Chapter 17 – The Management & Control of Quality

Chapter 17

The Management & Control of Quality

Teaching Notes for Cases

Case 17-1: Precision Systems, Inc.

This case illustrates that quality cost information can play an important role in alerting top management

about the importance of quality improvement in a non-manufacturing department of a manufacturing

firm. The case is based on the following article:

Kalagnanam, S. S., and E. M. Matsumura, “Cost of Quality in an Order-Entry Department,” Journal

of Cost Management (Fall 1995), pp. 68-74.

The required questions are designed to acquaint students with some of the terminology of “cost of

quality” and some aspects of conducting a cost of quality study. Quality costs, defined as those that arise

because poor quality may exist or does exist, have been classified into the following four categories:

Prevention (prevention of poor quality, or quality assurance);

Appraisal (inspection and testing);

Internal Failure (costs, such as rework or scrappage, for nonconforming products identified

before delivery to customers);

External Failure (costs, such as warranty expenses or freight charges, for nonconforming products

delivered to customers).

This case focuses on prevention activities (see question 6), as well as internal failure and external failure

costs for the order entry department at Precision Systems, Inc. Internal and external failures are defined

with respect to the order entry department.

Additional readings on quality costs:

Kaplan, R. S. and A. A. Atkinson, Advanced Management Accounting, 2nd ed. (Englewood Cliffs,

NJ: Prentice-Hall, Inc., 1989), chapter 10.

Morse, W. J. and H. P. Roth, “Why Quality Costs are Important,” Management Accounting,

November 1987, pp. 42-43.

Scholtes, P. R., L. S. Weiss and S. Reynard, Quality Improvement in the Office (Madison, WE Joiner

Associates, Inc., 1988).

Schonberger, R. S., “Total Quality Management Cuts a Broad Swath,” Organizational Dynamics

(Spring 1992), pp. 116-27.

Suggested Solutions to Required Questions

1. Describe the role that assigning costs to order-entry errors played in quality improvement

efforts at Precision Systems, Inc.

17-1

Chapter 17 – The Management & Control of Quality

This question is designed to help students recognize how cost management systems can interface with

quality improvement efforts. As the case states, in spite of PSI’s commitment to quality improvement,

