Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

Note: An Excel spreadsheet solution file for this assignment is embedded below. You can

open this “object” by doing the following:

1. Right click anywhere in the worksheet area below.

2. Select “worksheet object” and then select “Open.”

3. To return to the Word document, select “File” and then “Close and return to…”

while you are in the spreadsheet mode. The screen should then return you to

this Word document.

Ex. 15-34 7e.xlsx

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15-35 Traditional ABC Costing (50 minutes)

Standard MH per unit = 32,000 MH 6,400 units = 5 MH per unit

No. of units manufactured during the period = standard allowed MH standard

MH/unit = 30,000 MH 5 MH/unit = 6,000 units

Budgeted no. of units/setup = 6,400 units 32 set-ups = 200 units/set-up

Standard no. of setups for the units manufactured = 6,000 200 = 30

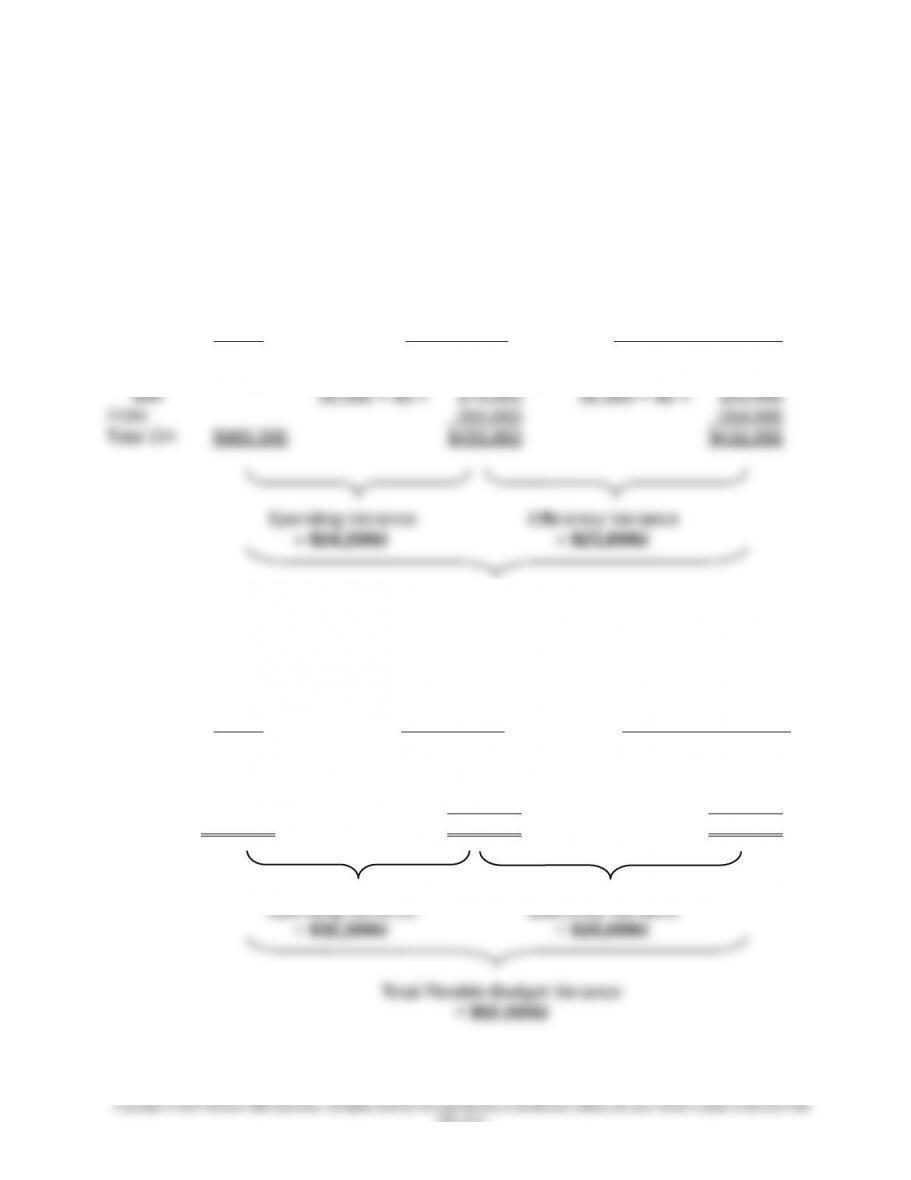

FB based on Inputs FB based on Outputs

(i.e., based on actual (i.e., based on standard

1. Actual activity units) allowed activity units)

VOH:

Setup 28 × $600 = $ 16,800 30 × $600 = $ 18,000

Total Flexible-Budget Variance

= $48,000U

FB based on Inputs FB Based on Outputs

(i.e., on actual (i.e., based on standard

2. Actual activity units) allowed activity units)

VOH:

Setup 28 × $2,600 = $ 72,800 30 × $2,600 = $ 78,000

MH 35,000 × $5 = 175,000 30,000 × $5 = 150,000

FOH: 200,000 200,000

Total OH $480,000 $447,800 $428,000

15-32

Education.

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15-35 (Continued)

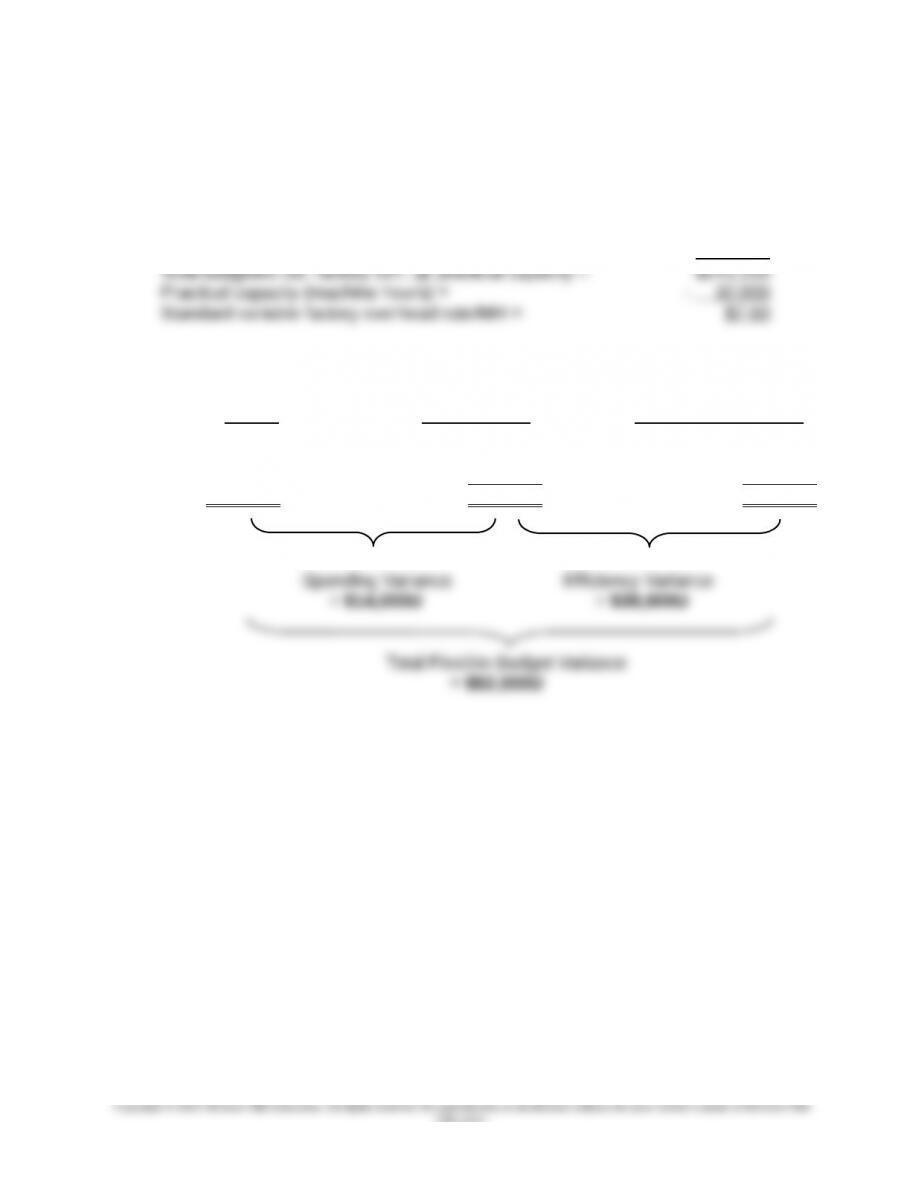

3. Standard variable overhead application rate = budgeted variable manufacturing

overhead in the master budget practical capacity (MH)

