Chapter 06 – Process Costing

6-49 (continued -1)

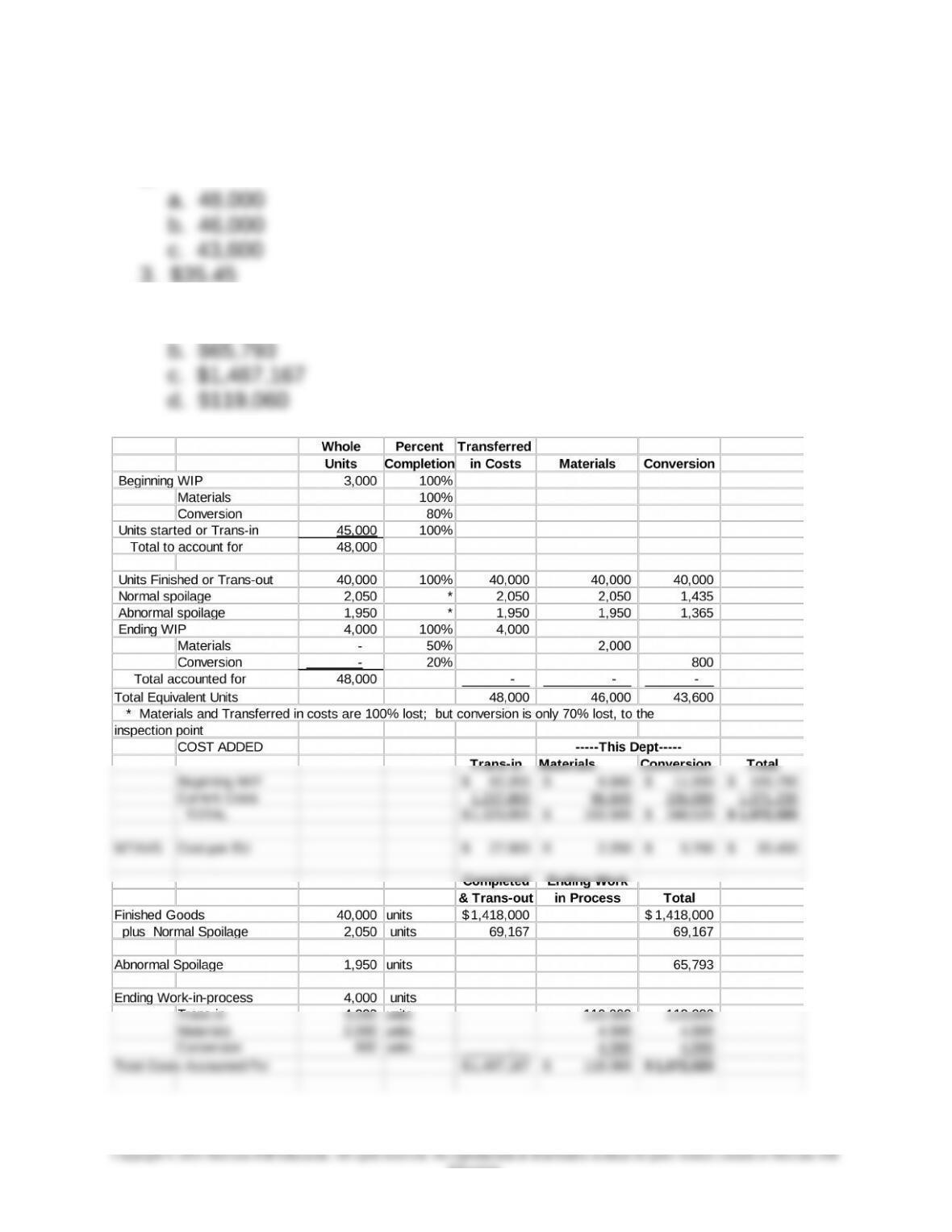

2.

4.

a. $69,167

6-41

Education.

Chapter 06 – Process Costing

6-49 (continued -2)

5. a. The cost of the normal spoiled units of $69,167 would be

transferred to the Packing Department as a portion of the cost of

the 40,000 good units transferred out. Thus, this amount would be

b. The abnormal losses of $65,793 would appear as a period

c. The cost of the good units completed and transferred to the

Packing Department ($1,487,167) would be included in the

Packing Department’s production costs. The unit cost would

6-42

Education.

