Chapter 09 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-32 Further Analysis–Degree of Operating Leverage (DOL) (40-45 min)

1. Demonstrating that DOL represents the % change in operating income

DOL = CM ÷ Operating Income (OI), for any given sales volume (Q)

New level of OI = DOL × percentage change in sales volume

= (CM ÷ OI) × (new sales volume ÷ current sales

volume)

= percentage change in Operating Income (OI)

2. Relationship between definition of “operating leverage” and the DOL

measure

First, recall the basic profit equation for operating income (OI):

OI = [(p − v) × Q] − F

where p = selling price per unit

9-20

Education.

Chapter 09 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-32 (Continued)

Second, we can rewrite the above as (where CM = total contribution

margin):

F + OI = (p – v) × Q

= CM

Third,

Finally,

DOL = (F ÷ OI) + 1.0

The advantage of the above specification is that we can more readily

9-21

Education.

Chapter 09 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-33 Cost Structure of Retailers; the Internet; Operating Leverage (15

min)

1. A retailer can significantly reduce its operating leverage and reduce

costs during a period of initial growth in e-commerce by outsourcing

its e-commerce activity to service-providers. The term ESP for “e-

commerce service provider” is sometimes used for this type of

successful.

2. Globalization presents an opportunity for the retailer to obtain the

outsourcing service in low-cost countries throughout the world.

9-22

Education.

Chapter 09 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-34 Contribution Income Statements; Sensitivity Analysis; Goal Seek

(Excel) (40-45 minutes)

