Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Chapter 20 - Management Compensation, Business Analysis, and Business Valuation

20-45 Incentive Pay Formula Development (30 min)

1.

There are two goals, a goal for number of customers and a price

goal:

Customer goal:

300/day target customers x 365 days = 109,500 customers

½ weight x $12,800 = $6,400

$6,400/109,500 = $ .058 per customer served

Price goal:

Thus the compensation plan is:

Note that there are alternative ways to develop the

compensation plan. For example, the restaurant manager can

develop a reward system which pays no bonus unless the average

2. If 280 customers are served per day at $6.75 average price per

person, the total compensation to the manager would be:

Chapter 20 - Management Compensation, Business Analysis, and Business Valuation

20-46 Compensation Pools; Residual Income; Review of Chapter 19

(40 min)

1.

Revenue Income Assets Asset Return on

Return

on

Consumer Electronics Turnover Sales Assets

2014 $ 155,780 $ 16,750 $ 84,550 1.842 10.75%

19.81

%

2015

125,480

9

,500 90,450 1.387 7.57%

10.50

%

2016

90,950

5

,700 92,450 0.984 6.27% 6.17%

Office Supplies

2014

48,750

2

,100 22,500 2.167 4.31% 9.33%

2

10.68

Computers

2014

100,500

2

,350 21,450 4.685 2.34%

10.96

%

1

WBI Total

2014

305,030

21

,200 128,500 2.374 0.070

16.50

%

2015

266,540

13

,490 134,900 1.976 0.051

10.00

%

2016

258,100

11

,525 134,550 1.918 0.045 8.57%

The calculations above show that 2016 had mixed results for MBI, as

income fell for one of the divisions and sales and profits increased for

20-32

Education.

Chapter 20 - Management Compensation, Business Analysis, and Business Valuation

20-46 (continued -1)

2016 its return on assets increased in both these years, and quite

significantly in 2016; the Consumer Electronics division, with falling

sales and income, while assets increased, saw its asset turnover,

The Computer division, another large division, had a bad year

in 2015 but recovered nicely in 2016. Overall, WBI saw a steady

decline in return on assets over the three years, due primarily to the

problems in the Consumer Electronics division.