Chapter 06 – Process Costing

6-50 Process Costing and Activity Based Costing (40 min)

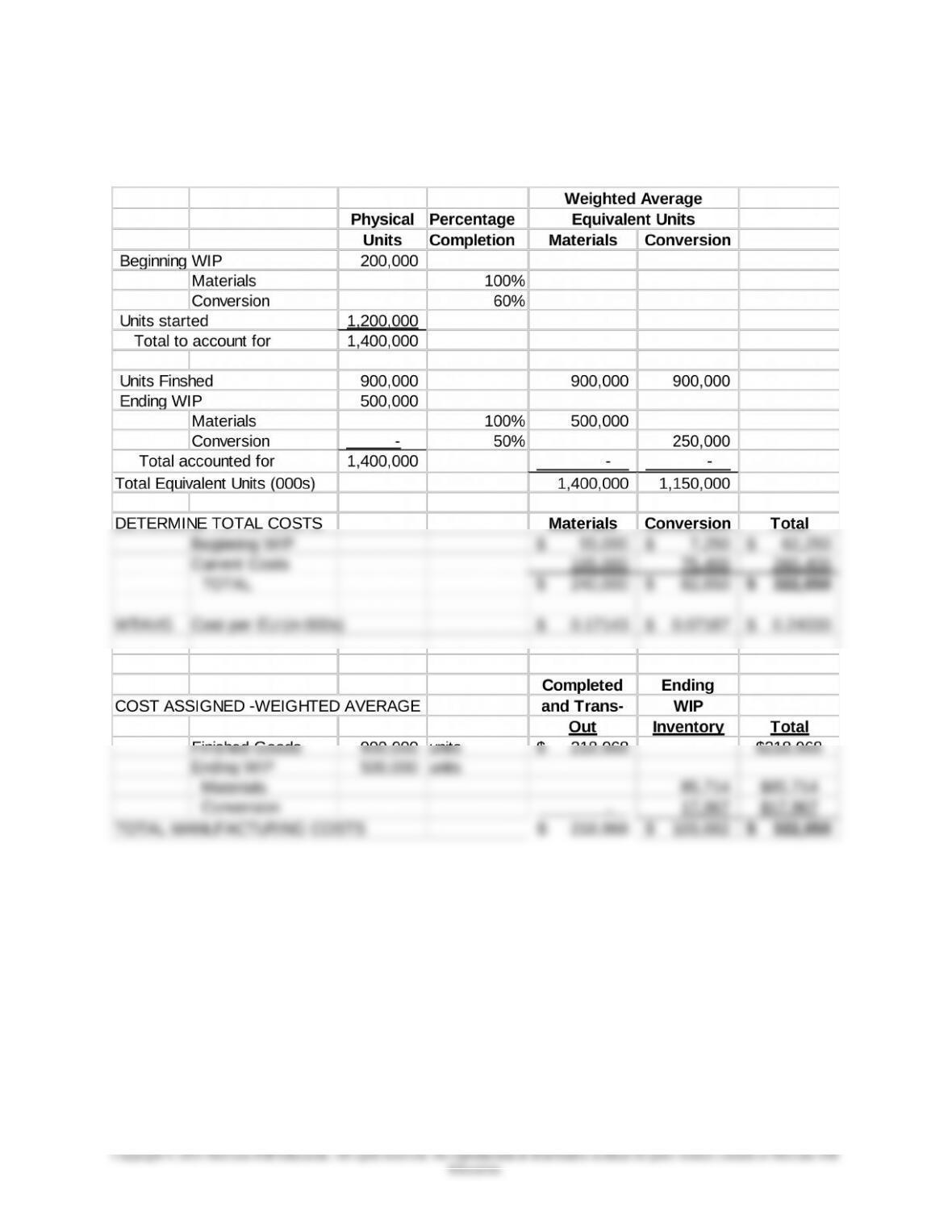

1.