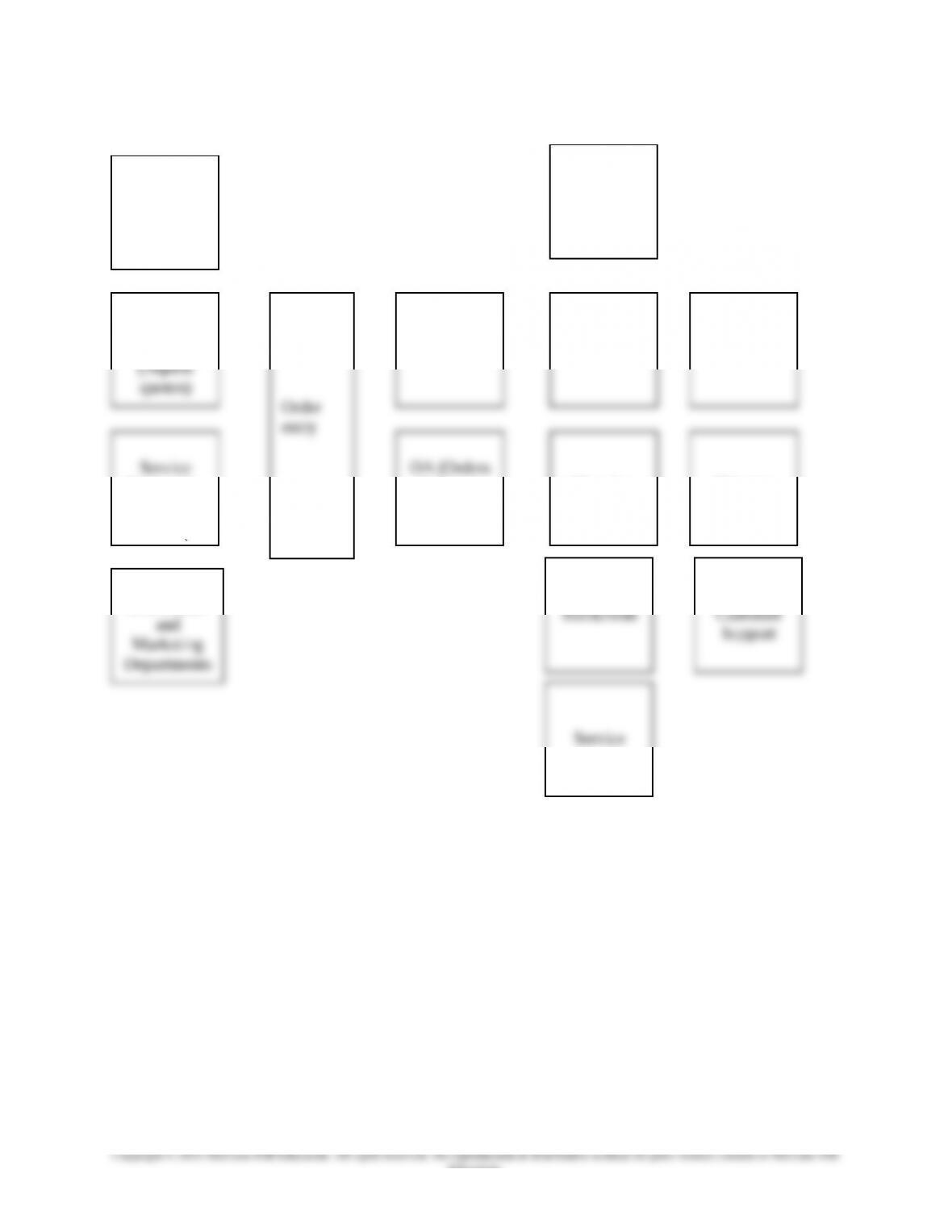

2. Prepare a diagram illustrating the flow of activities between the order entry department and its

suppliers, internal customers (those within PSI), and external customers (those external to

PSI).

There are many possible flows. For example, a sales representative may contact order entry to request

a quote for a system for a customer. Subsequently, the customer order entry to place the order; order

entry then generates and order acknowledge, which is sent to manufacturing, invoicing, and sales

administration. Once the system has been shipped, an invoice is sent to the customer. Ultimately,

service would result in an order acknowledgement being sent to the service department.

17-2

Education.

Chapter 17 – The Management & Control of Quality

SUPPLIERS PROCESS OUTPUT CUSTOMERS

17-3

Education.

Sales

Admini-

stration

Customers

(place

orders)

CollectionsInvoicingQuote

Sales

Representa-

tives

ShippingManufac-

turing

Acknow-

ledgement)

Representa-

tives

quotes)

Technical

Information

Chapter 17 – The Management & Control of Quality

3. Classify the failure items in Exhibit 1-1 into internal failure (identified as defective before

delivery to internal or external customers) and external failure (nonconforming “products”

delivered to internal or external customers) with respect to the order entry department. For

each external failure item, identify which of order entry’s internal customers (i.e., other

departments within PSI that use information from the order acknowledgment) will be affected.

Items 1, 2, 5, 8, 19 and 12 are internal failures; the remaining are external failure items. Internal

customers affected by external failure items are listed below.

Item Number Internal Customer(s) Affected

3 Manufacturing, service, stockroom, invoicing

4 Invoicing, accounting (profitability analysis)

Incorrect sales rep. Code Sales administration

4. For the order-entry process, how would you identify internal failures and external failures?

Who would be involved in documenting these failures and their associated costs? Which

individuals or departments should be involved in making improvements to the order entry

process?

An initial step would be to interview employees in order entry, as well as its suppliers and internal

customers. Based on the interviews, data collection forms can be developed. For internal failures,

5. What costs, in addition to salary and fringe benefits, would you include in computing the cost

of correcting errors?

Possible responses include the following:

Office equipment and office space

Telephone (to clarify problems)

Computer costs (making changes on the computer)

17-4

Education.

Chapter 17 – The Management & Control of Quality

Scrappage of returns

6. Provide examples of incremental and breakthrough improvements that could be made in the

order entry process. In particular, identify prevention activities that can be undertaken to

reduce the number of errors. Describe how you would prioritize your suggestions for

improvement.