Setup cost = $64,000 + ($600/setup × 32 setups) = $ 83,200

Applied based on machine hours = 32,000 hours × $5.00/hr. = 160,000

FB based on Inputs FB Based on Outputs

(i.e., on actual (i.e., on standard

Actual activity units) allowed activity units)

VOH: 35,000 × $7.60 = 266,000 30,000 × $7.60 = 228,000

FOH: 200,000 200,000

Total OH $480,000 $466,000 $428,000

Notice that assumptions made regarding the number and type of activity measures used

to apply standard overhead costs to production can affect both the total flexible-budget

variance and the components of this variance. For this reason, the activities used to

construct flexible-budgets for control purposes should be carefully selected.

15-33

Education.

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15-36 ABC and Practical Capacity; Spreadsheet Application (50 minutes)

15-35

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15-36 (Continued)

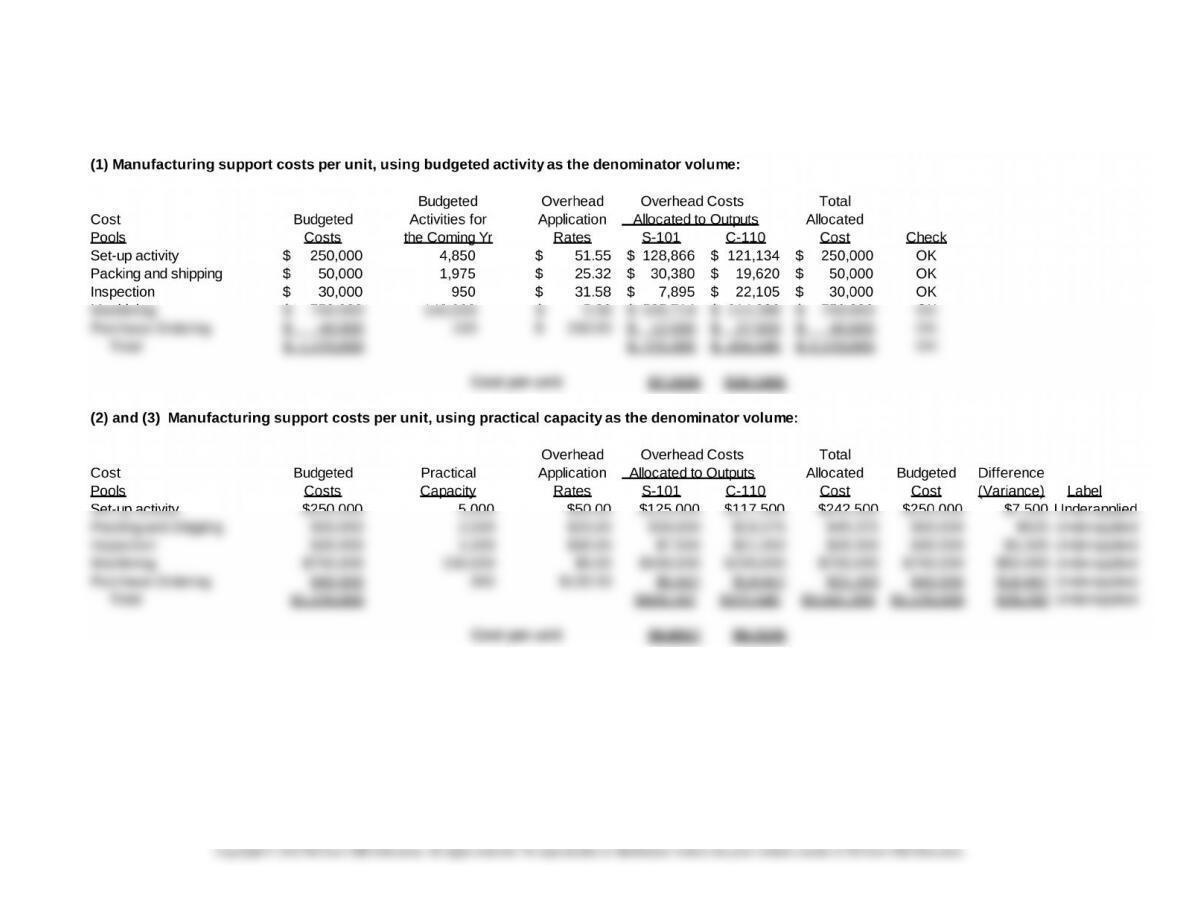

The difference (variances) reported when the denominator activity level is defined as

“practical capacity” can be interpreted as the “cost of unused capacity.” This information

can be reported over time (time-series basis) to management to determine whether

some of the available capacity should be eliminated or whether some alternative uses to

this available capacity can be made. Notice that when practical capacity is used as the

denominator, there is consistency between the numerator and denominator: the

Note: An Excel spreadsheet solution file for this assignment is embedded below. You

can open this “object” by doing the following:

1. Right click anywhere in the worksheet area below.

2. Select “worksheet object” and then select “Open.”

3. To return to the Word document, select “File” and then “Close and return

to…” while you are in the spreadsheet mode. The screen should then return

you to this document.

15-36

Ex. 15-36 7e.xlsx

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15-37 Use of Payoff Tables (Appendix); Spreadsheet Application (30-45 minutes)

(1) Expected value of the decision to investigate the variance:

E(Investigate) = [(I × (1 −p)] + [(I + C) × p]

(2) Payoff table:

Management States of Nature (prob.) Expected

Action Random (75%) Systematic (25%) Value

(3) Let p = the indifference probability, that is, the probability of for a nonrandom

