123. T-shirts R Us Inc. operates two divisions that each manufactures t-shirts for universities.

Each division has its own manufacturing facility. The historical-cost accounting system reports

the following financial data for 2016.

Atlantic Coast Division

Condensed Income Statement Data

(000s)

Revenues $600

Operating Costs 470

Operating Income $130

Big-10 Division

Condensed Income Statement Data

(000s)

Revenues $600

Operating Costs 400

Operating Income $200

T-shirts R Us Inc. estimates the useful life of each manufacturing facility to be 15 years. The

company uses straight line depreciation, with a depreciation charge of $70,000 per year for each

division and no salvage value at the end of 15 years. The manufacturing facility is the only long–

lived asset of either division. Current assets are $300,000 in each division. At the end of 2016 the

Atlantic Coast Division is 4 years old and the Big-10 Division is 6 years old. An index of

construction costs, replacement cost, and liquidation values for manufacturing facilities used in

the production of t-shirts for the 7-year period that T-shirts R Us Inc. has been operating, are as

follows:

Liquidation Value

Year

Cost Index Replacement

Cost Atlantic

Coast

Big 10

2010 80 $1,000,000 $800,000 $800,000

2011 82 1,000,000 800,000 800,000

2012 84 1,100,000 700,000 700,000

2013 89 1,150,000 700,000 600,000

2014 94 1,200,000 800,000 600,000

2015 96 1,250,000 900,000 600,000

2016 100 1,300,000 1,000,000 500,000

Required:

Round answers to 2 decimal places where appropriate.

1. Compute return on investment (ROI) for each division using net book value (NBV). Interpret

the results.

2. Compute return on investment (ROI) for each division, incorporating current–cost estimates as

follows, using:

(a) Gross book values (GBV) under historical cost;

(b) GBV at historical cost restated to current cost using the index of construction costs;

(c) NBV of long-lived assets restated at current cost using the index of construction costs (the

facility was constructed the year before the first year of use);

(d) Current replacement cost; and

(e) Current liquidation value.

3. Which of the measures calculated in (2) above would you choose for (a) performance

evaluation of each division manager, and (b) deciding which division is most profitable for the

overall firm? What are the strategic advantages and disadvantages to the firm of each measure

for both (a) and (b)?

124. Domi Products, a multi-divisional manufacturing company, measures performance and

awards bonuses to division managers based upon divisional operating income. Under the current

bonus plan, common company-wide operating expenses are allocated evenly to all five of its

divisions. For example, if rent were $50,000, each division would be charged $10,000. In planning

next year’s budget, corporate management has requested that the division managers recommend

how common expenses should be distributed to the divisions. The division managers met and

jointly developed an incentive plan that would more equitably distribute common expenses on the

basis of resources used and that would measure each division manager’s performance based on

return on assets (ROI), with divisional bonuses based on a target ROI. They jointly presented

their recommendation to corporate management.

Required:

1. Describe at least three problems that Domi Products could encounter when using return on

investment (ROI) as the basis of performance measurement.

2a. Define the residual income (RI) approach to segment performance measurement.

2b. Determine if Domi Products should implement this approach instead of the ROI approach.

3. Discuss the behavioral implications of the division managers’ involvement in the corporate

budgeting process, and the decision to more equitably allocate common costs.

125. Eikelberry, Inc. has the following financial results for 2016 for its three regional divisions:

Current Cost

Region

Income Net Book

Value Gross

Book Value Replacement

Cost Liquidation

Value

FINANCIAL DATA

North Atlantic $45,000 $225,000 $450,600

$990,000 $350,000

Mid Atlantic 33,000 289,000 310,000 380,000

445,000

South Atlantic 22,000 115,000 166,000 650,000

980,000

Required:

126. Edwards Inc. manufactures electronics. It consists of several divisions classified as

investment centers for performance-evaluation purposes. Division A desires to purchase

materials from Division B at a price of $85 per unit. Division B can produce 25,000 units at full

capacity, and is currently operating at 90% capacity with a variable cost of $80 per unit. Division

B currently sells only to outside customers who pay $115 per unit. Division A pays an outside

company $110 per unit. If purchased from Division B, B’s variable costs per unit would be $10

less because the division would save on marketing expenses for these internal transfers. Division

A requires 10,000 units.

