Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and The Role of

Nonfinancial Performance Measures

14-51 (Continued-2)

the quality of information produced by the organization’s comprehensive

management accounting and control system. One desirable quality is that such

information be timely. (Another qualitative characteristic might be “accuracy.”) The

point is that to be useful/relevant to decision makers, accounting information

organizations to monitor resource consumption on a real-time basis.

2. Variances are not tied to specific product lines, production batches, or FMS cells.

This is a variation of the data-aggregation argument presented above in (1).

should recall that standard cost systems in this country were developed many

years ago when product layouts were used (in which long runs of relatively

standardized products were produced). This is, in essence, completely different

from the production environment of today’s advanced manufacturers.

5. In earlier days, products had relatively long life-cycles. This, combined with product

layouts (see #4 above), facilitated the development of standard manufacturing

costs. Today, however, products have much shorter product life cycles. In turn, this

customer service.

The instructor might provide, as a basis for discussion, the following plan that could be

used to evaluate the operating performance of a manufacturing facility each period:

Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and The Role of

Nonfinancial Performance Measures

14-51 (Continued-3)

a. Production processing activity: Cycle time, manufacturing-cycle efficiency, and

productivity measures.

b. Product quality: Number of defective finished products, number of products returned,

Note the focus on activities in the above hypothetical performance evaluation scorecard.

For each major activity (or business process) there would logically be, each period, one

or more strategic objectives. The extent to which these objectives are being

accomplished is assessed through the monitoring and reporting of non-financial

performance indicators such as those listed above. These non-financial performance

metrics would complement the financial performance measures (e.g., standard costs,

flexible budgets, and related variances) in a comprehensive management accounting

and control system.

Benefits/Advantages of Standard Cost Systems

1. Provides a good basis for cost comparisons. To the extent that “cost” is a critical

an organization’s overall management accounting and control system.

2. Enables managers to use management by exception. A standard cost system

can be viewed as a “diagnostic control system,” which monitors itself and

14-72

Education.

Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and The Role of

Nonfinancial Performance Measures

14-52 Production Planning and Control Strategy (30 minutes)