Students can brainstorm about possible improvements during a class discussion. Possible responses

include:

Incremental Improvements

Empower employees

Allow sales representatives to correct errors without approval.

Urge order entry to improve communication with manufacturing and other departments.

Provide feedback to order entry on types of errors, numbers of errors, and cost impact.

Daily, by computer (suggestions for improvement)

Educate sales representatives about effects of errors and about the process.

Provide better training for sales representatives.

Train sales representatives to develop accurate quotes and take on the order entry function.

Have sales representatives take responsibility for the process.

Track customer purchases to improve service to customers.

Survey customers about problems; use the responses to prioritize problems.

Stop the double-entry of information.

Get input from order entry on development of forms.

Implement checking in order entry to help prevent order acknowledgement errors.

Develop a reward system that motivates error-free performance of sales reps. and order entry.

Benchmark.

Breakthrough Improvements

Develop a computer system to decrease the number of times data are entered.

Develop a spreadsheet or computer program to check for inconsistencies between P.O. and quotes.

Check for duplication of orders.

Check prices.

Develop a computer system that allows sales representatives to prepare accurate quotes.

Install a computer system linking order entry, manufacturing, invoicing, etc.

Use cross-functional teams to manage “large” costs or different segments.

Develop a system that allows parts customers to get their own quotes on-line.

Incremental Improvements Made by PSI

1) Key information for quotes is now obtained up-front by the sales representative; earlier, the sales

representative faxed partial information to order entry and requested a quote. Order entry staff

then spent a great deal of time obtaining missing information. With this change, the sales

representative cannot request a quote until he/she has supplied key information to order entry

staff. This could be considered a prevention activity.

17-5

Education.

Chapter 17 – The Management & Control of Quality

2) Customers are asked to include quotation numbers on their purchase orders. This allows PSI to

match orders with quotes and avoid duplication in manufacturing. PSI prepares its manufacturing

plan based on the quotes received because they have a reasonably good idea of which ones are

likely to become firm orders.

3) Proper tools are provided to the order entry staff:

Procedure manuals.

Guidelines for sales discounting. Prior to this, the order entry staff had to call sales to seek

clarifications regarding discounts.

Printed configuration guides that contain information in the format that order entry requires.

Prior to this, the formats did not always match.

4) Order-entry staff members are now responsible for both quotes and orders. Previously, some staff

members were responsible for only quotes, and other staff members were responsible only for

orders. This change had an immediate impact, as the person who prepared a quote now had

responsibility for processing the subsequent order.

5) A regular feedback system is now in place. Each internal customer department provides feedback

to order entry once every quarter.

Benefits: Cycle time for preparing quotes was reduced by 60% and cycle time for processing orders

was reduced by 50%. Also, order entry staff experienced greater pride in their work.

Breakthrough Improvement Efforts by PSI as of 1993

Many of these improvements are prevention activities.

1) PSI began working with a vendor to develop an on-line configurator that would configure their

standard systems (order entry staff would avoid keying-in part numbers).

2) PSI planned to acquire a new, more integrated order entry system that can communicate with the

configurator and turn a quote into an order acknowledgement when the order comes in. The

system will also be able to generate an invoice, thereby avoiding re-keying the information.

3) PSI began working towards providing sales representatives with a laptop computer equipped with

a built-in configurator. This will allow them to prepare quotes in the field.

The anticipated benefits include a reduction in errors caused by incorrect or duplicate part numbers,

and a reduction in cycle time for preparing quotes or processing orders and preparing invoices.

Prioritizing Improvement Activities

Three considerations in prioritizing improvement activities are the perceived seriousness of the

problems, the benefits of improvements, and the costs of the improvements. In this case study, the

breakthrough improvement projects involve higher costs than the incremental improvement efforts.

To identify the most serious problems, a Pareto analysis can be performed.

In PSI’s case, correcting order acknowledgement errors became the highest priority because of its

associated cost of 7% of the salary and fringe benefits budget (see Exhibit 2).

17-6

Education.

Update: Improvement Efforts by PSI as of 1996

The first incremental improvement, a stringent policy of sales representatives filling out quote forms

correctly, was abandoned because the forms quickly became obsolete and the policy was unpopular

with sales representatives. In addition, the policy slowed the quotation process.

