Chapter 16 – Operational Performance Measurement: Further Analysis of Productivity and Sales

Chapter 16

Operational Performance Measurement: Further

Analysis of Productivity and Sales

Learning Objectives

1. Explain the strategic role of the flexible budget in analyzing productivity and sales.

2. Calculate and interpret the measures for total productivity, partial operational productivity and

partial financial productivity.

3. Use the flexible budget to calculate and interpret the sales quantity, sales mix, market size, and

market share variances.

4. Use the flexible budget to analyze sales performance over time.

New in this Edition

Two New Real World Focus (RWF) items related to productivity

Seven new or revised problems

Teaching Suggestions

The critical success factors for many firms include the effectiveness of sales and marketing efforts,

productivity of operations, and the retention and acquiring profitable customers. This chapter explains

how variance analysis is used to analyze the effectiveness of sales and marketing, the productivity of

operations, and, to complete analyses of marketing effectiveness, the identification of customer

profitability. The analytic schemes for sales and marketing analysis and for productivity are a natural

follow-up to the standard costing material presented in Chapters 15 and 16. A unique aspect of the

presentation is its unified approach — the different forms of analysis are shown in a way that shows

clearly how they are inter-related and can be integrated.

The three topics can be covered in three class periods. However, because of time constraints, you may

find you can only spend one or two days on this chapter, covering only two of the three topics. You might

begin with a short presentation on the strategic role of marketing effectiveness and explain the business

purpose of the variances — the control of the marketing and sales function and effectiveness in attaining

the strategic goals. Then give an overview of all the variances and then focus on the selling price and

volume variances before moving on to sales mix, sales quantity, market share, and market size variances.

Finally, move on to customer profitability analysis and productivity analysis.

16-1

Education.

Chapter 16 – Operational Performance Measurement: Further Analysis of Productivity and Sales

Assignment Matrix

End-of-Chapter Exercises & Problems Learning Objectives Text Features

7e

EOC

6e

EOC

Transition

6e to 7e

X = included in Connect

Time

1.

Strategic role of productivity and sales

2.

Total and partial productivity

3.

Sales quantity, mix, market size and

variances

4.

Sales performance over time

Strategy

Service

International

Ethics

Sustainability

Brief Exercises

16-22 Moved to 16-25

16-22 16-28 Moved X 05 min X

16-23 16-23 X 05 min X

16-24 16-24 X 05 min X

16-25 Moved to 16-28

16-25 16-22 Moved X 05 min X

16-26 16-26 X 05 min X

16-27 16-27 X 05 min X

16-28 Moved to 16-22

16-28 16-25 Moved X 05 min X

Exercises

16-29 16-29 – 15 min. X X

16-30 16-30 – 15 min. X X X X

16-31 16-31 – 15 min. X X

16-32 16-32 X 20 min. X

16-33 16-33 X 20 min. X

16-34 16-34 – 15 min. X X

16-35 16-35 – 20 min. X X

16-36 16-36 – 20 min. X

16-37 16-37 – 20 min. X

16-38 16-38 – 20 min. X X

16-39 16-39 X 30 min. X X

16-40 16-40 X 25 min. X

Problems

16-41 16-41 Revised – 15 min. X

16-42 16-42 Revised – 30 min. X

16-43 16-43 Revised – 15 min. X

16-44 16-44 Revised – 45 min. X

16-45 16-45 Revised – 30 min. X

16-46 16-46 – 30 min. X

16-47 16-47 – 20 min. X

16-48 16-48 – 15 min. X X

Continued on next page …

16-2

Chapter 16 – Operational Performance Measurement: Further Analysis of Productivity and Sales

Assignment Matrix continued

End-of-Chapter Exercises & Problems Learning Objectives Text Features

7e

EOC

6e

EOC

Transition

6e to 7e

X = included in Connect

Time

1.

Strategic role of productivity and

sales

2.

Total and partial productivity

3.

Sales quantity, mix, market size and

riances

4.

