Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-38 (continued)

3. The total value chain cost provides the firm a long-term perspective of

the product cost, in addition to the short term manufacturing cost.

Different industries have different cost structures. For example, firms in

5-39 Resource and Activity-Based Cost Drivers (25 min)

1. The activity based cost pools are determined from the percent-of-use

information; for example, total setup cost = $157,500 = (.15 × $850,000)

+ (.2 × $150,000).

Factory

Costs Setup Assembly

Inspect

&Finishing

Packagin

g

Salaries $ 850,000 $127,500 $ 467,500 $ 170,000 $ 85,000

2. The activity rates are determined as follows:

Safe-V Safe-T

Total Activity

Consumption

Activity

Costs

Activity-

based

Rates

Batches 250 600 850 $157,500 $185.29

Units 60,000 72,000 132,000 $997,500 $ 7.56

5-21

3. The per unit activity-based costs are $14.18 for Safe-V and $18.63 for the

Safe-T

Activity Requirements

Activity-Based

Costs/Unit

Safe-V Safe-T Safe-V Safe-T

Setup 250 600 $ 0.77 $ 1.54

Assembly 60,000 72,000 $ 7.56 $ 7.56

Inspect and Finish 0.2 0.3 $ 1.85 $ 2.77

Packaging 0.1 0.15 $ 0.51 $ 0.76

Materials per unit $3.50 $6.00 $ 3.50 $ 6.00

Total Cost per Unit $ 14.180 $ 18.628

5-39 (continued)

4. The activity-based information can be used by EEI to set prices and

assess the profitability of its two product lines.

5. The collection of more accurate cost driver data can only be justified when

the cost of data collection and analysis is less than the expected benefit.

Management would have to decide whether they think their decisions would

change based on the more accurate data. If not, then the extra effort and cost

associated with collecting the new data would not be justified. In this situation,

for example, an employee might not be assigned to a single job function. If

5-22

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-40 Activity-Based Costing; Customer Group Cost Analysis (40 min)

