Chapter 16 – Operational Performance Measurement: Further Analysis of Productivity and Sales

16-49 (continued -1)

3.

MEMO

TO: Rajat Patel, Integrated Medical Care

FROM: Joseph Marin, Marin & Associates

I have calculated the financial partial productivity measure for IMC

for the current and prior year and the supporting documentation is

attached.

Nursing productivity improved by .003882 over the prior year, while

administrative productivity improved by .012823. I attribute this to the

There was a small decline in the pricing component of productivity,

since average wages increased in both nursing and administrative

support; overall, taking both the change in wages and change in hours

into account, the financial productivity of both nursing and administrative

support improved from the prior year.

An important finding is that the financial partial productivity of FMC

compared very well to the industry average, with a current productivity for

nursing at .04168, compared to the industry average of .035. This is a

significant achievement and shows that the management of the FMC

practice in nursing support is in very good shape. In contrast, the

financial partial productivity for the administrative support is below the

16-41

Education.

Chapter 16 – Operational Performance Measurement: Further Analysis of Productivity and Sales

16-49 (continued -2)

Medical practices are under pressure in recent years as Medicare

1. Cross-training employees so that overall staff positions can be reduced

2. Using a larger portion of part-time employees in order to improve the

practice’s flexibility to reduce labor costs when demand patient demand

fluctuates

3. Join with other practices to become multiple-doctor practices. The

multiple-doctor practices are able to utilize facilities and staff more

Source: Katherine Reynolds Lewis, “Medical Practices Work on Ways to

Serve Patients and Bottom Line,” The New York Times, September 8,

2011, p B10.

16-42

Education.

Chapter 16 – Operational Performance Measurement: Further Analysis of Productivity and Sales