1. A variety of possible spreadsheets could satisfy this requirement. One

example is the spreadsheet embedded below. The sensitivity analysis

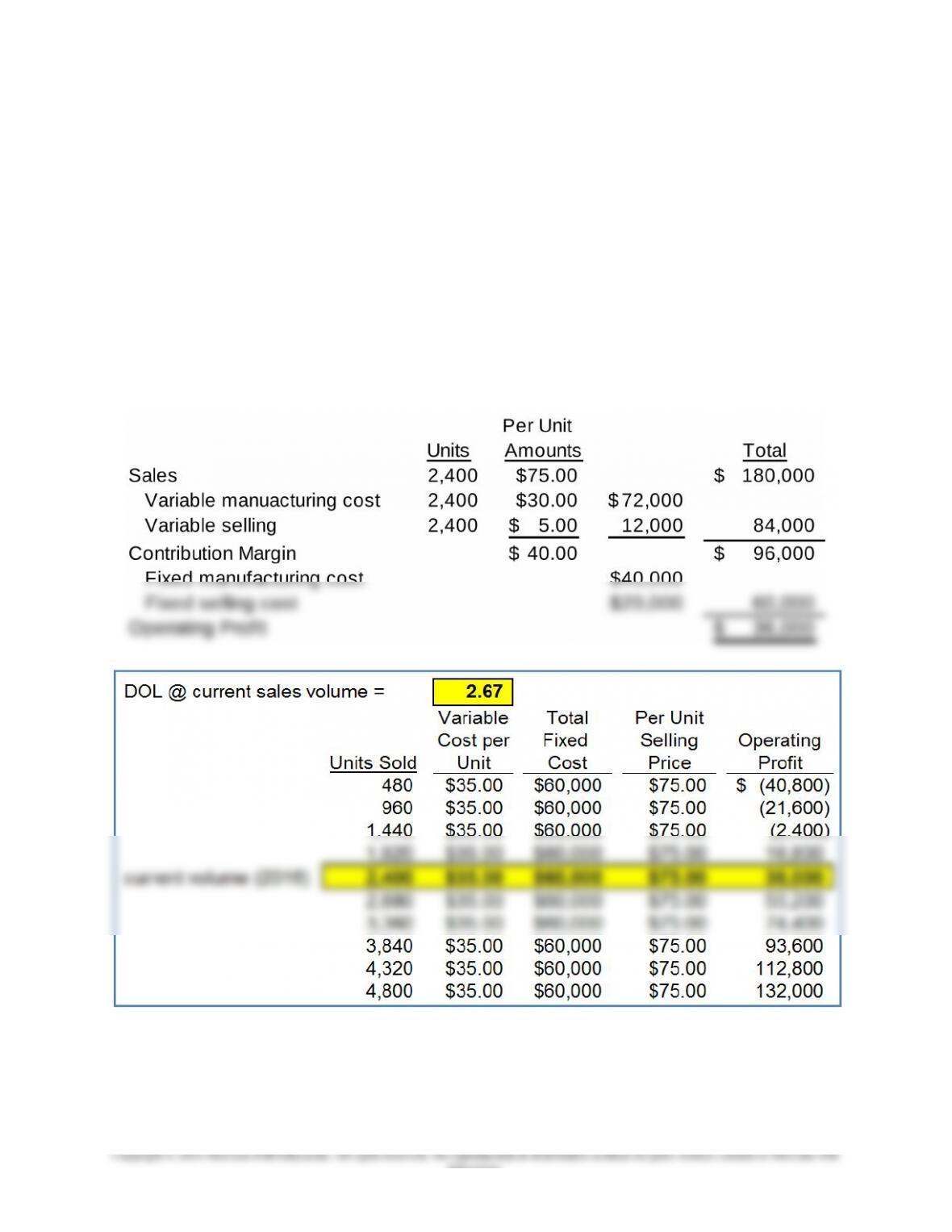

shows sales levels from 20% to 200% of 2016 expected sales of 2,400

units, and the related effect on operating profit.

At a sales volume of 2,400 units HFI’s degree of operating leverage

(DOL) is 2 2/3. From this volume level, each percentage change in sales

results in a 2.667% change in operating profit.

9-23

Education.

Chapter 09 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-34 (continued-1)

