Chapter 20 – Management Compensation, Business Analysis, and Business Valuation

Profitability

Ratios Relevance 2008 2009 2010 2011 2012 2013

Return on

A measure of management’s

20-11

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation

20-3. Economic Value Added; Review of Chapter 18; Strategy

(Adapted from teaching note prepared by the case writer, Paul Dierks, Wake Forest University)

1. Economic Value Added, or EVA, is a measure of financial performance that combines the familiar

concept of residual income with principles of modern corporate finance NIspecifically, that all capital

has a cost and that earning more than the cost of capital creates value for shareholders. EVA is after-tax

net operating profit (NOPAT) minus cost of capital. If a company’s return on capital exceeds its cost of

capital, it is creating true value for shareholders. Companies consistently generating high EVAs are top

primary emphasis on placating the interests of a firm’s lenders in order to provide a conservative

assessment of the firm’s liquidation value. Thus, the quality of reported earnings are diminished by

various financial accounting rules, like incorporating charge-offs of such value-building capital outlays as

R&D and bookkeeping entries that have little to do with recurring cash flow. This group also feels that

many investors may be fooled by accounting “shenanigans,” but investors who matter are not misled.

the amount of accounting equity capital. However, ROE suffers from distortions of accounting earnings

by, among other things, expensing R&D, selecting LIFO or FIFO for inventory costing, recording

acquisitions as a purchase or a pooling, and burying recurring cash flows generated from operations in

reserves because of accrual accounting methods.

Also, ROE reacts to changes in the debt-to-equity mix a company employs and in the rate of

project by mixing operating and financing decisions. Instead, all projects should be thought of as being

financed with a target blend of debt and equity no matter how they might indeed be financed. Moreover,

by focusing just on ROE, managers may pass up good (wealth creating) projects that are safer than the

average assets of the firm because the return on the project would lower the firm’s ROE. Similarly,

managers may take on bad (wealth reducing) projects that are riskier than the average asset of the firm

most profitable year, had a return on assets that was over 11 %, but its cost of capital was almost 13 %.

Assuming their cost of capital remains at 13 %, accepting projects with risks similar to existing assets, but

with a return below 13 %, reduces shareholder value.

Another comparison to make is against earnings per share (EPS). In contrast to EVA, EPS tells

little about the cost of generating those profits. Since EPS is directly influenced by the amount of earnings

Education.

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation

measures only the quantity of earnings, but the quality of earnings reflected in the price-to-earnings

multiple also matters.

Calculating EVA

In The Quest for Value (Harper Collins Publishers, 1991), G. Bennett Stewart calculates a firm’s

EVA in two ways: an Operating Approach, and a Financing Approach. The Financing Approach builds up

to the rate of return on capital from the standard return on equity in three steps: eliminating financial

leverage, eliminating financing distortions, and eliminating accounting distortions. As a result of the first

two steps, NOPAT is a sum of the returns attributable to all providers of funds to the company, and the

NOPAT return is completely unaffected by the financial composition of capital. What matters is simply

the productivity of capital employed in the business. The financial form in which the capital has been

obtained does not matter. Only the financial approach is presented here; for the development of the

operating approach, consult Stewart’s text.

Before developing the calculations for EVA it is important to first cover the concepts of the equity

equivalent adjustments, or EE’s.

Understanding / Use of Equity Equivalents

Equity equivalents, or ‘EE’s’, per Bennett Stewart’s book, are adjustments that turn a firm’s

accounting book value into “economic book value,” which is a truer measure of the cash that investors

have put at risk in the firm and upon which they expect to accrue some returns. In this way, capital-related

items are turned into a more accurate measure of capital that better reflects the financial base investors

expect to accrue their returns on. Also, revenue- and expense-related equity equivalent adjustments are

included in a NOPAT that is a more realistic measure of the actual cash yield generated for investors from

recurring business activities.

Stewart has identified a total of 164 equity equivalent reserve adjustments; however, only about

1.) Is it likely to have a material impact on EVA?

2.) Can the managers influence the outcome?

3.) Can the operating people readily grasp it?

4.) Is the required information relatively easy to track and derive?

