Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

CHAPTER 5: ACTIVITY-BASED COSTING AND CUSTOMER

PROFITABILITY ANALYSIS

QUESTIONS

5-1 Undercosting a product may appear to have increased the reported profit the

product earned (assuming the firm did not lower its selling price because of the

reported lower product cost). However, the increased profit is, at best, a twist in

truth. Costs of the product not charged to the product itself are borne by other

products of the firm.

Worse, undercosting a product may result in managers erroneously believing the

5-2 Overcosting does not increase revenues. A firm can increase the selling price of a

product, thereby increasing the total revenue from the product only if the market

allows. Increases in the selling price of a product without experiencing noticeable

decrease in the sales quantity of the product is likely an indication that the product

was not priced properly, which might be a result of undercosting of the product.

Furthermore, overcosting a product is likely accompanied by undercosting of the

5-3 Product costs are likely distorted when a firm uses a volume-based rate if the plant

has more than one activity in its operations and not all activities consume overhead

5-4 Activity-based costing recognizes that resources are spent on activities and the cost

of a product or service is the sum of the costs of activities performed in

manufacturing the product or providing the service.

5-1

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

An activity-based costing system traces costs to the activity that consumes

resources. Costs are determined based on the activities performed for cost objects

5-5 Based on the activities of most manufacturing firms, the general levels of cost

hierarchy of an activity-based costing system are:

Unit-level cost;

5-6 In an activity-based costing system, the second-stage procedure in tracing costs to

products or services is a process by which the costs of activities or activity pools are

drivers.

5-7 All firms should use an ABC system when the benefits of such a system exceed the

5-8 Unit-level activities are activities performed on individual units of product or service.

The frequency of a unit-level activity varies in proportion with the units of product

5-9 Batch-level activities are activities performed for a group of units of products or

services rather than for each individual unit of product or service. The frequency of

batch-level activity is determined by both the size of the group and the total number

handling materials.

5-10 Product-level activities are activities undertaken to support individual products or

services rather than for each individual unit of product or service or a group of

individual units of products or services.

5-2

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-11 Facility-level activities are activities performed for the entire organization or division

to meet the required operating procedure or support the operation of the

5-12 A product-costing system that uses a single volume-based cost driver is likely to

overcost high-volume products because high-volume products do not consume

support resources in proportion to their production volumes. As a result, a product-

costing system that uses a single volume-based cost driver often overcosts high-

sufficient resources on more profitable items.

5-13 Activity-based management is the use of an activity-based costing system to

5.14 Service organizations such as banks, hospitals, transportation companies, law firms,

and trading companies can use activity-based costing and management in all

phases of their operations as manufacturing firms do. For example, a bank can use

5.15 Opportunities afforded by performing customer profitability analysis are:

Providing better services to highly profitable customers;

Identifying and securing highly profitable customers from competitors;

Setting prices based on the cost to serve;

5-3

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

BRIEF EXERCISES

5-16 Total Cost per Batch = $50 + ($0.10× 5,000)= $550

= $11,000

5-17 ((30,000 × 0.2) ÷ 60) × $10= $1,000

5-18 Cost for 50 Heads = (50 ÷ 20; rounded up to 3 packages) ×$5 + (50 × $0.10)

= $20

5-19 (($15×.5) + $5) × 5 cars × 5 days = $312.50 per week

5-20 Cost per computer = $1,000,000 ÷ 5,000 = $200 per computer

$200 = (2 × (cost of one technician hour)) + (5 × $10)

5-21

Direct Labor = $8 × 5 = $40

5-22 Data Analysis= $3,000,000 ÷ 30,000 = $100 per hour

5-23

6 pounds × 10,000 units× $.50 per unit = $30,000

5-4

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

EXERCISES

5-24 Role of Activity Based Costing in Implementing Strategy (20 min)

To assess the strategic issues facing Laurent and the strategic role of ABC for

Laurent, we first look at its strategy, and in particular its marketing and

manufacturing strategies.

What is Laurent’s Competitive Strategy?

