Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15-31 Three-Variance Factory Overhead Analysis (40 minutes)

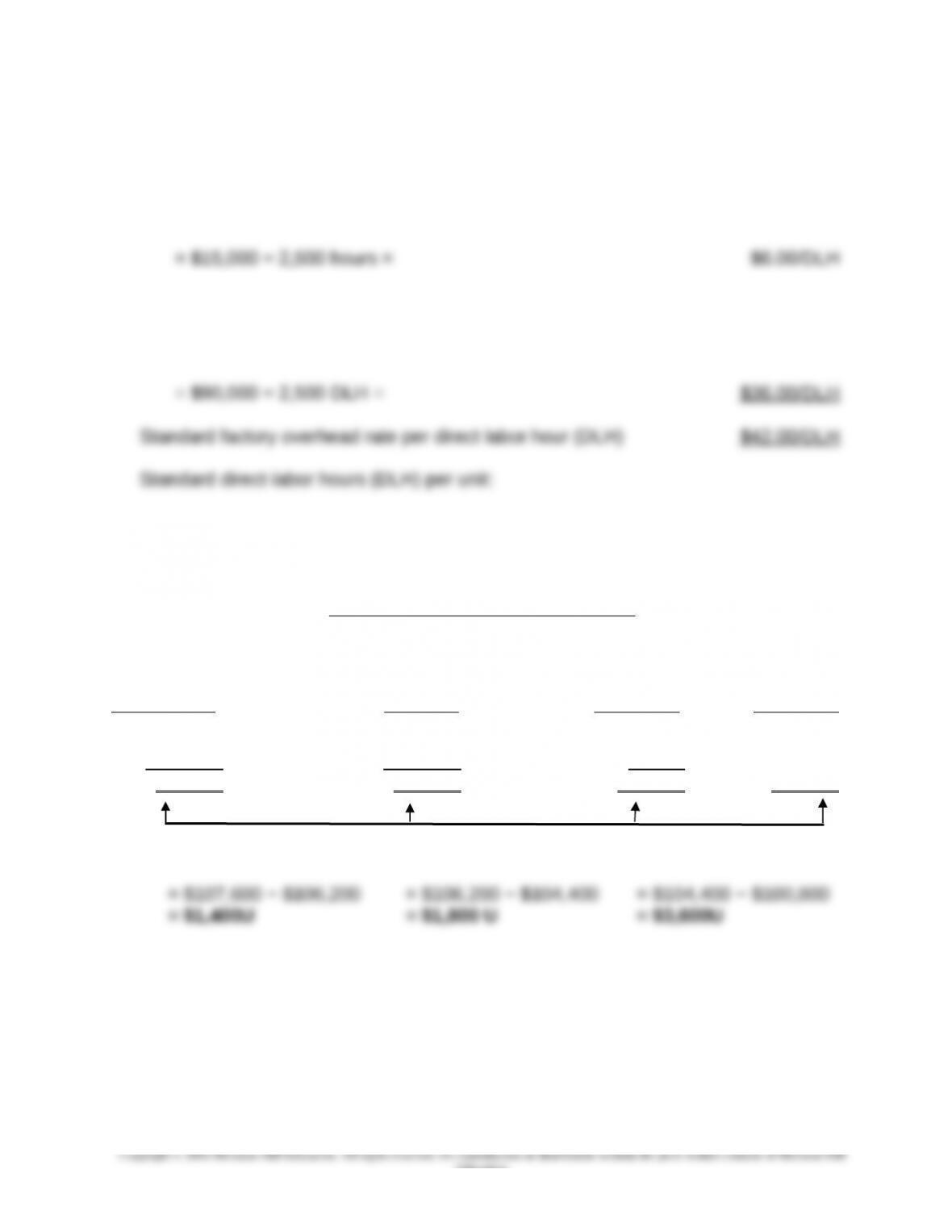

1. Standard variable factory overhead rate per direct labor hour (DLH):

= Budgeted Total Variable Factory Overhead ÷ Budgeted Total Direct Labor Hours

Standard fixed factory overhead rate per DLH:

