Chapter 17 – The Management and Control of Quality

17-71 (Continued-1)

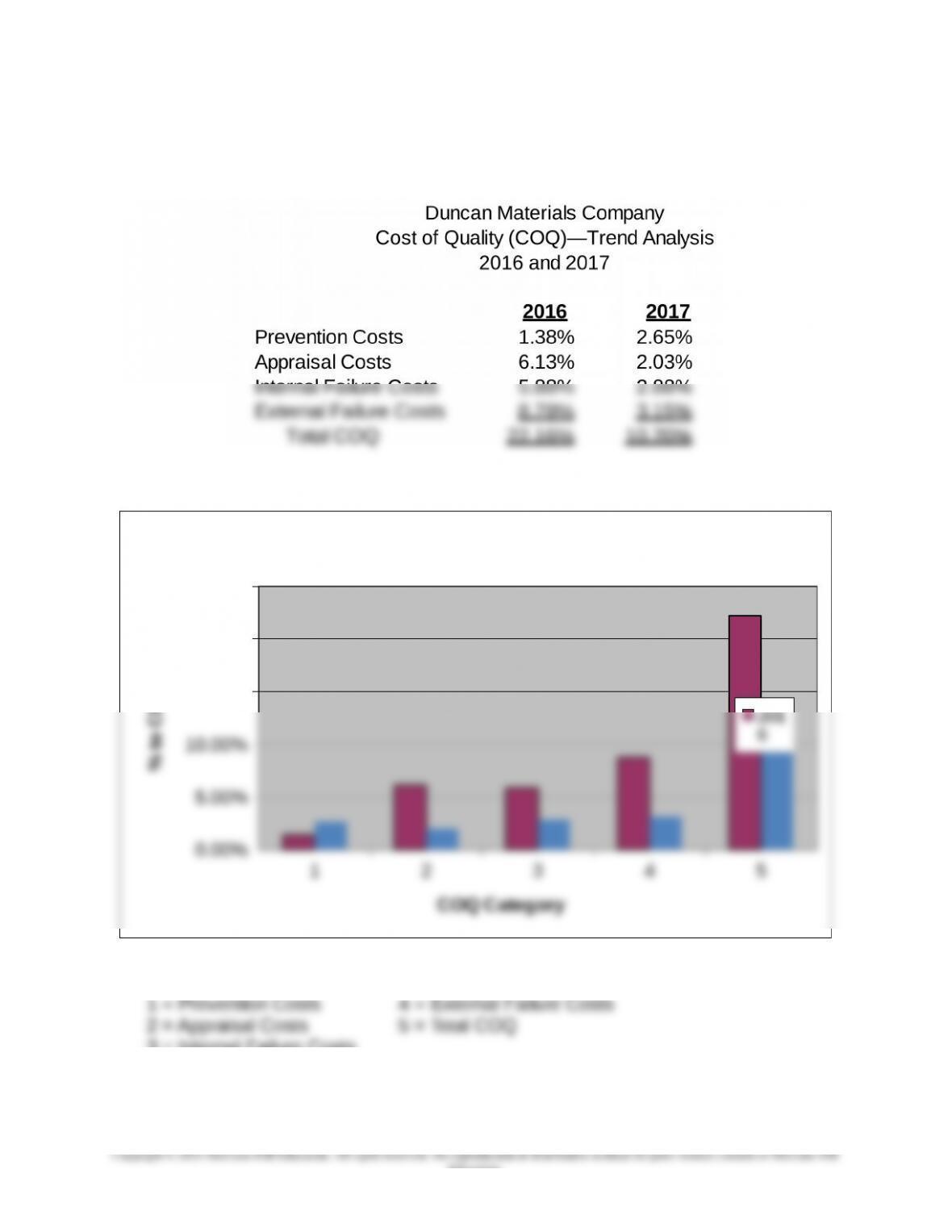

5. Data for Trend Analysis (2016 and 2017 Category Results)

6. Bar Chart: COQ Report, 2016 and 2017

12345

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

Duncan Materials: COQ Trend Analysis

201

6

COQ Category

% to CGS

COQ Categories:

17-72

Education.

