Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18-45 (continued -1)

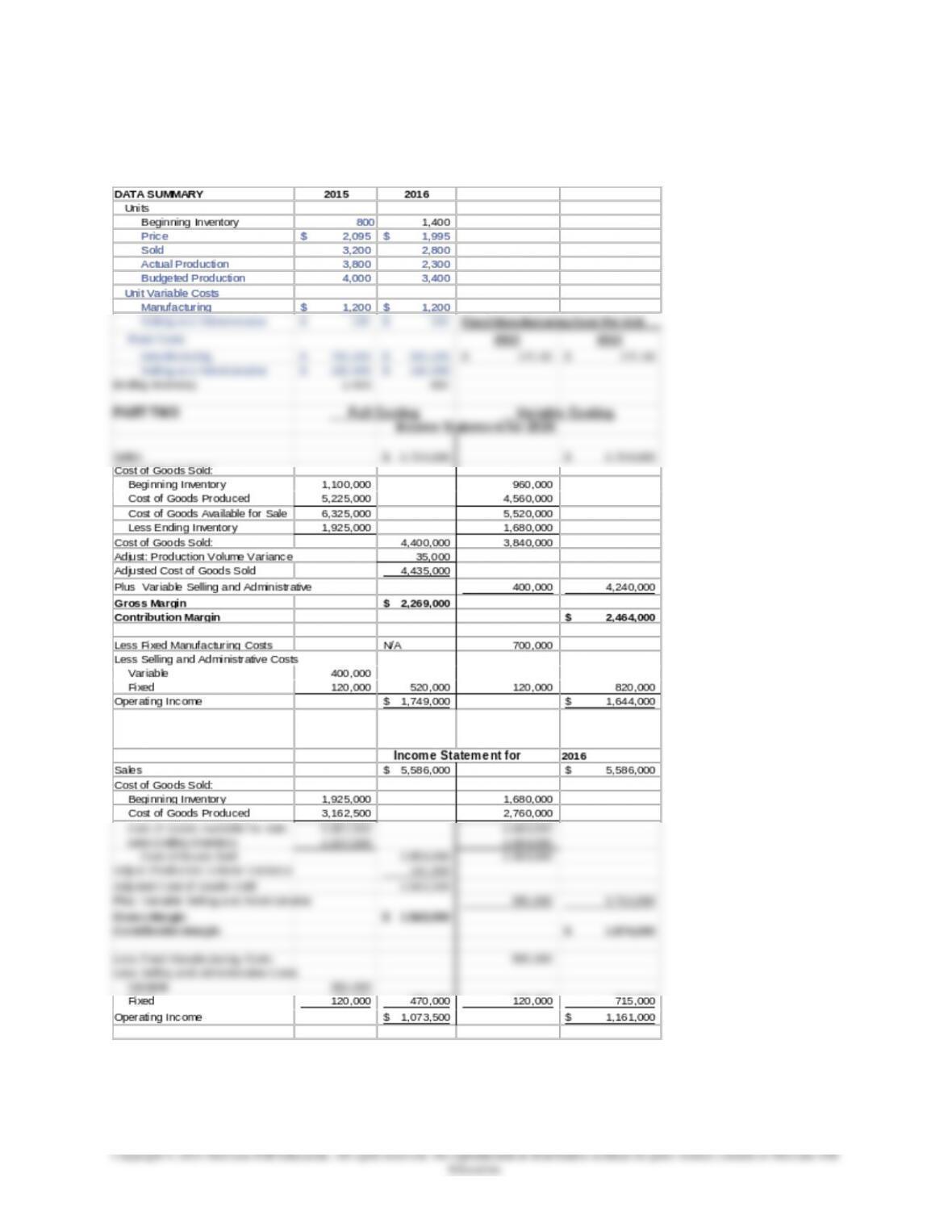

PART THREE

Reconciling Difference in Operating Income between Full and Variable Costing

2015 2016

Change in Inventory in Units 1,000 (1,000)

Multiply times Fixed Overhead Rate $ 8.00 $ 8.00

=Difference in Operating Income $ 8,000 $ (8,000)

An increase in inventory units means full costing operating income is higher

than variable costing operating income.

18-41

Education.

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18-46 Profit Centers: Comparison of Variable and Full Costing

(Underapplied Overhead) (30 min)

1., 2.

