Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

The following questions were not part of the requirements in the case competition. The questions

could serve as the basis for the final question in the live presentations at the Annual Meeting. Also,

the suggested solutions might give you ideas as to what represents a more in-depth or insightful

analysis of the case, which may help judges evaluate the teams.

Additional possible questions

Question 2 could be revised to give a more directed focus by changing the wording as follows:

“Management of Customer Paint Shop used ABC to obtain a better understanding the “true” cost of the

products. Management is now working toward a more proactive approach to capacity utilization, and

TOC costing has been suggested and some additional cost analysis was done. Discuss the potential

strategic value of the ABC versus TOC cost information in making decisions about the use of existing

capacity.” This wording offers the opportunity to spend time focusing on ABC and TOC would allow the

instructor to avoid or delay dealing with RCA if desired.

Possible solution: TOC promotes focusing on the contribution margin per unit of scare

resource, but this approach to managing a scarce resource would be a short-term approach to developing a

Also, TOC is not a panacea. For example, TOC looks at the constrained resource while a technique like

JIT looks to improve all processes, not just the process related to the constrained resource. The JIT

approach allows for a deeper understanding of all processes and their interrelationships that may not be

gained from a strict TOC approach. Thus potentials for uncovering opportunities may also be missed

from a strict TOC approach. Also, TOC takes only a short-term view of capacity utilization, whereas a

process like activity-based costing takes a longer-term perspective.

Other possible questions:

The case states the change to ABC “was made to better understand the costs associated with

painting the various products.” How effective is ABC in supporting such an objective as compared to

TOC and RCA. This question changes the context of the comparison to highlight that different tools

might be preferred for different purposes and reinforce the need to understand more than one costing

concept in order to be able to decide when a tool might be most effective.

The instructor could ask the students to identify the characteristics that make an organization’s

processes a candidate for the use of RCA and comment on whether PPS meets each of those

characteristics.

Possible solution: Grasso (2005, p.16)

The approach assigns resource elements to resource centers using the following criteria

1. The center must have an identifiable, measurable output and identifiable, separable costs specific

The paint booths along the conveyor line display these characteristics, making PPS a candidate for RCA.

References

Grasso, LawrenceP., 2005, Are ABC and RCA Accounting Systems Compatible with Lean Management?,

Management Accounting Quarterly, Fall, 2005, Vol. 7, No. 1, pp.12-27

Johnson, H. Thomas, Relevance Regained: From Top-down Control to Bottom-up Empowerment, Free

Press, New York, NY, 1992, p.139.

5-21

Education.

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

Keys, D. E., and A. Van der Merwe. (2002). Gaining Effective Organizational Control with RCA.

Strategic Finance. May 2002, pp. 41-47.

Keys, D. E., and A. Van der Merwe. (1999). German vs. United States Cost Management. Management

Accounting Quarterly. Fall 1999, pp. 19-26.

5-22

Education.

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-4 Forest Hill Paper Company

1. What is the competitive environment facing FHPC? What is and/or should be FHPC’s

competitive strategy?

Questions to generate discussion:

1. What is the competitive strategy of the company? What should it be? (Of the industry?)

2. How would you change the competitive strategy of the company? What is the role of cost

information in determining the strategy of the company?

GO TO QUESTION 2 and come back to this…..

Reduce product variety

Batch size

Slitting, or charge appropriately for it

Reduce the number of grades

The industry

Paper products, generally a commodity cost leadership

“Capital intensive, mature industry” cost leadership

overhead is 105% of materials cost

Very cyclical; down in the 1980s and early 1990s, at present demand exceeds supply

Effect on customer order pattern; exaggerates swings in demand

Importance of the cost/management of unused capacity

Firms in the industry do not readily increase capacity

FHPC market share down from 35 to 25%

Customers move to plastic and environmentally sound products (where is FHPC

In these products??) cost leadership

Paperboard manufacturing is a continuous process; hard to trace costs to individual

units of output; also this points up speed (cycle time) as a key cost driver

Producers cannot control prices; “selling price reflect spot market prices,”

cost leadership

The company

Focus on full range of products – 19 different grades of paperboard; also

widths (slitting) and coatings.

Focus on offering special services (slitting) differentiation???

Wide range of batch sizes

5-23

Education.