6-43

Chapter 06 – Process Costing

6-50 (continued -1)

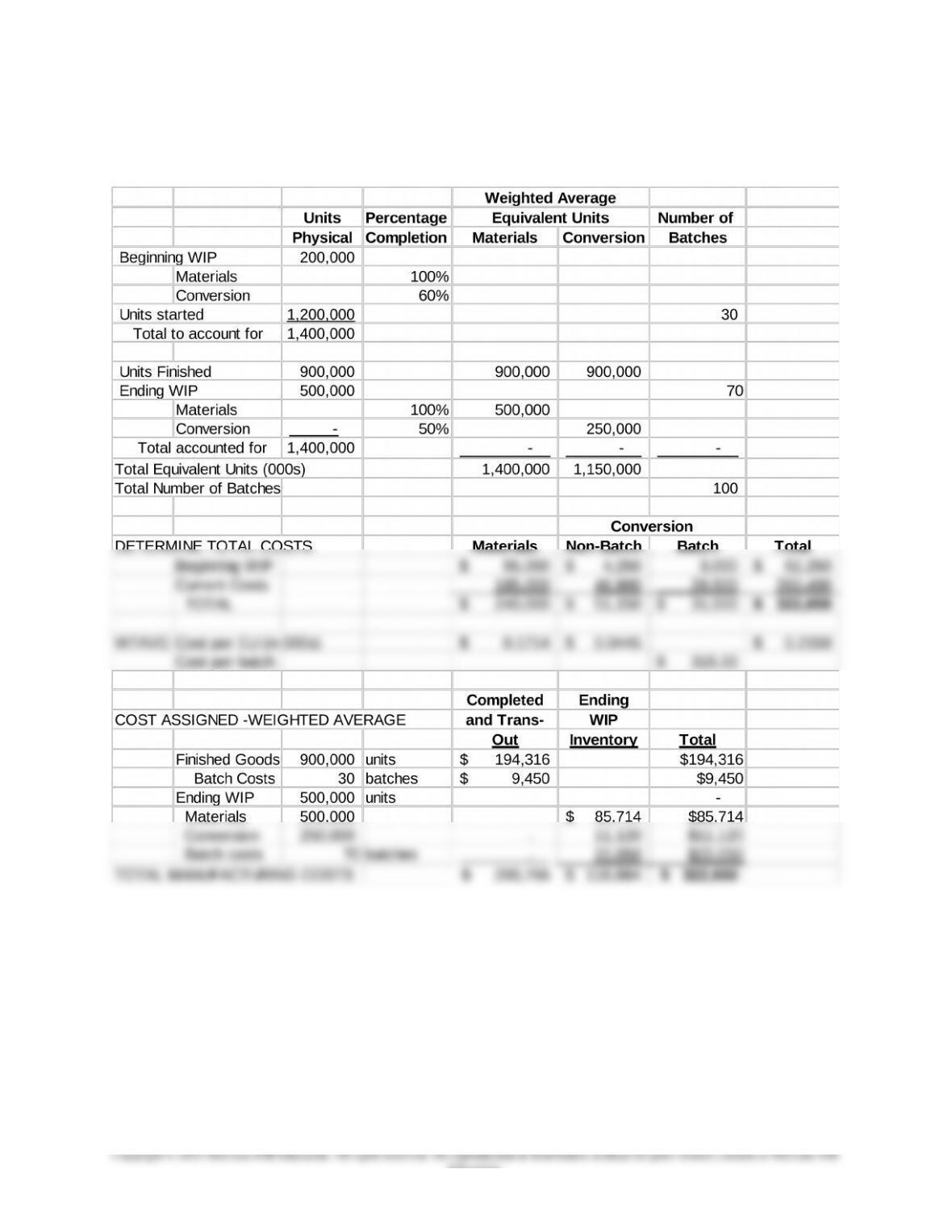

2.

6-44

Education.

Chapter 06 – Process Costing

Problem 6-50 (continued -2)

Ted is apparently correct about the under-costing of ending working

process. The activity-based method, which separates the batch-related

costs from the other conversion costs, shows $118,884 ending work in

6-45

Education.