The initial vendor’s quote for the desired configurator was judged unaffordable. After an 18month

search, however, PSI was able to purchase a new integrated information system (including materials

resource planning and accounting) that included a configurator. In the meantime, PSI developed an

in-house configurator program that runs on the sales representatives’ laptop computers. As a

consequence, problems with missing, incorrect, or changed part numbers have been greatly reduced.

Information on part numbers originates in manufacturing, and is maintained and kept current by the

marketing department. A change from line-item pricing (listing each component part with its

associated price) to bundling (listing the component parts but providing only a bottom-line price)

reduced processing time because customers previously would call for verification if any one of the

component prices on the invoice differed from what appeared on the quote.

The current cycle typically runs as follows:

Sales representative prepares a quote using laptop computer configurator and emails it to order

entry;

Order entry reviews the quote and sends a quote packet to send to the customer (Pricing on quote

is reviewed by order entry supervisor);

When the customer’s order is received by order entry, the order is entered into PSI’s system

configurator; the order entry supervisor approves the order;

The controller approves the order;

The order acknowledgement is transmitted electronically to manufacturing; Manufacturing builds

the product;

The product is shipped;

The invoice is generated the same day the product is shipped, with no further review.

7. What nonfinancial quality indicators might be useful for the order entry department? How

frequently should data be collected or information be reported? Can you make statements

about the usefulness of cost-of-quality (COQ) information in comparison to nonfinancial

indicators of quality?

Nonfinancial indicators that might be useful in improving quality in the order entry department

include: 1) The frequency of the different types of errors; 2) Time spent on correcting problems.

Frequency of reporting is an important issue when implementing a COQ system. Options for

frequency of tracking data and reporting include:

1) Keep track of the information on a daily basis but report monthly. Continue doing this until

improvements are made and the information is no longer needed. The assumption is that

continuous improvement projects will be undertaken to rectify the situation.

2) Collect sample data for a specified period once every quarter or six-month period, for

example, and assess the changes in the magnitude of problems. The assumption is that results

from the sample data will be used to make process improvements.

17-7

Chapter 17 – The Management & Control of Quality

COQ information is useful for the following reasons:

1) COQ quantifies the financial impact of the errors/problems, thereby providing a universally

understood method of assessing the seriousness of the situation. As emphasized in question 1,

COQ figures can play an important role in alerting top management to the seriousness of

quality problems overall or in a particular area.

2) Quality cost systems cut across departmental boundaries, thereby providing a holistic

measure of the benefits derived from improvement efforts.

COQ information should be used in conjunction with nonfinancial indicators, as the latter provide

the information actually required for making changes to the system.

17-8

Education.

Chapter 17 – The Management & Control of Quality

Case 17-2: Kelsey Hospital

The purpose of this case is to have students analyze and categorize costs of quality (COQ) in a nonprofit

health care setting. The case describes the need for a quality costing system in a hospital and the

development of such a system for two primary treatments (intubation and bronchodilator treatments)

performed in the Respiratory Therapy Department of the hospital. A list of items pertaining to quality

costs is presented and described for analysis, estimation, and categorization.

Teaching Notes

In recent years, companies have realized that to be globally competitive, they must focus on the quality of

their products and services. Traditionally, the costs relating to quality have been buried in other cost

categories (i.e., administrative overhead). To evaluate the costs and benefits of efforts to enhance quality

and also to better control costs relating to quality, the quality costs need to be segregated and properly

measured. Therefore, many companies have established cost of quality systems. Cost classification is an

important aspect of these systems because different categories are controlled differently, some categories

are more serious in terms of future consequences than others, and investment in certain categories is

believed to greatly reduce those in other categories.

Determining and measuring costs of quality in a service organization are especially challenging.

Manufacturing companies can inspect their products before delivery to customers and quality can be

assessed visually or by the use of instruments. In contrast, service organizations cannot assess quality until

after the service is rendered and measuring instruments are usually of no use because physical

measurements are not applicable. Hence, it is much more difficult to determine and measure the costs of

quality in a service organization than in a manufacturing firm.