Chapter 17 – The Management and Control of Quality

17-71 (Continued-2)

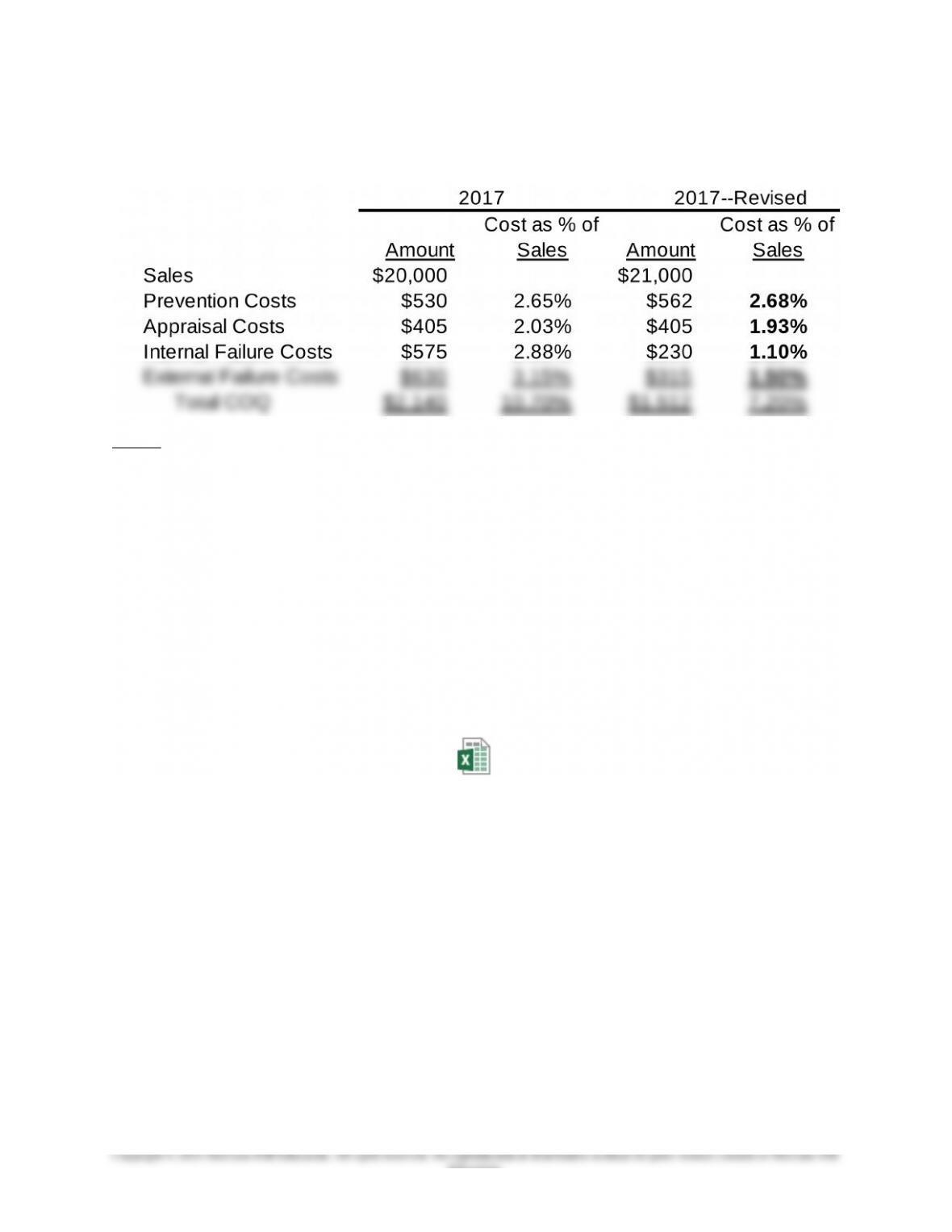

7. Sensitivity Analysis

Notes:

11.05 × $20,000 = $21,000 3(1 − 0.60) × $575 = $230

21.06 × $530 = $562 4(1 − 0.50) × $630 = $315

Note: An Excel spreadsheet solution file for this Problem is embedded in this

document. You can open the spreadsheet “object” that follows by doing the

following:

1. Right click anywhere in the worksheets below.

2. Select “worksheet object” and then select “Open.”

3. To return to the Word document, select “File” and then “Close and return to…”

while you are in the spreadsheet mode. The screen should then return you to

the Word document.

Pr. 17-71 7e.xlsx

17-73

Education.

Chapter 17 – The Management and Control of Quality

17-72 Environmental Performance—Meeting Stakeholder Expectations (60 Minutes)

1. As indicated in the cited HBR piece, the following stakeholders are likely to be

interested in corporate disclosures regarding environmental performance:

customers, employees, capital markets (i.e., investors and potential investors),

government (both federal and state), and not-for-profit organizations (such as

Climate Counts).