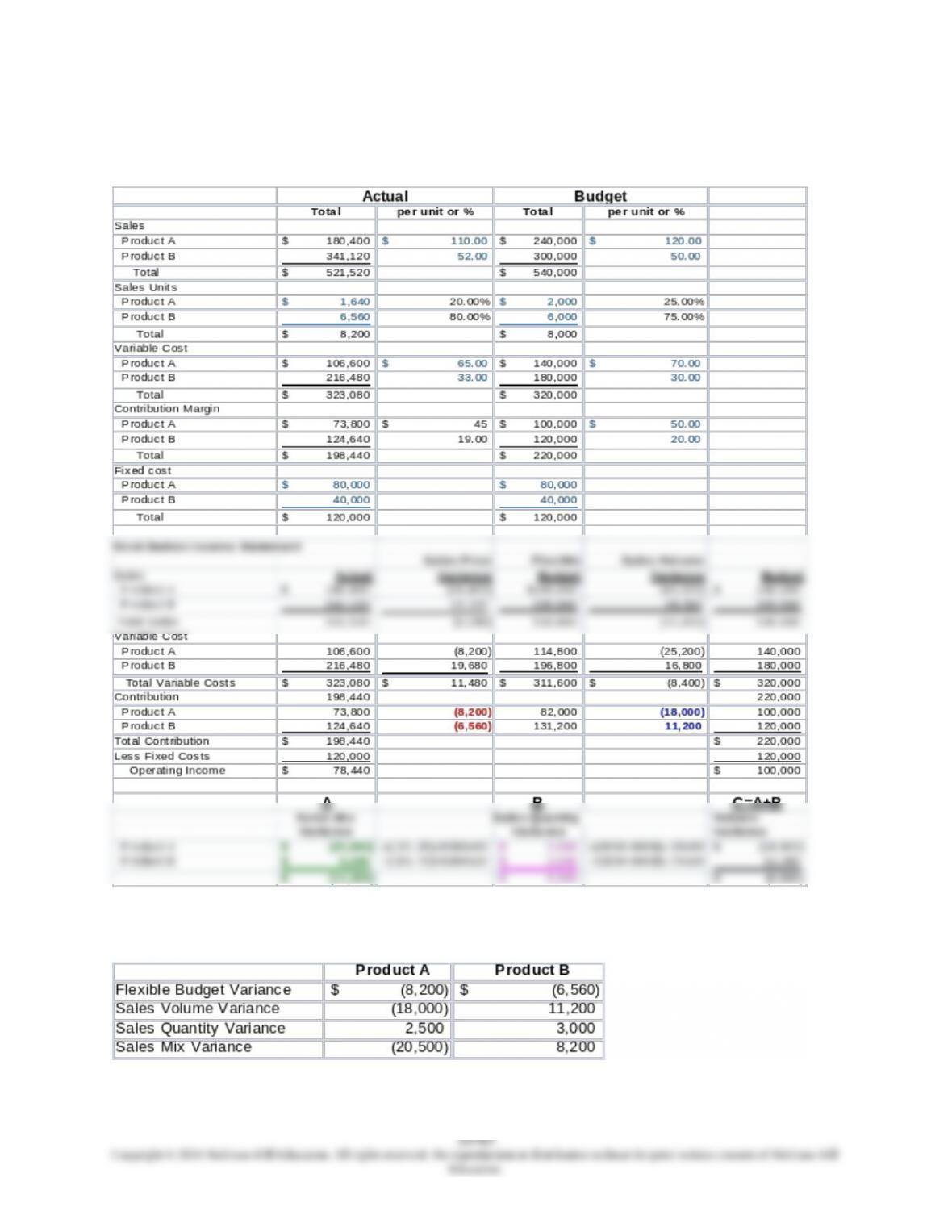

16-50 Flexible Budget, Sales Volume, Sales Mix, and Sales Quantity

Variances (40 min)

1.

Summary of Variances, as calculated above in contribution margin

(negative is unfavorable, positive is favorable):

Chapter 16 – Operational Performance Measurement: Further Analysis of Productivity and Sales

16-50 (continued -1)

2.

The reconciliation of the selling price, variable cost, and flexible cost

variances is as follows. The variances are in the solution shown in part 1.

16-44

Education.

Chapter 16 – Operational Performance Measurement: Further Analysis of Productivity and Sales

16-51 Flexible Budget, Sales Volume, Sales Mix, and Sales Quantity

Variances (30 min)

1.

16-45

16.51 (continued -1)

The solution is summarized below, and the calculations are shown above

(a negative is unfavorable and a positive is favorable):

