Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products

Case 7-3 Business Services Corporation

The case involves the allocation of the indirect costs associated with holding and distributing replacement

parts used in servicing the computer and other business products sold to customers under a service

agreement. The company has two business units, the computer division and the business products

division. The source of the issue in the case is the determination of an appropriate method for allocating

the indirect costs of holding and distributing replacement parts used by both divisions. The costs

involved are significant. The company stocks 100,000 different parts in 40,000 locations. Further,

although a small number of parts may never be needed, the firm feels it must have at least a few units of

every part on hand so that it could service every customer’s need. This policy leads to obsolescence of

parts, an additional cost to that of storing and distributing the parts. At the time of the meeting described

in the case, parts overhead was averaging 70% of the cost of the parts charged directly to the product.

To put the issue in perspective, Exhibit 1 shows how each item in parts overhead is related to the

activity in the two divisions.

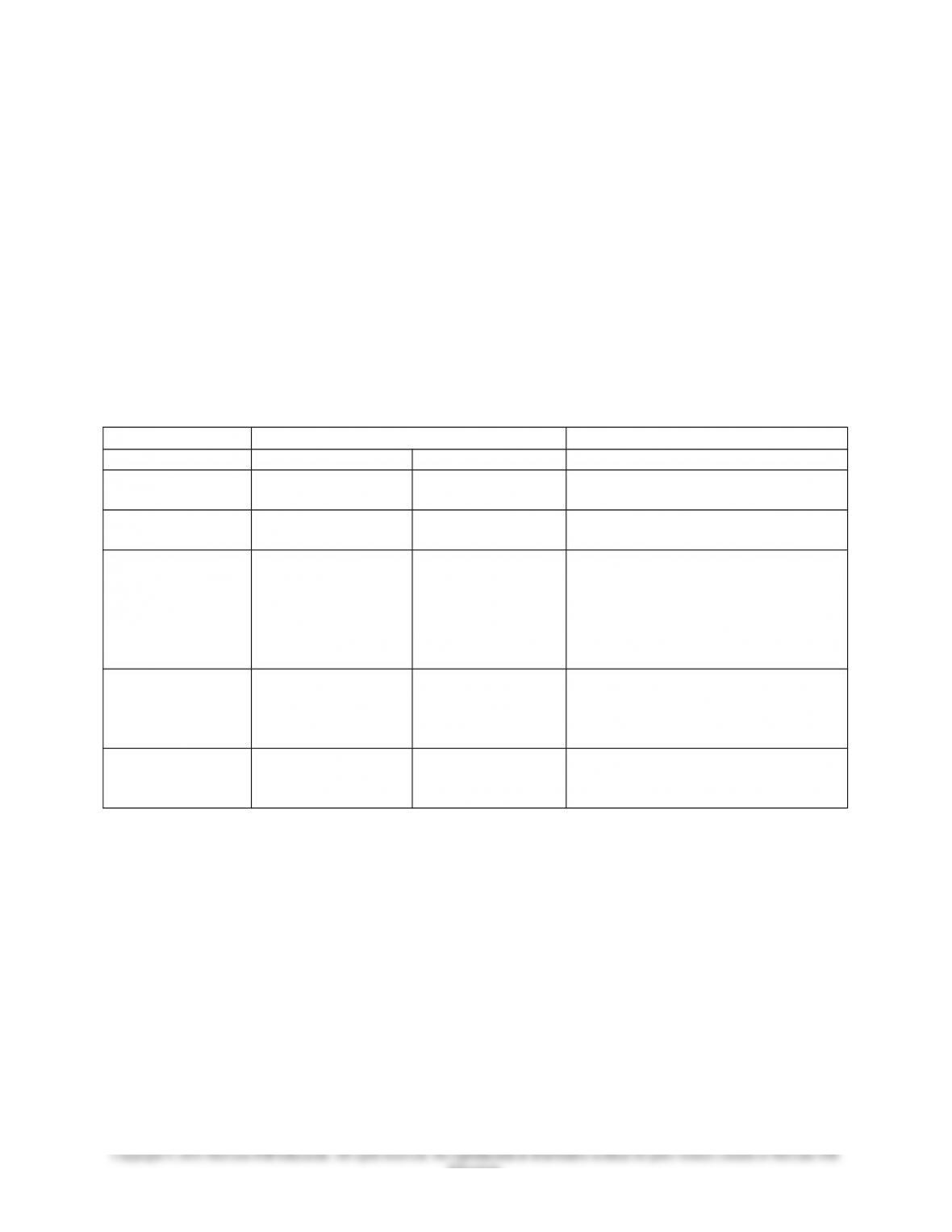

Exhibit 1: Relationship of parts overhead costs to activities in the two divisions.