2. The environmental performance scorecard created by Climate Counts

(http://www.climatecounts.org/pdf/Climate_Counts_Scorecard.pdf) consists of 22

items, broken down into four areas, as follows:

Review:

(1) GHS emissions inventory completed? (5 points)

(2) Rough calculations or standard protocol/calculator? (3 points)

(3) Are Kyoto gases besides CO2 included? (2 points)

(4) Are indirect emissions accounted for (supply chain, travel, etc.)? (4 points)

(5) Is there external, qualified third-party verification of emissions data,

reductions, and reporting (where applicable)? (4 points)

(6) Is the inventory an ongoing, regular process accounting for multiple years?

(4 points)

Reduce:

(7) Has a clear goal been set? (4 points)

(8) Strength of baseline year used for the reduction goal? (3 points)

(9) Magnitude of reduction goal? (5 points)

(10) Have a measurement plan and organizational structure been established

for climate? (5 points)

(11) Is there top-level support for climate-change action? (2 points)

(12) Has the company taken steps towards achieving reduction target? (Interim

progress on reduction) (8 points)

(13) Has the company achieved emissions reductions? (10 points)

(14) Absolute or intensity-based reductions? (4 points)

(15) Has the company achieved verified reductions to date (prior to current goal

setting)? (5 points)

(16) Has the company made successful efforts to reduce greenhouse gas

(GHG) impacts associated with the use of its products/services? (4 points)

(17) Does the company work to educate its employees, trade associations,

and/or customers on how they can reduce individual GHG emissions

(through direct education programs, incentives, or philanthropic projects?

(4 points)

(18) Does the company require suppliers to take climate change action or give

preference to those that do? (2 points)

17-72 (Continued-1)

17-75

Chapter 17 – The Management and Control of Quality

Policy Stance:

(19) Does the company support public policy that could require mandatory

climate change action by business? (10 points)

(20) Does the company oppose public policy on climate change that could

require mandatory action by business, or has it made efforts to undermine

climate-change action? (-10 points)

Report:

(21) Is the company publicly reporting on emissions, risks, and actions? How is

information disclosed? Company-based (e.g., on their website or annual

report) or through a credible third-party program (e.g., CDP, GRI, etc.)? (10

points)

(22) Are emissions broken out by facility, business unit, country of operations,

or other meaningful sub-segments? (2 points)

3. As seen at http://www.climatecounts.org/scorecard_score.php?co=28 (accessed 25

November, 2011), IBM’s scorecard total for the current year is 82 (an increase of 3

points over last year’s score). It has scored highly in each of the areas, with the

possible exception of Policy Stance (4 out of 10 points). Its current score places it #2

among the 12 firms from the electronics sector. The website lists IBM as “striding,” as

follows:

Apple, on the other hand, scored last among 12 companies in the electronics industry

category (see http://www.climatecounts.org/scorecard_score.php?co=7, accessed 25

January, 2011). Apple’s current score is 60, a one-point change from last year, but

significantly above the score of three years ago (which score is mentioned in the HBR

article). Apple’s component scores are as follows: Review: 19/22 points. Apple has

completed a comprehensive inventory of the impact it has on global warming and that

the company expects to continue its review in the future. Reduce: 26/56 points.

Apple has established clear goals to reduce the company’s greenhouse gas

emissions and has initiated projects that have resulted in reductions. Policy Stance:

7/10 points. Apple has distinguished itself by strongly advocating for comprehensive

public policy that addresses climate change and would lead to market-wide reduction

in greenhouse gas emissions and the growth of renewable energy capacity. Apple

resigned from the US Chamber of Commerce over the trade group’s opposition to

comprehensive climate and energy legislation. Report: 8/12 points. Apple has made

some public information available on its efforts to address global warming.

17-76

Education.

Chapter 17 – The Management and Control of Quality

17-72 (Continued-2)

4. As indicated in the referenced HBR piece (October 2007, pp. 30, 34), companies that

have sub-par performance in the environmental area face potential risks for four

reasons:

a) Reputation risk

5. Role of the management accountant: environmental performance, as evidenced by

the corporate-performance scorecard used by Climate Counts, fundamentally

involves measurement, reporting, and analysis. Presumably, the management

accountant has a competitive advantage in these areas and, therefore, should be

able to add value to the organization by participating in the design of a

17-77

Education.

