Chapter 10 – Strategy and the Master Budget

10-56 (Continued-3)

2. What additional real-life refinements would you envision for the budgets you

prepared above in (1)? What additional budgets would you anticipate preparing for

the company were you in charge of the budget-preparation process?

a) As the person in charge of the budget-preparation process, one obvious

recommended change would be to report separately the number of new policies

written (the logical offset in Part b to the number of policy cancellations). Currently

b) In the example problem we assumed, for simplicity, that all policyholders paid

the same premium. Alternatively, we used an average premium rate per month per

c) The budget we created applied to those individuals whose policies covered the

calendar year, January through December. A fuller, more realistic analysis would

d) The cancellation rate, and growth rate in new underwritings, would probably be

monitored carefully since these are key drivers of future financial performers. That

e) The problem includes information regarding a mid-term policy cancellation rate

(i.e., policies cancelled before the annual renewal date).It would seem

f) The above calculations and budgets deal solely with forecasted volume (# of

policies) and premiums revenue ($). The output of the budgets we prepared

would then be used to prepare other budgets for the company. In this sense, and

similar to the extended example in the chapter, we say that the budgets articulate

10-90

Education.

Chapter 10 – Strategy and the Master Budget

versus “complicated” claims, the average time to process a claim, the time

10-56 (Continued-4)

available per day (month) for each claims handler, the % of submitted claims that

are paid, etc. would all be “drivers” that would be incorporated into the claims-

processing budget.

g) The budget as presented is static in nature and covers a fixed period of time.

For reasons discussed more fully in the chapter, the limitations of such budgets

can be addressed by generating “rolling forecasts.”

3. The budgets you prepared above in (1) can be referred to as “driver-based

budgets.” List some of the pros and the cons of such budgets, relative to traditional

budgeting practices.

Pros

1. Driver-based budgeting (e.g., traditional activity-based budgeting (ABB) or

Time-Driven Activity-Based Budgeting) reduces the time to produce a

budget or to re-forecast.

2. Driver-based budgeting requires fewer iterations–that is, it reduces the “give

budgets.

3. Driver-based budgeting saves costs–for example, overtime payments

budget-preparation process can be reduced or eliminated. Managers are

“freed” to attend to more strategic imperatives.

non-financial information, which can be incorporate into the organization’s

Balanced Scorecard (BSC).

6. Driver-based budgeting reduces risk exposure–if performance drivers are

appropriately defined and included in the budget, then management can

7. Driver-based budgeting may decrease the amount of “gaming behavior” on

Chapter 10 – Strategy and the Master Budget

10-56 (Continued-5)

Cons

1. Driver-based budgeting is perceived to be difficult to implement.

2. Driver-based budgets require a sophisticated information processing

10-92

Education.

Chapter 10 – Strategy and the Master Budget

10-57 Budgets for a Service Firm (45-60 Minutes)

1. The annual cash budget is presented on the next page.

2. Operating problems that Triple-F Health Club could experience include:

The cash contribution from lessons and classes will decrease because the

projected wage increase for lesson and class employees is significantly greater

than the projected increases in revenues (i.e., in additional volume). Last year,

the cash generated from these operations was $39,000 ($234,000 – $195,000).

The 2018 projection is only $12,675 ($304,200 – $291,525).

Operating expenses are increasing faster than revenues from membership fees.

Last year (2017), cash generated from regular operations was $91,000

projected to increase 13%.

Triple-F Health Club seems to have a cash-management problem. The club does

not generate enough cash from operations to meet its obligations. It may not be

able to meet expenditures for day-to-day operations if the trend continues. To

avoid cash crises, the club should prepare monthly cash budgets to help cash

management.

Non-operational payments are projected to use up virtually all of the cash

generated from operations. Given the recent declines in mortgage interest rates,

management should consider refinancing this debt to reduce this cash drain.

3. Jane Crowe’s concern with regard to the Board’s expansion goals is justified. The

2018 budget projections show only a minimal increase in the cash balance (i.e., an

increase of only $2,757). The total cash available is well short of the $60,000 annual

10-93

Education.