Sales performance over time

Strategy

Service

International

Ethics

Sustainability

16-49 16-49 Revised – 25 min. X X

16-50 16-50 – 40 min. X

16-51 16-51 – 30 min. X X X

16-52 16-52 Revised – 20 min. X

16-53 16-53 – 20 min. X X

16-54 16-54 – 15 min. X

16-55 16-55 – 20 min. X X

16-56 16-56 – 35 min. X X

16-57 16-57 – 25 min. X X

16-58 16-58 – 30 min. X

Lecture Notes

Productivity

Productivity is the ratio of output to input. The higher the ratio is, the better.

Common Benchmark for Productivity Measures

• performance of a previous year,

• performance of another division of the firm,

• performance of a competitor, and

• a target measure set by management.

Classification of productivity measures:

Total productivity

Partial productivity

Operational productivity

Financial productivity

Total productivity measures the relationship between the output attained and the total input costs of all

the input resources.

16-3

Education.

Chapter 16 – Operational Performance Measurement: Further Analysis of Productivity and Sales

The numerator can be either in number of units or in dollar amount of the output attained.

Partial productivity focuses on only the relationship between one of the inputs such as, units of

materials, persons employed, machine hours, and the output attained. In contrast total productivity

includes all the input resources.

An operational partial productivity is the required number of units of an input resource for the

production of one unit of the output.

A financial partial productivity is the number of units of output manufactured or the dollar generated

for each dollar of an input resource the firm spent.

Difference In Computations Between Operational And Financial Partial Productivity

The difference is in the denominator– an operational partial productivity uses the units of the input factor

while a financial partial productivity uses the dollar amount of the input factor.

Advantage of total productivity measures

Using a total productivity measure decreases the possibility of manipulating one or two manufacturing

factors to improve the measure.

Partitioning Financial Productivity

A financial productivity can be separated into changes due to:

productivity change – the difference between the actual and the budgeted quantity of input resources

for the manufacturing of the output,

input price change – the effects of differences in prices for the input resource between the actual price

paid and the budgeted (or a benchmark) price, and

output change – the change in cost due to changes in units of output.

16-4

Education.

Chapter 16 – Operational Performance Measurement: Further Analysis of Productivity and Sales

An Example:

Current year: Manufactured 500 units with 1,000 pounds of materials at $4 per pound.

Last year: Manufactured 400 units with 1,000 pounds of materials at $5 per pound.

Productivity: Current year = 500/1,000 = 0.5; Last year = 400/1000 = 0.4

Output unit: 500 500 500 600

1/Productivity: × 2 × 2.5 × 2.5 × 2.5

Input cost: × $4 × $4 × $5 × $5

$4,000 $5,000 $6,250 $7,500

Productivity Change Input Price Change Output Change

= $4,000 – $5,000 = $5,000 – $6,250 = $6,250 – $7,500

= $1,000 Favorable = $1,250 Favorable = $1,250 Favorable

Measuring Productivity In Service Industries Or Not-For-Profit Organizations

Same concepts for measuring productivity are applicable to service industries and not-for-profit

organizations.

Some limitations:

oimprecise output measures,

olack of definite relationships between output and input resources, and

othe absence of revenue for not-for–profit organizations.

Managing Marketing effectiveness

Marketing effectiveness includes achieving budgeted operating income, attaining budgeted market share,

and adapting to changes in the market. To be effective management needs to monitor changes in selling

prices, sales volumes, sales mix, market sizes, and market shares on operations and the strategy of the

firm so that appropriate actions can be taken at the earliest time in responses to the changes. The

