Chapter 12 – Strategy and the Analysis of Capital Investments

12-54 (Continued–1)

2. The following spreadsheet excerpt contains the PV of each alternative:

Sample Calculation:

Cell D111 = after-tax cash operating cost ($48,000 = (8,000 machine hours ×

$10/machine hour) × 0.60) less tax savings on depreciation ($4,000 =

Then, use the following Goal Seek commands in Excel:

12-83

Education.

Chapter 12 – Strategy and the Analysis of Capital Investments

12-54 (Continued-2)

3. Alternative facts:

Revised overhaul cost = $80,000

Note: the PV cash-flow amounts listed below (viz., ($42,323.6) and ($39,471.2)) were generated using

the NPV built-in function in Excel

12-84

Chapter 12 – Strategy and the Analysis of Capital Investments

12-54 (Continued-3)

Calculations for the above are from part (1), Problem 12-53,

reproduced as follows:

Overhaul in 2 Years

Years 1 and 2:

Depreciation expense per year (SL basis):

($120,000 – $20,000) 10 years = $10,000

Income Tax Rate (t) × 0.40

Tax savings on depreciation, Years 1 and 2 $ 4,000

Years 3, 4, and 5:

Book value before overhaul (end of original useful life) $ 20,000

Overhaul cost, Year 3 100,000

Overhaul Now and Again in Two Years:

Savings from the improved productivity = $10/hr. × 8,000 hours × 20% = $16,000

Less: Income Taxes on the savings (@40.0%) = – 6,400

After-tax savings $9,600

Depreciation Tax Savings: Years 1 and 2:

Book value at the time of overhaul: $10,000 × 2 + $20,000 = $ 40,000

Overhaul cost + 80,000

Total amount to be depreciated $120,000

Number of years 2

Depreciation expense per year $60,000

Number of years 3

Depreciation expense per year $10,000

Income tax Rate × 0.40

Tax savings on depreciation $ 4,000

Chapter 12 – Strategy and the Analysis of Capital Investments

12-54 (Continued-4)

4. As a follow-up to (3) above: although the cost difference between

the two alternatives is only $2,852.4, which is less than 0.3% of

12-86

Hill Education.

Chapter 12 – Strategy and the Analysis of Capital Investments

12-55 Comparison of Capital-Budgeting Techniques, Sensitivity Analysis

(75 minutes)

1. Effects of the new equipment on operating income after tax:

Sales $200 × 10,000 = $2,000,000

Cost of goods sold:

Variable manufacturing costs per unit $ 97

Fixed manufacturing costs per unit:

Additional fixed manufacturing overhead:

$250,000 ÷ 10,000 units = $25

Depreciation on new equipment, per unit:

($1,000,000 – $200,000) ÷ 4 = $200,000/year

$200,000 ÷ 10,000 units per year = 20 $ 45

Total manufacturing cost per unit (@ 10,000 units) $142

Times: Number of units × 10,000

Total cost of goods sold (CGS) 1,420,000

Gross margin $ 580,000

2. Years

1 to 3 Year 4

After-tax operating income (see #1 above) $182,000 $182,000

Add: increased depreciation expense (SL basis) 200,000 200,000

After-tax cash inflow from disposal of equipment 0 200,000*

12-87

Hill Education.

Chapter 12 – Strategy and the Analysis of Capital Investments

12-88

Hill Education.

Chapter 12 – Strategy and the Analysis of Capital Investments

12-55 (Continued-1)

3. Under the assumption that cash inflows occur evenly throughout the

year, the payback period is as follows:

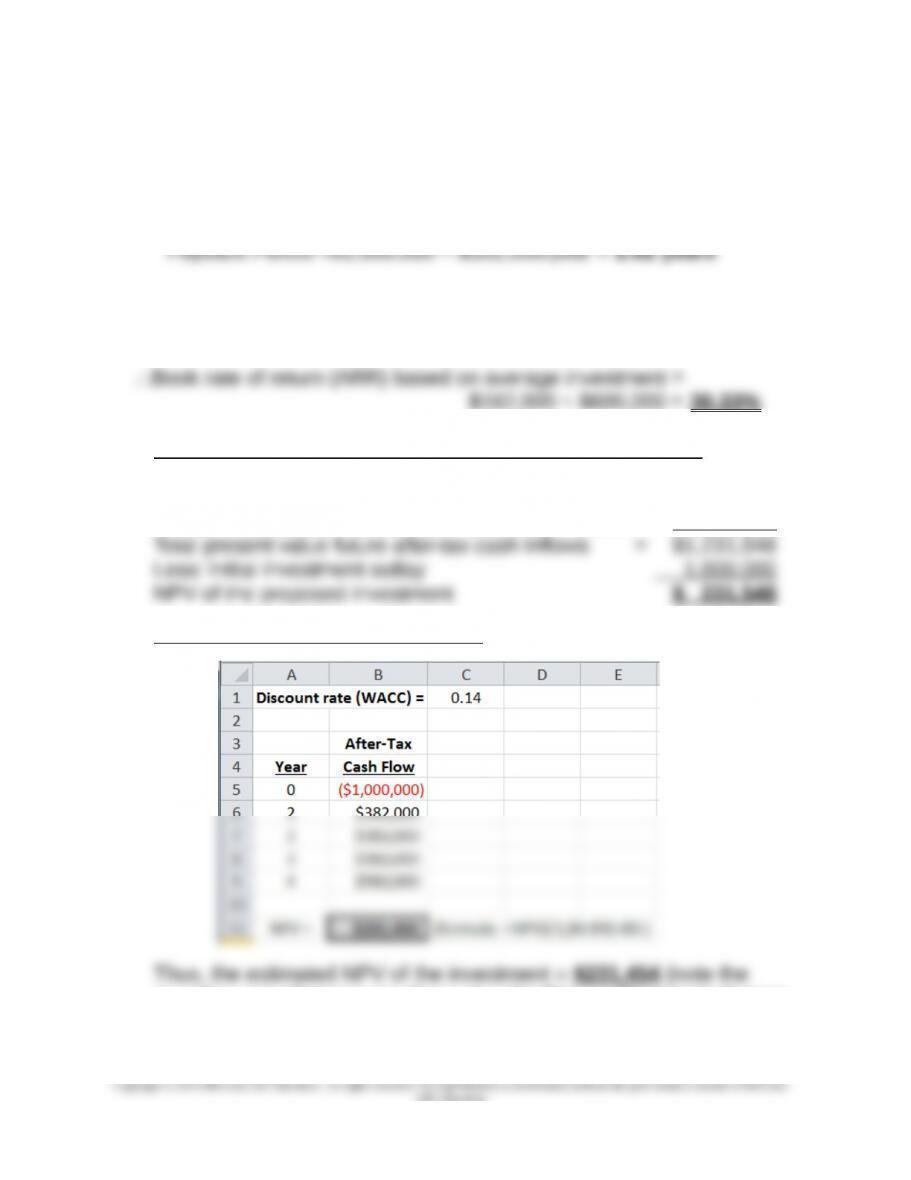

4. Average investment = ($1,000,000 + $200,000) ÷ 2 = $600,000

Average after-tax operating income = $182,000

5. Using PV and Annuity Tables (Chapter 12, Appendix C):

PV of after-tax cash inflows (@14%):

Years 1 through 3: $382,000 × 2.322 = $ 887,004

Year 4: $382,000 + $200,000 = $582,000 × 0.592 = 344,544

Using the NPV Function in Excel:

rounding error that occurs when using the PV and PV annuity factors

from Chapter 12, Appendix C rather than the NPV built-in function in

Excel)

12-89

Hill Education.

Chapter 12 – Strategy and the Analysis of Capital Investments

12-55 (Continued-2)