Laurent has built its business on differentiation, in the large grocery

chain market. The labor-saving bagging they developed differentiated them

and gave them a competitive advantage. As other manufacturers are catching

up in this segment, Laurent is moving to the wholesale segment of the market,

also with a differentiation strategybased on product variety. The wholesale

segment is expected to require higher product variety and smaller lot sizes.

with the firm’s overall strategy.

What are the implications of the marketing initiatives undertaken by Laurent?

The new marketing focus, involving increased product variety (and

smaller customer order sizes), is not well supported by the manufacturing

ABC has an important role to play for Laurent. Because of the increased

product variety as a result of the new marketing initiative, the firm will need

accurate cost information for pricing and for product and customer profitability

analysis. A looming question, will the company be able to meet the demands

of the new customers profitably? Will the company be able to increase price

to cover the cost of adding the additional complexity (smaller batches, more

colors,..)?

5-5

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-25 Activity Levels and Cost Drivers (5 min)

1. Activity Levels

a. Unit-level f. Facility-level

b. Batch-level g. Product-level

c. Batch-level h. Product-level

d. Batch-level i. Unit-level; Batch-level

e. Product-level j. Batch-level.

2. Cost Drivers

a. Machine hours

b. Number of setups or setup hours

c. Number of production orders

d. Number of material receipts; Number of purchase orders

e. Number of products

f. Number of machine hours

g. Number of engineering change notices; number of modifications;

Number of products

h. Number of parts; Number of products; Number of purchase orders

i. Number of inspection hours; Number of units; Number of batches

j. Number of loads; Number of material moves; Material weights

5-6

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-26 Activity Levels (5 min)

1. Cost Hierarchy

a. Unit-level f. Product-level

b. Unit-level g. Facility-level

c. Facility-level h. Facility-level

d. Unit-level i. Batch-level

e. Unit-level j. Batch-level (one bag per customer).