R&D expenditures provide a good example of an equity equivalent adjustment. Under accounting

conventions, outlays for R&D are charged off to the income statement in the period when they are

incurred. These immediate charge-offs as operating expenses say there is no future value to be derived

from R&D. Thus, the firm’s profits are reduced and its capital is undervalued. For EVA purposes, all

reflect the costs and profit of a period. The portion of R&D expenditures that has future value should

appear as an asset. These equity equivalent adjustments are made in calculating EVA.

The following list of equity equivalents and their effect on capital and NOPAT is taken from

Stewart’s book. The asterisked items are equity equivalents in the OSI case. They are described further in

the paragraphs after the list.

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation

Add to Capital: Equity Equivalents

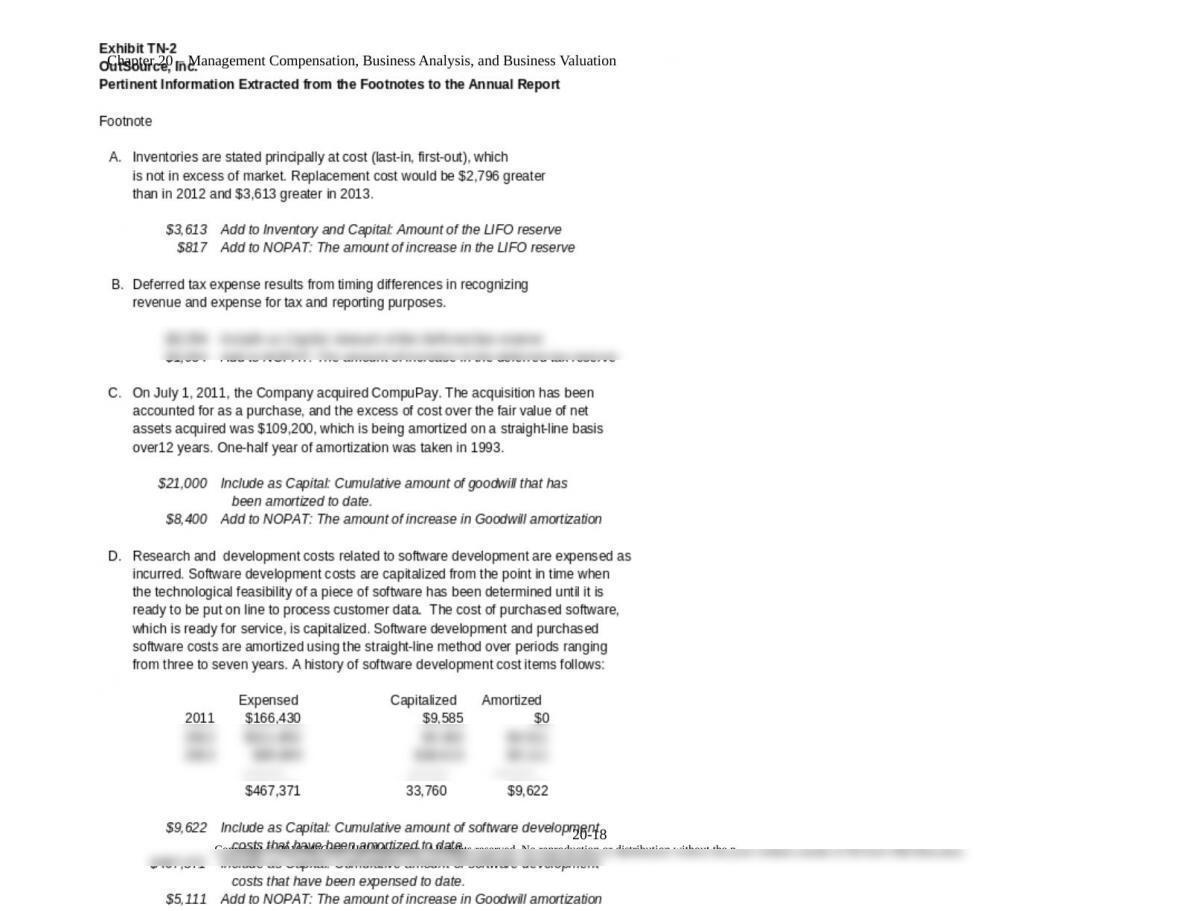

Deferred income tax reserve*

LIFO reserve*

Cumulative goodwill amortization*

Unrecorded goodwill

(Net) capitalized intangibles

Full-cost reserve

Cumulative unusual loss (Gain) after tax

Other reserves, such as:

Bad debt reserve Inventory obsolescence reserve

Warranty reserve Deferred income reserve

Add to NOPAT: Increase in Equity Equivalents

Increase in deferred tax reserve*

Increase in LIFO reserve*

Goodwill amortization*

Increase in (net) capitalized intangibles

Increase in full-cost reserve

Unusual loss (gain) after tax

Increase in other reserves

Deferred Income Tax Reserve. Deferred taxes arise from a difference in timing when revenues

and expenses are recognized for financial reporting versus when they are reported for tax purposes. The

difference between the accounting provision for taxes and the tax amount paid is accumulated in the

reserve for deferred income taxes account. If long-term assets that give rise to tax deferrals are

replenished, a company’s deferred tax reserve increases, which constitutes the equivalent of permanent

equity. Adjusting NOPAT for the change in deferred tax reserve results in NOPAT being charged only

with the taxes actually paid instead of the accounting tax provision. This provides a clearer picture of the

true cash-on-cash yield actually being earned in the business. Action(s) to be taken:

Add to Capital: Amount of the deferred tax reserve

Add to (Deduct From) NOPAT: Amount of increase (decrease) in the deferred tax reserve

The LIFO Reserve. In periods of rising prices, firms save taxes by using a LIFO basis of

inventory costing. Under LIFO, recently acquired goods are expensed and the costs of prior periods are

accumulated in inventory, resulting in an understatement of inventory and equity. A LIFO reserve account

captures the difference between the LIFO and FIFO value of the inventory and indicates the extent that

the LIFO inventories are understated in value. Adding the LIFO reserve to capital as an equity equivalent

adjustment converts inventories from a LIFO to a FIFO basis of valuation, which is a better

approximation of current replacement cost. Also, adjusting NOPAT for the change in the LIFO reserve

brings into earnings the current period effect of unrealized gain attributable to holding inventories that

appreciated in value. Action(s) to be taken:

Add to Capital: Amount of the LIFO reserve

Add to (Deduct From) NOPAT: Amount of increase (decrease) in the LIFO reserve

Changes in the LIFO reserve can also be viewed as a difference between the LIFO and FIFO cost

of goods sold. Including this change in reported profits converts a LIFO cost of goods sold expense to

FIFO, but LIFO’s tax benefit is retained. The overall effect of treating a LIFO reserve as an equity

equivalent adjustment is to produce a FIFO balance sheet and income statement but preserve the LIFO tax

20-14

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation

benefit.

Cumulative Goodwill Amortization. Goodwill arises when the acquisition of another firm is

recorded as a purchase and there is an excess of cost over the fair value of the net assets acquired. The

amount of the goodwill recorded can be amortized against earnings over a period not to exceed 40 years.

To make this non-cash, non-tax-deductible item the non-issue it really is, the amortized amount should be

added back to reported earnings. And, to be consistent, the cumulative goodwill that has been amortized

must be added back to equity capital and to goodwill remaining on the books. By un-amortizing goodwill

in this way, the rate of return will properly reflect the true cash-on-cash yield that is of interest to

shareholders. Action(s) to be taken:

Add to Capital: Amount of the cumulative goodwill amortization

Add to NOPAT: The amount of increase in goodwill amortization

An Overview of the Process Involved in Calculating EVA

The solution of the OSI case is in the attached Exhibits that have been prepared for OSI (TN-1

through TN-3).