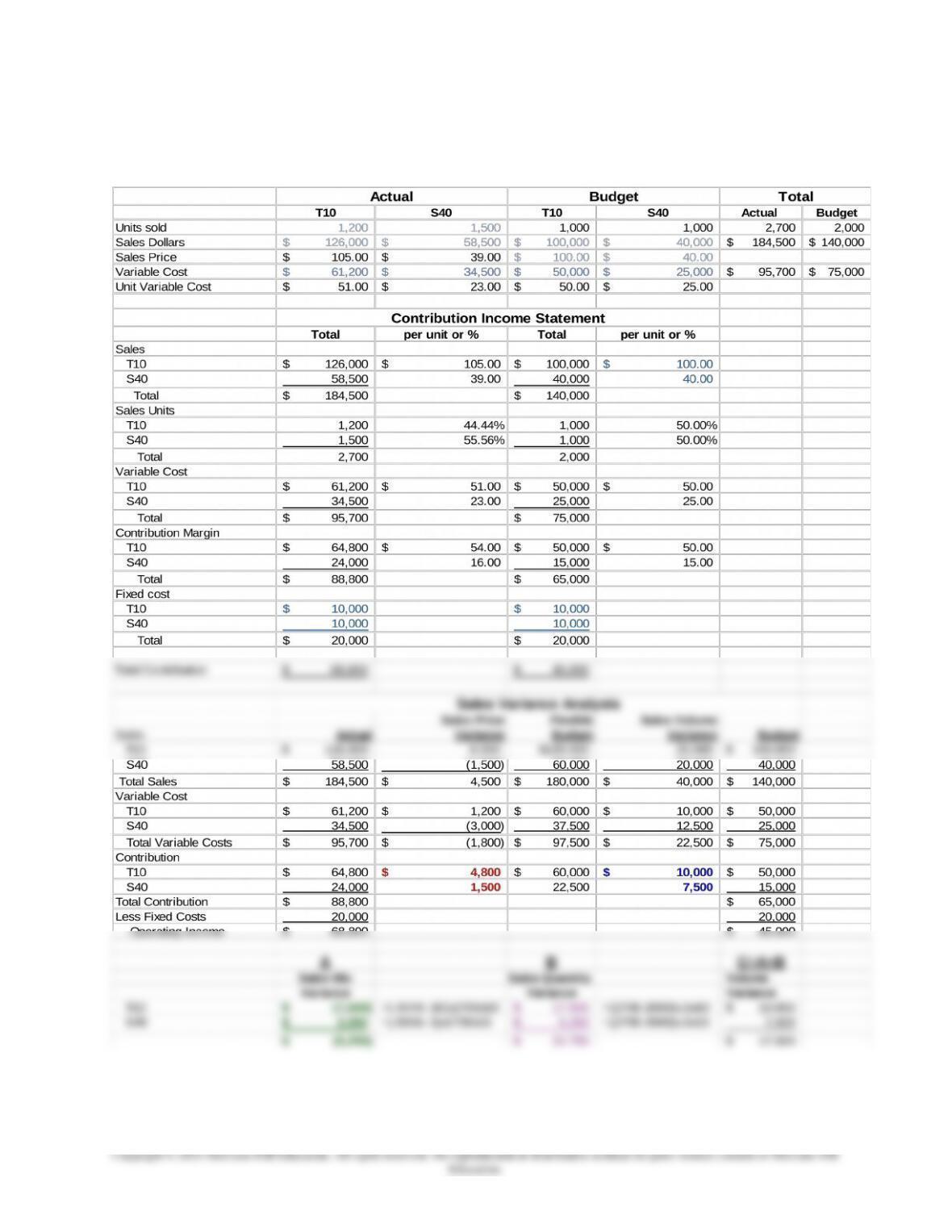

2.

MEMO

TO: Jay Banning, CEO

FROM: I M Student

RE: Banning Inc. Variance Analysis

The following information describes the results of variances

calculated on the attached spreadsheet (see requirement 1) with regard

to what was planned for the past year and the actual results reported.

The firm has a favorable sales volume variance for both T10 and S40

due to increase sales volumes over budget for both products. The total

sales mix variance for T10; the net is a negative overall sales mix

variance.

The flexible budget variance is favorable for both S40 and T10

because T10’s increase in price was greater than its small increase in

16-46

Education.

Chapter 16 – Operational Performance Measurement: Further Analysis of Productivity and Sales

16-52 Sales Volume, Sales Quantity, and Sales Mix Variances (20 min)