Manufacturing cost of quality cases have been written in settings such as electronics1 and paper mills.2 The

issues covered in these manufacturing cases are similar to those in the Kelsey Hospital case study, but how

the costs are determined and measured in the service setting are more complex. With products, one can

assess the quality of materials, the quality of product design, and the conformance to product

specifications. In service settings, however, one is usually assessing quality associated with intangible

items, making it a more nebulous exercise to measure quality costs.

At least one service case exists in the context of a railroad3 and involves the use of quality costs relating to

environmental management. Kelsey Hospital also differs from most other manufacturing and service

settings in that consideration needs to be given to quality perceptions of an outside customer group–third

party payers. Furthermore, because health care organizations deal with human lives, quality is even more

paramount than in most other types of organizations.

The Kelsey Hospital case involves the analysis and categorization of quality costs in a nonprofit service

setting. The case is based on an actual hospital’s experience with developing a cost of quality program,

although all names in the case are fictional. The case largely involves opinionated discussion. The learning

objectives for the case are as follows:

1 Examples are: Signetics Corporation: Implementing a Quality Improvement Program (A), Stanford University,

1982; Texas Instruments: Cost of Quality (A), Harvard Business School, 1988.

2 Iron River Paper Mill, in Anthony, R. N. and V. Govindarajan, Management Control Systems, Irwin/McGraw-Hill,

1998, pp. 646-655.

3 Union Pacific Railroad: Using Cost of Quality in Environmental Management, Institute of Management

Accountants (IMA), 1997.

17-9

Education.

Chapter 17 – The Management & Control of Quality

1. To help students understand different “customer” groups’ concerns and perceptions about quality;

2. To help students understand the nature of the four cost of quality categories and its application in a

health-care setting;

3. To help students understand how to measure costs of quality (COQ);

4. To help students understand how COQ measures can fit into a balanced scorecard (BSC).

Students should have had prior exposure to some elementary material on costs of quality from either a

cost/managerial accounting textbook4 or journal article.5 The case is appropriate for both undergraduate

and graduate cost or managerial accounting courses. This case can be covered in a 50-minute class period.

Kelsey Hospital has been used several times in undergraduate introductory managerial accounting classes

immediately after textbook material on costs of quality has been covered. Lively discussions have ensued

about customer perceptions and how to categorize the various costs. Drawing out additional quality costs

from the students (particularly the undergraduate ones) can be challenging and it may be necessary to give

some hints to them. Like most cases, when students are asked to turn in write-ups on this case prior to

class discussion, there is a greater level of preparation than otherwise and this improves the quality of

class discussion. However, because the case does not have complex technical accounting issues and

contains no number crunching, it does not require a lot of advance preparation for students to

meaningfully discuss the case. In fact, on one occasion, students were given 15 minutes of class time to

read the case and the resulting class discussion was rather good. Students have reported that the case

helps them better appreciate and understand costs of quality because they see it applied in a setting that

they are familiar with rather than an obscure factory setting. While it may seem that some of the medical

terminology would be unfamiliar to students, they seem to absorb it well from the case. Furthermore,

class discussions tend to be centered around basic health-care issues and not medical complexities.

Suggested solutions for the assignment questions are as follows:

1. What groups and individuals are the “customers” of the respiratory therapy department?

Describe the concerns and perceptions about quality that might differ across the different types

of customer. Identify the problems that the different customers would want quality control to

prevent, detect, or correct.

Various “customer” groups include:

Different types of customers may have different perspectives on the quality of services they receive

and may react differently to a given level of performance. Often, a patient cannot evaluate the quality

of clinical treatment received. Most patients can only assess the quality of their treatment based on

4 Examples are: Barefield, J.T., C.A. Raiborn, and M.R. Kinney, Cost Accounting: Traditions and Innovations,

Southwestern, 2003, pp. 310-321; Horngren, C.T., S.M. Datar, and G. Foster, Cost Accounting: A Managerial

Emphasis, Prentice-Hall, 2003, pp. 654-663.

5 Examples are: Carr, L.P., “Cost of Quality—Making It Work,” Journal of Cost Management, Spring 1995, pp. 61-

65; Kalagnanam, S. S. and E. M. Matsumura, “Cost of Quality in an Order-Entry Department,” Journal of Cost

Management, Fall 1995, pp. 68-74.

17-10

Education.