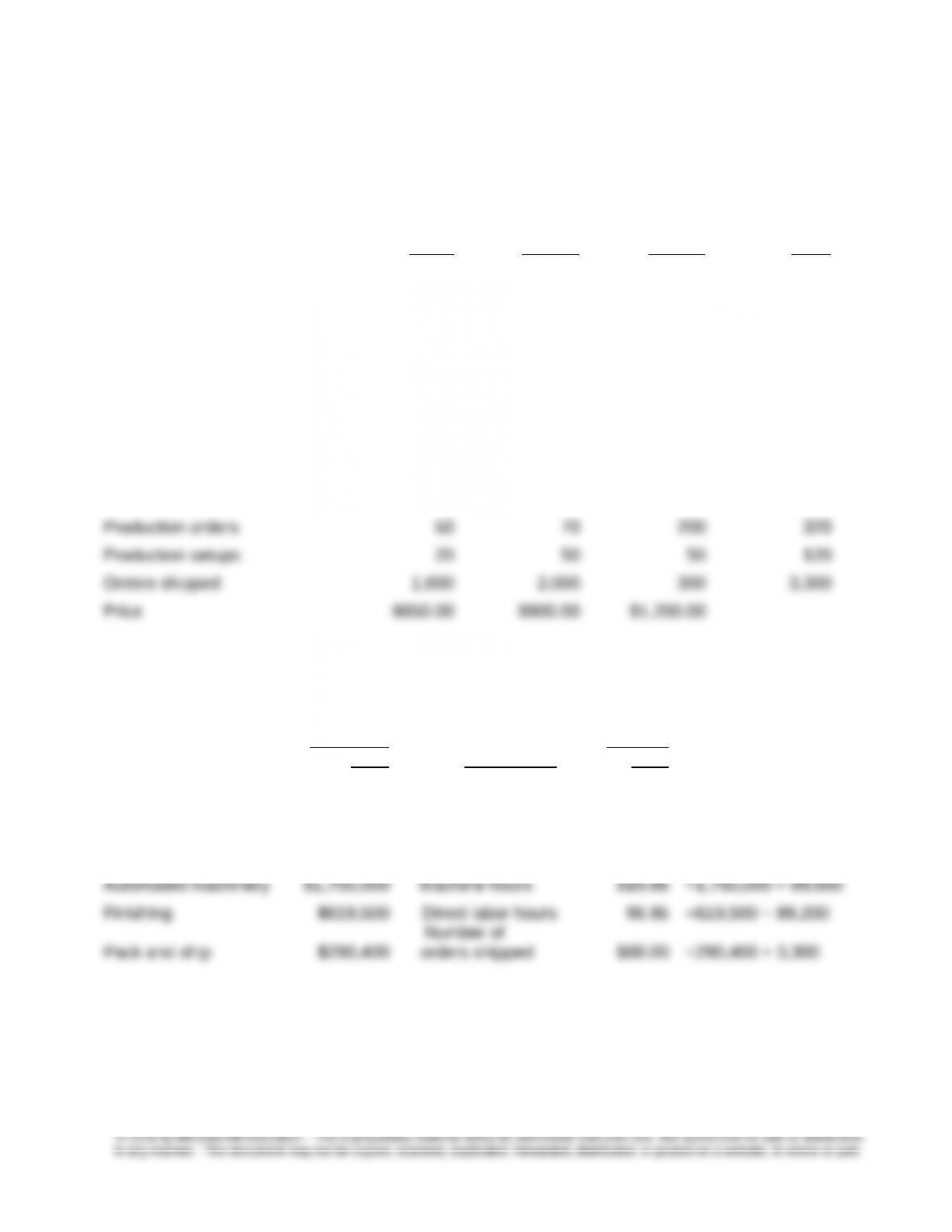

1. First, obtain the total levels for activity cost drivers:

Product Lines Value Quality Luxury Total

Units produced 15,000 5,000 600 20,600

Direct materials cost per unit $80 $50 $110

Total direct materials cost $ 1,516,000

Number of parts per unit 30 50 120

Total parts 772,000

Direct labor hours per unit 4 5 7

Total labor hours 89,200

Machine hours per unit 3 7 15

Total machine hours 89,000

Then, obtain the activity rates:

Budgeted

Cost Cost Driver

Activity

Rate

Materials handling $349,600 Number of parts $0.45 =$349,600 ÷ 772,000

Product scheduling $160,000

Number of

production orders $500.00 =160,000 ÷ 320

Setup labor $216,000 Number of setups $1,800.00 =216,000 ÷ 120

5-23

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-40 (continued -1)

Finally, determine unit and total costs ,as follows:

Value Quality Luxury

Direct Materials $80.00 $50.00 $110.00

Direct Labor $60.00 $75.00 $105.00

Overhead:

Materials handling $13.50 $22.50 $54.00

Product Scheduling $1.67 $7.00 $166.67

Setup Labor $2.40 $18.00 $150.00

2. Volume-based results $3,385,500 ÷ 89,200 DLH = $37.95 per DLH (rounded to 2

decimal places)

Value Quality Luxury

Direct Materials $80.00 $50.00 $110.00

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-40 (continued -2)

3. The new activity rates based on practical capacity are as follows.

Budgeted

Cost

Cost Driver

Practical

Capacity

Practical

Capacity-Based

Rates

Materials handling $ 349,600 Number of parts 990,000 $ 0.35

Product scheduling 160,000

Number of

production orders 800 200.00

Setup labor 216,000 Number of setups 200 1,080.00

$ 3,385,500

Note that the rates have changed significantly from the calculations in part 1

above, because there is a significant level of unused capacity in many of the

activities. This information could be used by management to calculate unit

ABC-based costs using the practical capacity rates, and thereby identify the

cost of unused capacity. Moreover, the information about capacity utilization

can be used to help bring resource spending in line with resource usage. As

5-25

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-40 (continued – 3)

