Chapter 06 – Process Costing

6-52 Implementing Process Cost Systems; Activity-based Costing;

Standard Costing (25 min)

Case 1: Because of the moderate volatility in materials prices and because

of the relatively large percentage of costs in ending work-in-process, the

FIFO method should be chosen over the weighted-average method in this

case. The batch sizes fit in a relatively narrow range (100-250 batch size

Case 2: This is the simplest case, with stable prices, low ending inventory

and average batch size. A normal cost, traditional, weighted-average

method is likely to work fine. Because prices do not fluctuate, there is little

need for department-level standards and analysis to identify cost variances,

and since there is little ending inventory, there is little need for FIFO

Case 3: this case involves highly volatile materials prices and materials are

a significant percentage of product cost, so that a standard cost and a FIFO

method would be appropriate. The fact that ending work-in-process is a

relatively significant cost supports this conclusion; using FIFO would mean

Case 4: Prices are stable so that standard costing and FIFO are probably

not needed. Also, ending work-in-process inventory is relatively low, so

that FIFO is probably not needed to more accurately determine the

assignment of costs to ending work-in-process and finished goods.

6-48

Chapter 06 – Process Costing

6-52 (continued -1)

Case 5: The range of batch sizes is relatively narrow, so there is no

apparent need for ABC costing. However, with the relatively large

percentage of materials cost in product, and because of the moderate

volatility in materials prices, a standard costing system should be

considered. Also, because of the materials price volatility and the

6-49

Education.