= Budgeted Total Fixed Factory Overhead ÷ Practical Capacity Labor Hours

= Practical Capacity Labor Hours ÷ Practical Capacity, in Units = 0.5 DLH/unit

Three-Variance Overhead Analysis

Flexible Budget Flexible Budget

Based on Inputs Based on Output Applied

Actual Cost AQ × SP (SQ × SP) (SQ × SP)

$ 15,600 2,700 × $6 = $ 16,200 2,400 × $6 = $14,400

+ 92,000 + 90,000 + 90,000 2,400 × $42

$107,600 $106,200 $104,400 = $100,800

Spending variance Efficiency Variance Production Volume

Variance

15-21

Education.

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15-31 (Continued)

2. Total overhead spending variance = variable overhead spending variance + fixed

overhead spending variance

Total overhead efficiency variance = variable overhead efficiency variance

the overhead variance)

In sum, the only difference between the three-way and four-way analysis is that in the

former, the spending variances for fixed and for variable overhead (reported in the

latter) are combined into a single overhead spending variance.

Three- and Four-Variance Factory Overhead Analysis: Summary

Overhead Spending Variance:

Variable Overhead Spending Variance $ 600F

Fixed Overhead Spending Variance 2,000U $1,400U

Overhead Efficiency Variance:

Variable Overhead Efficiency Variance $1,800U

15-22

Education.

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15-32 Two-Variance Analysis of the Total Overhead Variance (40 minutes)