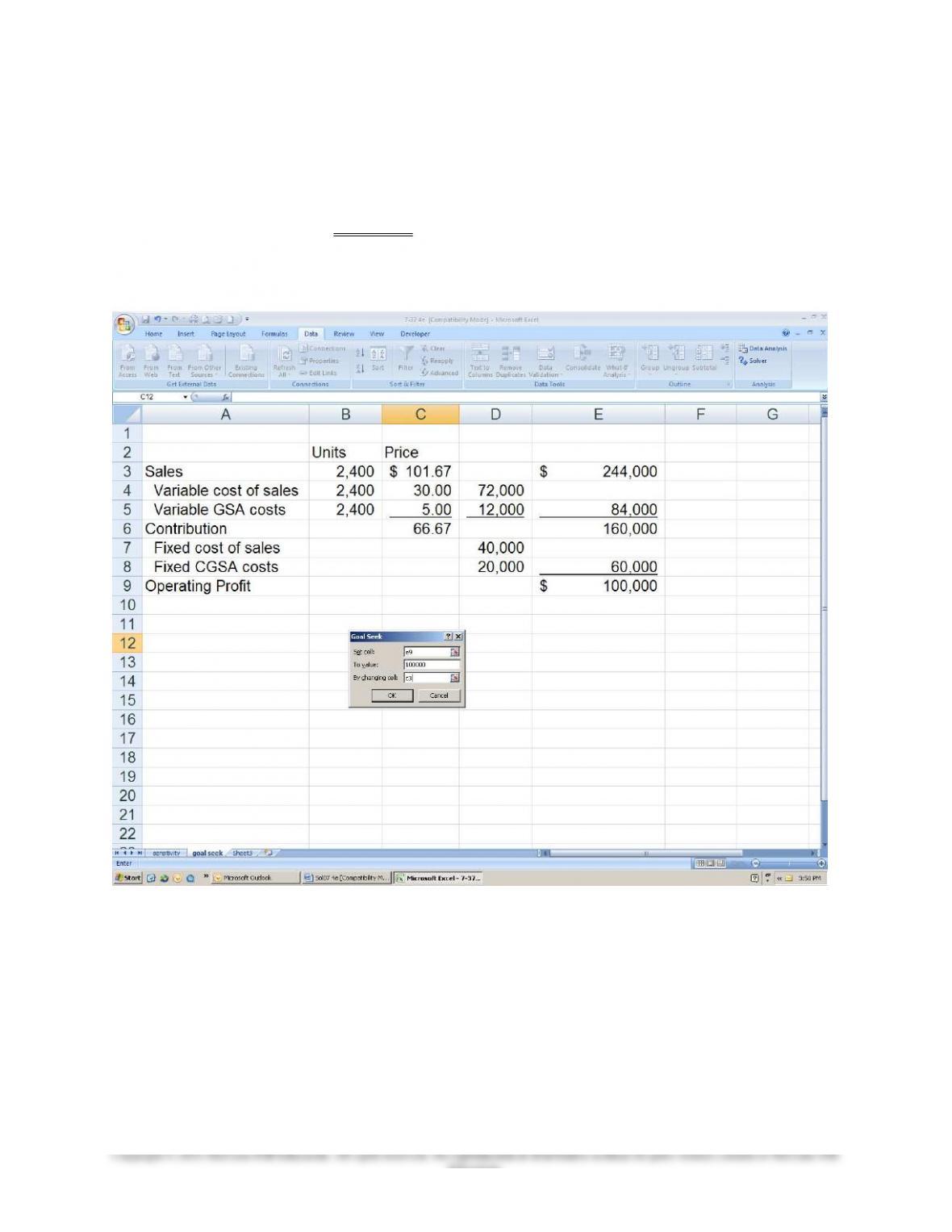

2. The Goal Seek tool is available under Data//What-if Analysis/Goal Seek

in Excel. An example of how it is used is show below. The price would

have to increase to $101.67 in order for HFI to make a $100,000 before

tax profit.

9-24

Education.

Chapter 09 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-35 CVP Analysis (20 min)

1. Contribution margin ratio (CMR) = Contribution margin ÷ Sales

Thus, CMR = ($46,000,000 − $32,200,000) ÷ $46,000,000

3. Variable cost ratio = Total variable costs ÷ Sales ($)

= (Original variable costs × 1.12) ÷ Sales ($)

= ($32,200,000 × 1.12) ÷ $46,000,000

9-25

Education.