Chapter 06 – Process Costing

6-51 FIFO Method with Rising Prices (30 min)

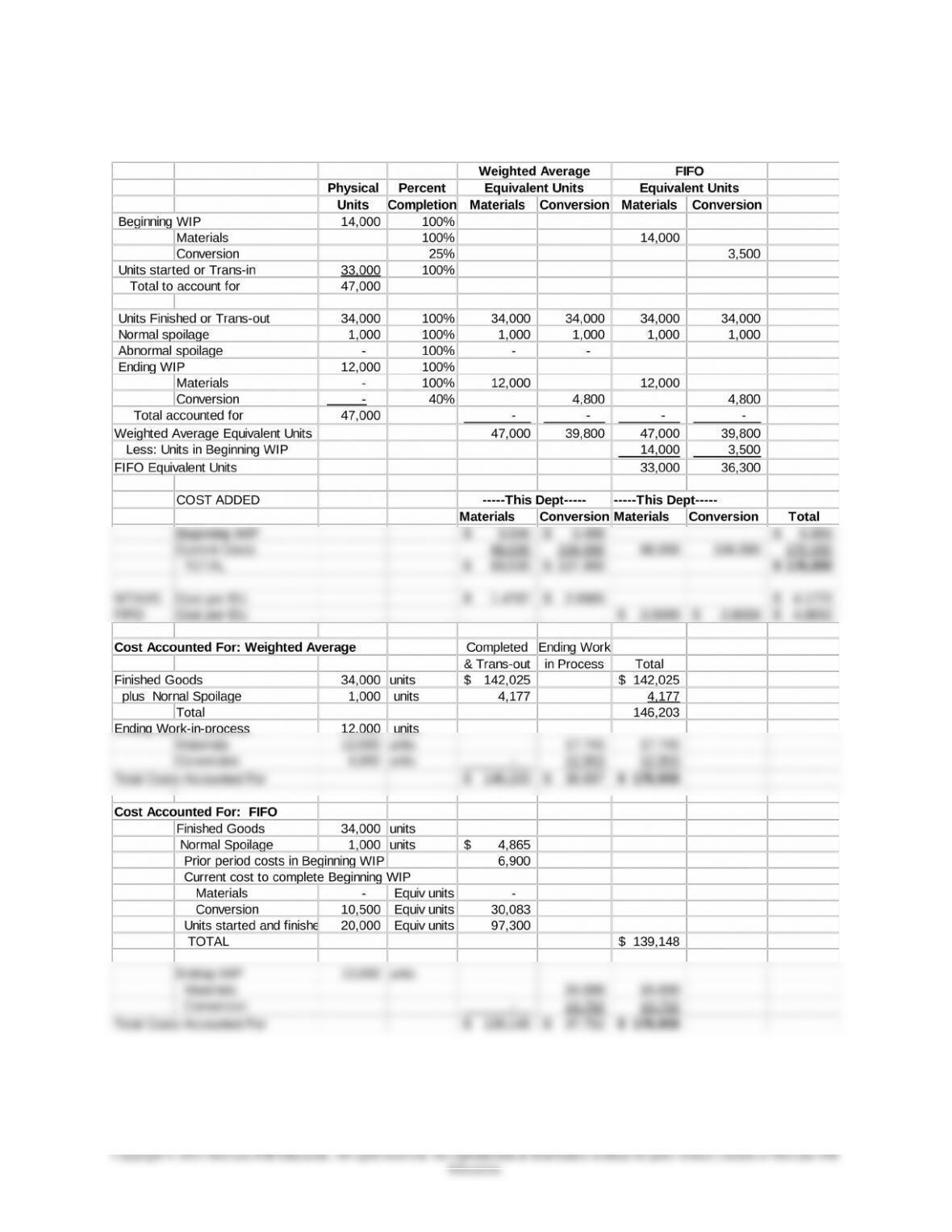

1.,2.

6-46

Chapter 06 – Process Costing

6-51 (continued -1)

3. The CFO is on the right track to consider FIFO costing. With prices

rising rapidly, FIFO provides a way to separate the current and prior

period costs, so that the price increases can be examined and

charged properly to each period’s production. Note that in this case

there is a sizeable amount of beginning and ending work-in-process

inventory, which makes the issue of separating prior period and

FIFO method shows a smaller amount for finished goods (and thus

also for cost of goods sold) because, under FIFO, all of the

(relatively small) prior period costs are traced to finished goods.

For a company like HSC that competes on quality and brand loyalty,

it is likely that the company will be able to pass along at least a good

portion of these increased costs. The FIFO method provides HSC a

good tool to watch the cost changes as they affect the company’s

6-47

Education.