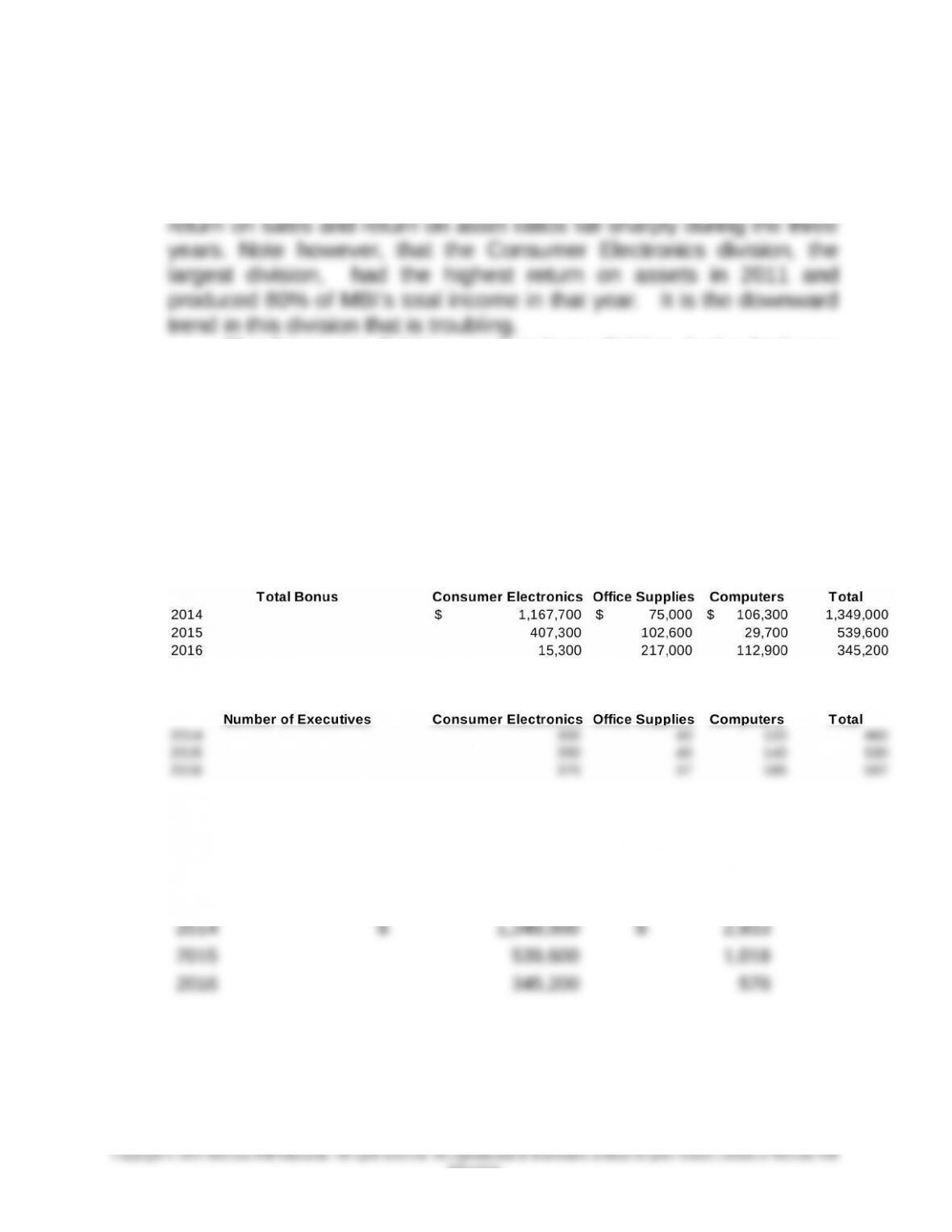

2. [Operating Income - (.06 x Invested Assets)] x .10 = Bonus

Amount

The total bonuses for each division and in total are determined as

follows: (actual amounts; not in 000s)

And given the number of executives:

The Firm-wide bonuses for executives are as follows

Firm-wide Bonus Bonus

Bonus per

Executive

As for the sales and income in 2016, the bonus amounts for

executives fell sharply in 2016, and declined over the three-year

period.

20-33

Education.

Chapter 20 - Management Compensation, Business Analysis, and Business Valuation

20-46 (continued -2)

3.

When bonuses are determined on a division-based method, the

results are as follows:

Bonuses per executive were largest for consumer electronics in 2014

because this division, the largest, generated the largest amount of

residual income in 2014; per-executive pay is highest in Consumer

Electronics despite the fact that it has the largest number of

executives. Bonuses increased in Office Supplies because of the

4.

Comparing the results for the three divisions in parts 2 and 3, it is

clear that the Consumer Electronics division managers would benefit

from the division-based plan based in 2014 and 2015, while the

Office Supplies division would benefit in 2015 and 2016 and those is

the Computers division benefit in 2016.

motivation for MBI. To make the firm-wide plan work for all divisions,

particularly the Office Supplies division, MBI top management should

work to make the opportunities for cross-division profit clear.

20-34

Chapter 20 - Management Compensation, Business Analysis, and Business Valuation

20-46 (continued -3)

Pros: The company-wide bonus plan promotes the sharing of

expectations.

Cons: The company-wide bonus plan includes many factors not

20-35

Education.

20-47 Compensation; Strategy (25 min)

For companies with substantial growth opportunities or long

product life cycles, bonus plans based on short-term decisions may

not adequately reflect long-term consequences of managerial

decisions.

DBI could consider a stock option plan that initially sets the

exercise price of the option at the current share price, but then

options to be paid off.

DBI may want to consider granting stock options where the

exercise price is adjusted with the appreciation of an industry index.

This will allow DBI to reward executives for an increase in the value

of their stock relative to that of companies facing similar risks.

DBI could also establish a bonus account system (deferred

bonus system). Under this system the executives do not receive the

increase current performance measures at the expense of damaging

future performance.

Developing effective compensation plans is more difficult for

multinational companies such as DBI because foreign currency

frequently managers of foreign SBUs are able to protect their unit

from unfavorable currency fluctuations by carefully chosen

purchasing, sales, and financing practices.

20-36

Chapter 20 - Management Compensation, Business Analysis, and Business Valuation

20-48 Executive Compensation; Teams; Strategy; Ethics (30

min)

1. Universal should use the new measures to improve product

quality and customer satisfaction.

a. At least three customer value-added measures for Universal Air

Inc. include the following:

Availability of products to meet customer needs on a timely

b. At least three process-efficiency measures for Universal include

the following:

New product development time and introduction time to market.

2. At least three types of employee behavior that Universal Air Inc.

can expect by having middle management participate in the

development of the second set of new performance measures include

the following:

Increased job satisfaction and morale, as well as a feeling of

3. To ensure that the cross-functional teams are effective, the

executive management at Universal Air Inc. needs to provide:

20-37

Education.

Chapter 20 - Management Compensation, Business Analysis, and Business Valuation

20-48 (continued -1)

functional managers and team members, and support for the

implementation of team-suggested changes.

4. Referring to the specific standards (competence, confidentiality,

integrity, and credibility) in the Institute of Management Accountants

Statement on Ethical Professional Practice, John Brogan's behavior

is unethical for the following reasons:

Competence

Brogan is undermining the preparation of complete and clear

Integrity

By curtailing the reporting of customer complaints, Brogan has failed

to:

avoid a conflict of interest,

Credibility

Brogan did not:

communicate information fairly and objectively disclose fully

all relevant information.

