11-47 Profitability Analysis (45-50 min)

1. First, calculate the contribution margin per unit for traffic and commercial

paint.

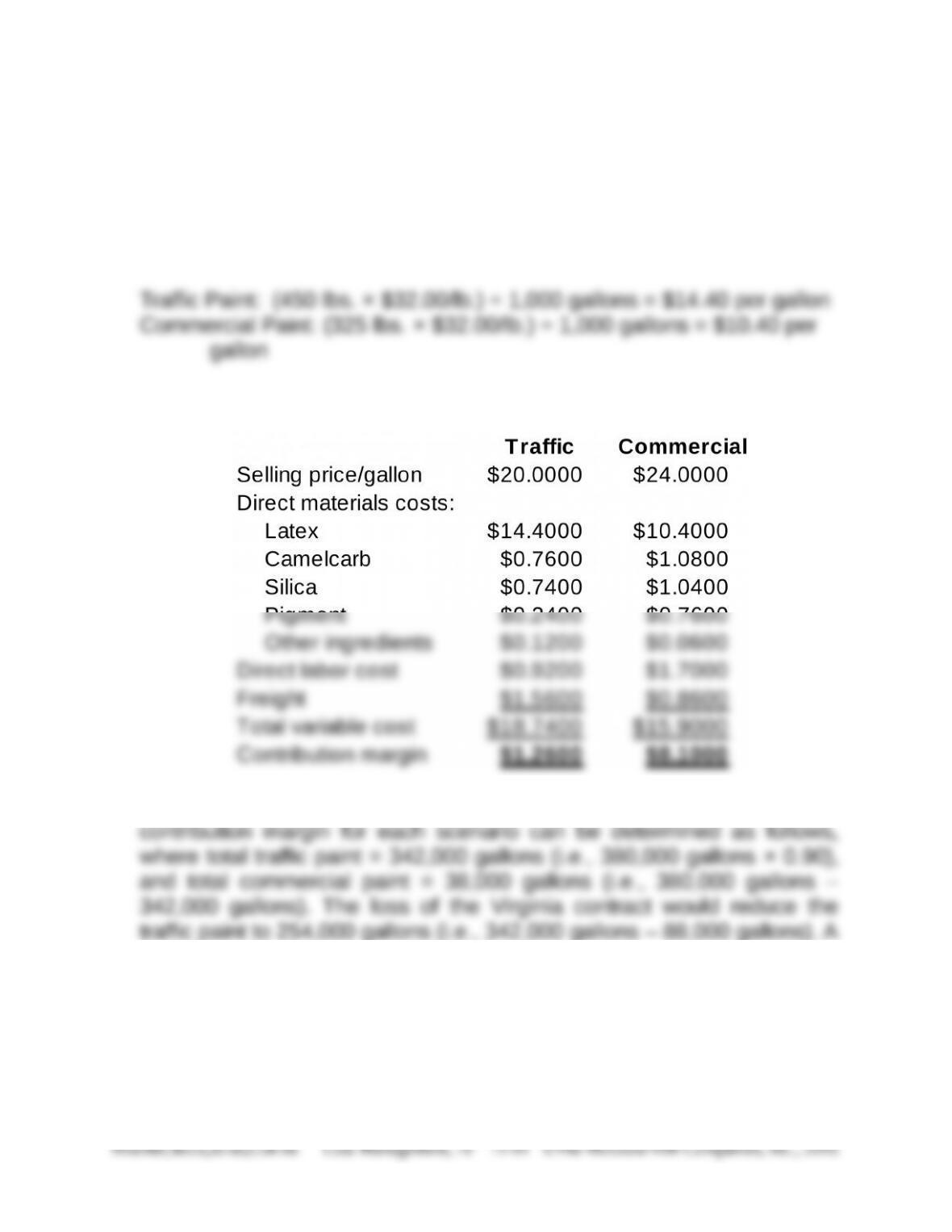

The first step is to determine the unit cost of latex, as follows:

The per-unit contribution margins are then determined as follows:

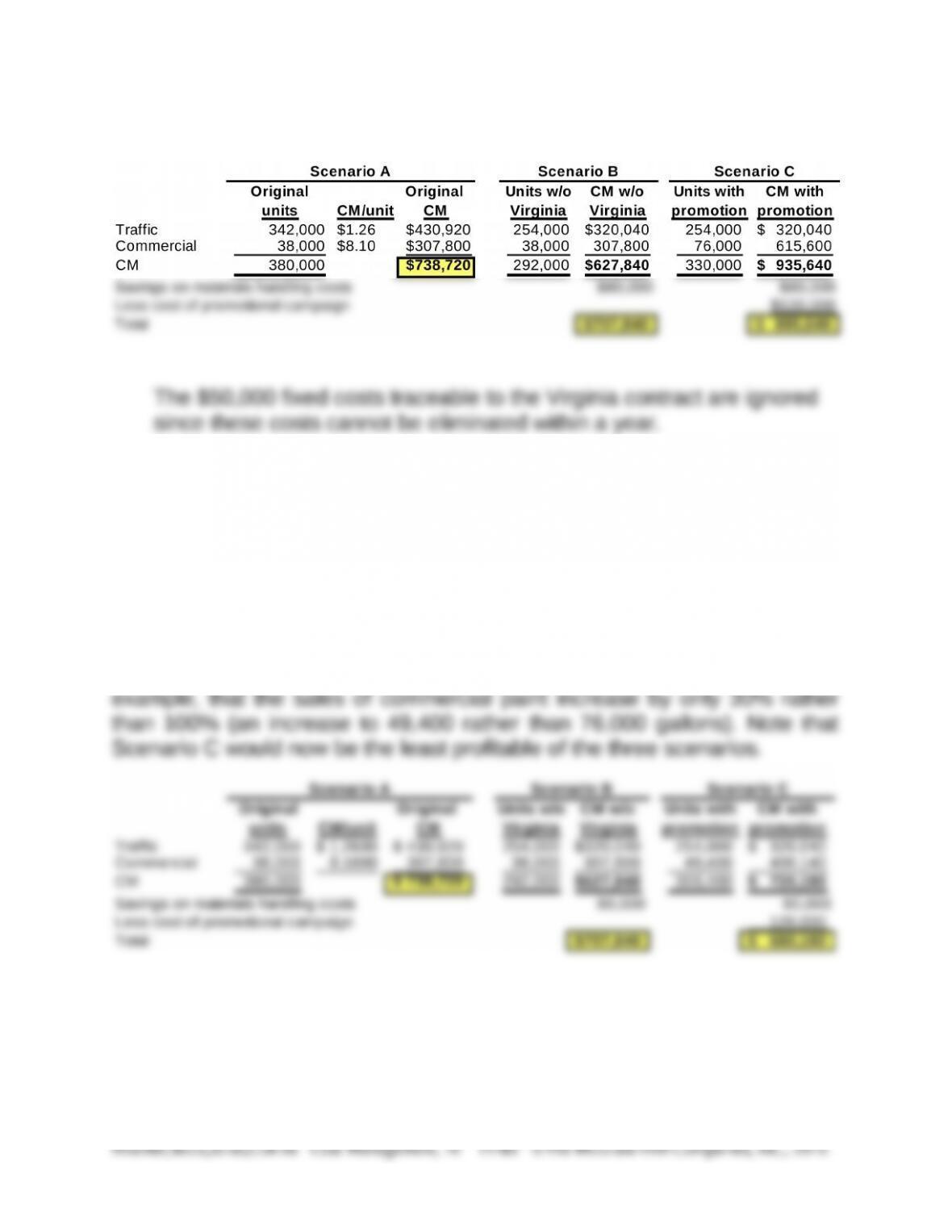

Using the above contribution margin per unit figures, the total

doubling of commercial paint (using the promotion) would result in

76,000 gallons (i.e., 38,000 gallons × 2).