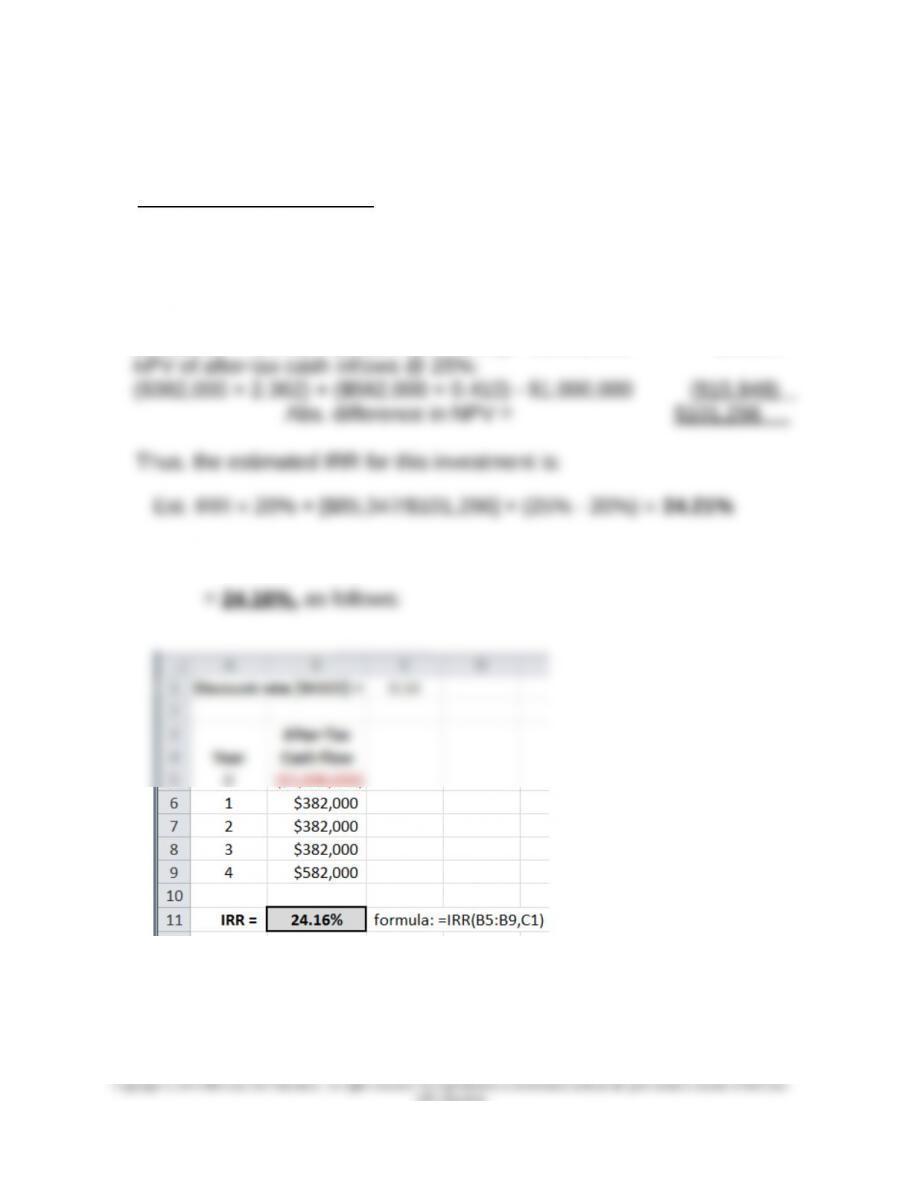

6. Trial-and-Error Approach (initial investment outlay = $1,000,000)—

choose two discount rates (by trial and error) and compute NPV; we

are looking for a discount rate that results in an NPV of $0. Here, we

chose 20% and 25%:

NPV of after-tax cash inflows @ 20%:

($382,000 × 2.589) + ($582,000 × 0.482) – $1,000,000 $85,347

Based on the built-in function in Excel, the estimated IRR of this project

12-90

Hill Education.

Chapter 12 – Strategy and the Analysis of Capital Investments

12-55 (Continued-3)