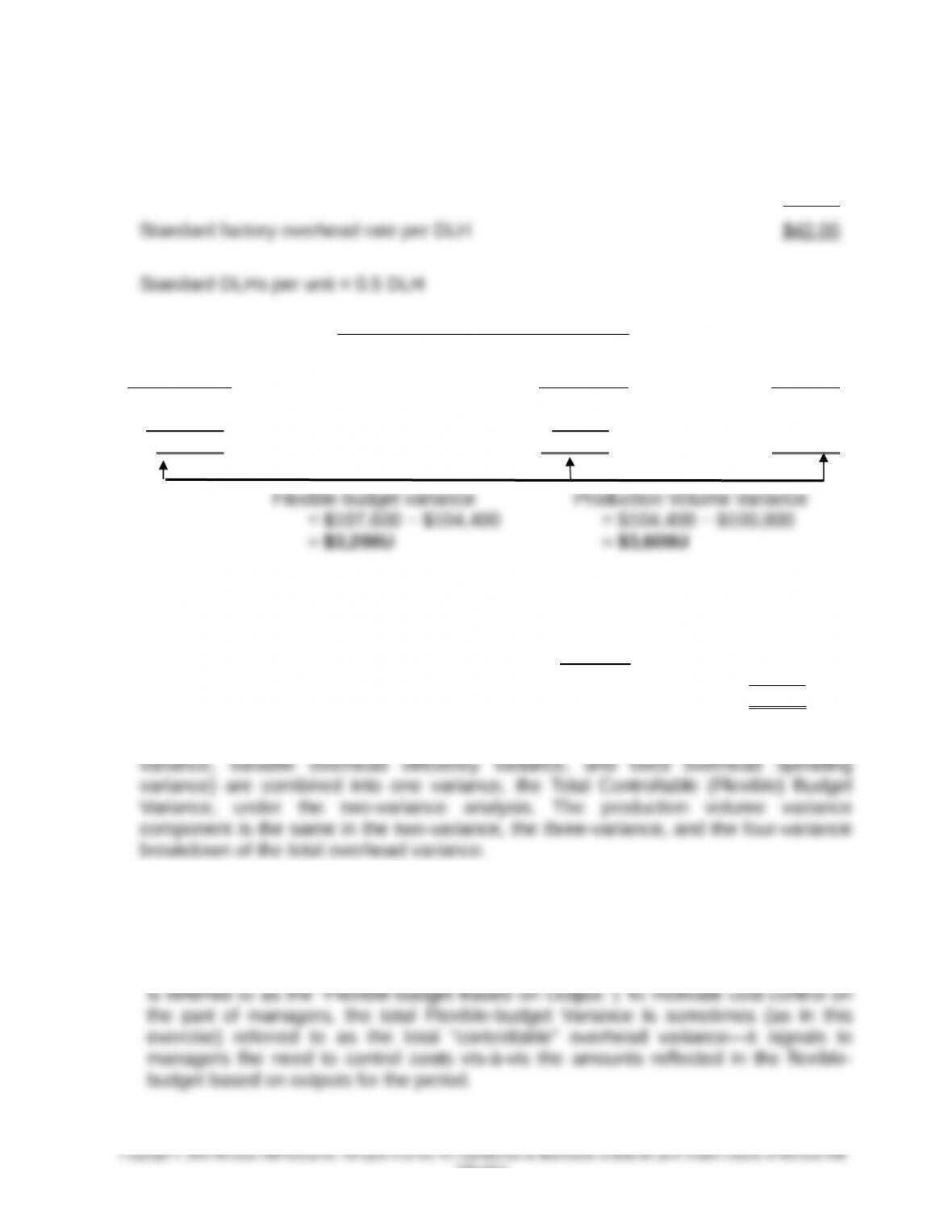

1. Standard variable factory overhead rate per direct labor hour (DLH) $ 6.00

Standard fixed factory overhead rate per DLH 36.00

Two-Variance Overhead Analysis

Flexible Budget Based Overhead

Actual Cost on Output Applied

$ 15,600 2,400 × $6 = $14,400

+ 92,000 + 90,000 2,400 × $42

$107,600 $104,400 = $100,800

2. Total Controllable (Flexible) Budget Variance for Overhead:

a) Variable Overhead Spending Variance $ 600F

b) Variable Overhead Efficiency Variance $1,800U

c) Fixed Overhead Spending Variance $2,000U $3,200U

Production Volume Variance 3,600 U

Total Overhead Variance $6,800U

That is, three items from the four-variance analysis (viz., variable overhead spending

3. The two-variance breakdown of the total overhead variance reports two important

factors concerning overhead costs. The flexible-budget (controllable) variance

measures the difference between the actual overhead incurred and the overhead that

should have been incurred based on the actual output of the period. (This latter term

15-23

Education.

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15-32 (Continued)

The production volume variance, when the fixed overhead application rate is based

on practical capacity, reports the effectiveness of the organization in using available

15-24

Education.

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15-33 Factory Overhead Analysis–Two, Three, and Four Variances; Spreadsheet

Application (60 Minutes)

1. Total Factory Overhead Application Rate:

Fixed factory overhead application rate:

Total machine hours at practical capacity:

Number of units of output at practical capacity = 40,000

Machine hours per unit × 2

Standard machine hours @ practical capacity 80,000

Fixed factory overhead rate per machine hour = budgeted

2. Total Flexible Budget (FB) for Overhead Based on Units Produced :

Total standard machine hours allowed for the units produced =

42,000 units produced × 2 machine hours per unit = 84,000 hours

Manufacturing overhead in the flexible budget for 42,000 units:

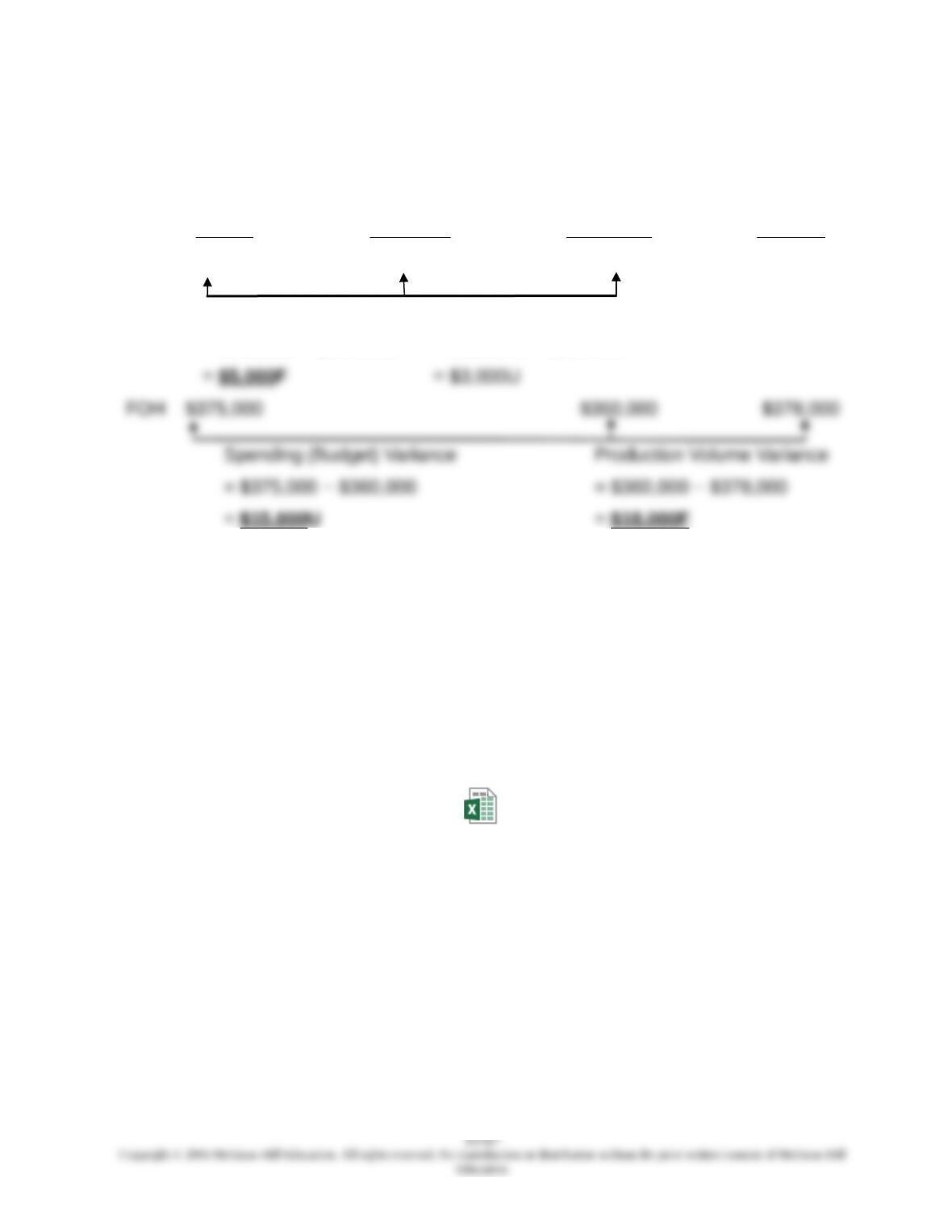

3. Production Volume Variance for 2016:

Fixed Overhead:

Actual Cost Budget Applied

15-33 (Continued-1)

or, Production Volume Variance = SP × (Denominator Volume − SQ)

15-25

Education.

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

= $4.50/machine hr. × (80,000 − 84,000) machine hours

= $18,000F

4. and 5.

FB Based on FB Based on

Actual Inputs Output Applied

VOH $3 × 85,000 hrs. $3 × 84,000 hrs. $3 × 84,000 hrs.

= $255,000 = $252,000 = $252,000

FOH $4.50 × 84,000 hrs.

360,000 360,000 = 378,000

Total factory overhead incurred $625,000

FB for Overhead Based on Inputs (i.e., actual machine hours):

Variable factory overhead: 85,000 mach. hrs. × $3/hour = $255,000

Fixed factory overhead (“lump-sum” amount): 360,000 615,000

Factory overhead spending variance $ 10,000U

FB for Overhead Based on Inputs (i.e., actual machine hours) $615,000

15-26

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15-33 (Continued-2)

FB Based FB Based

on Inputs on Outputs

6. Actual (AQ × SP) (SQ × SP) Applied

VOH $250,000 $255,000 $252,000

Spending Variance Efficiency Variance

= $250,000 − $255,000 = $255,000 − $252,000

An Excel spreadsheet solution file for this assignment is embedded below. You can

open this “object” by doing the following:

1. Right click anywhere in the worksheet area below.

2. Select “worksheet object” and then select “Open.”

3. To return to the Word document, select “File” and then “Close and return

to…” while you are in the spreadsheet mode. The screen should then return

you to this Word document.