2. Describe FHPC’s current costing system, and explain the type of costing system you would

recommend for FHPC and why. For products A, B, C and D shown in the case, what are product

costs using the current and your recommended costs system?

Overall cost problem: We have 4 batches, one each of products A,B,C and D; there are several

reels of product in each batch. What is the cost per reel, cost per batch and total production cost?

Gross margin per batch?

Note, you cannot focus your costing on reels only, because you would miss the importance of batch

level costs (grade change and slitting) and the influence of these batch related costs on total costs.

Good starting questions:

1. What are the cost drivers in this case

2. Just looking at Exhibits 1 and 2, which products do you think will be over costed with the current

costing system and why?

Product B has so few reels, so batch costs of grade change will strongly effect it

Product D has a large number of reels per batch, and no slitting, it is over costed.

3. How would you describe the current cost system

4. Show the current cost per reel and per batch of the current cost system

5. What are the activities in the ABC system

6. Show the costs under the ABC system

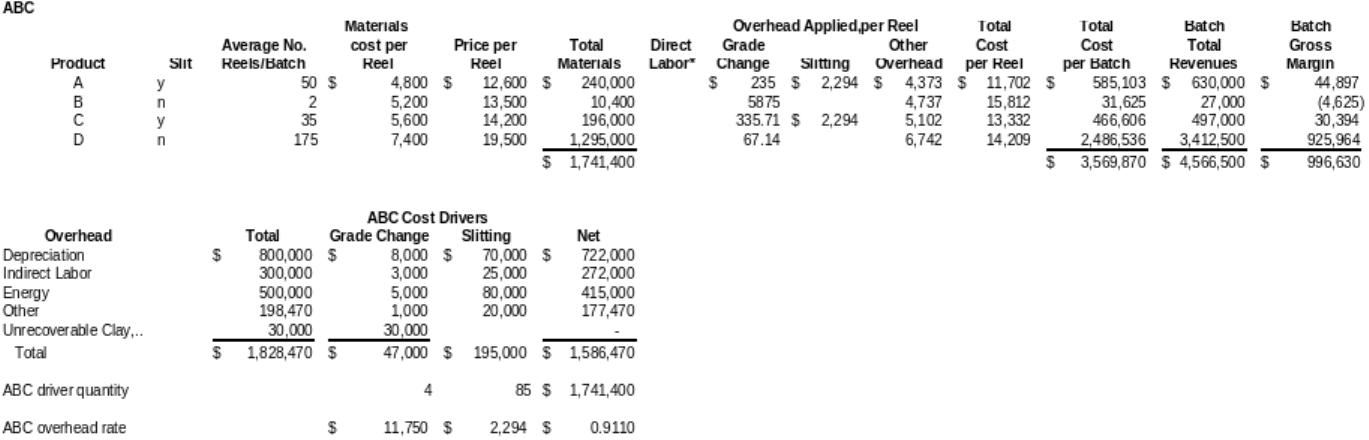

Cost Drivers

Volume: how do we measure it??? The firm uses tons of materials in costing, feet in

pricing

Tons of materials, or

Linear feet of paperboard produced

Grade; a combination of both:

Slitting

Not included in the case….

Cycle time (because it is a continuous process industry and there is now excess demand)

Quality of raw materials

Effectiveness of scheduling so as to reduce the cost impact of grade changes

Current Cost System

Slitting cost is shared among all grades of paperboard; customers are charged a small

amount for slitting (presumably not enough to recover the cost of slitting)

Volume based drivers are used – materials cost, with the idea that thicker material takes

longer to process (slower machine rate) and longer to dry

overhead rate = 105% x materials cost

Note however (not in case) that while tons of materials produced drives costs, the

industry practice is to set price by linear foot

5-24

Education.