variance such that management is indifferent between the two courses of action,

investigate or do not investigate:

p = I ÷ (L − C)

where I = the expected cost to conduct an investigation, L = expected loss

associated with leaving an out-of-control process out of control (i.e., the present

value of losses the organization will experience until the next decision point), and

C = the expected cost to correct the process if the variance is found to have a

nonrandom cause.

Thus, if the probability (p) for a nonrandom cause (or causes) is 4.96%,

management would be indifferent, in expected value terms, between investigating

15-37

Education.

15-37 (Continued)

Note: An Excel spreadsheet solution for this exercise is embedded below. You can open

this “object” by doing the following:

1. Right click anywhere in the worksheet area below.

2. Select “worksheet object” and then select “Open.”

3. To return to the Word document, select “File” and then “Close and return to…”

while you are in the spreadsheet mode. The screen should then return you to

this document

15-38

Education.

Ex. 15-37 7e.xlsx

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

PROBLEMS

15-38 Capacity Levels and Fixed Overhead Rates (60 minutes)

1. As the name suggests, maximum (theoretical) capacity is the maximum output

level for the plant, one that assumes operating at maximum efficiency. This

level of productivity suggests no “down time” for machine maintenance, no

internal disruptions to the manufacturing process, and no slack in external

(expected sales demand over an upcoming three- to five-year period).

2. A revised variance report for Yuba Machine Company using expected

(budgeted) activity as the basis for applying fixed factory overhead is

presented below.

Yuba Machine Company

Revised Variance Report

for Six Months ended May 31, 2017

Applied

Actual Overhead

Costs Costs Variance

Total variable factory overhead $120,220 $120,000 $ (220 )

Fixed factory overhead:

Salaries $ 39,000 $ 40,000 $ 1,000

Depreciation and amortization 25,000 25,000 –

Depreciation and amortization:

40,000 DLHs × $0.625/DLH = $25,000

Other expenses: 40,000 DLHs × $0.375/DLH = $15,000

15-39

Education.

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15-40

Education.