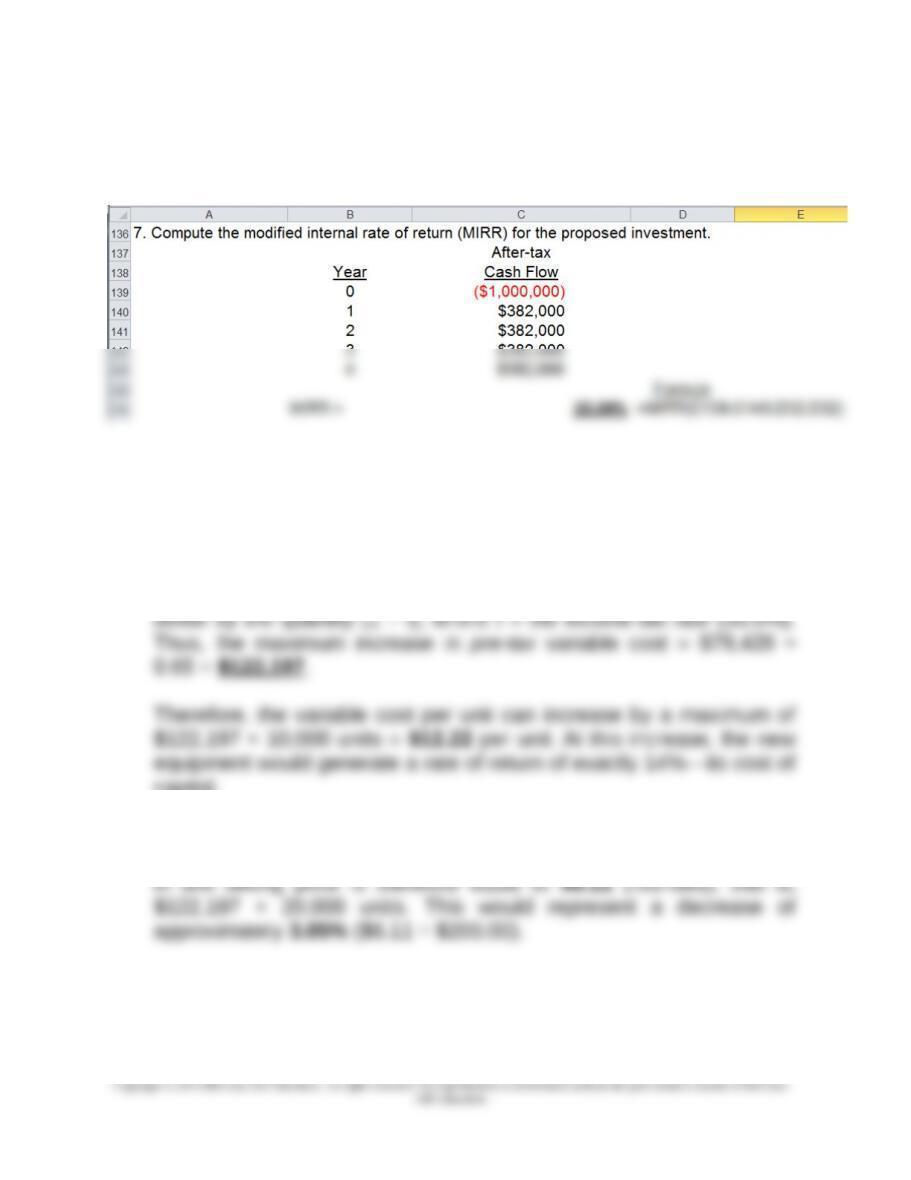

7. The modified internal rate of return (MIRR) = 20.09%, as follows:

8. a. Based on an estimated NPV of $231,548 (part 5, above), the PV of

any after–tax increase in variable costs associated with units

produced by the new machine = $231,548. Thus, the annual after-tax

increase that would be permissible = $231,548 ÷ 2.914 = $79,428.

To convert this annual cost to a pre-tax basis, we would have to

capital.

b. The maximum pre-tax decrease in selling price = $154,466 (see (a)

above). On a per-unit basis, for all units sold, the maximum decrease

9. Strategic considerations–-among the additional factors to be considered:

What is the associated risk of not expanding capacity? (e.g., loss

of market share, achievement by competitors of increased

12-91

Chapter 12 – Strategy and the Analysis of Capital Investments

12-55 (Continued-4)

operating efficiencies due to economies of scale, lost opportunity

for Nil Hill to cross-sell to new customers, etc.)

Are there any “real options” embedded in this investment decision

(beyond the abandonment option included in the basic analysis)?

In the absence of increased volume, would Nil Hill be able to

match the anticipated lower prices by competitors?

Are there any strategic factors associated with this investment?

a) Impact of the new equipment on customer response time?

b) Impact of the new equipment on plant safety?

c) Impact of the new equipment on environmental

performance/

management?

d) Impact of the new equipment on process (i.e.,

manufacturing) cycle time?

e) Impact of the new equipment on quality of outputs (e.g., %

of first-pass yield or PPM defects)?

f) Are there any more profitable uses of the existing space?

That is, would this space best be used to increase capacity

of the particular product in question?

12-92

Hill Education.