Ex. 15-33 7e.xlsx

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

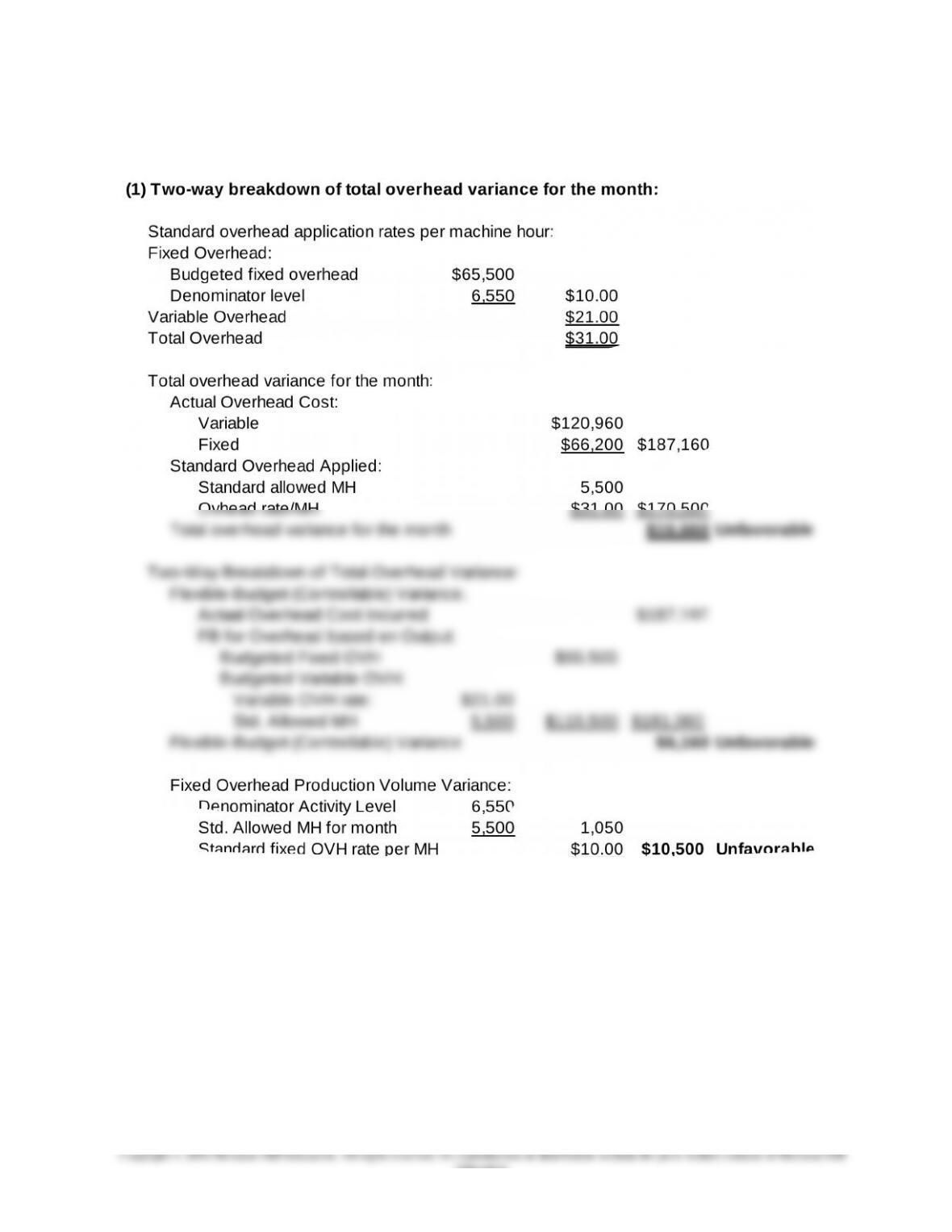