Chapter 17 – The Management and Control of Quality

17-73 Net Promoter Score (25 minutes)

1. The “net promoter score” is an example of a non-financial customer-related

performance indicator. It is calculated based on responses to the following question

posed to an organization’s customers: “How likely is it that you would recommend

our firm/company to a friend or to a colleague?” As indicated in this exercise,

customers respond to this question using a 10-point scale, from 1 = “extremely

unlikely” to 10 = “extremely likely.” In this scale, a score of 5 represents “neutral/no

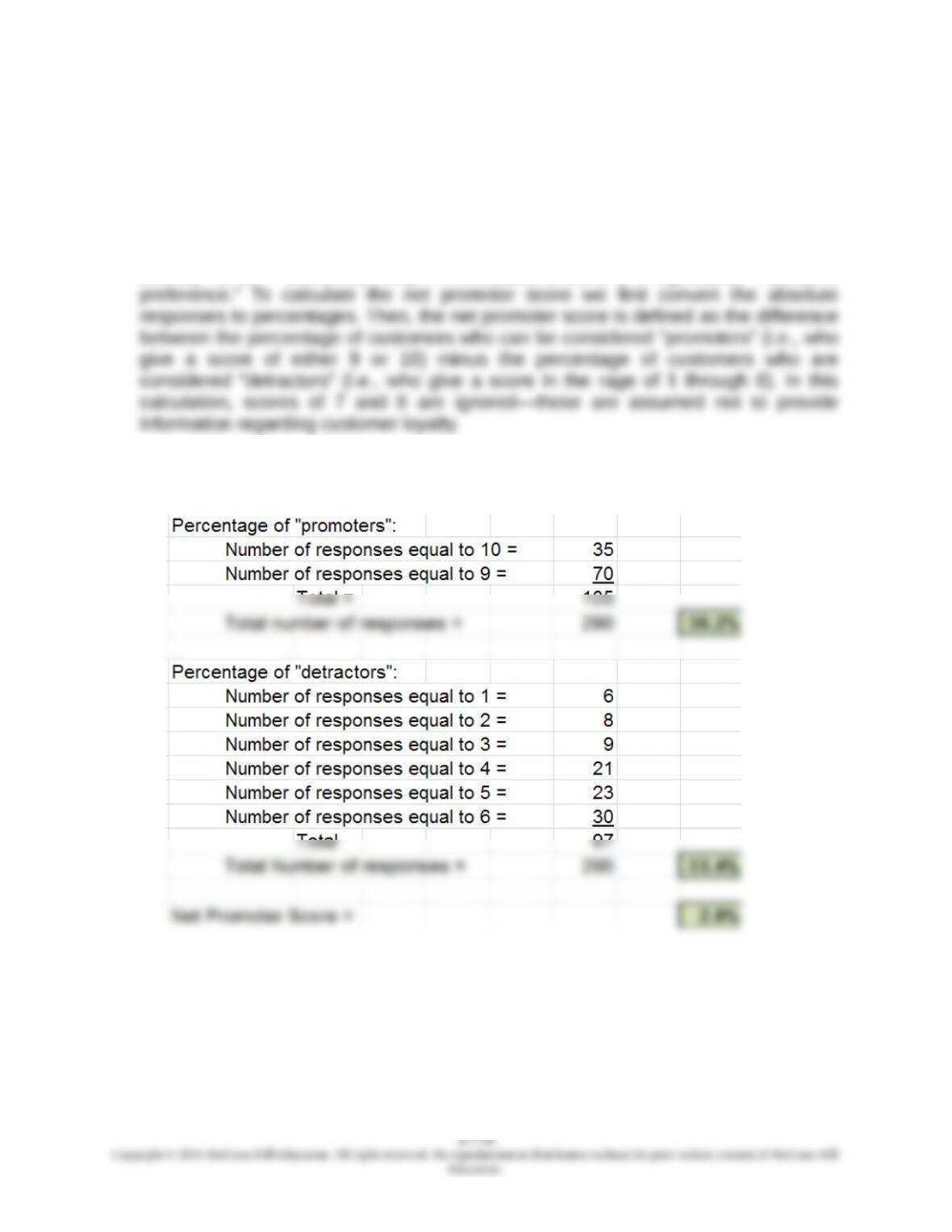

2. Net promoter score based on the assumed data/customer responses is 2.8%, as

follows:

Chapter 17 – The Management and Control of Quality

17-73 (Continued)

3. The net promoter score is recommended as a nonfinancial customer-related

performance measure based on research that indicates that a customer’s

willingness to recommend a company is positively correlated with future growth and

profitability of the company. The net promoter score can be viewed as a measure of

customer loyalty. The underlying argument is that a traditional measure of customer

loyalty, customer retention, is not a good indicator of a customer’s loyalty. This is

because customers may remain as a customer either because there are no

alternatives, because of high switching costs, or simply because of inertia, not

because of “customer loyalty.” Academic research shows that the only true loyal

customers are those classified as “promoters” of the company’s business.