Problem 11-47 (continued)

2. The proposed promotional campaign without the Virginia contract,

scenario C, has the greatest contribution margin, as shown in the

calculations above. Strategic issues for the decision between scenario B

and scenario C include the reliability of the projected sales-volume increase

in commercial paint and of the assumption that the volume of commercial

paint can be doubled without increasing fixed costs, other than the cost of

the promotion. A strategic opportunity, on the other hand, is that Meyer can

move from a relatively low contribution product line (traffic paint) to a

relatively high contribution product line (commercial paint). Suppose for

11-48 Constrained Optimization Analysis; Linear programming (50-60

min)

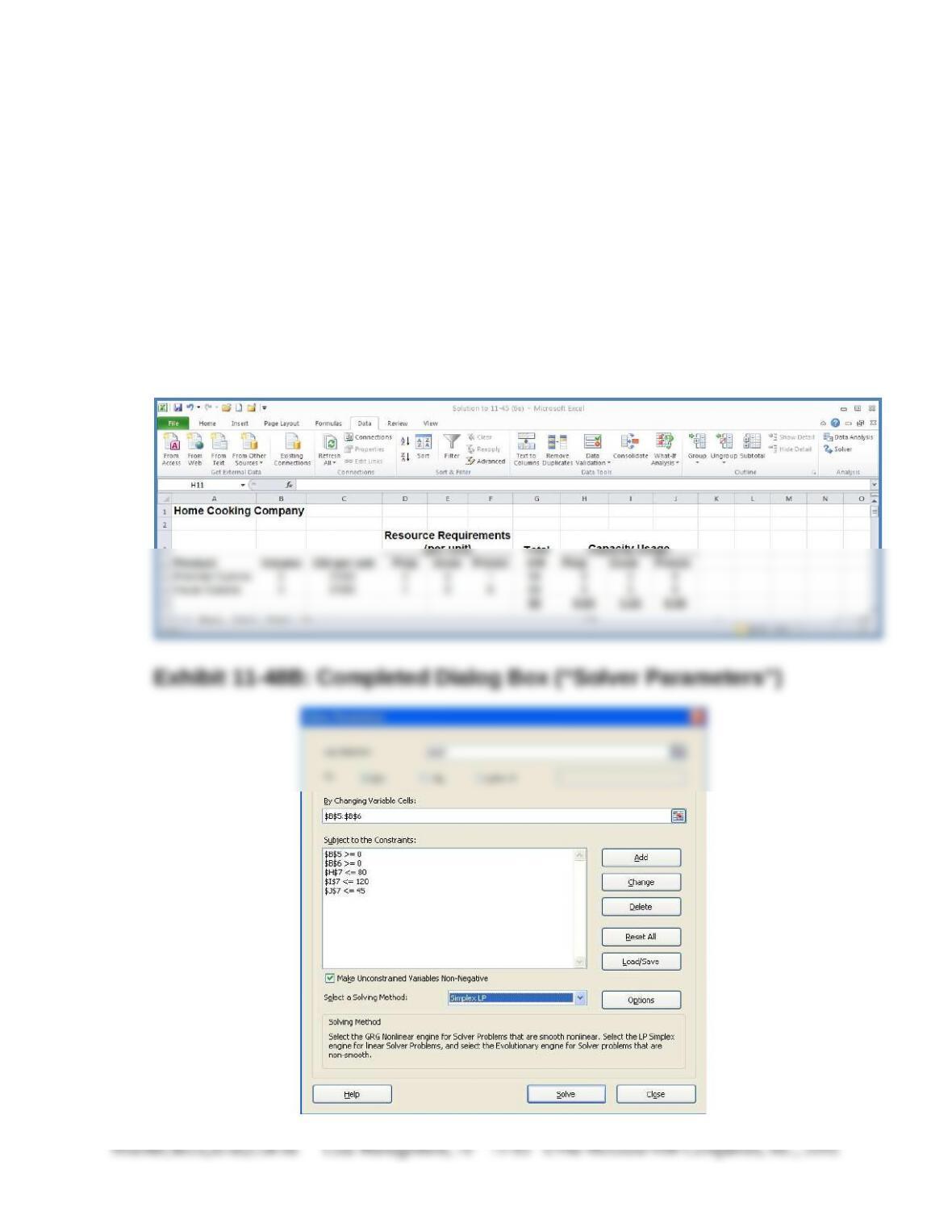

1. Solve for all three constraints: the solution is 17 units of Premier

Cuisine and 29 units of Haute Cuisine, as shown in Exhibit 11-48C,

cells B5 and B6. Total contribution margin for this mix is $5,429. The

Solver set up for this solution is shown in Exhibit 11-48A. The

completed dialog box (“Solver Parameters”) is presented in Exhibit 11-

48B.

Exhibit 11-48A: Solver Set Up

11-48 (Continued-1)

Exhibit 11-48C: Solver Solution (Optimum Product Mix)

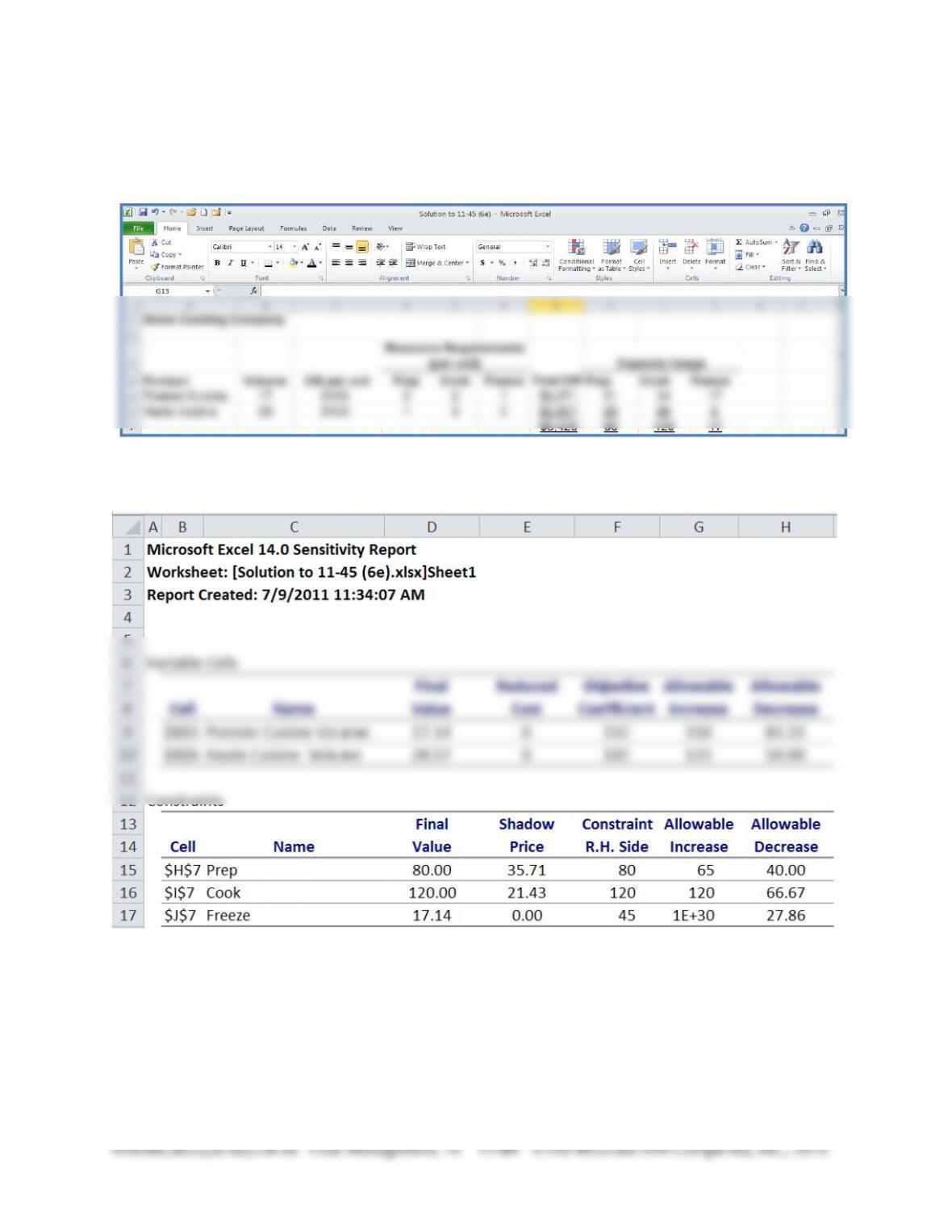

2. Sensitivity Report

Notes–Sensitivity Report:

1. Reduced costs: these pertain to the two decision variables (Premier

and Haute). If all such variables are in the optimum solution (as in the

present case), then these values will all be zero. Technically, the

11-48 (Continued-2)

“reduced cost” for a variable not in the optimum solution represents

the amount by which the per-unit contribution margin would have to

change in order for the variable to enter the optimal solution.

2. For each decision variable, the “Allowable Increase” and “Allowable

Decrease” provide a range over the objective function coefficients

3. For each constraint (Prep, Cook, and Freeze) the Final Value

represents the amount of the resource used under the optimum

solution. If you look at cell H7 and I7 you see that the entire

time allotment for Prep and Cook are used up under the

optimum solution. As such, each of these two constraints has a

4. Finally, for each constraint there is an “Allowable Increase” and an

“Allowable Decrease.” This information shows the range, around the

3. Optimal Solution after removing preparation time constraint: the optimal

solution, as showed in Exhibit 11-48D below, is to produce 45 units of

11-48 (Continued-3)

Exhibit 11-48D

Check Figures: Chapter 11

11-21 No check figure available.

11-26 1. If annual volume is at least 100,000 units, Vista should purchase and use

1 = 72.73%; 3. Required increase in sales from T-1 = 31.82%

11-28 1. 8,000 units of SilPol; 2. Operating income: for 0 units of SilPol, $2,000; for

11-29 1. Gross profit figures, per square yard: Commercial, $4.50; Residential, $7.75

11-30 a. Relevant cost to produce the product = $62.00 per unit; savings by producing

internally = $4,000; b. Difference in favor of the re-machining alternative =

per meal

11-31 1. One-year cost differential = $13,125; 2. Difference between paying the fine

11-32 1. Average cost per unit: prior to special order = $181.67; including special sales

11-33 1. Total relevant cost = $147,500; 2. Operating income would decrease by

per unit = $19.15

11-36 1. Number of fans manufactured = 15,000; number of fans purchased = 5,000;

11-37 1. Savings if parts are purchased = $48,975 (relevant cost to make = $21.8825

11-38 Non-discounted five-year cost advantage in favor of the Naftel contract =

11-39 1. To close the budget gap would require the following increases in sales

volume at budgeted cost, budgeted selling price, and budgeted resource usage.

11-40 1. Current level of fixed costs = $4,000,000; 2. Required sales volume = 64,000

units; 3. Pro-forma Operating Income = $2,280,000

11-41 2. Gross Profit per unit Figures: No Frills Model = $14; Standard Model = $24;

Standard Model = $15.00; Super Model = $15.50.

11-42 1. Lifetime cost function, regular model: Lifetime cost (Y) = $17,000 + (2,608.7

calculations (lifetime miles = 60,000): Hybrid = $27,360; Gas-Power Car =

$27,401

11-43 No check figure

11-44 2. First-year cost savings from closing the plant and outsourcing = $7,200,000

($7,200 in thousands)

11-45 2. Contribution margin per processing hour: Process #1 = $48.00; Process #2 =

across levels of variable overhead cost.

11-46 1. From a contribution income statement, contribution margins are as follows:

11-47 1. Per-unit contribution margins: Traffic Paint, $1.26; Commercial Paint, $8.10;

$738,720; Scenario B = $707,840; Scenario C = $680,180.

11-48 1. 17 units of Premier Cuisine and 29 units of Haute Cuisine (total Contribution

Margin = $5,429); 2. example interpretation: optimum solution holds as long as