The following is a list of the steps to be completed in calculating OSI’s EVA amounts:

1. Obtain a Balance Sheet and Income Statement for 2013

2. Obtain the footnotes to those financial statements;

3. Analyze the footnotes for information on equity equivalent adjustments;

4. Obtain information on the firm’s stock, debt and interest rates;

5. Determine equity equivalent adjustment amounts by analyzing the footnotes;

6. Calculate the firm’s weighted average cost of capital;

7. Prepare worksheets of EVA statements

8. Prepare final statements of EVA showing amounts calculated for RONA (Return on Net

Assets), and EVA

Calculating EVA

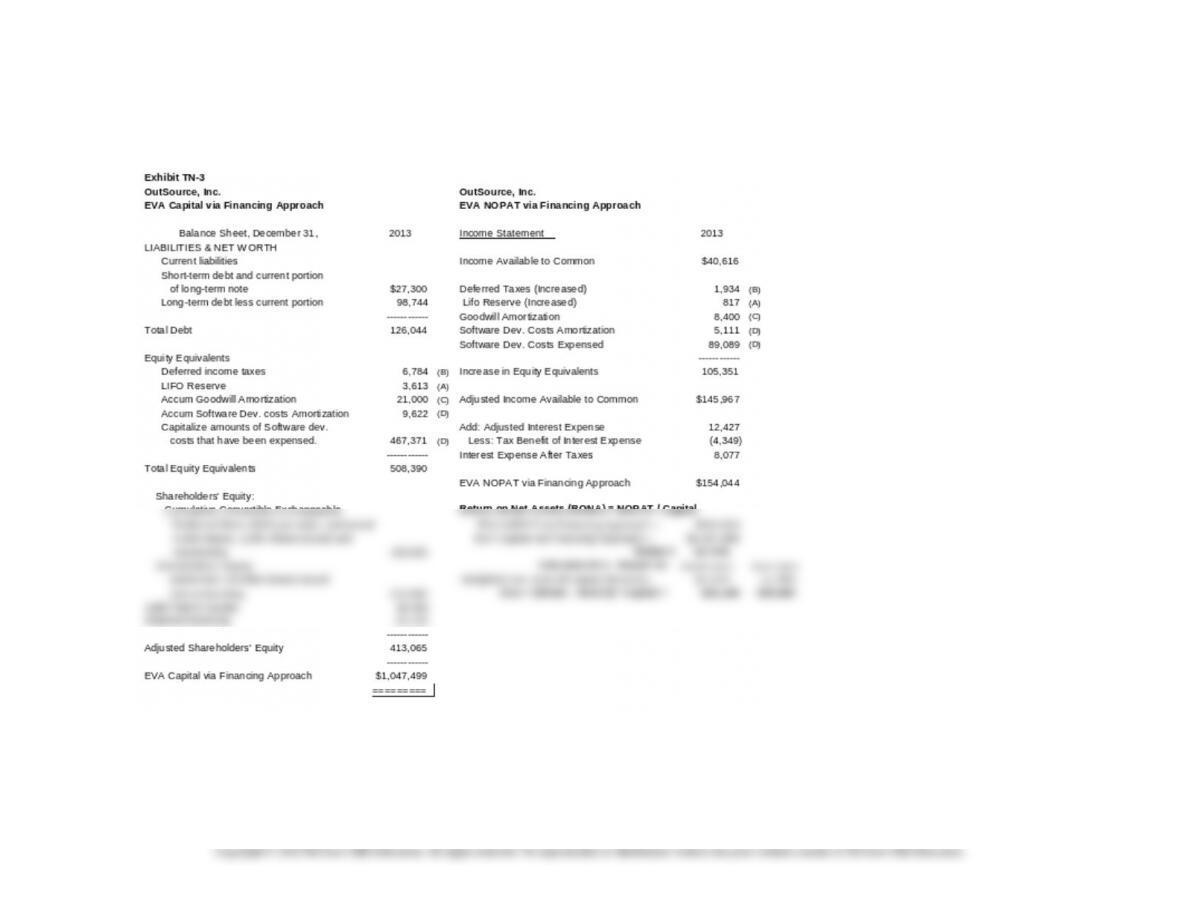

EVA calculations for OSI in 2013 using the Financing Approach are detailed in Exhibit TN-3.

Refer to Exhibits TN-1 and TN-2 for relevant information on the WACC and the equity equivalent

adjustment amounts involved in these calculations.