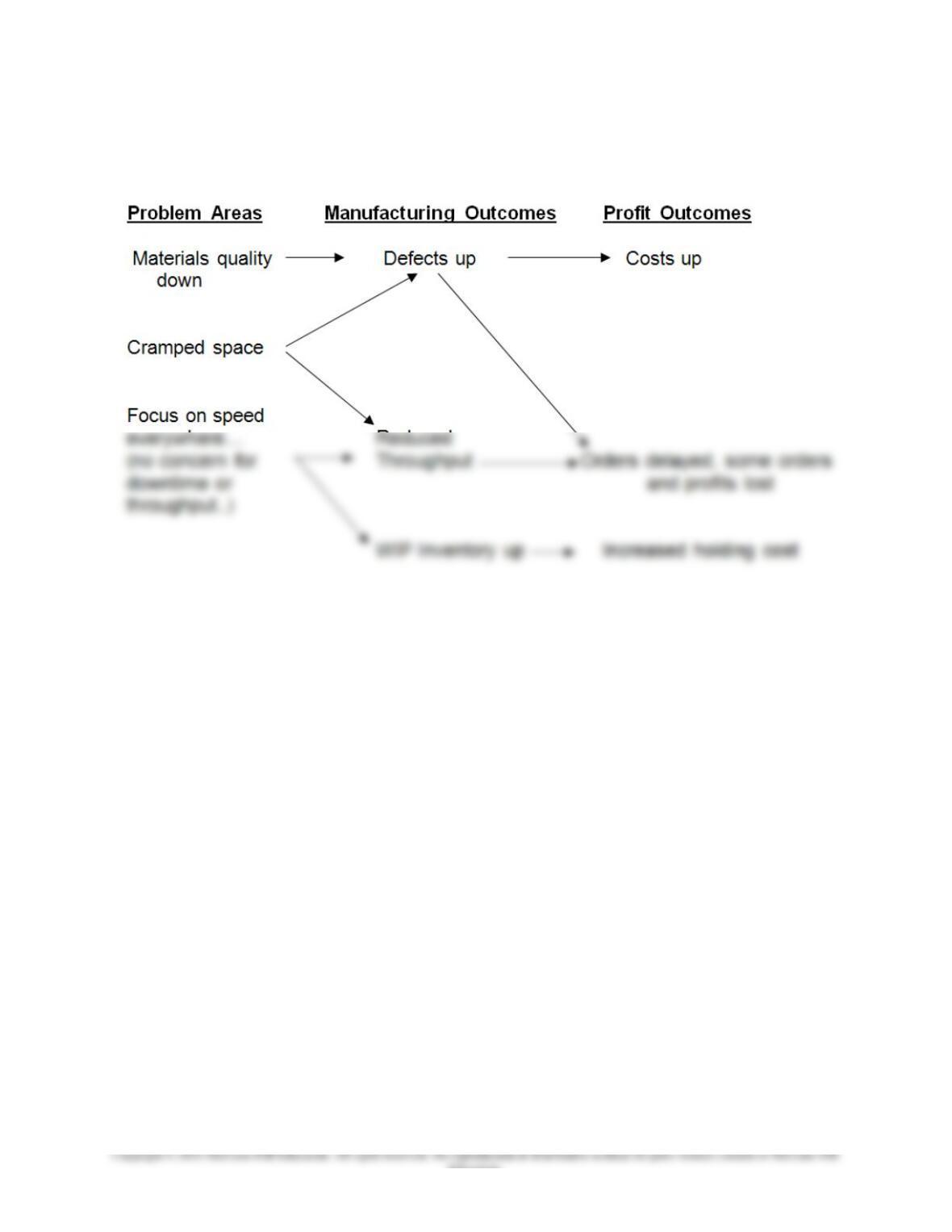

There may be a happy ending to this story if Kristen and Bryan change the focus in

the plant from productivity at each work station and meeting budgets to a focus on

speed and throughput. The current emphasis on productivity at each work station has

the effect that each employee has the incentive to work very hard to meet their

productivity targets, without a consideration of the overall productivity of the entire plant.

This is why work-in-process inventory builds up in places. Some operators are keen on

moving the product through their work stations, and not concerned about what happens

to it downstream.

Also, the emphasis on meeting cost budgets (as in the case of the purchasing

department manager), creates incentives to reduce costs in ways which can cause

delays and defective products. The purchase of discounted material which apparently

led to product defects is an example.

The emphasis on individual productivity has other effects. Since it creates a focus

only on moving product through individual processes, inadequate attention appears to

be given to equipment maintenance or to the prevention of defects. There is insufficient

attention to preventing quality defects. In contrast, there is excessive attention to

correcting defects (re-work). To speed up the process, the rate of defects has to be

reduced. The emphasis on correcting defects merely slows things down. Six-sigma

firms such as Toyota and GE have learned it is less costly as well as faster to prevent

defects rather than to spend time on inspection and re-work. Inspection and re-work are

non-value adding processes that should be eliminated.

Another unfortunate result of the cost allocation method in the plant is that

department managers apparently have the incentive to reduce the amount of space in

which they operate in order to reduce the overhead costs allocated to them. This means

that some work stations, for example Ed’s, are possibly too small for efficient

processing, leading to lower productivity and increased defects. Again, the focus of the

accounting system has set things awry, and provided a dysfunctional incentive.

To repair the situation, Kirsten and Bryan should refocus the plant on throughput and

use a system like the theory of constraints. With the theory of constraints, managers

and employees are rewarded for moving total product through the plant, not just through

their individual work stations. Everyone in the plant has the incentive to look for

bottlenecks and to find ways to reduce the effect of these bottlenecks. Moreover,

employees have the incentive to work together to reduce the bottlenecks and improve

throughput, since the focus is no longer on individual productivity, but on overall

productivity, which is the plant’s ultimate goal.

Summary Presentation of Problem on Chalk/White Board

(see next page)

Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and The Role of

Nonfinancial Performance Measures

14-53 (continued)

14-74

Education.

Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and The Role of

Nonfinancial Performance Measures

X14-53Research Assignment: Service-Based Innovation; Strategy (45-60 minutes)

1. Chapter 14 covers (among other topics) the control of labor and raw material

resource inputs to the manufacturing process. Traditional financial control systems for

these resource inputs consist of the use of standard costs, flexible budgets, and end-of-

period standard cost variance analyses (for example, for price/rate and

quantity/efficiency components of an overall cost variance). At the end of the chapter

the discussion is expanded to make the point that operational control extends beyond

short-term financial control to include a focus on business (including operating)

processes. In this context the importance of non-financial performance

indicators/measures is discussed. The assigned article looks at a method that has been

used successfully to improve operating processes in the health-care sector. As such, it

relates directly to the material covered at the end of Chapter 14. Students should find

the discussion interesting both because of the non-manufacturing context of the

discussion and because, at a macro level, the article deals with a method that if widely

used could improve health-care practice. The latter point is particularly important given

the current health care debate in the U.S.

2. Kaiser Permanente (KP) (www.kaiserpermanente.org/) is one of the nation’s largest

not-for-profit health plans, serving more than 8.8 million members, with headquarters in

Oakland, CA. Innovation Consultancy comprises a small group of

individuals(“innovation specialists”) within KP whose function it is to help develop better,

more efficient ways of performing activities related to the health-care delivery process.

(Go to http://xnet.kp.org/newscenter/opexcellence/2010/081810hbr.html for additional

information.) Innovation Consultancy uses what the unit calls “human-centered design”

or “design thinking” to address operational issues in health-care delivery.) In some

respects, this approach parallels the industrial engineering approach (“time-and-motion

studies”) used in the development of labor standards in a manufacturing context. By

contrast, however, Innovation Consultancy focuses on operating process improvements,

not time-based labor-hour specifications. Specific projects assumed recently by

Innovation Consultancy relate to medication administration error (MedRite), nurse shift

handoff (Nurse Knowledge Exchange), and pain management (Painscape). (See part 4,

below.)

3. Design thinking (or, “human-centered design”) is the term used for the research

methodology used by KP to develop improvements in operating activities/processes

associated with the health-care delivery process. In this method, the consultants work

with nurses (i.e., frontline staff) and patients as collaborators to develop process

innovations to what can be viewed as universal problems in health care (such as the

three problems listed above in part 2). Design thinking is a particularly useful innovation

tool because it brings both health care providers and patients together into the process

to design solutions that result in patient-centric care. Team members observe how

health care providers interact with one another, with patients, with technology, and how

patients respond. To learn more about how Kaiser Permanente’s Innovation

Consultancy has used design thinking, please go to:

http://xnet.kp.org/innovationconsultancy/.

14-75

Education.

Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and The Role of

Nonfinancial Performance Measures

14-53 (Continued)

4. Examples:

a) KP MedRite: As the name implies, the goal of this project was to develop and

implement a plan that would reduce medication errors in hospitals. This requires a

process that ensures that the right medication is given in the right dose to the right

individual. Observation of the existing process by members of Innovation

Consultancy revealed that interruptions and distractions were leading causes of

medication errors. In response (and using inputs from nurses, physicians,

addition, the team developed a five-step sequential process that would ensure that

medications were appropriately dispensed.

b) Nurse Knowledge Exchange: The focus of this project was to improve how

nurses exchanged patient information between shifts, which can typically take 45

minutes or more using conventional procedures. During this “shift-transfer time,”

patients basically have little-to-no direct contact with members of the nursing staff.

Further, the underlying exchange process was unreliable and idiosyncratic. KP’s

Innovation Consultancy team created a new process for passing on higher-quality

to ensure that appropriate information is accurately captured and reliably

transferred to the incoming nurse.

c) Inflection Navigator: The focus of this project was to help patients who have

received a frightening diagnosis (serious cardiac disease, cancer, etc.) deal with

the ensuing steps (follow-up tests, visits to specialists, etc.) for dealing with the

diagnosis. (The delivery of such life-threatening diagnoses is referred to as an

to help the patient navigate through the required steps following deliverance of a

life-threatening diagnosis.

d) Cardiac surgery: Cardiac surgeon Devi Shetty has shown that speed and

efficiency of by-pass surgery can be increased without sacrificing quality of care.

