Chapter 16 – Operational Performance Measurement: Further Analysis of Productivity and Sales

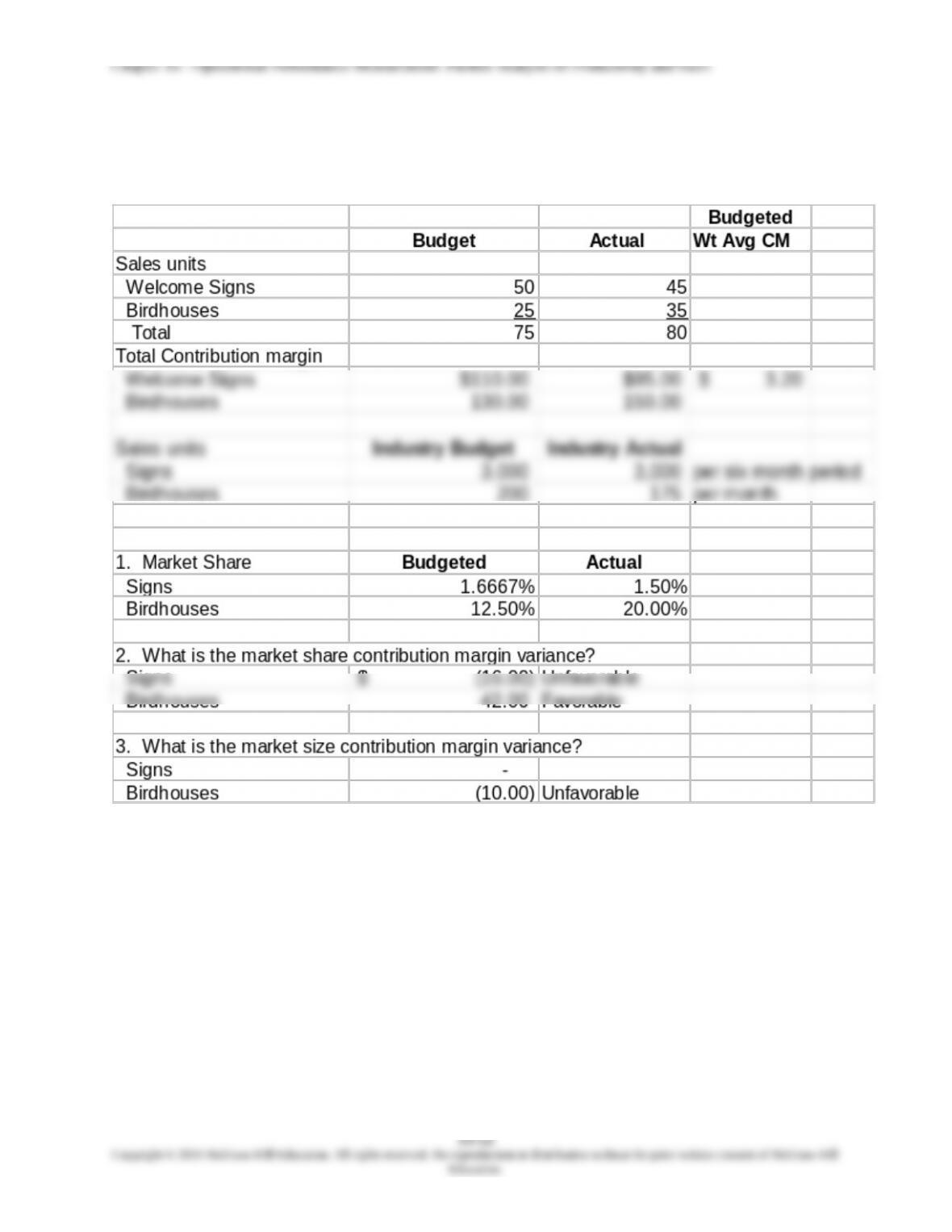

16-54 Market Size and Market Share Variances (15 min)

WS= Welcome Signs; BH= Birdhouses

1. Budget Actual (per month)____

Diane’s Designs Industry Share Diane’s Designs Industry Share

2. Weighted Average Budgeted Contribution Margin Per Unit:

Budgeted contribution margin per unit for both products:

Market Share Variance

3. Market size variance

4. Diane’s market share for Welcome Signs decreased while she did

very well for Birdhouses. The total market for Birdhouses decreased.

16-51

Education.

