Chapter 19 – Strategic Performance Measurement—Investment Centers

19-49 (continued)

If Partial Sales to Division A are OK:

Division B should sell as many units as possible (in this case 50,000 of total demand) to outside

consumers. The remaining capacity (20%, or 12,500 units) should be used to provide Division A

with equipment.

2. Assuming that Division B limits its sales to Division A to the excess capacity of 12,500 units, the best

transfer price should fall in the range of $60 (Division B’s variable cost) and $80 (the outside

purchase cost to Division A). The two divisions should negotiate to determine the desired price in

this range. A price of $60 would allocate all the profit on the manufacture of the equipment to

Division A, while a price of $80 would allocate all the profit to Division B. Any price less than $60

19-81

O/S

P=$130

B’s Capacity = 62,500

O/S

A

B

Chapter 19 – Strategic Performance Measurement—Investment Centers

19-50 Transfer Pricing; Strategy (45 minutes)

1. There are three options for the commercial division: buy from the internal supplier (the industrial

division), buy from Admiral Electric, or buy from Advanced Micro. The analysis follows, from the

perspective of FMI:

Buy inside from the industrial division:

Cost to FMI (assuming the Industrial Division is at full capacity):

Ind. Div.’s variable cost: $155 × 5,000 $775,000

Buy from Admiral Electric: Cost to FMI is $210. The contribution on sales to Admiral by the

industrial division is ignored because these sales are not contingent on the commercial division’s

decision.

The best transfer price, which would cause the buying division to autonomously make the correct

decision, would be to use the selling division’s market price of $205.

2. If the sales to Admiral Electric by the industrial division were contingent on the commercial

division’s decision, the relevant cost to FMI would be the price of $210 × 5,000 units (amount

19-82

Chapter 19 – Strategic Performance Measurement—Investment Centers

needed over the capacity of the industrial division). The net cost would then be the cost of $210 ×

19-83

Chapter 19 – Strategic Performance Measurement—Investment Centers

19-50 (continued)

3. The decision to have the commercial division buy outside to reduce overall costs is also consistent

with a strategy of decreasing the reliance of the commercial division on products from the industrial

division. If top management is unsure about the growth potential of the industrial division and has

declined any new investments there, perhaps the future holds capacity reduction or divestment of

19-84

Chapter 19 – Strategic Performance Measurement—Investment Centers

19-51 Strategy; Strategic Performance Measurement; Transfer Pricing (50 minutes)

1. Transfer prices based on cost are not appropriate as a divisional performance measure, and among

the reasons are because they:

2. Using the market price as the transfer price the contribution margin for both the Mining Division and

the Metals Division for the year ended May 31, 2016 is as calculated below.

Ajax Consolidated Calculation of

Divisional Contribution Margin

For the Year Ended May 31, 2016

Mining Division Metals Division

Selling Price $90 $150

Less: Variable costs

Direct materials 12 6

Direct labor 16 20

Manufacturing overhead (1) 24 10

19-85

Chapter 19 – Strategic Performance Measurement—Investment Centers

Notes:

19-86

Chapter 19 – Strategic Performance Measurement—Investment Centers

19-51 (continued)

3. If the use of a negotiated transfer price was instituted by Ajax Consolidated, which also permitted the

divisions to buy and sell on the open market, the price range for toldine that would be acceptable to

both divisions would be determined as follows.

The Mining Division would prefer to sell to the Metals Division for the same price it can obtain on the

would benefit both divisions and the company as a whole.

4.A negotiated transfer price is the most likely to elicit desirable management behavior as it will:

Encourage the management of the Mining Division to be more conscious of cost control

19-87

Chapter 19 – Strategic Performance Measurement—Investment Centers

19-52 Transfer pricing; International Taxation; Ethics (30 minutes)