Chapter 09 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

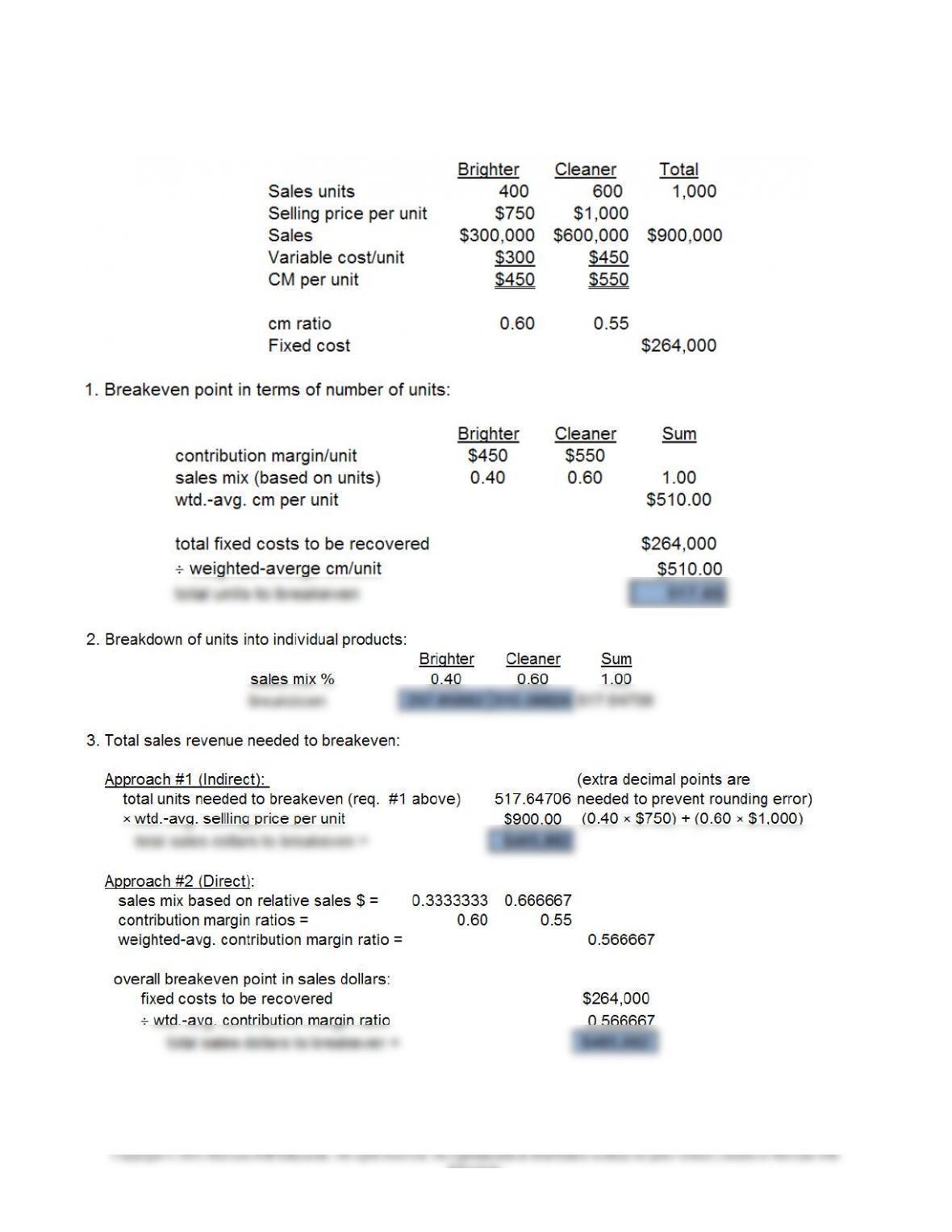

9-36 Multiple Product CVP Analysis (40-45 minutes)

9-26

Education.

Chapter 09 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-36 (Continued)

4. If machine hours are limited (i.e., if they represent a “scare resource”),

then information regarding the machine-hour consumption of each of the

two products would be important for product-planning purposes. That is,

such information could be used to calculate the contribution margin per

machine hour for each of the two products. This information, in turn, would

help guide the product-mix decision: the greater the contribution margin per

machine hour, the greater the profitability (and therefore desirability) of the

product.

An Excel spreadsheet that provides the solution for this exercise is

embedded below:

9-27

Education.

Ex 9–36.xlsx

Chapter 09 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

PROBLEMS

9-37 CVP Analysis; Strategy (45-50 min)

1. BE units = F ÷ (p − v) = $500,000 ÷ ($80 − $52)/unit = 17,857 units

= $500,000 ÷ 0.35 = $1,428,571

2. πB= Sales − variable costs − fixed costs

= [Q × (contribution margin/unit)] − F

Contribution Income Statement:

Sales (20,000 units × $80.00/unit) =

$1,600,00

0

Less: Variable costs (20,000 units × $52.00/unit) =

$1,040,00

0

Contribution Margin = $560,000

3. Margin of safety (MOS) = Budgeted sales volume – Breakeven sales

volume

MOS ratio = MOS ÷ Budgeted sales volume

Both the MOS and the MOS ratio refer to the extent to which sales

could fall before losses are realized. In this sense, they are rough

measures of operating risk and are therefore helpful in addressing

9-28

Education.

Chapter 09 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

inherent uncertainty in the profit-planning process.

9-29

Education.