2. Cost Driver

a. Number of hamburgers

b. Number of hours

c. Square feet

d. Number of hamburgers; Size of hamburgers

e. Number of hamburgers

f. Number of time the advertising is run

g. Number of hours store is open

h. Square feet

i. Number of coupons redeemed

j. Number of customers

5-7

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

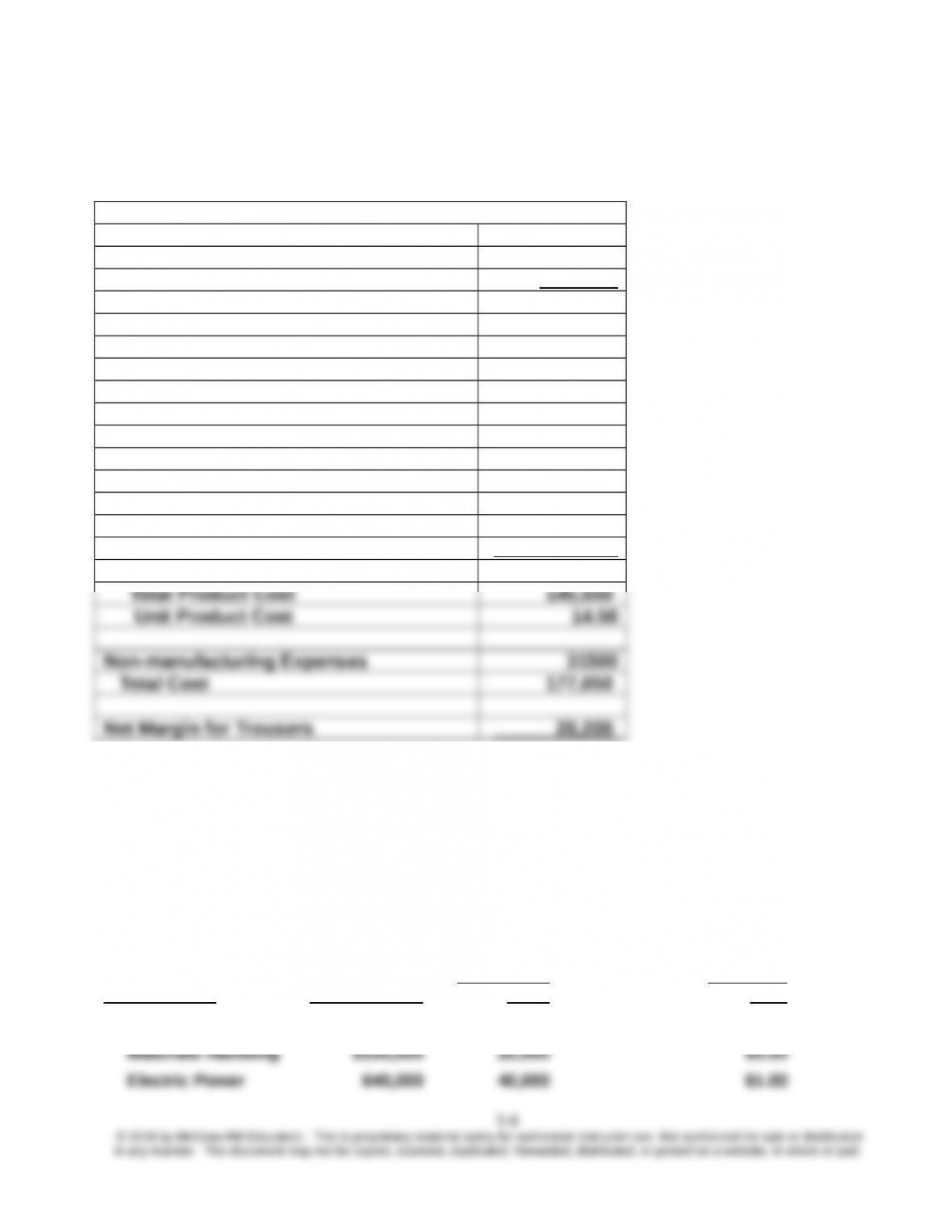

5-27 Activity-Based Costing in the Fashion Apparel Industry (20 min)

The ABC-costing solution follows:

The ABC-costing solution follows:

(all figures in £)

Units 10,000

Price × 20.525

Total Revenue 205,250

Direct Materials 33,750

Labour and Overhead Costs

Pattern cutting 22,000

Grading 19,000

Lay planning 18,500

Sewing 21,000

Finishing 14,300

Inspection 6,500

Boxing up 3,500

Storage 7,000

Labour and Overhead (ABC-based) 111,800

The results suggest that the trouser line is more profitable than previously

thought (using volume-based costing). This is likely due to the common

situation in which the high-volume products are overcosted using volume-

based costing.