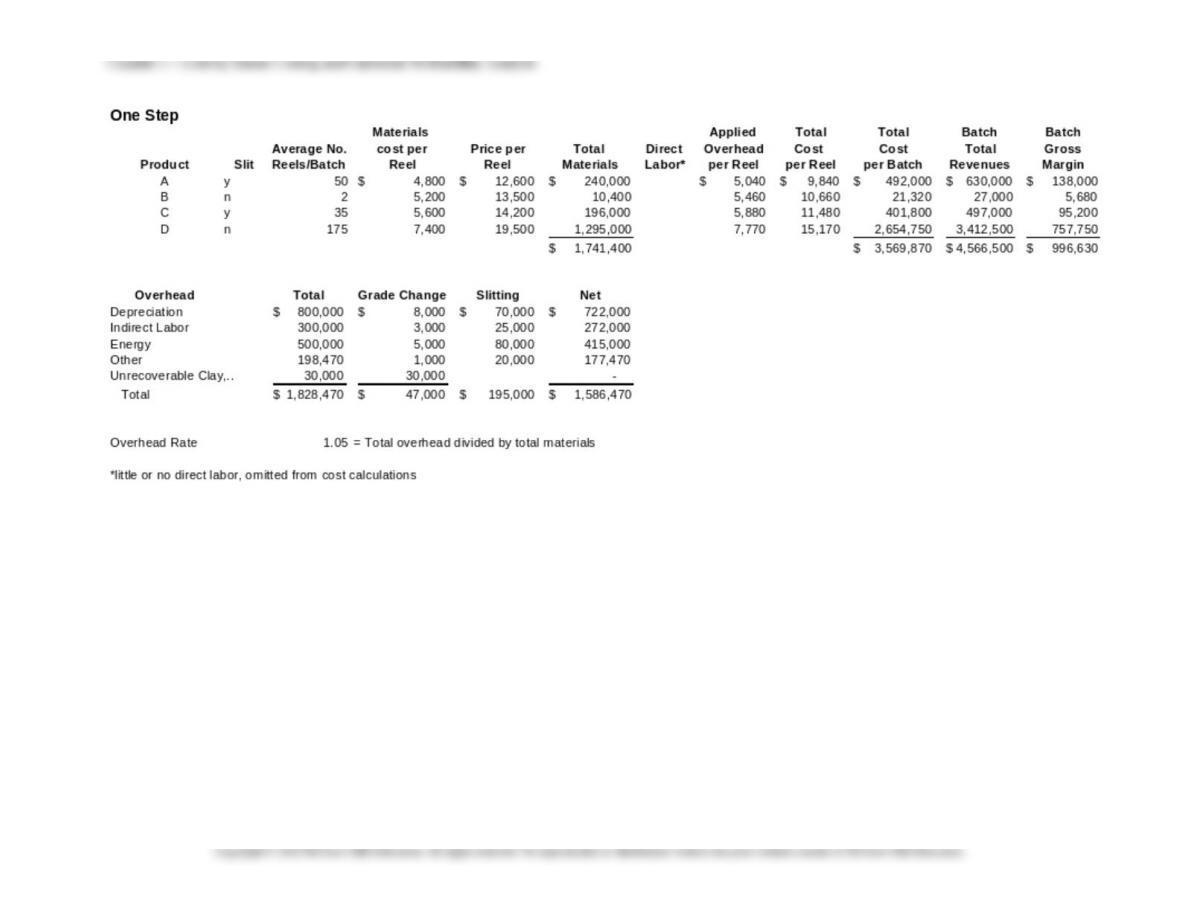

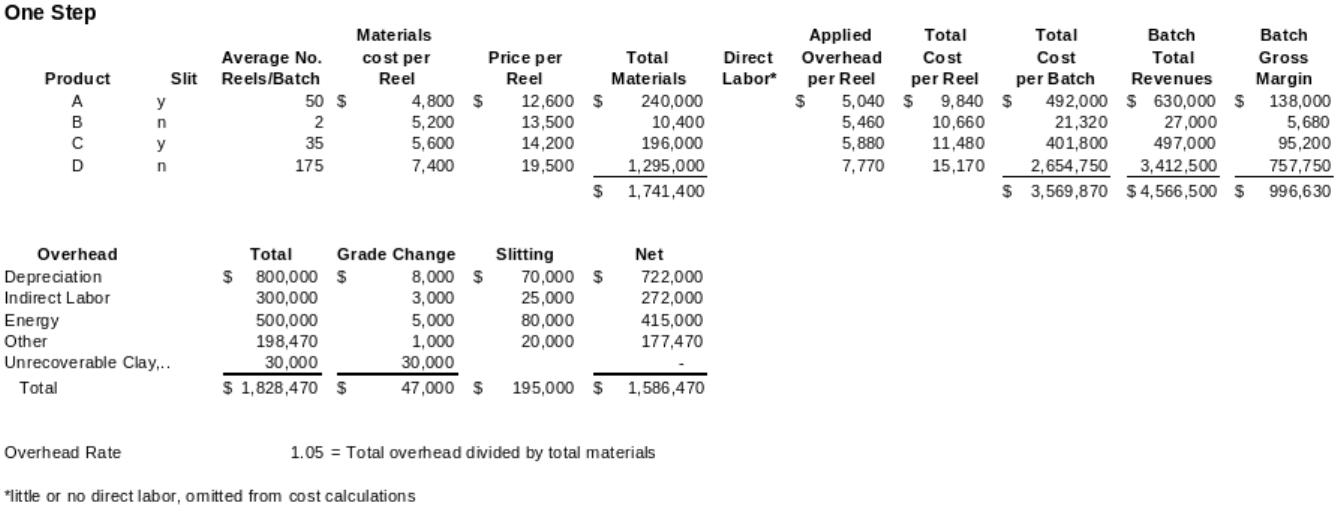

Calculating the FHPC Overhead Rate (One Step)

First, total materials cost

• Product A 50 x $4,800 = $240,000

• Product B 2 x $5,200 = 10,400

• Product C 35 x $5,600 = 196,000

• Product D 175 x $7,400 = 1,295,000

Total $1,741,400

Second, the overhead rate

Total Overhead Costs $ 1,828,470

Total Materials Costs $ 1,741,400

= $1.05 per dollar of materials cost

(or 105% of materials cost)

Third, Overhead Cost for Product A per reel:

$4,800 x 1.05 = $5,040

Total Cost for Product A per reel

$4,800 + $5,040 = $9,840

One Step Cost per Batch = 50 x $9,840 = $ 492,000

5-25

Education.