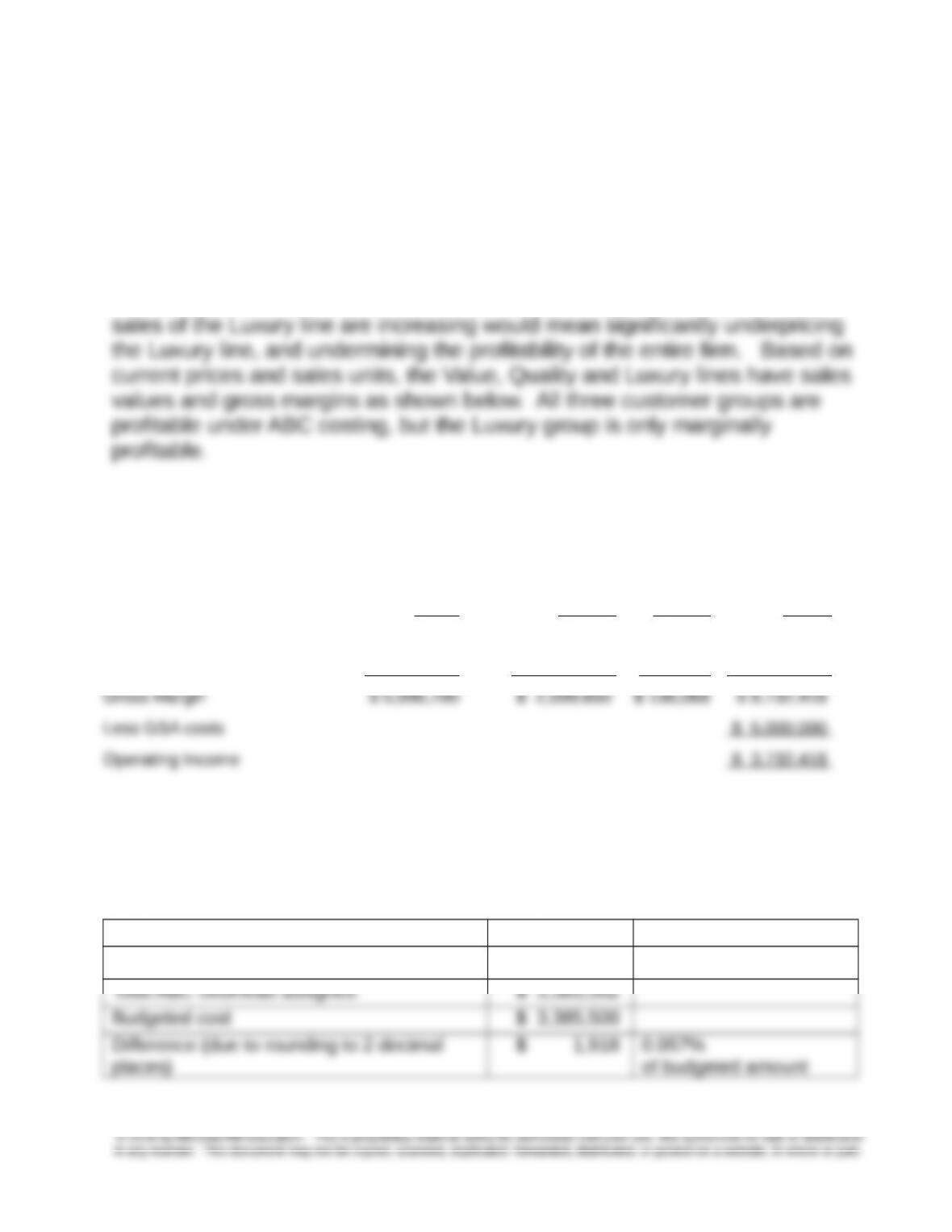

4. The ABC costing shows clearly how expensive the Luxury group is to

produce. The volume-based approach fails to account for the activity usage

of the Luxury line, and undercosts it significantly. ABC allows FFI to better

understand how its costs will increase with the expected increased production

of the Luxury line, and how it will have to adapt its pricing practices

accordingly. Continued use of the volume-based approach at a time when

Profitability by Customer Group

Profitability by Customer Group

Value Quality Luxury Total

Sales Value of each product $ 9,750,000 $ 4,500,000 $720,000 $ 14,970,000

Less ABC Manufacturing cost $ 3,753,300 $ 1,900,350 583,932 $ 6,237,582

Note that due to rounding the total ABC manufacturing costs assigned are

$1,918 more than the actual total costs. This is an insignificant difference that

is not likely to change any management actions.