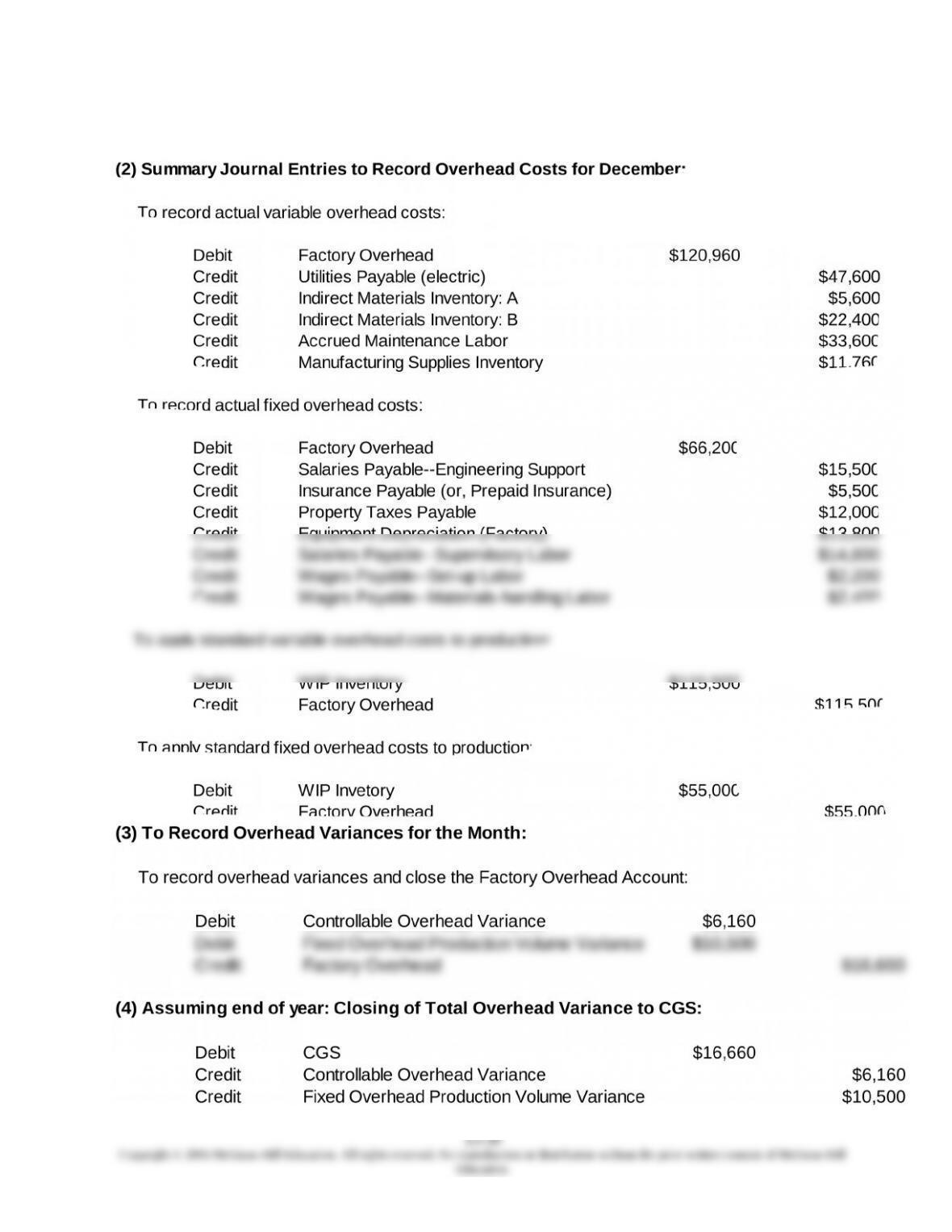

15-34 Journal Entries for Factory Overhead Costs and Standard Cost Variances;