Note: This case situation focused primarily on EVA, but other valuation-based performance

metrics exist such as NPV, CFROI, and RI. CFROI (cash flow return on investment) is a rate of return

measure calculated by dividing inflation-adjusted cash flow from the investment by the inflation-adjusted

amount of the cash investment. While CFROI does adjust for inflation, it fails to account for risk and the

appropriate required return on the project. In a sense, CFROI is similar to the internal rate of return (IRR)

after including the EE adjustments, hence it measures the investment’s return as opposed to the wealth

created or destroyed by the investment.

2. Benefits / Advantages and Disadvantages of EVA

All managers basically have the same objective putting scarce capital to its most promising

uses. To increase their company’s stock price, managers must perform better than those with whom they

compete for capital. Then, once they get the capital, they must earn rates of return on it that exceed the

return offered by other, equally risky seekers of capital funds. If they accomplish this, value will have

is used and on the cash flow generated from it. It runs counter to the notion that long-term stock

appreciation comes from earnings.

20-15

Education.

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation

Focusing on EVA growth provides two benefits: 1) management’s attention is focused more

toward its primary responsibility increasing investor wealth; and, 2) distortions caused by using

historical cost accounting data are reduced, or eliminated. As a result, managers spend their time finding

ways to increase EVA rather than debating the intricacies of the fluctuations in the earnings reported in

their traditional accounting statements.

EVA measures the amount of value a firm creates during a defined period through operating

decisions it makes to increase margins, improve working capital management, efficiently using its

production facilities, redeploying underutilized assets, etc. Thus, EVA can be used to hold management

accountable for all economic outlays, whether they appear in the income statement, on the balance sheet

or in the financial statement’s footnotes. EVA creates one financial statement that includes all the costs of

being in business, including the carrying cost of capital. The EVA financial statement gives managers a

complete picture of the connections among capital, margin and EVA. It makes managers conscious of

every dollar they spend, whether that dollar is spent on or off the income statement, or on operating costs

or the carrying cost of working capital and fixed assets.

Another very subtle benefit for a firm that adopts EVA is that it creates a common language for

making decisions, especially long-term decisions, resolving budgeting issues, evaluating the performance

of its organizational units and their managers, and measuring the value-creating potential of its strategic

options. An outgrowth of such an environment is that the quality of management also improves as

managers begin to think like owners and adopt a longer horizon view.

3. To this point, the emphasis has been on how focusing on EVA may help managers increase shareholder

wealth. However, for the metric to help in creating shareholder wealth, managers must behave in a

manner consistent with wealth creation. One powerful way to align managers’ interests with those of the

shareholders is to tie their compensation to output from the EVA metric. In fact, it is not just for

managers, but may be used for all employees. When implemented correctly, the basic notion of increasing

shareholder value will permeate the entire organization, and employees at all levels will then begin to act

in concert with upper levels of management.

Implementing an EVA-based incentive plan is fundamentally a process of empowerment

getting employees to be entrepreneurial, to think and act as owners, getting them to run the business as if

they owned it, and giving them a stake in the results they achieve.

The overall, firm-wide objective is to generate a persistent increase in EVA. To achieve that,

employees must understand the role they play in increasing a firm’s EVA. A key factor in sustaining a

continuing interest in EVA and in making it work is to revise the compensation system to focus on

creating value. It has been shown that one of the critical components in successfully using EVA to

improve a company’s MVA is tying it to bonuses and pay schemes. Designing an incentive compensation

system that pays people for sustainable improvements in EVA, in concert with an understanding of what

drives EVA, and what drives economic returns, is what transforms behavior within a company.

A good way to get started quickly is to increase insider ownership of the firm’s stock. One way to

do this is to turn old profit-sharing plans into employee stock-ownership plans.

If an incentive system is to work, it must have certain distinctive properties:

1. An objective measure of performance, which cannot be manipulated by one of the parties who

may benefit. For example, in many existing plans, the budget is a commonly used target for

performance, but the manager being evaluated is usually heavily involved in negotiating that

budget.

2. It must be simple so that even employees far down in the organization will understand how EVA

is tied to economic value and can follow it well.