16.54 (continued -1)

The spreadsheet solution for 16-54 is shown below

Chapter 16 – Operational Performance Measurement: Further Analysis of Productivity and Sales

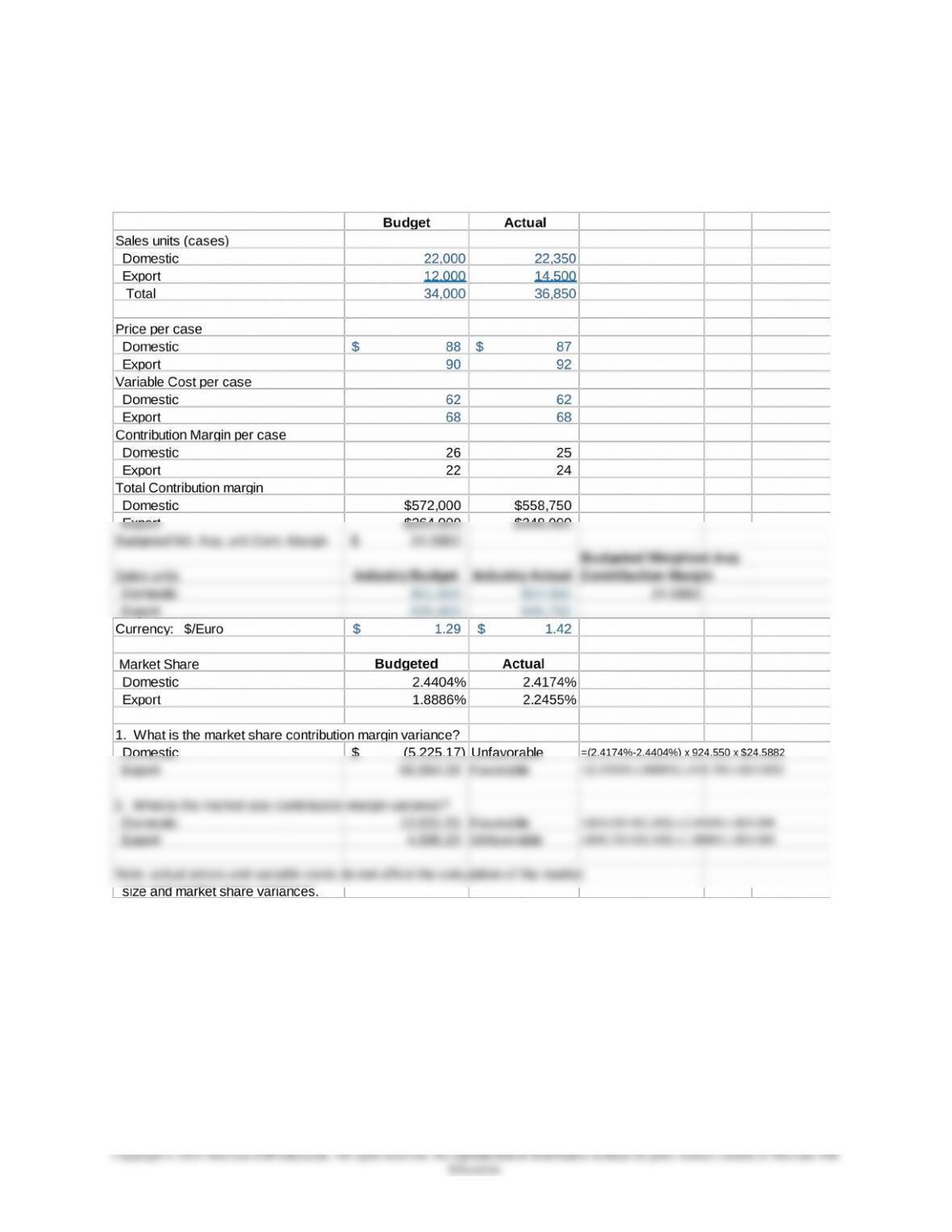

16-55 Market Size and Market Share Variances; Foreign Currency

Fluctuations (20 min)

1.,2.

16-53

Chapter 16 – Operational Performance Measurement: Further Analysis of Productivity and Sales

16-55 (continued -1)

3.

The unfavorable market share for the domestic market reflects the decline in

the company’s sales as the market increased; the unfavorable domestic

The large increase is due to the lower cost of the beer to Euro consumers,

plus an additional increase due perhaps to the Euro consumer becoming more

familiar with the Tall Pines brand. This is good news for TPB, as it could

mean that, when the dollar should rise again relative to the Euro, it may be

able to retain some of its new foreign customers.

16-54

Education.