Sales Mix

Budget Actual

Flavor Quantity Mix Quantity Mix

Vanilla 240,000 .3000 180,000 .18750

Chocolate 300,000 .3750 270,000 .28125

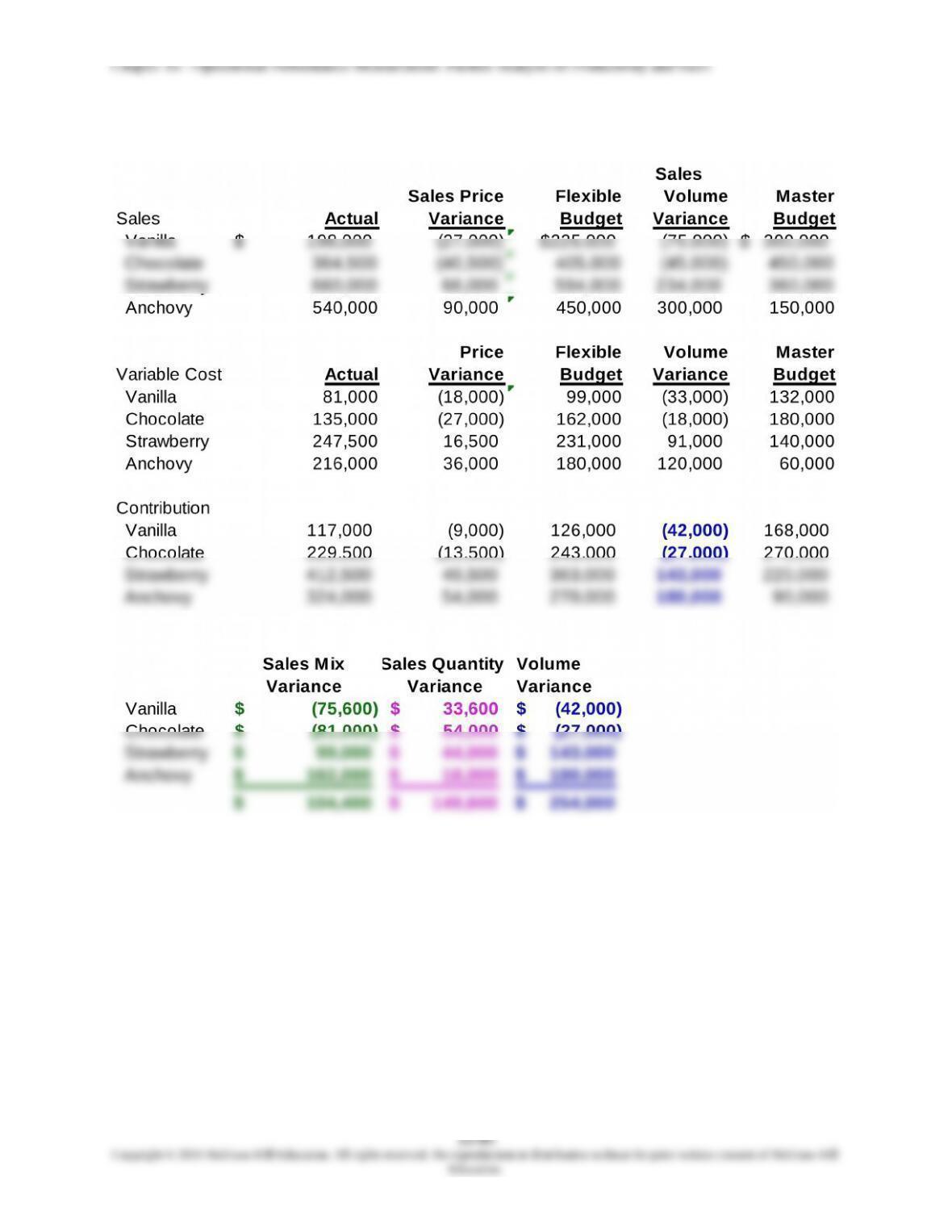

1. a. Sales Volume Variance

Budgeted Sales

Sales Quantity Contribution Volume

Flavor Actual Budget Difference Margin/Unit Variance

Vanilla 180,000 240,000 60,000 x $0.70 = $ 42,000 U

Chocolate 270,000 300,000 30,000 x $0.90 = 27,000 U

1. b. Sales Mix Variance

Total Budgeted Sales

Sales Mix Actual CM Mix

Flavor Actual Budget Difference Quantity per Unit Variance

Vanilla .18750 .3000 – .11250 x 960,000 x $ .70 = 75,600 U

Chocolate .28125 .3750 – .09375 x 960,000 x $ .90 = 81,000 U

16-52 (continued -1)

16-47

Education.

1. c. Sales Quantity Variance

Budget Budgeted Sales

Sales Mix Sales CM Quantity

Flavor Actual Budget Difference Mix per Unit Variance

Vanilla 960,000 800,000 160,000 x .3000 x $0.70 = $33,600 F

Chocolate 960,000 800,000 160,000 x .3750 x $0.90 = 54,000 F

Recap

Sales Mix Sales Quantity Sales Volume

Flavor Variance Variance Variance

Vanilla $ 75,600 U + $ 33,600 F = $ 42,000 U

Chocolate 81,000 U + 54,000 F = 27,000 U

2. Overall, the firm has enjoyed a good year. The total units sold

substantially exceed the budgeted amount (20%). The increases in

sales could have been a result of the increase of the entire market

size for ice cream and other competing merchandises. In any event,

16-48

Education.