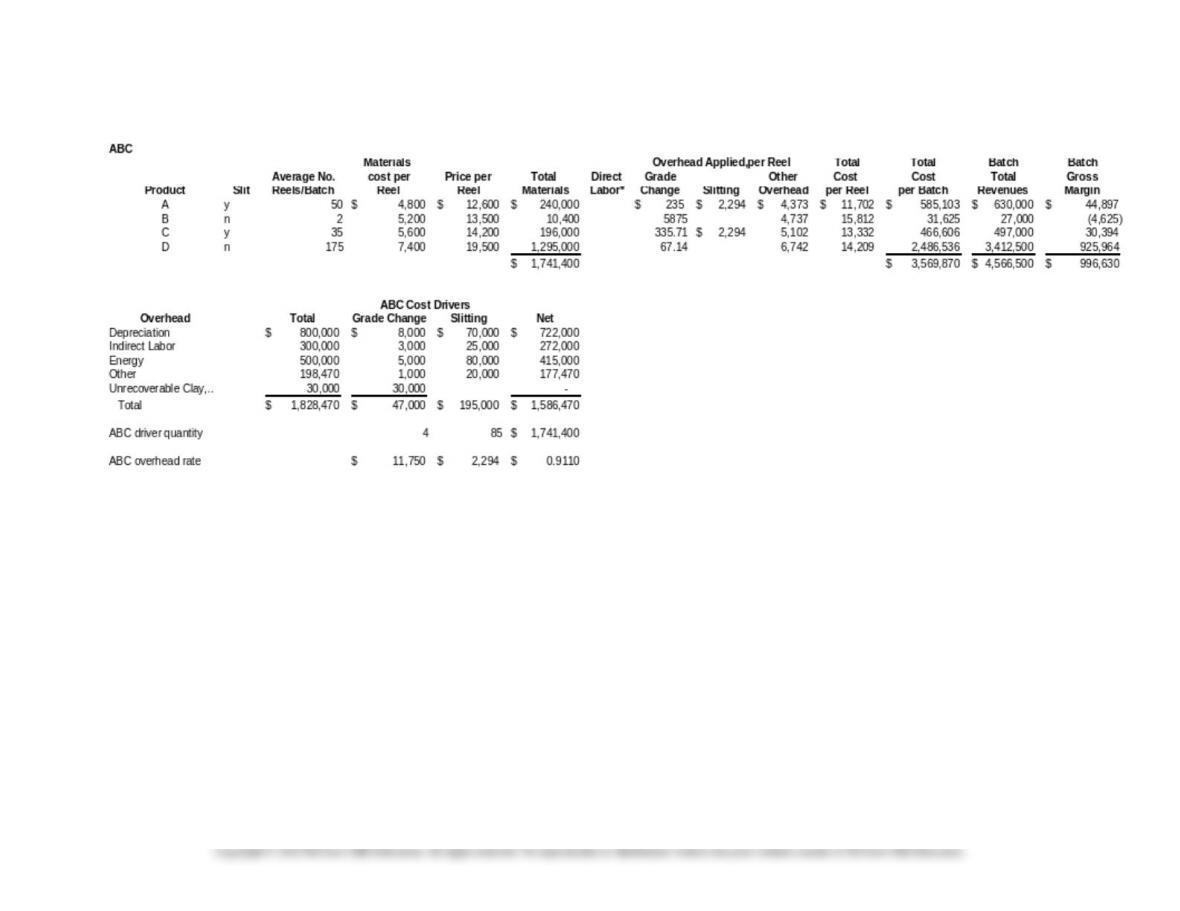

ABC Costing – Product A

First, Overhead rate for Other Overhead:

Total Other Overhead Costs $1,586,470

Total Materials Costs 1,741,400

= .911 per $ of direct material

Second, Overhead for the Two Activities, per reel

• Slitting $2,294

• Grade Change $11,750/50 235

Third, Total Cost for Product A per reel

• Materials $4,800

• Overhead

• Other OH $4,800 x .911= 4,373

• Slitting 2,294

• Grade Change $11,750/50 235

• Total Overhead 6,902

Total $11,702

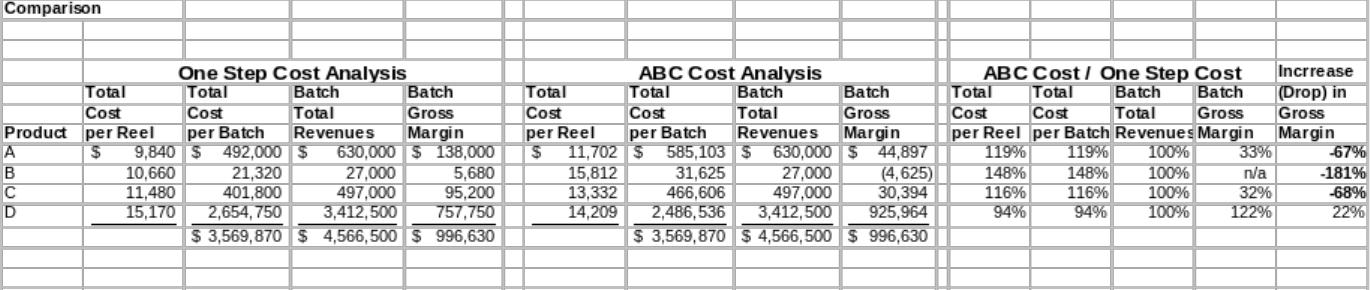

Compare to One Step solution of $9,840

Also,

ABC cost per batch = $11,702 x 50 = $585,100

ABC Cost per Batch of Product A, figured directly

Materials $4,800 x 50 $240,000

Overhead

Other $240,000 x .911 218,640

Grade Change 11,750

Slitting $2,294 x 50 114,700

Total Cost per batch $585,090

(small difference due to rounding)

5-26

Education.

5-27

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-28

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-29

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

Key points from ABC Analysis

1. Products A,B, and C are more costly than thought, because of the high cost of grade change (has to

be averaged over the number of reels, smaller for A,B, and C) and the high cost of slitting (for A and

C). Note that the grade changes are made between batches, while slitting is done for each reel,

so the effect of the slitting is potentially much greater than the effect of grade change. This does not

2. Gross margins after ABC are much smaller for A, B and C, and B’s gross margin is negative. Need

to consider the pricing issues for B and whether we can make this product more profitable.

3. How should we use the ABC information in pricing, in planning, and in performance evaluation?

Increase the price of B

ABC information is better for planning which products to drop, keep or add

ABC information is better for performance evaluation

4 How would you change the competitive strategy of the company? What is the role of cost

information in determining the strategy of the company?

Reduce product variety

Batch size

Slitting, or charge appropriately for it

5. How would analysis of the value chain help FHPC meet its strategic goals?

Look for ways to add value and reduce costs

Are shipping costs high; how to reduce them?

5-30

Education.