Required:

1. How would Division B selling to Division A affect Division A’s purchasing costs?

2. How would intercompany sales affect Division B?

3. What solution would be best for Edwards Inc., assuming Division B has the ability to operate

at full capacity?

127. Max Ltd. produces kitchen tools, and operates several divisions as investment centers.

Division M produces a product that it sells to other companies for $16 per unit. It is currently

operating at its full capacity of 45,000 units per year. Variable manufacturing cost is $9 per unit,

and variable marketing cost is $3 per unit. The company wishes to create a new division, Division

N, to produce an innovative new tool that requires the use of Division B’s product (or one very

similar). Division N will produce 30,000 units per year. Currently, Division N can purchase a

product equivalent to Division M’s from Company X for $15 per unit. However, Max Ltd. is

considering transferring the necessary product from Division M.

Required:

1. Assume the transfer price is $12 per unit:

a. How would this price affect the purchasing costs of Division N?

b. How would this price affect the profits of Division M?

c. How would this price affect Max Ltd. as a whole?

2. What if the transfer price was $13 per unit?

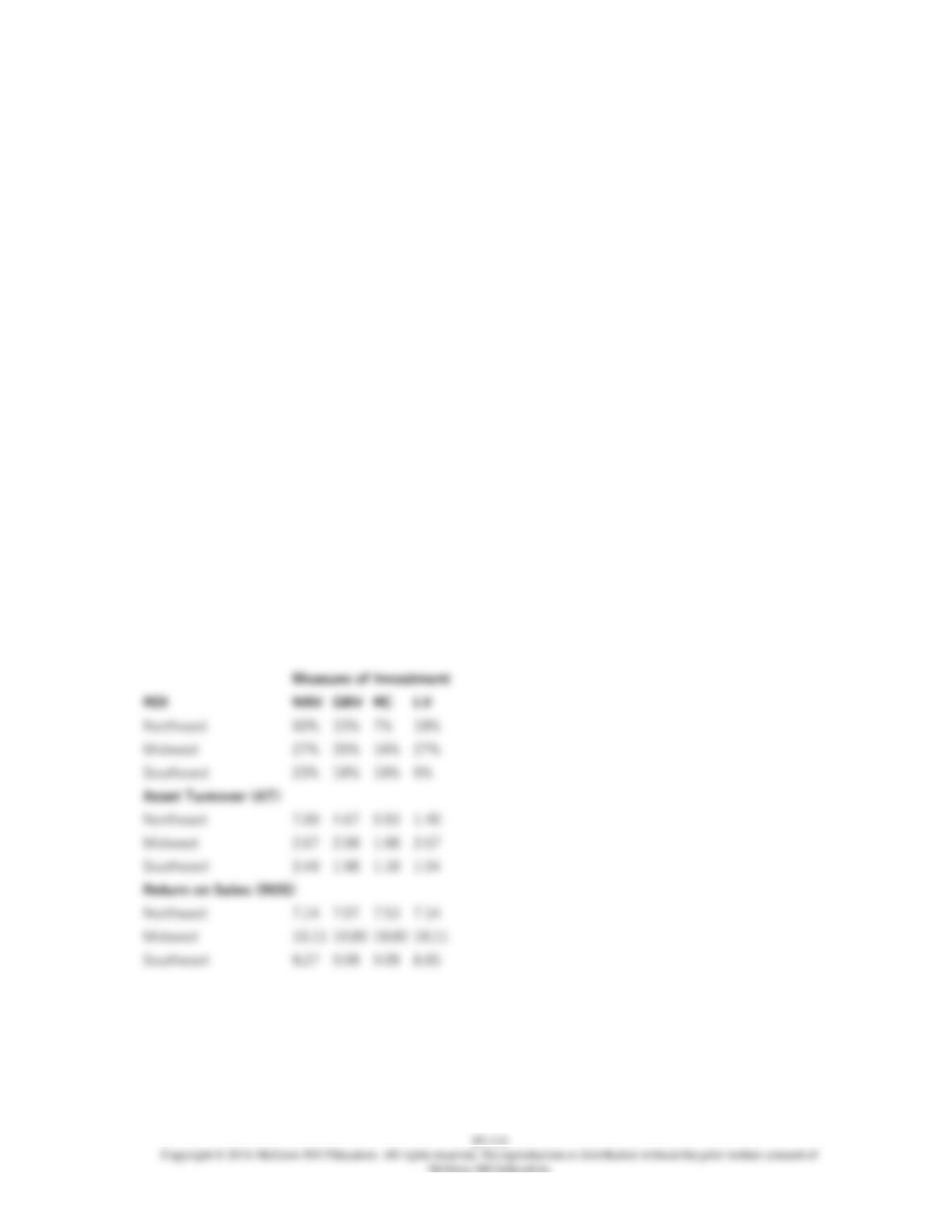

128. Pearl Inc. has the following financial results for 2016 for its three regional divisions:

Historical Cost Estimated Current Cost

Region Operating Income

NBV

GBV Replacement Cost Liquidation Value

Northeast $50,000 $100,000 $150,000 $750,000 $500,000

Midwest $80,000 $300,000 $400,000 $500,000 300,000

Southeast $90,000 $400,000 $500,000 $900,000 950,000

Required:

Calculate return on investment (ROI), asset turnover (AT), and return on sales (ROS) for each

division for 2016. The sales in the Northeast, Midwest, and Southeast regions are $700,000,

$800,000, and $990,000, respectively. Calculate ROI and AT for each of the four measures of

investment (i.e., NBV (net book value), GBV (gross book value), Replacement Cost, and

Liquidation Value). Round all answers except ROI to 2 decimal places (e.g., 0.12522 becomes

12.52%); round ROI to whole percentage amounts, e.g., 0.1998 becomes 20%.

129. Selected data from one of the investment centers from Jones Company are as follows:

Sales $400,000

Average divisional assets $320,000

Divisional operating income $40,000

Minimum rate of return 11%

Required:

1. Calculate return on investment (ROI), including each of the two component measures of ROI.

2. Calculate residual income (RI).

130. Brown’s Mill has two operating units, each of which is considered an investment center

for evaluation purposes. The Cutting Division of the mill prepares timber at its sawmills.

Afterwards, the Assembly Division prepares the cut lumber into finished wood, to be sold to

furniture manufacturers. During the most recent year, the Cutting Division produced 120,000

cords of wood, at a total cost of $1,320,000. The entire output was transferred to the Assembly

Division, where additional costs of $6 per cord were incurred. The 1,200,000 board-feet of

finished wood were then sold in the open market for $5,000,000.

Required:

1. Determine the operating income for each division if the transfer price from the Cutting

Division to the Assembly Division is set at full production cost, $11 per cord.

2. Determine the operating income for each division if the transfer price is set at $9 per cord.

3. Since the Cutting Division sells all of its output internally, does the manager care about what

price is charged? Why? Should the Cutting Division in this case be considered a cost center or

a(n) profit/investment center?

131. Simmons Bedding Company manufactures an array of bedding-related products,

including pillows. The Cover Division of Simmons makes covers, while the Assembly Division of

the company produces finished pillows. The covers can be sold separately for $10.00 a piece,

while the pillows sell for $12.00 per unit. For performance-evaluation purposes, these two

divisions are treated as investment centers. Financial results from the most recent accounting

period are as follows:

Division

Division

Traceable manufacturing costs

External sales

Market value of output transferred from Cover Division to the Assembly Division

$6,000,000

Required:

1. What is the operating income for each of the two divisions and for the company as a whole?

(Use market value as the transfer price.)

2. Do you think each of the two divisional managers is happy with this transfer-pricing method?

Explain.