Chapter 06 – Process Costing

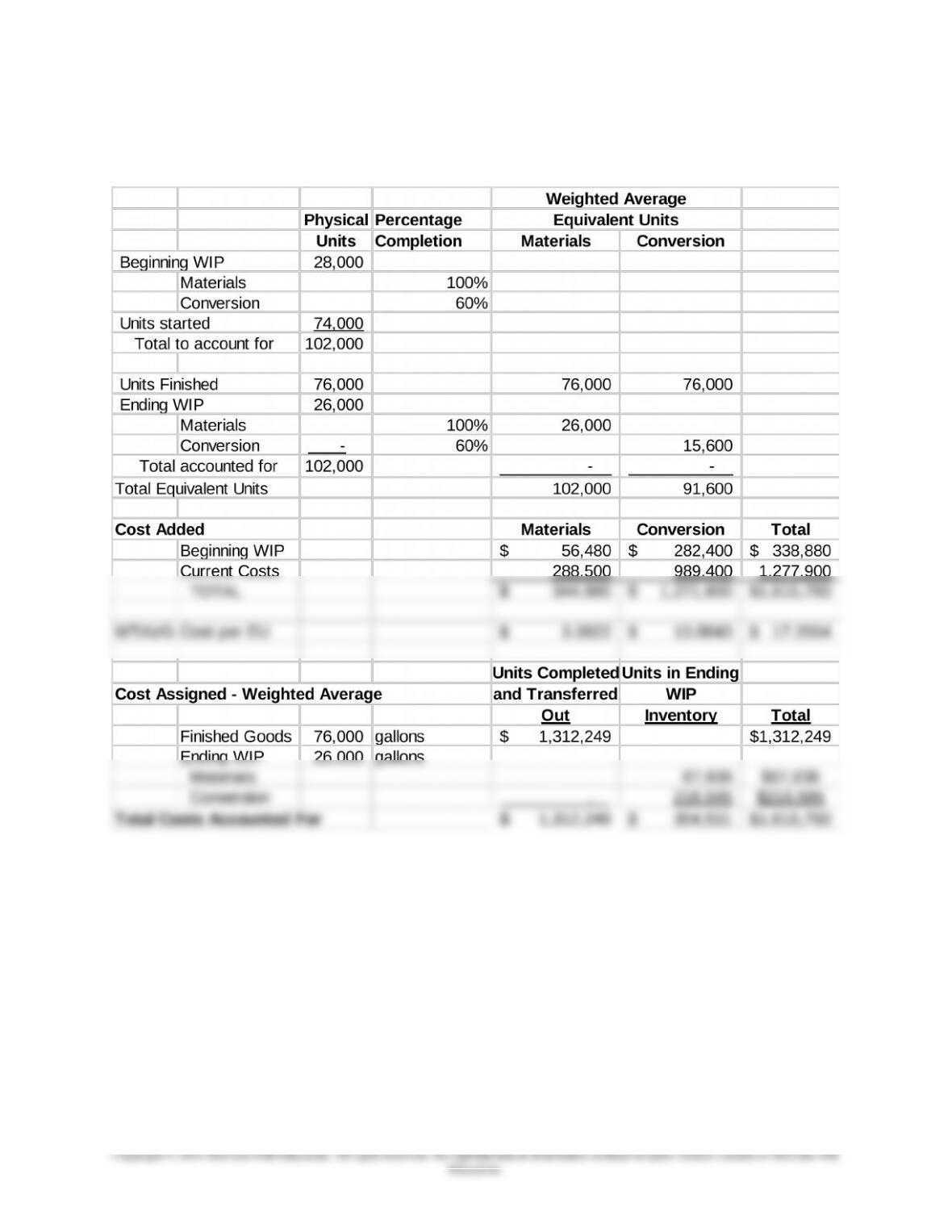

6-53 Weighted Average Method; Two Departments

1. Production Cost report for the mixing department

6-50

Chapter 06 – Process Costing

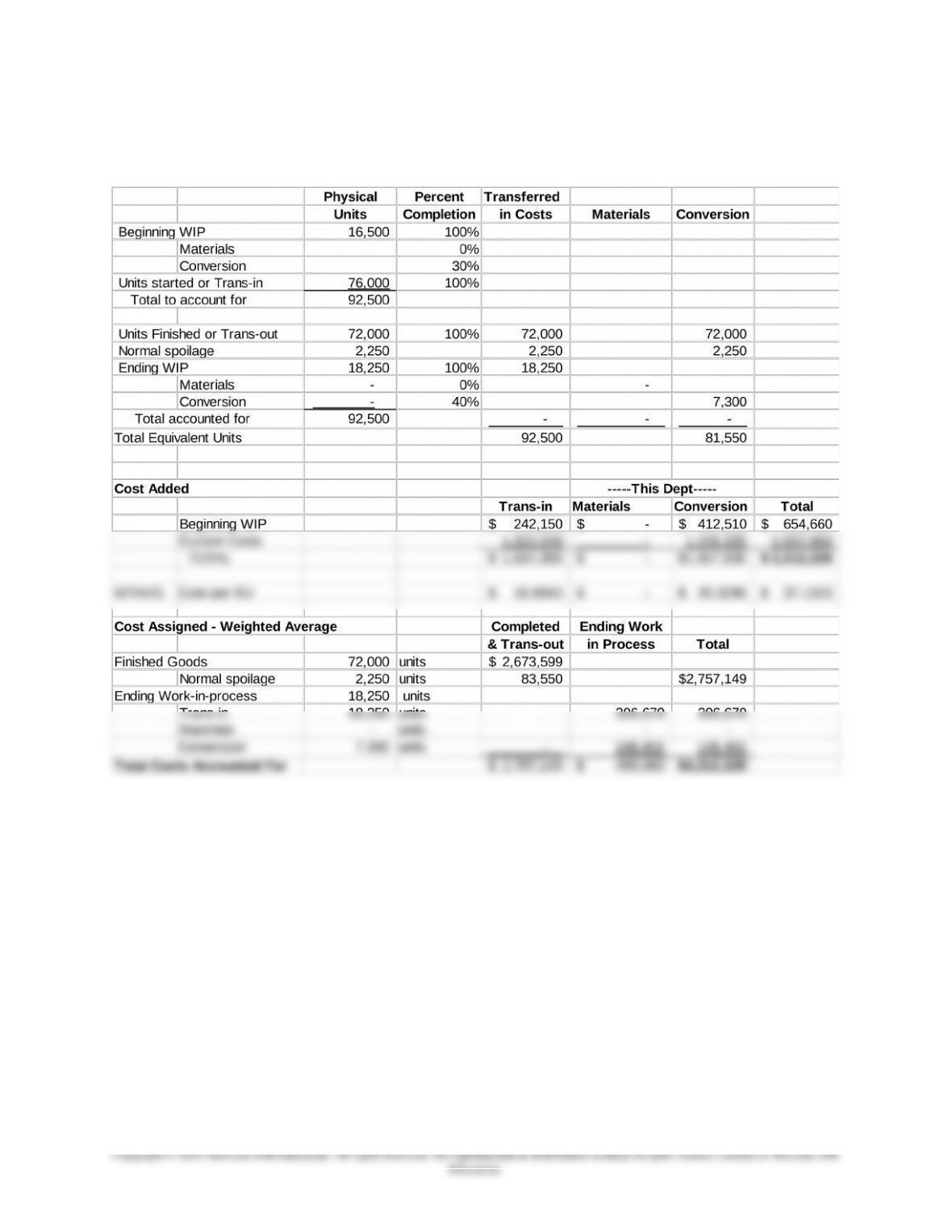

6-53 (continued -1)

2. Process cost report for reacting department

6-51

Chapter 06 – Process Costing

6-53 (continued -2)

3. Some observations about the two cost reports:

The amount of normal spoilage is relatively small at less than

3%. Why, however, does the firm not consider accounting for

abnormal spoilage to take into account the cost of spoilage

arising from for example: operating error, impure materials,

4. The company’s strategy is best described as a differentiation strategy

based upon its focus on research, product development and

customer service. Note in particular that the company has focused

on a small number of customer that purchase in large quantities. So

a part of the company’s strategy is to achieve strong profits through

lower downstream costs, as noted in the previous chapter in the

The company uses a combination of job and process costing. Job

costing is a good fit for the company’s strategy of focusing on large

purchases; the job costs are efficiently and conveniently allocated to

these large purchase orders. Also, the use of process costing

6-52

Education.

Chapter 06 – Process Costing

6-54 Backflush Costing

1.

(1) Materials purchased.

Materials Inventory 710,000

Accounts Payable, Cash 710,000

(2) Conversion cost incurred.

Conversion Cost Incurred 1,450,000

Wages payable, other accounts 1,450,000

($8.50×155,000)

(4a) Close the two conversion cost accounts to Cost of Goods Sold:

Conversion Cost Applied 1,317,500

Cost of Goods Sold 132,500

Conversion Cost Incurred 1,450,000

(4b) Close the actual usage of inventory to Cost of Goods Sold

Actual usage = $142,000+$710,000 – $185,000 = $667,000

Note to Instructor: the above treatment of the differences between actual

and applied materials and conversion is simplified for this brief section on

backflush costing, and assumes that the topic is covered prior to standard

costing. If covered after standard costing, the treatment of the materials

and conversion variances can be enhanced.

6-53

Education.

Chapter 06 – Process Costing

2. Backflush costing is used when the level of work-in-process inventory

is very small. This can be the case for firms that use just-in-time

manufacturing (JIT), so that purchases are carefully coordinated with

6-54

Education.