18-42

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18-46 (continued -1)

2. (continued)

PART THREE

Reconciling Difference in Net Income between Absoprtion and Variable

Costing

2015 2016

Change in Inventory in Units 600 (500)

Multiply times Fixed Overhead Rate $ 175 $ 175

= Difference in Net Income $ 105,000 $ (87,500)

An increase in inventory units means full costing operating income is higher

than variable costing operating income.

A decrease in inventory units means variable costing operating income is

higher than full costing operating income.

In 2015, inventory units increased, so operating income for full costing is

higher than variable costing in that year.

In 2016, inventory units decreased, so in that year operating income for

variable costing is higher than full costing.

Additional Note on the Production Volume Variance: A recent CFO

magazine item notes how the use of full cost accounting in the auto

industry has biased profit reporting in that industry. See, Marielle Segarra,

“Accounting: Lots of Trouble,” CFO, March 2012, pp. 29-30.

18-43

Education.

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

3.

Memo

TO: Mr. Mark Hancock

FROM:

DATE:

The difference in operating income between variable costing

and full costing is due to the fact that the level of units in finished

goods inventory increased by 600 units (from 800 to 1,400) in 2015

and decreased by 500 units (from 1,400 to 900) in 2016. The

variable cost income statements do not include fixed manufacturing

costs in inventory, but treat these costs instead as a cost of the

current period. Thus, variable costing income statements are not

affected by changes in inventory levels.

You may use the variable cost income statements as a more

reliable measure of operating income when fixed manufacturing costs

are high and inventory changes significantly, as in this case. The

variable cost statements.

Note that the production volume variance does not affect the

difference between variable and full costing income. The difference in

income is fully explained by the change in inventory multiplied times

the fixed overhead rate, as illustrated in the end of part 2 above.

18-44

Education.

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18-47 Balanced Scorecard (15 min)

Solution for problem 2-35

1. Medical University’s strategy should encompass a focus on the

quality of its clinical care, education, and research. The relative size

of the healthcare system is important as a way to attract third party

payers, providers, and patients. A large hospital system tends to offer

a greater breadth of services, which often increases the clinician’s

level of expertise. A physician at a larger institution will most likely

2. Yes. The balanced scorecard goes beyond simply monitoring

financial performance. Because the four areas: financial

performance, customer satisfaction, internal processes, and learning

factors.

3.

Financial: operating margin, cost per discharge, days in

accounts receivable

Customer: patient satisfaction, employee satisfaction, referring

18-45

Education.

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18-47 (continued -1)

4. One of the hardest challenges is convincing employees that the

balanced scorecard is not simply a management tool. The reluctance

of employees to implement the balanced scorecard may prevent the

organization from achieving its strategic goals. In order to increase

buy-in from employees, management needs to educate them on the

relevance of the balanced scorecard. A hospital in the Southeast

realized that they needed to educate employees not only on how the

18-46

Education.

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18-48 Balanced Scorecard (15 min)