Chapter 16 – Operational Performance Measurement: Further Analysis of Productivity and Sales

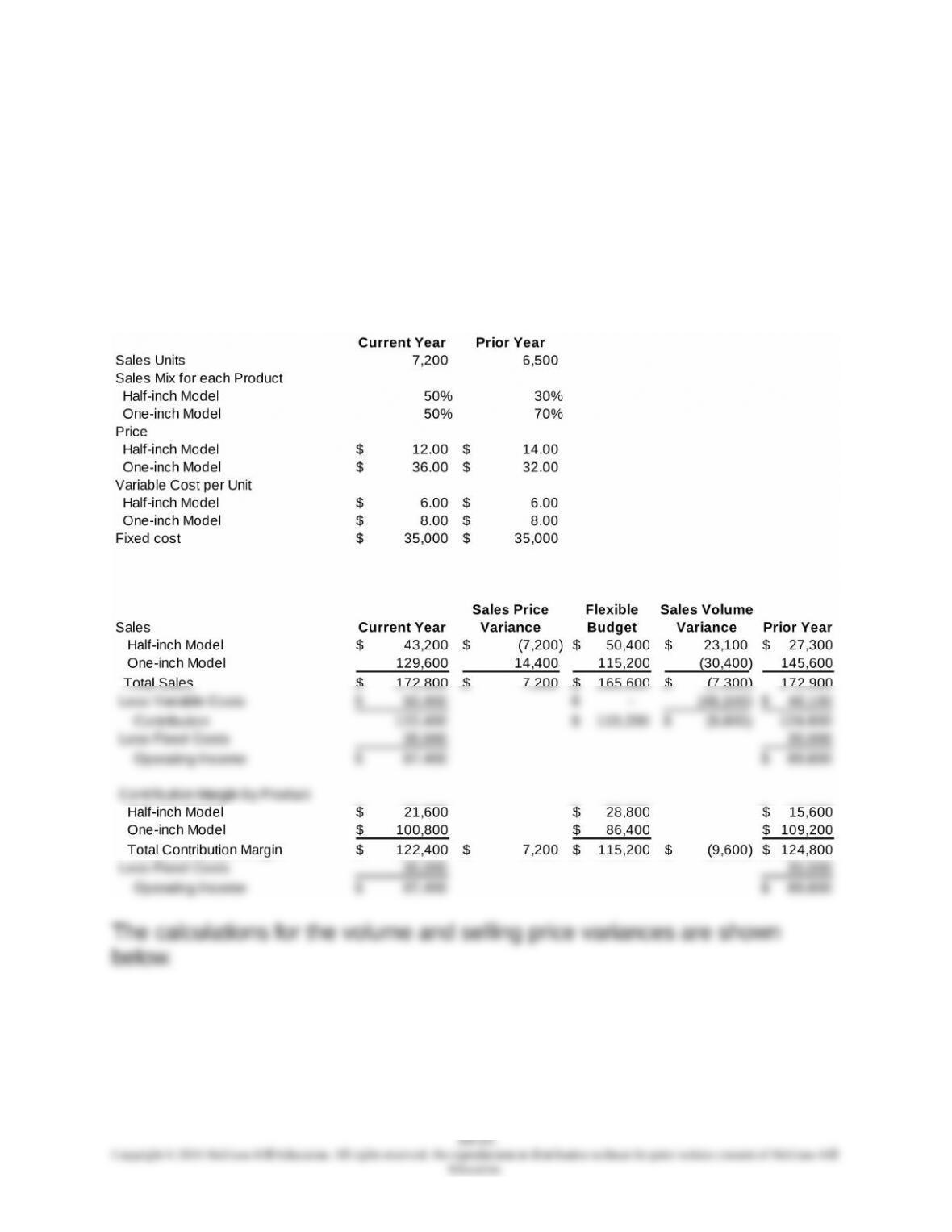

16-56 Comparative Income Statements and Sales Performance

Variances; Current to Prior Year (35 min)

1. Comparative Income Statement for two years based on the flexible

budget (Exhibit 16.15)

Chapter 16 – Operational Performance Measurement: Further Analysis of Productivity and Sales

16-56 (continued -1)

The volume variances for each product:

Half Inch: $13,200 (F) = [(.3 x 6,500) – (.5 x 7,200)] x ($14-$6)

One Inch: $22,800 (U) = [(.7 x 6,500) – (.5 x 7,200)] x ($32-$8)

The selling price variances are as follows:

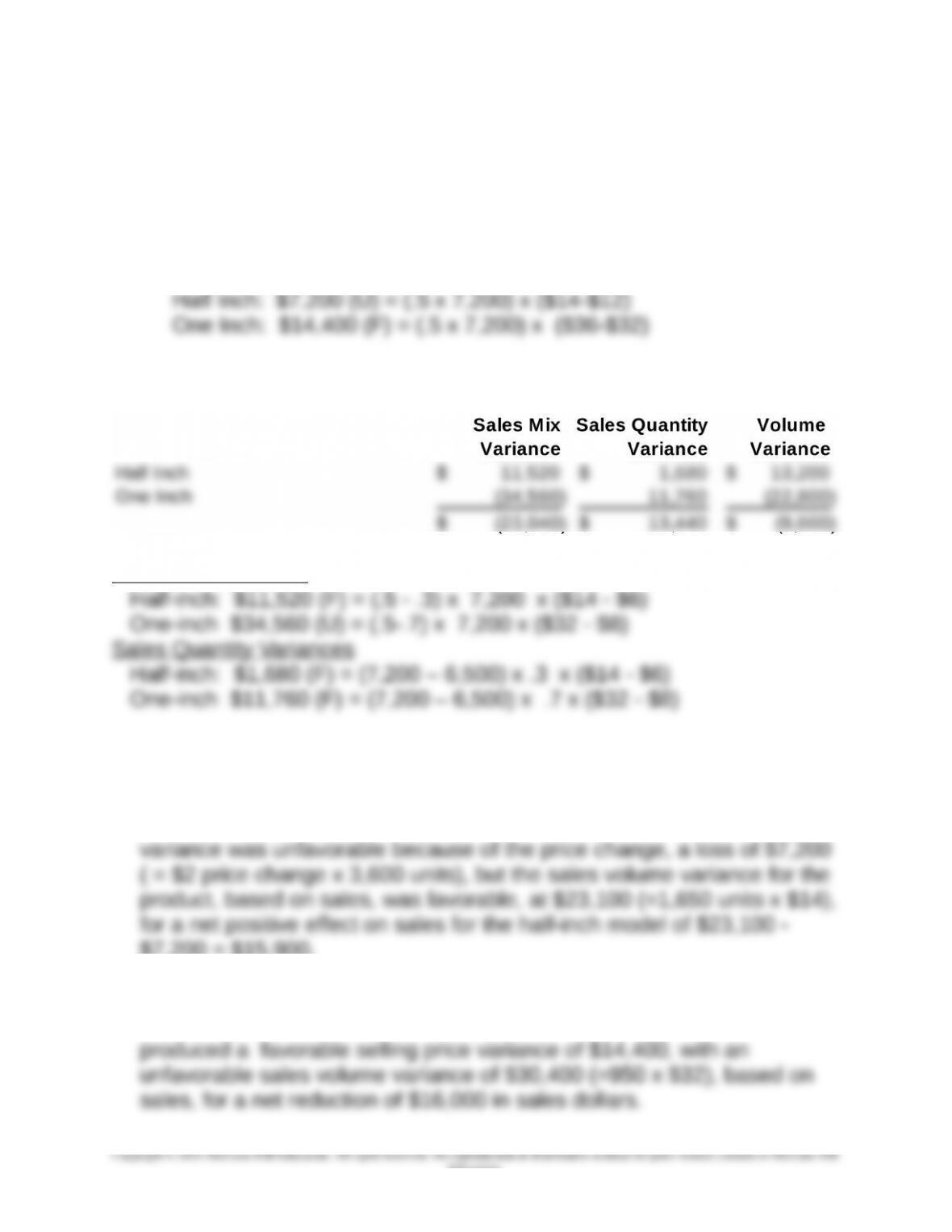

2. The sales mix and quantity variances based on contribution margin are

shown below.

Sales Mix Variances

3.

The sales strategy of decreasing price on the half-inch model was a

success in sales volume as sales units increased from 1,950 (.3 x 6,500)

to 3,600 (.5 x 7,200), an increase of 1,650 units. The selling price

$7,200 = $15,900.

The strategy of increasing price on the one-inch model could have

caused the fall in sales of 950 units (.7 x 6,500 – .5 x 7,200) but it

16-56

Education.

Chapter 16 – Operational Performance Measurement: Further Analysis of Productivity and Sales

16-56 (continued -2)

The cost of the increased sales volume on variable costs was $9,900 =

1,650 x $6 for the increased sales of the half inch model. The reduced

variable costs because of the reduced sales of the one-inch model was

950 x $8 = $7,600.

The net effect on operating income of the sales strategies was

16-57

Education.