Chapter 10 – Strategy and the Master Budget

10-57 (continued)

TRIPLE-F HEALTH CLUB

Cash Budget

For the Year Ending October 31, 2018

Price

2017 Growth Increase 2018

Operating Cash Inflows:

Annual membership fees $355,000 3.0% 10.0% $402,215

Lesson and class fees 234,000 30.0% 304,200

Miscellaneous 2,00033.33% 2,667

Total Operating Cash Inflows $591,000 $709,082

Operating Cash Outflows:

Manager’s salary and benefits $36,000 15.0% $41,400

Employee wages and benefits:

Payoff of outstanding A/P N/A given 2,500

Total Operating Cash Outflows $461,000 $603,925

Net Operating Cash Flow $130,000 $105,157

Non-Operating Cash Outflows:

Payoff of equipment payable given $15,000

Mortgage principal given 30,000

Mortgage interest 32,4001

Planned equipment purchases given 25,000

Total Non-Operating Cash Outflow $102,400

10-94

Chapter 10 – Strategy and the Master Budget

10-58 Budgeting and Sustainability (75 minutes)

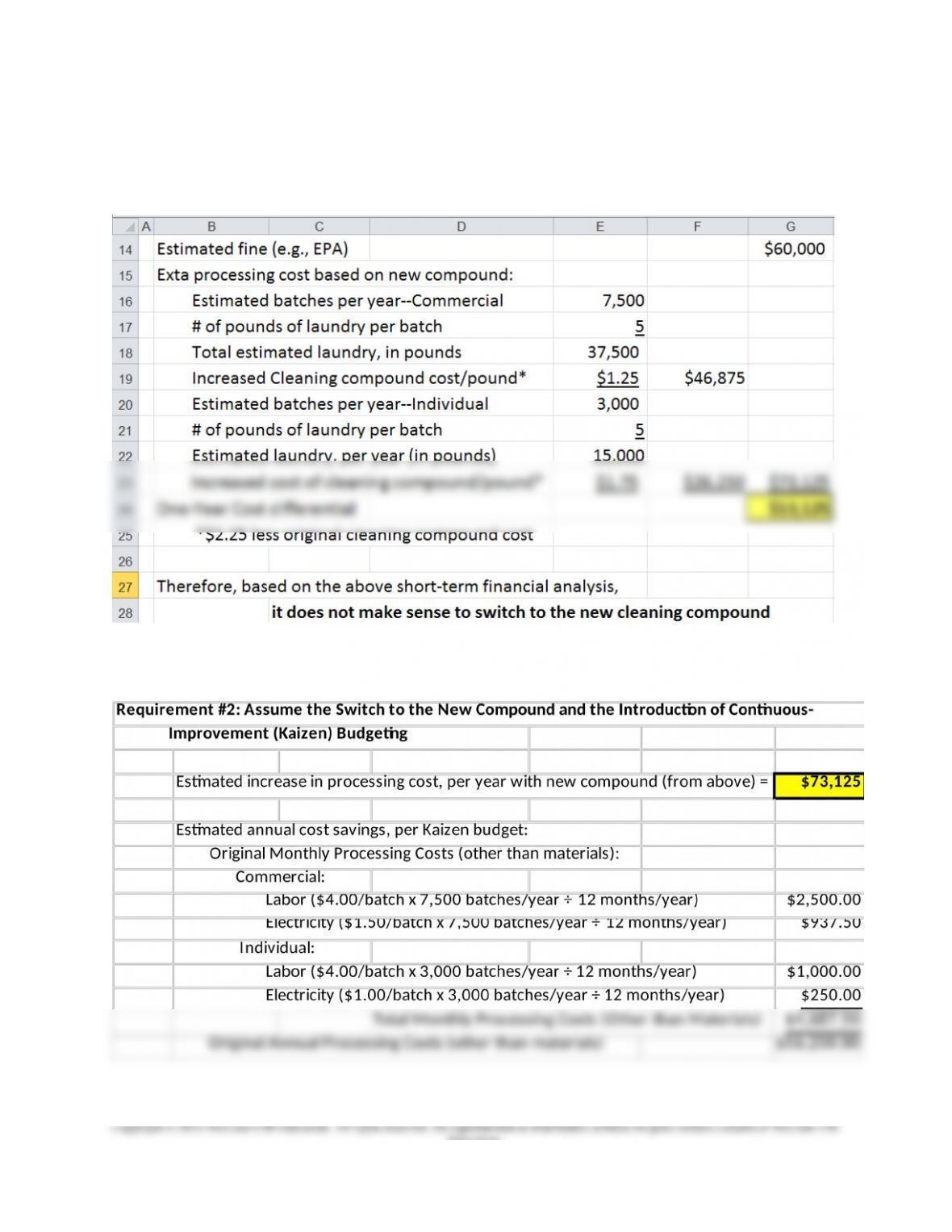

Requirement 1: Short-Term Financial Analysis

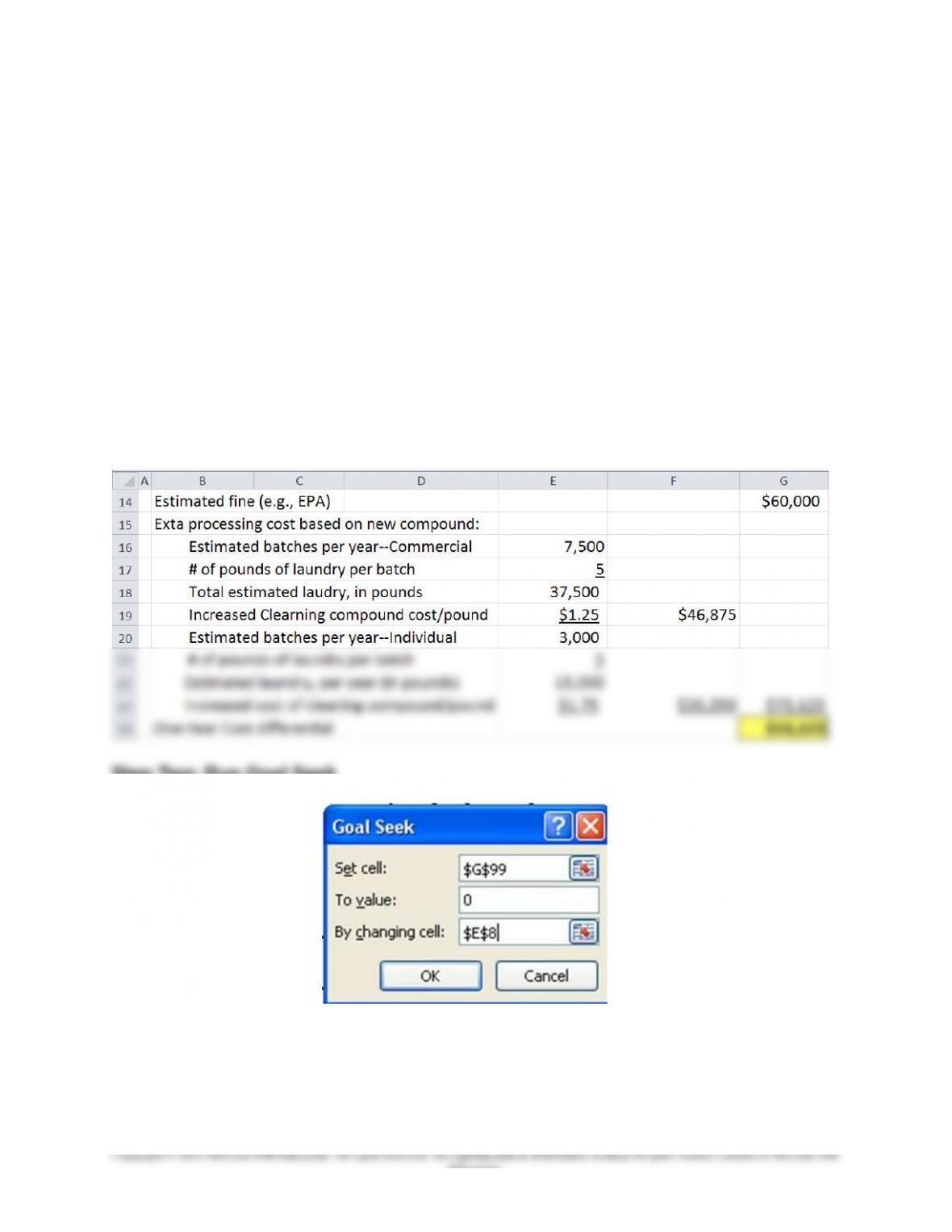

For purposes of illustration (and for Requirement 3 below), the cell reference for

$13,125 (above) is G24; the cell reference for $60,000 (above) is G14.

10-95

Education.