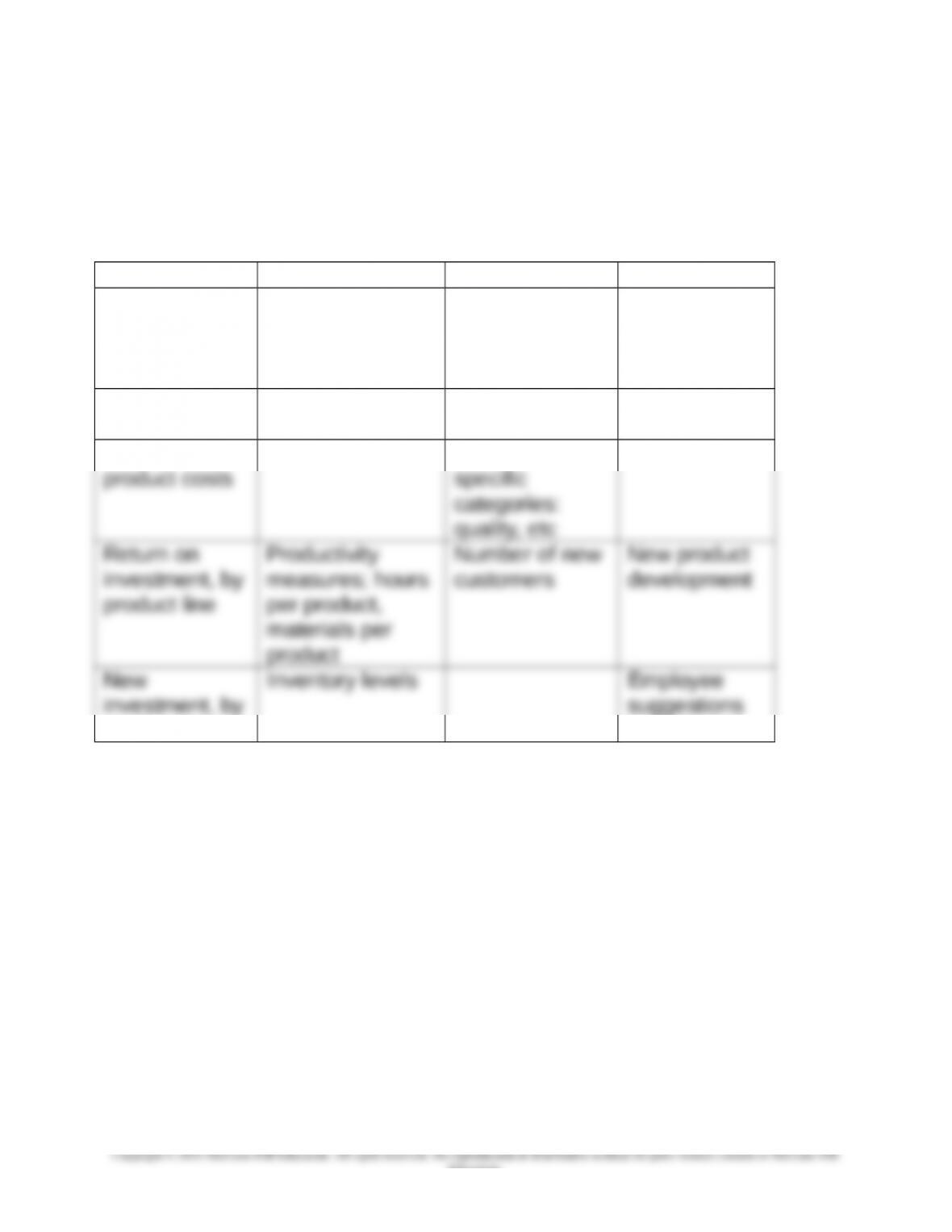

Solution for problem 2-39; Balanced Scorecard for Fowler’s Farm

There are a number of possibilities for determining both the number

and types of perspectives for the balanced scorecard, and for

determining the critical success factors which belong under each

perspective. The answer below is representative of a balanced

scorecard that would be a good fit for the Fowler farm. This

Operations

crop rotation; number of fields in rotation

inventory of supplies and parts, by type of equipment, cost and

date purchased

weather forecast, days missed, important weather changes

irrigation schedule; % days on schedule

prices received for each major product

interest cost

Employees

turnover (number and percent)

accidents (number )

18-47

Education.

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18-48 (continued -1)

Regulatory Compliance and Environmental

compliance with local, state and federal laws on tobacco

farming

compliance with FDA regulations regarding handling raw milk

usage of restricted chemicals known to have negative

environmental effects (amount, percent)

Customer

orders shipped on time (number and percent)

quality complaints (number, percent)

18-48

Education.

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18-49 Balanced Scorecard (15 min)

Solution for problem 2-43, The Tartan Corporation.

An example of a balanced scorecard for Tartan Corp follows:

Financial Internal Customer Employee

Sales, sales

growth, by

product and

region

Cycle time Lead time Training hours

Earnings, as

above

Waste of

materials

Retention Retention

ABC-based

Rework Satisfaction, in

Satisfaction

product line

18-49

Education.

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

PROBLEMS

18-50 Profit Center Limitations (25 min)

This question is intended primarily for class discussion. The objective

of the question is to have the class understand and discuss some of the

key limitations of the profit center approach for strategic performance

measurement, and to understand some of the methods for addressing

these limitations. The question will work best if the class has some prior

experience in either intermediate accounting, financial statement

analysis, or both. The Merchant and Sandino article is one of many that

have addressed the limitations of profit centers over the years, and it is

one of my favorites. Instructors may have their own favorite in this

regard, and could add their own favorite reading assignment on the topic

as part of the class assignment for this question,

1. Merchant and Sandino (especially in the full article) present a solid

case for moving away from the pure profit center evaluation, and

incorporating one or more of their four suggested approaches for

addressing the problem. Students who have had a solid financial

accounting background including for example, the financial

intermediate course or the financial statement analysis course, will be

18-50

Education.