Spreadsheet Application (60 minutes)

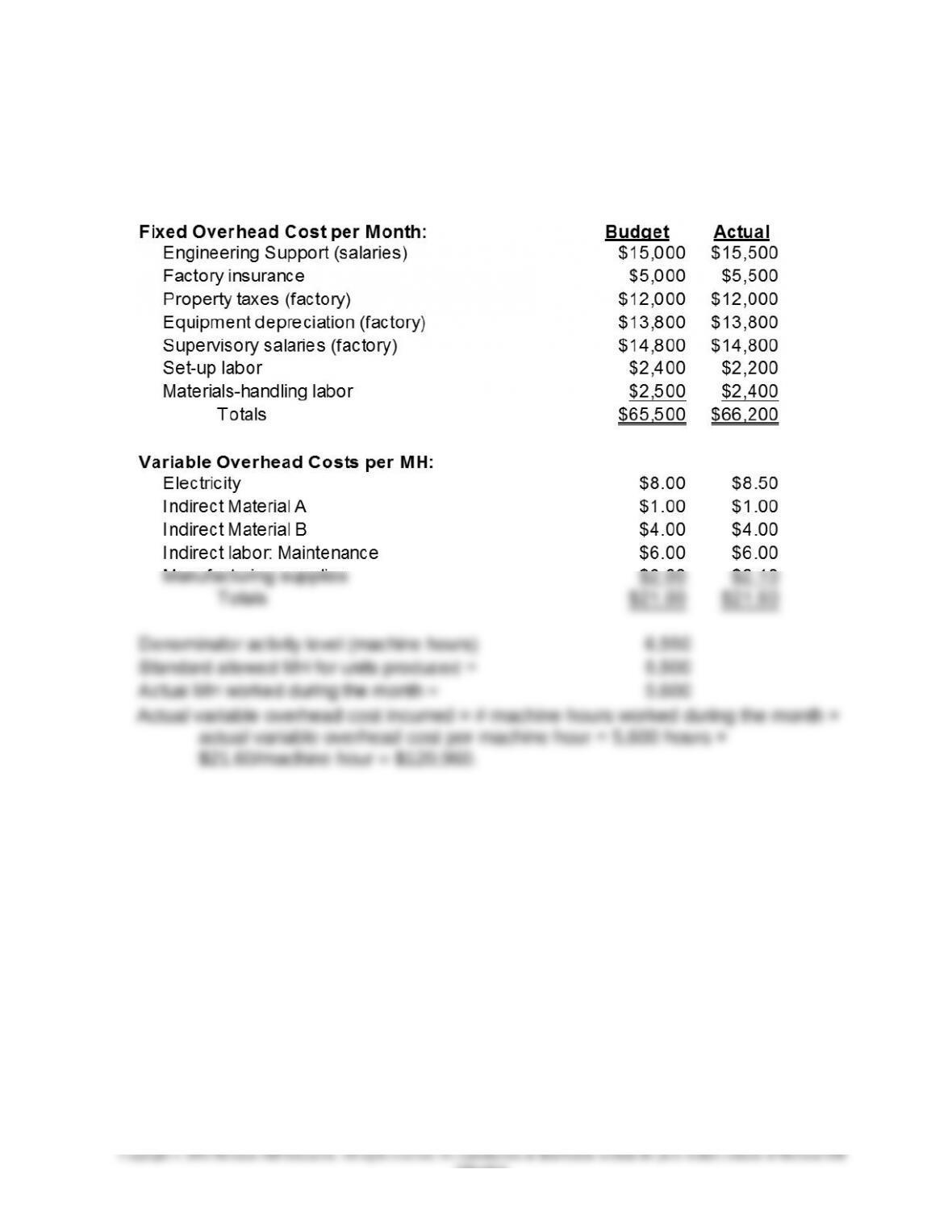

Supporting data:

15-28

Education.

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15-34 (Continued-1)

15-29

Education.

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15-34 (Continued-2)