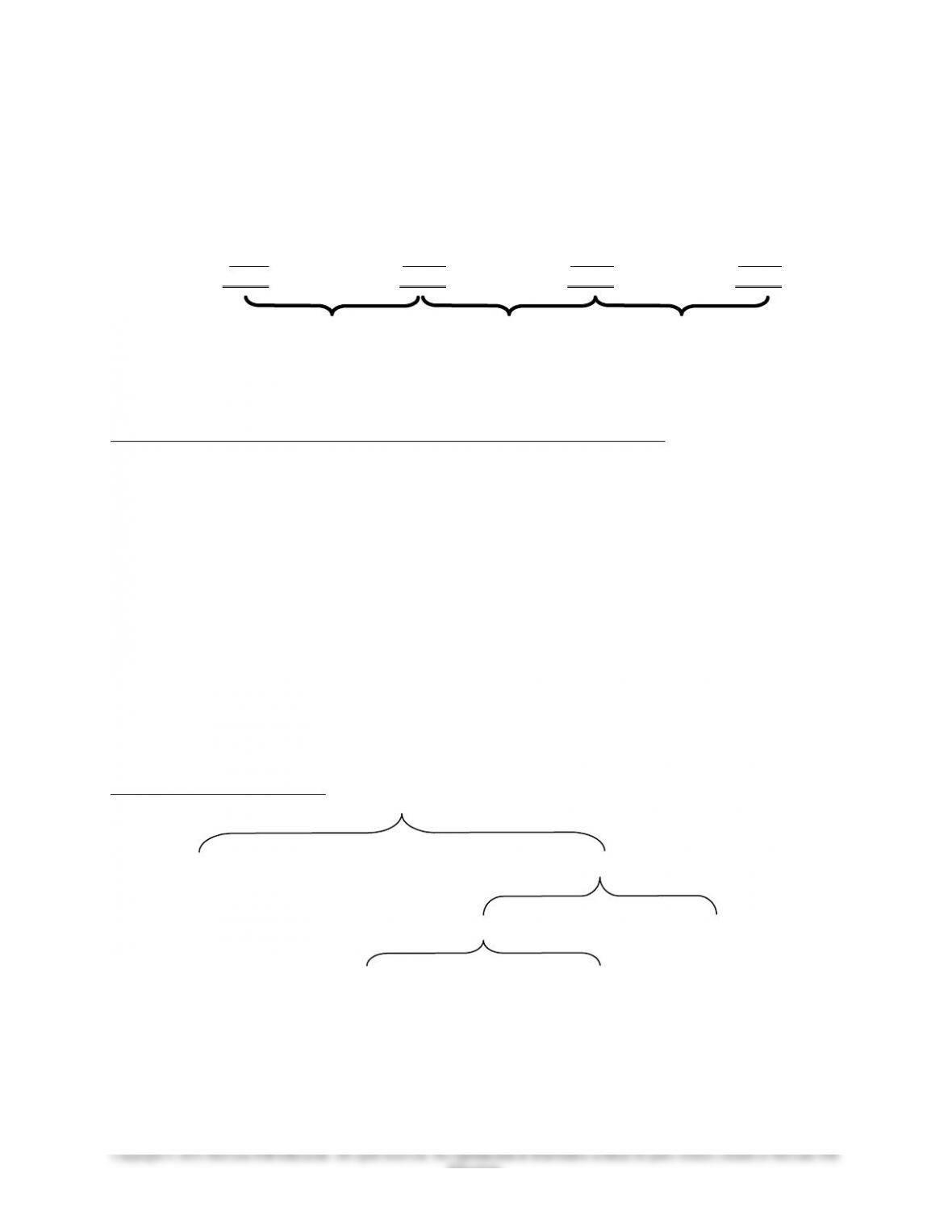

following exhibit shows the relationships of these variances.

Components of Sales Variance

Sales Variance

Selling Price Variance Sales Volume Variance

(Included in flexible budget variance)

Sales Quantity Variance Sales Mix Variance

Market Size Variance Market Share Variance

16-5

Education.

Chapter 16 – Operational Performance Measurement: Further Analysis of Productivity and Sales

Selling price variance is the difference between the dollar amount received from all the units sold and

the dollar amount the firm would have received had the firm sold these units at the master budgeted

selling price per unit.

Selling Actual Budgeted Number

Price = Selling Price – Selling Price × of Units

Variance Per Unit Per Unit Sold

This variance is included in the flexible budget variance.

Sales volume variance is the difference in contribution margins or operating incomes between the

flexible budget amount and the master (static) budget.

Sales Number Number of Budgeted (Standard)

Volume = of Units – Units in the × Contribution

Variance Sold Master Budget Margin Per Unit

Components of Sales Volume Variance

Firms with multiple products need to decompose sales volume variances into sales mix and sales quantity

variances.