16.52 (continued -2)

The spreadsheet solution for 16-52 is provided below:

Chapter 16 – Operational Performance Measurement: Further Analysis of Productivity and Sales

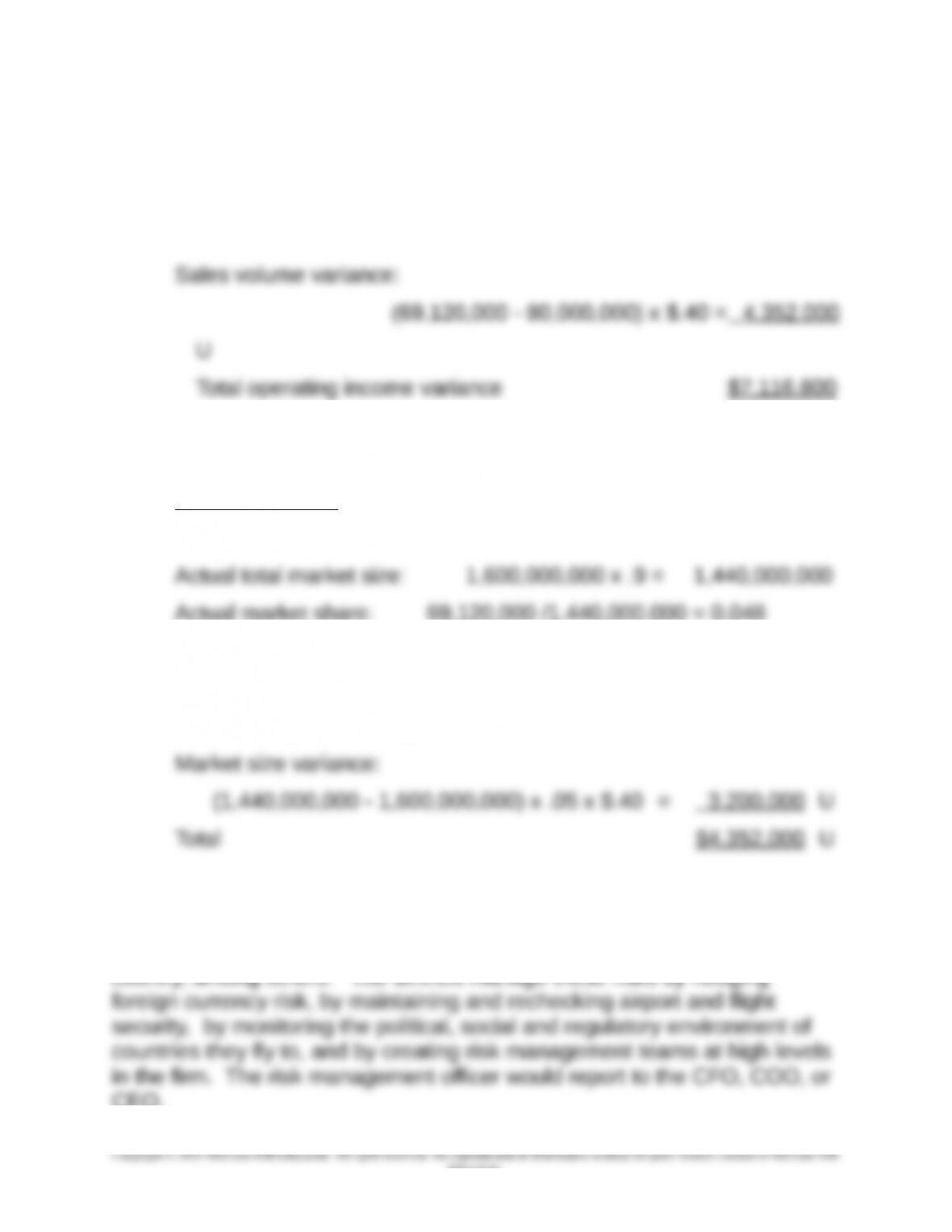

16-53 Market Size and Market Share Variances (20 min)

1.

Selling price variance: ($.48 – $.52) x 69,120,000 =$2,764,800

U

U

Total market size

Budgeted total market size: 80,000,000 /.05 = 1,600,000,000

Actual market share: 69,120,000 /1,440,000,000 = 0.048

Market share variance:

(0.048 – 0.05) x 1,440,000,000 x $.40 = $1,152,000 U

2. The global risks for an airline include weather events, foreign currency

fluctuations, disruptions in political environments, terrorist activities (as in

the case in this problem), and changes in regulations from country to

CEO.

16-50

Education.