3. Bonus amounts have to be significant enough in amount for employees to alter their behaviors.

20-16

Education.

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation

20-17

Exhibit TN-1

Financial Data Input and Calculation of Interest Rates/Expense:

Calculate Weighted Ave. Cost of Capital – Based on Market:

Rate

Interest

Weights:

Pct of Total

Short-term Debt:

$8,889

8.00%

$711

Long-term Note Payable

$117,155

17.8%

Long-term Debt: Current portion

$18,411

10.00%

$1,841

Preferred Stock

Long-term Debt: Long-term portion

$98,744

10.00%

$9,874

Shares o/s

1,000

$117,155

Interest paid=

$12,427

Par value

$100

$100,000

15.2%

Common Stock

Risk-free rate (90 day T-bills)=

5.0%

Shares o/s

219,884

Return on the Market=

12.5%

Market value

$2.00

$439,768

66.9%

Beta Value of common stock=

1.2

—–—-

Tax Rate=

35.0%

$656,923

Price per share of common stock=

$2.00

Weighted Average Cost of Capital

For Debt=

1.159%

Calculated Cost of Equity Capital:

14.0%

For Preferred Stock=

1.674%

Common stock dividend/share paid last year=

0.111

per share

Common Stock=

9.372%

Total common stock dividend paid last year=

$24,429

——-

Calculated current dividend yield (last year)=

5.555%

12.206%

Expected growth rate of dividends=

8.000%

Future dividend yield (next year)=

5.999%

Calculate Weighted Ave. Cost of Capital – Based on Book Value:

Common stk dividend/sh. expected-next year=

0.120

Weights:

Pct of Total

Total common stock dividend to pay next year=

$26,383

Long-term Note Payable

$117,155

22.1%

Check: Calculated Future dividend yield (next year)=

5.999%

Preferred Stock

Preferred stock dividend/share paid last year=

$11.00

per share

Shares o/s

1,000

Total preferred stock dividend paid last year=

$11,000

Par value

$100

$100,000

18.9%

Total preferred stock dividend for next year=

$11,000

Common Stock

Share Book Value

$219,884

Paid-in capital

$32,056

59.0%

Retained earnings

$61,125

$313,065

————

$530,220

Weighted Average Cost of Capital

For Debt=

1.436%

For Preferred Stock=

2.075%

Common Stock=

8.266%

——-

11.777%

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation

20-18

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation

20-19

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation

20-4 John Deere Case

Question 1: As discussed in the case, performance-evaluation and reward systems play a fundamental role in guiding employees’ actions and,

optimally, such systems should induce employees to engage in organizationally desirable behaviors. When entering into labor contracts,

employees and employers likely have differing objectives. On the one hand, employees want to maximize the benefits they extract from their

relationship with the organization. Employees likely desire to maximize their compensation, minimize their effort, and perform tasks that provide

the most intrinsic enjoyment (and future compensation). Employers (owners), on the other hand, hire employees to increase an organization’s

value. They want employees to exert high levels of effort towards projects with the greatest expected payoffs for the lowest possible cost.

Performance-evaluation and reward systems should dampen, if not mitigate, the conflicts of interest between employees and employers. To this

end, performance-evaluation and reward systems serve many vital functions in an organization (most of these are directly or indirectly discussed in

the case). First, such systems serve a motivational role whereby employees are enticed to exert high levels of effort (duration and intensity) on

organizational endeavors. In this regard, such systems not only need to compensate employees for hours spent at the firm site but also need to

reward employees for their productivity during working hours.

Second, performance-evaluation and reward systems serve a directing, or informational role. Employees typically perform several different tasks

Management could improve the effectiveness and efficiency of the production process, thereby reducing the cost, improving the speed, and/or

increasing the quality of production. Performance-evaluation and reward systems should make it profitable for employees to share their private

information with other members of the organization.

Finally, performance-evaluation and reward systems serve an attracting role. Such systems should entice employees with the requisite abilities and

skills desired by the organization to seek employment with the organization. Via employment contracts, organizations can attempt to sort or screen

20-20