Sales mix is the proportion of the unit of each product or service to the total units of products or services

of the firm. A sales mix variance measures the effect on operating income of the difference between the

actual sales mix and the budgeted sales mix of a firm during the period.

Sales Mix Actual sales Actual sales Total number Budgeted contribution

Variance = mix ratio of × mix ratio of × of units of all × margin per unit of

Of a Product the product the product products sold the product

Sales quantity variances of a product measures the effect of changes in the number of units sold from

the number of units budgeted to be sold. It is the product of three elements: (1) the difference between the

budgeted and the actual total sales quantity, (2) the budgeted sales mix, and (3) the budgeted contribution

margin per unit of the product.

Sales Total Budgeted Budgeted Sales Budgeted Contribution

Quantity = Units × Total Units × Mix Ratio of × Margin per Unit of

Variance Sold to be sold the Product the Product

Components of Sales Quantity Variance

Contribution factors to a sales quantity variance include changes in the total market size and in the firm‘s

market share.

The market size variance assesses the effect of changes in the total market sizes of the industry on the

firm’s operating income and is determined by the product of three factors: 1) the difference between the

actual and the budgeted total units of the market, 2) the budgeted market share of the firm, and 3) the

weighted average budgeted contribution margin per unit.

Market Actual Budgeted Budgeted Budgeted Weighted

Size = Total × Total × Market × Contribution

Variance Market Market Share Margin Per Unit

16-6

Chapter 16 – Operational Performance Measurement: Further Analysis of Productivity and Sales

The market share variance measures the effect of changes in the firm’s market share on the firm’s

contribution and operating income and is the product of three elements: 1) the actual total units of the

market, 2) the difference between the actual and the budgeted market shares of the firm, and 3) the

average budgeted standard contribution margin per unit.

Market Actual Budgeted Actual Budgeted Weighted

Share = Market × Market × Market × Contribution

Variance Share Share Size Margin Per Unit

Strategic Implications Of Marketing Variances

Favorable variances in both selling price and market share variances can be a signal of unexplored

market potential.

A tactical action of reducing prices to gain market shares is likely to be a right decision if

the product is at the growth stage, or

the increases in operating income from the favorable market share variance is greater than the

decrease in operating income due to unfavorable selling price variance.

A tactical action of reducing prices to gain market shares is likely to be futile in a mature market.

Unfavorable market share variance is a sign that management needs to heed.

Expansions during periods of declining market sizes can lead to overcapacities, decline in prices and

operating profits, or financial distress.

The Five Steps of Strategic Decision Making for Schmidt Machinery

Schmidt Machinery is a well-established firm that produces very high-quality all-weather furniture which

is used on patios, decks, and sunrooms. Product XV-1 is a lightweight but durable lounge chair and FB-

33 is a lightweight and durable table. Because of its very high quality and reputation for design

innovation, Schmidt’s products are sold largely by catalog, and over the firm’s web site; a few high-end

retailers also carry the brand. The firm has few direct competitors in the U.S., but there are a growing

number of competitors from Europe and Asia. Also, the falling dollar has helped Schmidt maintain its

domestic sales and to have some opportunities for foreign sales. However, a global economic recession

and a recent rise in the dollar has reduced sales worldwide. While Schmidt’s sales have increased, the

company is concerned that the recession will deepen and that sales of its products will eventually be

affected. Schmidt is facing questions such as which production lines to close and which product

advertising to increase or decrease, should that happen. Schmidt know that the XV-1 product has a larger

percentage of its sales overseas than FB-33, but is not sure which of its two products should be supported

at this difficult time.

1. Determine the Strategic Issues Surrounding the Problem

Schmidt is a differentiated manufacturer, selling a high-priced product to those who value its quality,

design, and functionality. With the growth of foreign competition and the increased price competition,

Schmidt is now looking for ways to maintain its profitability by determining an effective marketing

strategy for its two products.

2. Identify the Alternative Actions

The question facing Schmidt is whether to scale back production and marketing of one or both of its

products.

16-7

Education.