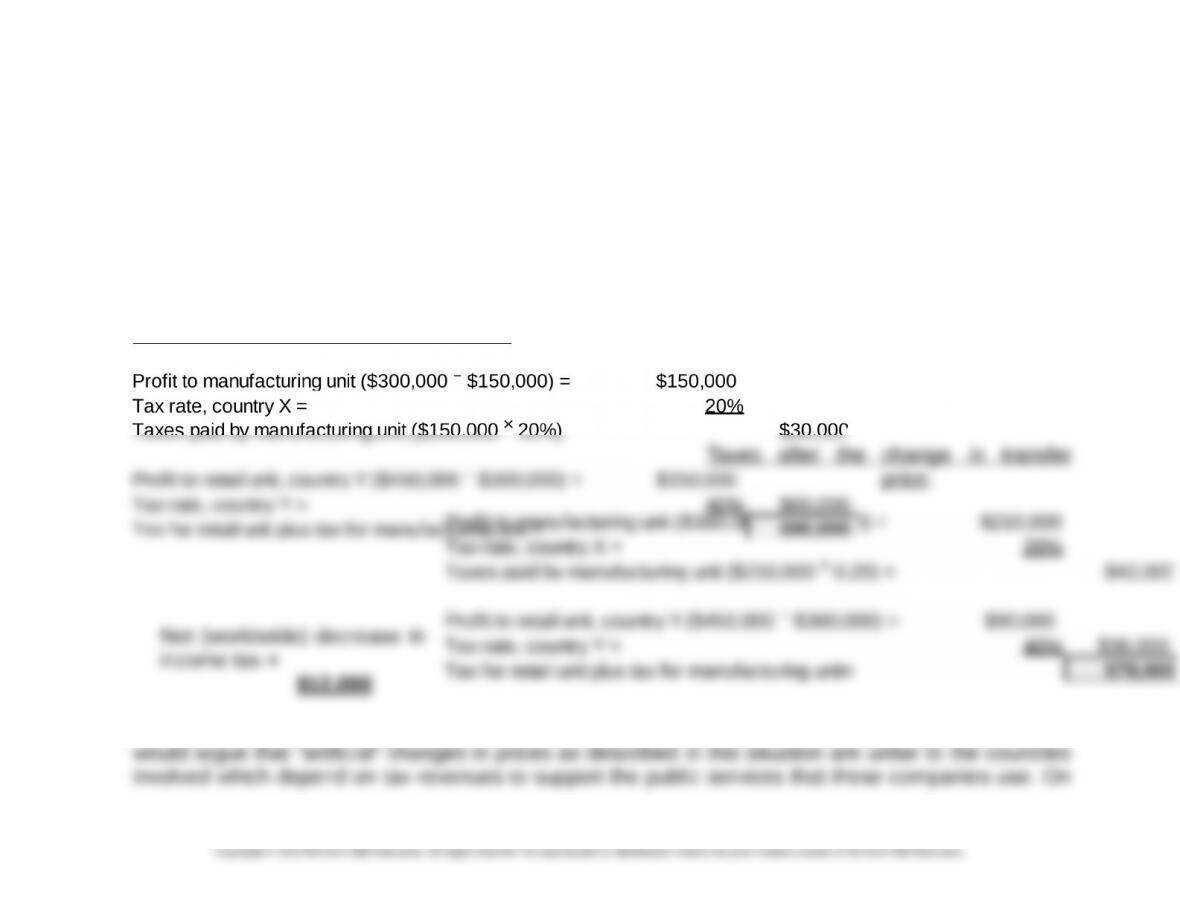

1. Because the tax rates are the same, there will be no effect on Target’s total tax burden from the

change in transfer price.

2. Now that the tax rates are different, Target has an opportunity to use transfer pricing to manage its

overall tax burden. The increase in the transfer price so that sales from the manufacturing unit to the

retail unit go from $300,000 to $360,000 would save Target $12,000 in taxes:

Taxes before the change in transfer price:

3. Most tax lawyers and accountants would call this good business and see no ethical issue. Others

19-88

Chapter 19 – Strategic Performance Measurement—Investment Centers

balance, it is most likely that tax treaties and tax policies and procedures within the major trading

countries have limited to a large extent the degree to which any multinational can reduce its tax

liability in this way. Most countries for example would insist on the “arm’s

19-52 (continued)

19-89

Chapter 19 – Strategic Performance Measurement—Investment Centers

19-53 Transfer Pricing—International Example (45-50 Minutes)

1. Combined (i.e., world-wide) after-tax income per unit:

Country A Country B

Subsidiary Parent Consolidated

Revenue/Unit = $200.00 $300.00 $300.00

Cost/Unit = $100.00 $200.00 $100.00

2. Revised selling price, subsidiary to parent company = $280.00:

Country A Country B

Subsidiary Parent Consolidated

Revenue/Unit = $280.00 $300.00 $300.00

Cost/Unit = $100.00 $280.00 $100.00

3. In this situation (i.e., where the income tax rate is the same in Country A as it is in Country B), then

the transfer price has no impact on the total amount of tax paid by the entity (as a whole) on the sale