20-49 Compensation; Regression Analysis (40 min)

20-38

Chapter 20 - Management Compensation, Business Analysis, and Business Valuation

The results are shown below:

Correlation Analysis:

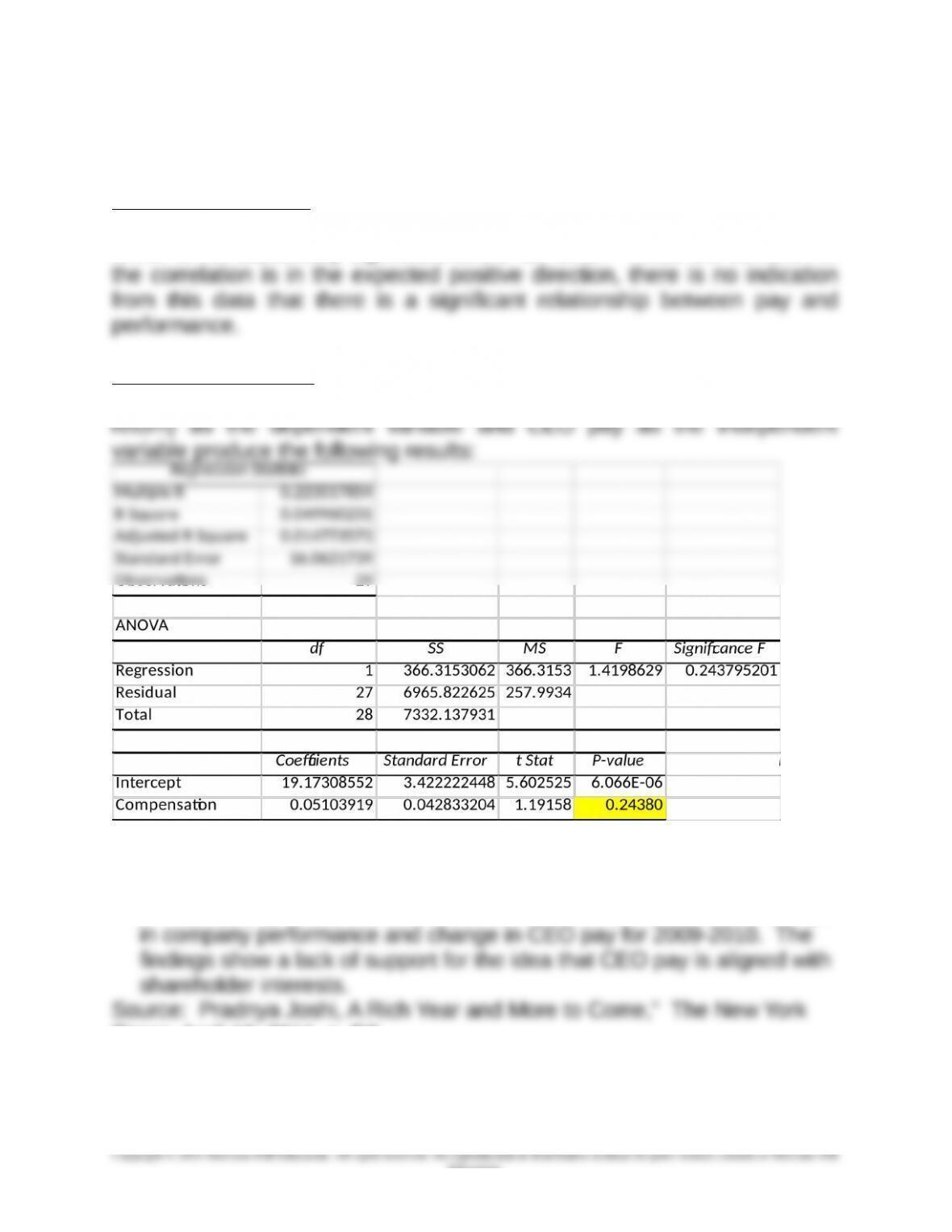

Correlation between executive pay and company performance is .223518

which is not statistically significant at the .10 level. While the direction of

Regression Analysis:

A regression analysis with company performance (measured by stock

The above regression results confirm the correlation results shown

above. The p-value for the compensation variable is .2438, well short

of a level for statistical significance.

The findings show little evidence of a correlation between the change

Times, April 10, 2011, p. B7.

20-50 Compensation; Regression Analysis (20 min)

20-39

Education.

Chapter 20 - Management Compensation, Business Analysis, and Business Valuation

1. Given the available information, the most reliable regression appears to

2. The regressions have some common patterns:

return on assets (ROA) is not a significant predictor of CEO pay for

any of the dependent variables.

stock price volatility is significant at the lower level of reliability (.05) in

is, less ownership means higher pay. The authors argue that this is

consistent with the expectation that lower levels of ownership require

stronger incentives, and thus higher CEO pay.

There are mixed results for the remaining variables, passenger load,

CEO tenure, and book to market value. These variables are not

significant in at least one of the regressions, indicating there is

potentially some relationship there but the nature of the relationship

depends on the dependent variable chosen, and that further analysis

would be necessary to understand the nature of the relationships

between these variables and CEO pay.

3. The principal goal of the study was to identify a potential relationship

between non-financial performance, as measured by passenger load, and

CEO compensation. Seven additional variables were added to control for