Chapter 10 – Strategy and the Master Budget

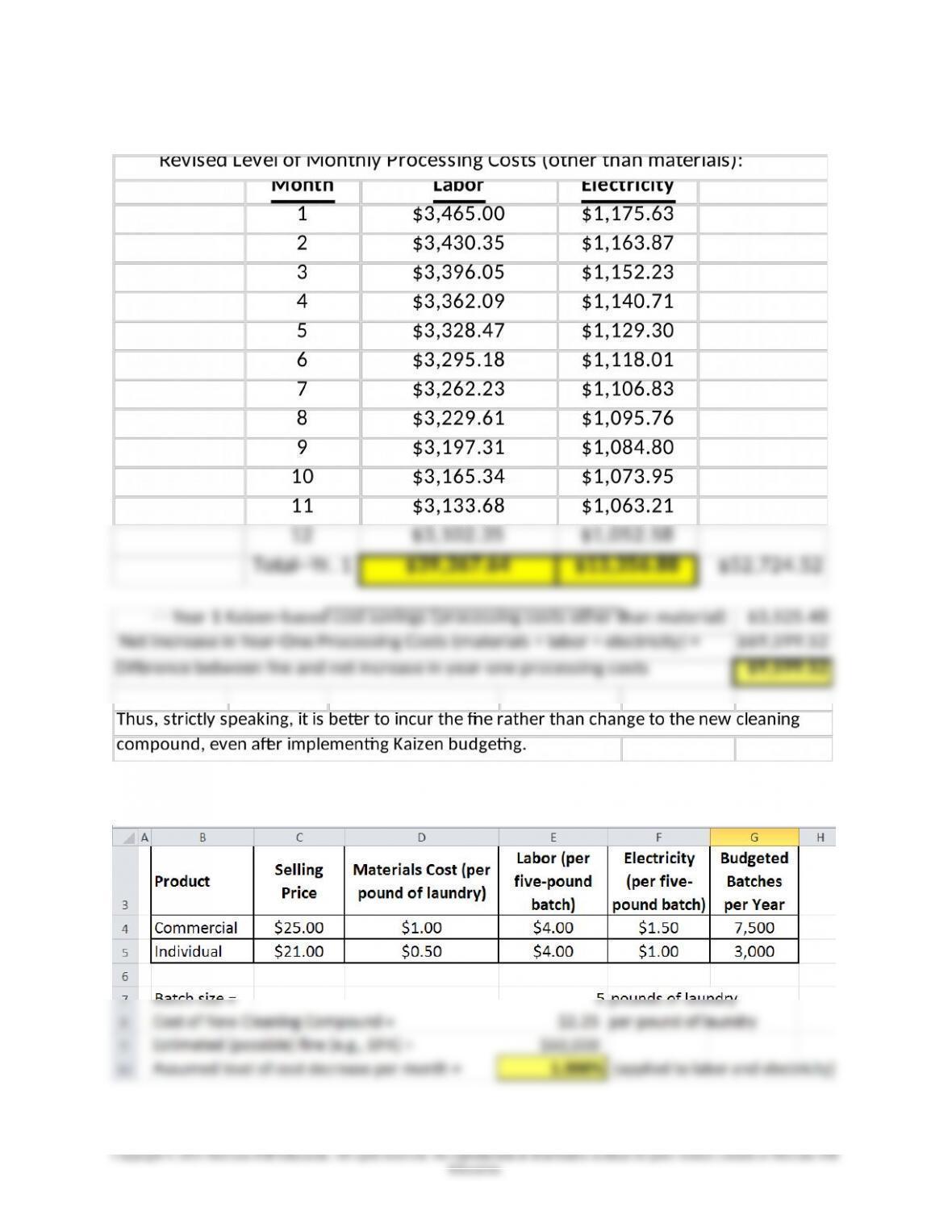

Cell references: $73,125 = cell G32 (=G23); $4,687.50 = cell G42 (=SUM(G37:G41));

$56,250.00 = cell G43.

10-96

Education.

Chapter 10 – Strategy and the Master Budget

10-58 (Continued-1)

For requirement 3 (below), assume the following input data:

10-97

Chapter 10 – Strategy and the Master Budget

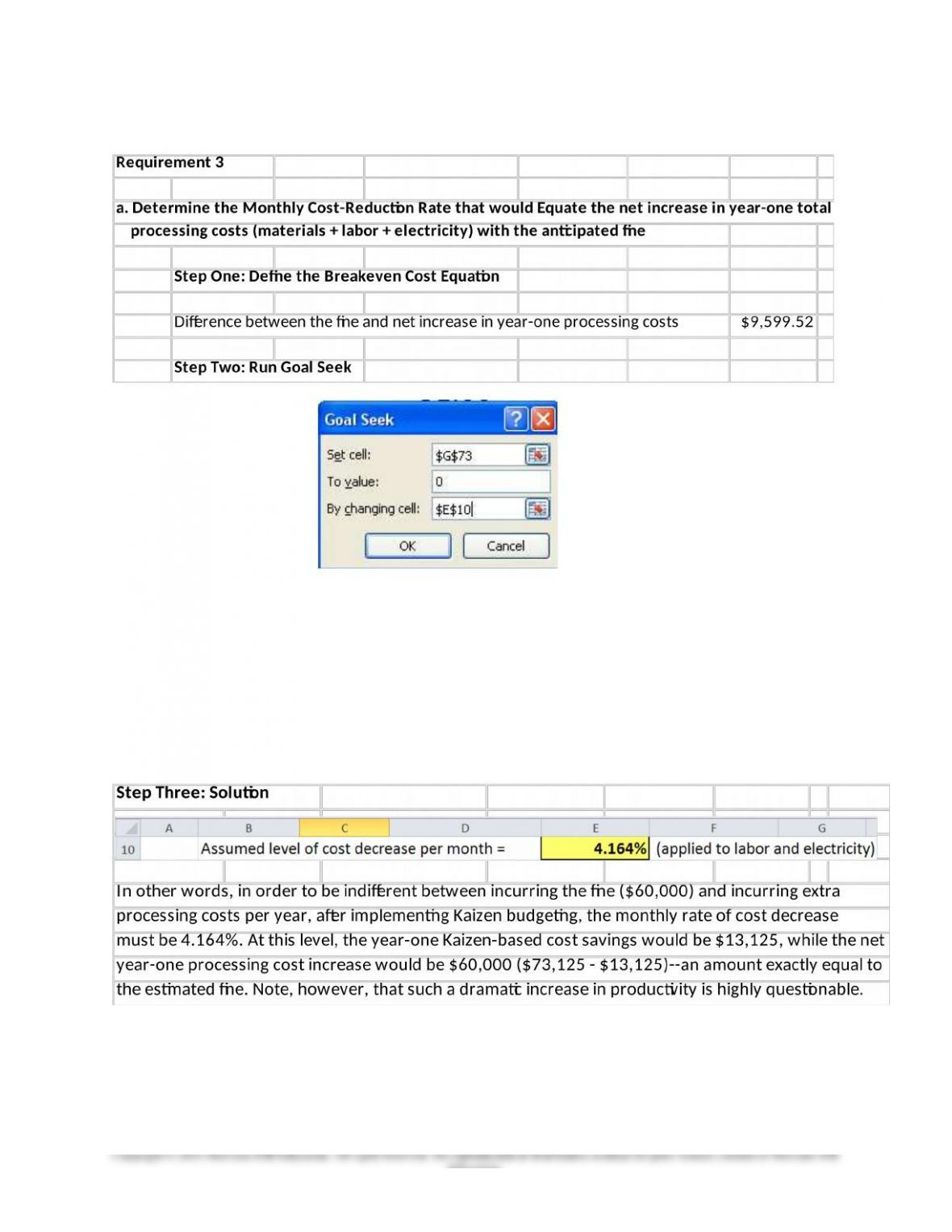

10-58 (Continued-2)

Note: cell E10 contains the assumed monthly rate of cost decrease; cell G73

contains arithmetic difference between the cost of the fine and the net increase in

processing costs—other than materials cost, and after implementing Kaizen

budgeting. The value “0” in the above formulation essentially solves for the

breakeven level: that is, the rate of monthly cost savings needed to equate the

value of the fine and the increased processing costs due to the new compound, but

after implementing Kaizen. As shown below, Goal Seek provides the answer:

4.164% per month.

10-98

Education.

Chapter 10 – Strategy and the Master Budget

10-58 (Continued-3)

b. The cost per pound for the new compound that would equate the anticipated fine with

the net year-one costs, assuming no Kaizen budgeting plan (i.e., no reduction per

month in processing costs):

Step One: Set Up the Cost Equation

Cost differential: anticipated fine and net one-year processing costs, with no Kaizen

budgeting plan = $13,125

Note: the above value is contained (in this example) in cell G99, which in turn is

defined as the contents from cell G24. G24 contains the difference between the

anticipated cost of the fine, $60,000 (entered in cell G14) and the expected increase

in material cost associated with the use of the new compound (G23), as shown

below:

Step Two: Run Goal Seek

10-99

Education.