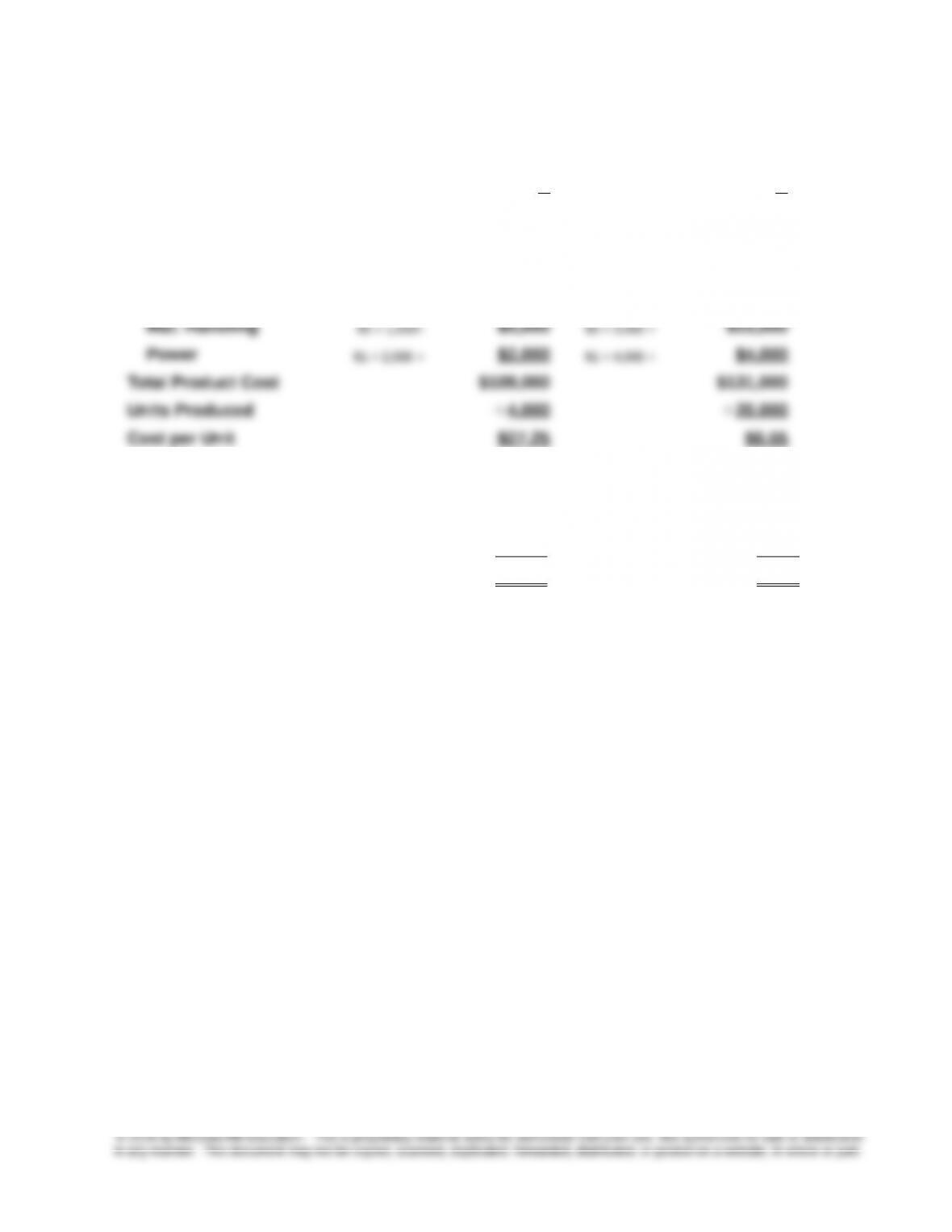

5-28 Activity-Based Costing (25 min)

Cost Pools Activity Costs

Cost Driver

Units

Overhead

Rate

Machine Setup $360,000 4,000 $90.00

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

Cost Assignment:

A B

DM $42,000 $54,000

DL $24,000 $40,000

Overhead:

Machine Setup $90 × 400 = $36,000 $90 × 200 = $18,000

DM per unit $10.50 $2.70

DL per unit $6.00 $2.00

OH per unit $10.75 $1.85

Cost per Unit $27.25 $6.55

2. While one could safely assume that the ABC system provides an improved

assignment of the overhead costs to the two products, the term “accuracy”

tends to be regarded as a measure of how close the numbers are to some

accepted target, but the target value is not known. It must be remembered

that allocations are needed because direct assignment of cost to products is

not possible and that all allocations are dependent upon subjective

management decisions. The new costs reflect the decisions made with regard

to the number of cost pools, the actual assignment of costs to those cost

pools, and the selection of the cost drivers for each cost pool. If, for example,

5-9

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-28 (continued)

number of setups rather than number of setup hours was used to assign

overhead from the machine setup pool, the cost of each product may have

been different, thereby making it difficult to say that any ABC system is entirely

accurate. The resulting values can only be evaluated with respect to those

generated under some other system.

5-29 ABC and Job-Costing; Working with Unknowns (15 min)

A. $6.00 = $0.20 × 30

B. 18.50 = $37.00÷ $2

5-30 High-value-added and Low-value-added Activities—Nurse (5 min)

(Note to instructor: Answer may vary if students perceive a different

operation)

a. High-value-added f. High-value-added

b. High-value-added g. High-value-added

c. High-value-added h. Low-value-added

5-10