The key is decomposing surgical procedures into basic elements and actions, and

then documenting (thereby standardizing) these procedures according to a “best

practices” model. The analogy to “time-and-motion studies” performed by industrial

engineers in a manufacturing context is apt.

14-76

Education.

Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and The Role of

Nonfinancial Performance Measures

14-54 Research Assignment: Supply-Chain Management; Strategy (30-40 minutes)

1. Chapter 14 covers (among other topics) the control of labor and materials. For the

most part, the discussion in Chapter 14 centers on the financial control of these two

resource inputs through the development of cost standards, flexible budgets, and cost-

variance analysis techniques. As discussed at the end of the chapter, however,

“operational control” extends beyond financial control to nonfinancial standards and

performance indicators. The topic of the assigned reading relates to risk management

and therefore operational control of an organization’s supply chain, particularly through

the use of innovative technology. As such, the topics covered in the article relate broadly

to the material covered in Chapter 14.

2. As used in the assigned reading, the term “provenance” refers to the origin or source

of materials added to a company’s product across the entire supply chain (suppliers of

the suppliers of the company, for example). Consumers, governments, and companies

along the supply chain are demanding increased disclosure about a given product’s

provenance. These stakeholders are concerned (for example) about product safety,

ethics, and assessing the environmental impact associated with a given product’s

supply chain. Companies that fail to take a proactive position by disclosing their supply

chains to public inspection are thought to be at an increased risk (e.g., trust and

reputation) of having such disclosure made by others, including competitors (for

example).

3. The larger point here is that until recently stakeholders had a limited view of a

product’s supply chain. The availability of sophisticated technology is changing this in

dramatic fashion. (The author, p. 79, refers to this as “transparency at a granular level.”)

As pointed out in the article, companies such as Wal-Mart, Tesco, and Kroger are using

such technology to “open up” their supply chains to public scrutiny. The following two

examples are offered in the assigned article:

a) Smaller generations of radio-frequency identification (RFID) tags can be

inconspicuously embedded in a product; such tags can be used directly to store

information about the product (perhaps being updated as the product moves

through its supply chain), or to point to web-links that contain (theoretically) a

vast amount of information about the product.

b) Next-generation 2D bar codes, such as the Microsoft Tag, will be able to

instantly link mobile devices to give consumers web-based access to such

things as sourcing maps for a given product, live (i.e., real-time) video capture

of manufacturing floors for the product, and detailed information regarding both

environmental and ethical certifications associated with the product.

One final point worth mentioning is the fact that data collected via sophisticated tracking

systems will provide management accountants with an incredible amount of data that

could be used to analyze a product’s durability, safety, quality, etc. In short, such data

analytics in this area could be used to support a continuous-improvement strategy of the

business.

14-77

Education.

Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and The Role of

Nonfinancial Performance Measures

Chapter 14: Check Figures

14-23 1. Sales volume variance = $1,800U; flexible budget variance, in terms of

contribution margin = $7,700U; flexible budget variance, in terms of operating

income = $9,700U; 3a. flexible budget operating income = $9,750; 3b. flexible

budget operating income = $13,350.

14-24 1. Actual operating income = $25,000; 2. master budget operating income =

2. Budgeted Gross Profit = $1,090,500; budgeted operating income = $620,150.

14-29 1. December: Standard direct labor hours per unit = 1.47015; standard direct

14-33 No check figure available.

14-34 No check figure available.

14-35 No check figure available.

14-36 1. Materials purchase-price variance = $720U; 2. Materials usage variance =

variance = $1,450U

14-39 No check figure available.

14-40 No check figure available.

14-41 No check figure available.

14-42 3. PCE, Pre-JIT = 30.77%; PCE, Post-JIT Implementation = 37.50%; 4.

Percentage improvement = 21.87% (22%, rounded).

14-78

Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and The Role of

Nonfinancial Performance Measures

total variable cost flexible-budget variance = $40,000U; 2c1. Flexible budget

14-47 No check figure available.

14-48 1a. Direct labor efficiency variance = $12,740F; 1b. Direct labor rate variance =

14-50 No check figure available.

14-51 1. Flexible budget: unit sales = 100,000; sales revenue = $500,000; contribution

14-52 No check figure available.

14-53 No check figure available.

14-54 No check figure available.