Total ABC costs $ 6,237,582

Less: direct labor and direct materials $ 2,854,000

5-26

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-41 Volume-based Costing Versus ABC (35 min)

Product A Product B Product C

Materials $50.00 $114.40 $65.00

Labor $20.00 $12.00 $10.00

Overhead* $120.00 $72.00 $60.00

Total Cost $190.00 $198.40 $135.00

1. Current Costing system

Product A Product B Product C

Actual Selling Price $286.00 $255.60 $310.00

Product Manufacturing Cost $190.00 $198.40 $135.00

Gross Margin $96.00 $57.20 $175.00

Gross Margin Ratio 33.57% 22.38% 56.45%

Product costs based on the activity-based costing system

(calculate on per unit basis) Product A Product B Product C

Direct Materials 50.00 114.40 65.00

Direct Labor 20.00 12.00 10.00

Factory Overhead:

Setups (a) 1.80 0.90 5.40

Materials Handling (b) 44.00 5.50 77.00

Hazardous Control (c) 62.50 22.50 150.00

Product Manufacturing Cost 214.00 169.79 373.10

Gross Margin $72.00 $85.81 ($63.10)

Gross Margin Percentage 25.17% 33.57% -20.35%

5-27

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-41 (continued -1)

Notes:

(a) Setups:

Cost per setup: $9,000 ÷ (2 + 5 + 3) = $900 per setup

(b) Materials handling:

Cost per pound = $110,000 ÷ (400 + 250 + 350) = $110 per pound

Product A = 400 × $110 = $44,000; $44,000÷1,000 = $44.00 per unit

(c) Waste and hazardous disposals:

Cost per disposal: $250,000 ÷ (25 + 45 + 30) = $2,500 per disposal

Product A = 25 × $2,500 = $ 62,500; $ 62,500 ÷ 1,000 = $ 62.50/unit

(d) Quality inspections:

Cost per inspection = $75,000 ÷ (30 + 35 + 35) = $750 per inspection

Product A = 30 × $750 = $22,500; $22,500 ÷ 1,000 = $22.50 per unit

(e) Utilities:

Cost per MH = $66,000 ÷ (2,000 + 7,000 + 1,000) = $6.60 per MH

Product A = 2,000 × $6.6 = $13,200; $13,200÷1,000 = $13.20 per unit

5-28

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-41 (continued-2)

2. Comparison of reported product costs, new target price, actual selling price,

and gross margin (loss):

Product A Product B Product C

Product Costs:

Direct-labor system $190.00 $198.40 $135.00

Activity system $214.00 $169.79 $373.10

ABC- based product costs:

Target price $321.00 $254.69 $559.65

Gross Margin ratio 33.57% 22.38% 56.45%

ABC system:

Gross Margin $72.00 $85.81 -$63.10

Gross Margin ratio 25.17% 33.57% -20.35%

3. Strategic and Compeiive Analysis

a. Emphasizing Product C as suggested by the current direct-

labor-cost based overhead costing system is likely to lead to

the demise of the firm. The activity-based costing system shows

b. If the actual selling prices of products A & B are fair market

prices for these products and a markup of 150% is a common

industry practice, the firm needs to examine the manufacturing

cost of product A. The fact that the firm’s target price,

5-29

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-42 Volume-based Costing Versus ABC (40 min)

1. a. Predetermined factory overhead rate = $3,000,000 ÷ $600,000

= $5 per direct-labor dollar

b. Product costs and selling prices

Product Costs Mona Loa Malaysian

Direct costs:

Direct materials $4.20 $3.20

Direct labor .30 .30

$4.50 $3.50

Indirect costs:

Budgeted selling prices per pound $7.80 $6.50

2. The cost per driver unit is:

Activity Cost Driver

Budgeted

Activity

Budgeted

Cost

Cost per

Unit

Purchasing Purchase orders 1,158 $579,000 $500

Materials handling Setups 1,800 $720,000 $400

Quality control Batches 720 $144,000 $200

Roasting Roasting-hours 96,100 $961,000 $10

Blending Blending-hours 33,600 $336,000 $10

Packaging Packaging-hours 26,000 $260,000 $10

5-30