Association With (usage by..)

Cost Computer Division Business Products Explanation

Non-product usage low high Most of the low value parts are used

by the business products division

Inventory variance low low These are random costs and small in

amount

Parts scrap,

obsolescence

high low The parts needed for the computer

division are generally much more

expensive and the need for parts much

more difficult to forecast. Demand

for business products’ parts are

relatively easy to predict

Holding high low Again, computer parts are very

expensive and tend to stay in

inventory for long periods. Business

products’ parts turn over quickly

Distribution low high Very large volumes of business

products’ parts flow through the

system

Note that the current allocation method allocates all overhead on the basis of the cost of those parts (in

excess of $10 per part) actually used. The computer division feels this approach over charges the unit for

obsolescence and holding costs. Both divisions, in effect, are arguing that the allocation method does not

capture cause-and-effect relationships.

7-7

Education.

Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products

Answers to questions:

1. The objectives of cost allocation are to motivate managers to work hard, to make decisions that

managers perceive to be fair.

2. What are the options to the current method? One option would be to trace all direct parts costs

(including cost of parts costing less than $10) to products and allocate overhead on this more

comprehensive measure of direct costs. This would solve one of the object is of the computer

division. Another possibility is to allocate on the basis of the number of parts used instead of

cost. This might be appropriate for example, for distribution costs. Because a good portion of

inventory holding costs are due to the average value of parts stored for each division, an

What the firm actually did:

The meeting ended with the president appointing a task force headed by the direct of accounting.

The task force recommended the following actions that were then implemented. First, all parts, including

low-value parts, that can be directly t4raced to a product or group of products are now charged to those

products. Similarly, the cost of obsolete parts that are identifiable with a particular product line are

charged to that product line. This increase in the identification of direct costs has greatly decreased the

7-8

Education.

Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products

Teaching Strategy for Readings

“Managing Shared Services with ABM”

This article outlines the benefits of using shared services (i.e., finance and accounting services) in

large companies such as Ford Motor company, Sun Microsystems and Marriott. There is also a

discussion of how activity-based management (ref: Chapter 5) is used to manage the costs of these shared

services.

Discussion Questions:

1. How do the concepts of cost management for shared services differ from the concepts and methods

presented in chapter 7?

The concepts for cost management of shared services (chapter 5) differ from the concepts and

methods presented in Chapter 7 in the following way. The concepts for cost management of shared

services focus on identifying the cost drivers of the services, and on reducing these costs through

standardizing and centralizing the activities. ABC/ABM is a natural application in this context, and

should reduce in lower overall costs and better decision making about support activities. For example,

2. Who are the customers referred to in the article?

3. What do you think is the best way to manage the costs of shared services such as finance and

accounting?

charging different rates to different users based on cost driver information (job complexity, etc).

7-9

Education.

Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products

7-2 “Simpler than ABC New Ideas for Using Microsoft Excel for Allocating Costs”

This article looks at a new method for service department cost allocation using Excel. It includes

important tips about making a useful Excel spreadsheet and it also factors in alternative methods to

compare against accounting for service department costs.

Discussion Questions:

1. Define an argument against the use of service department allocations.

Many reasons against allocating these costs refer to the arbitrary nature of the allocation method and the

distorting influence of these costs. The accuracy of the assignment of cost is in large part a function of the

2. In what cases should service department allocations be used instead of activity-based costing?

3. What are some key factors in making a useful Excel worksheet?

1. Start by constructing formulas that take into account all cost flows in and out of the service department

to other service departments only.

2. Rearrange the formula so that the original costs assigned are to one side and all coefficients, inward

and outward for any given service department are arranged in columns.

the appropriate column with the column of costs to be allocated. If correct, the given service department

matrix will have its assigned pre-allocated costs in the diagonal cell replacing its diagonal coefficient.

7. Use the MDETERM function in Excel to find the determinant for each matrix.

7-10

8. Divide the individual service department. Determinants by the determinant for the coefficient matrix

( Cramer’s Rule). The result(s) are your allocated reciprocal costs for each service department. Summing

the individual service departments will find a total that is equal to the total of the pre-allocated costs.

9. When allocating the costs from the service departments to the production departments, use the total

4. Explain why the matrix method can be seen as more efficient than the traditional method.

The matrix method demonstrated here avoids the double counting problem of the traditional method and

provides an intermediate cost, which can be directly associated with each service department. In addition,

there is the added benefit of traceability. With the use of a spreadsheet for the calculations, computational

7-11

Education.