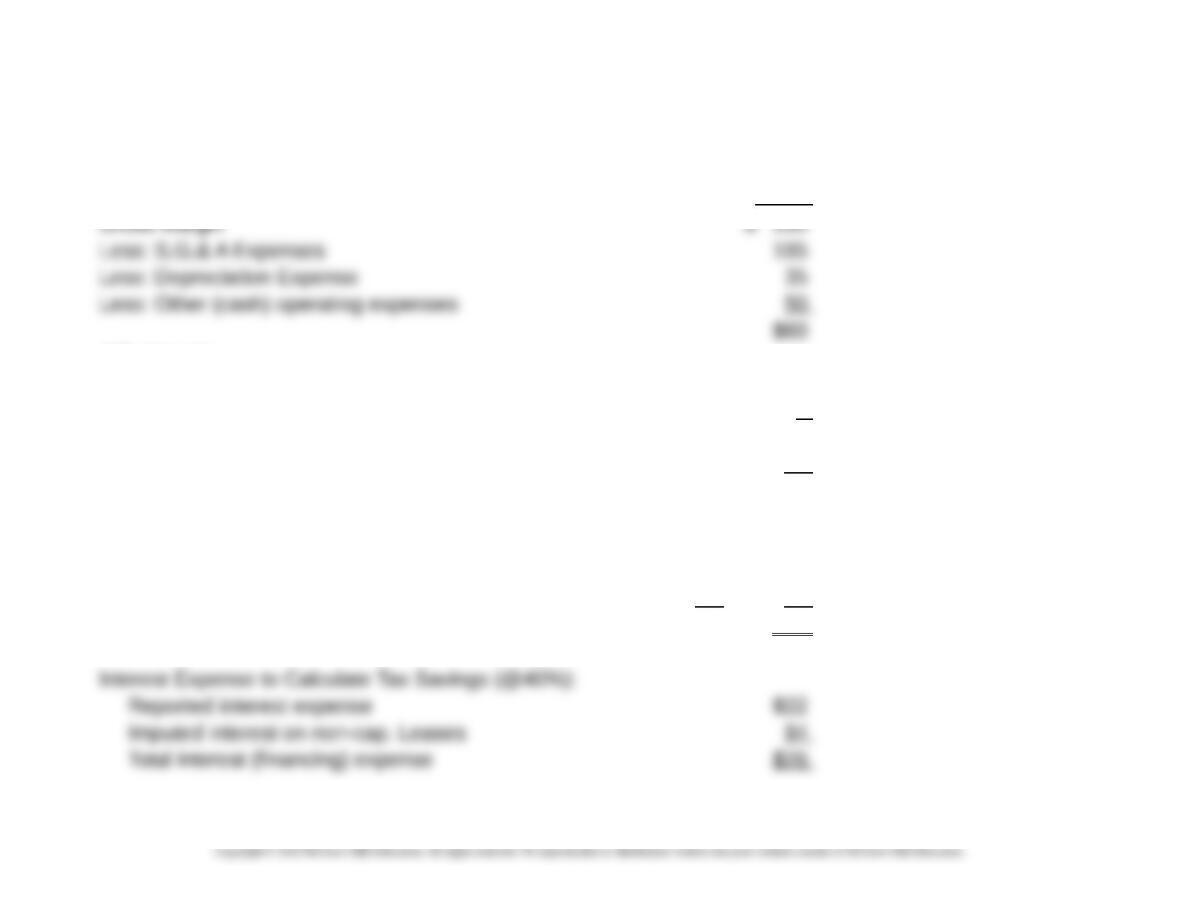

The Operating Approach to NOPAT estimation starts by deducting operating expenses—including

depreciation–from sales. Next, equity-equivalent (EE) reserve adjustments are made. Interest

expense, because it is a financing charge, is ignored, but other (operating) income is added to get

pretax economic profits, or Net Operating Profit Before Tax (NOPBT). Finally, an estimate of cash tax

expense on these operating profits is deducted, resulting in NOPAT. Under the Operating Approach,

EVA® capital is defined as the sum of net assets less non-interest-bearing current liabilities (NIBCLS).

1. EVA®NOPAT—Operating Approach (see next page):

19-56

Chapter 19 – Strategic Performance Measurement—Investment Centers

19-44 (Continued-1)

Net Sales $2,000

Less: CGS 1,670

Adjustments:

Increase in LIFO reserve (1) 2

Imputed Interest–Non-capitalized leases (2) 4

Net Operating Profit $66

Plus: Other Operating Income 12

NOPBT $78

Less: Cash taxes paid on net operating profit:

Reported Tax Expense $20

Less: Increase in Deferred Tax (3) 5

Plus: Tax Savings (foregone) on Interest (4) 10 25

NOPAT $53

19-57

Chapter 19 – Strategic Performance Measurement—Investment Centers

Rationale for EE Adjustments made:

(1)LIFO Reserve: brings into earnings the current-period effect of unrealized gain attributable to

holding inventory during period of rising prices

(2)Imputed Interest–Non-Capitalized Leases: Puts Operating and Capital Leases on equal footing in

terms of effects on EVA® NOPAT. In both cases, we want to remove the interest cost associated

with leases because this is a financing, not operating, expense.

19-44 (Continued-2)

2. EVA® Capital—Operating Approach:

Reported Current Assets (CA) $510

Plus: LIFO Reserve (1) 10

Adjusted CA $520

Less: NIBCLS:

Net Working Capital $150

Net Plant, Property, Equipment $605

19-58

Chapter 19 – Strategic Performance Measurement—Investment Centers

Rationale for Adjustments Made:

(1) LIFO Reserve: this adjustment converts the balance-sheet inventory amount from a LIFO to a

FIFO cost basis. In so doing, the resulting amount better approximates the current replacement

cost of inventories.

(2) PV of Non-capitalized leases: puts operating and capital leases on equal footing in terms of

determining the amount of “invested capital” in the business. (In essence, this adjustment

eliminates what some would consider an accounting “distortion.”)

Chapter 19 – Strategic Performance Measurement—Investment Centers

19-44 (Continued-3)

3. EVA® estimate—Operating Approach:

EVA® NOPAT = $53

Capital Charge:

The negative EVA® amount suggests that during the most recent period, the company did not earn

a sufficient amount of economic (cash) profit to fully compensate the suppliers of capital. That is,

during the most recent period, stockholder value was not created.

19-60