Source Documents for the Net Promoter Score:

1. F. Reichheld, The Ultimate Question: Driving Good Profits and True Growth (Boston,

MA: Harvard Business Press, 2008).

2. F. Reichheld, “The One Number You Need to Grow,” Harvard Business Review

(December 2003), pp. 46-54.

Chapter 17 – The Management and Control of Quality

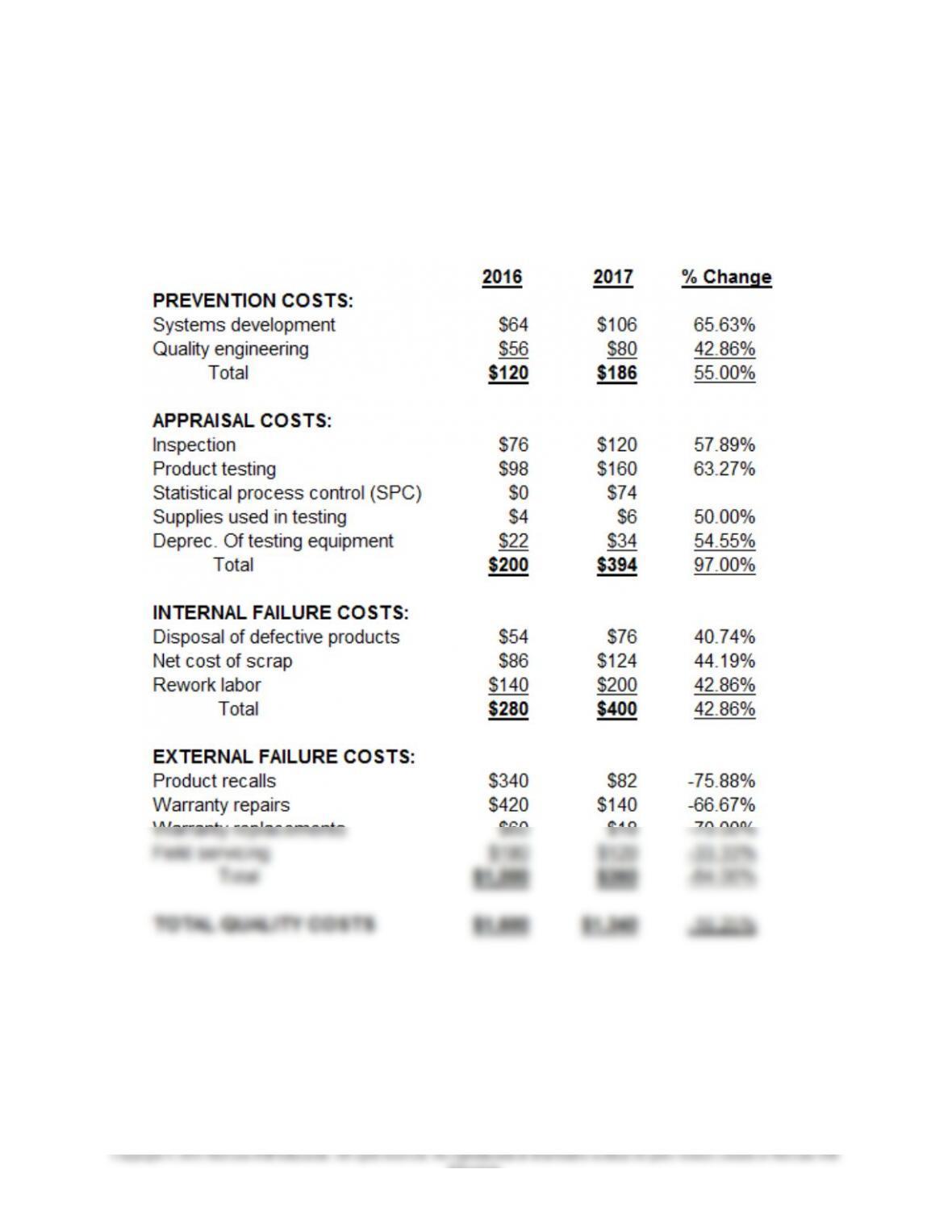

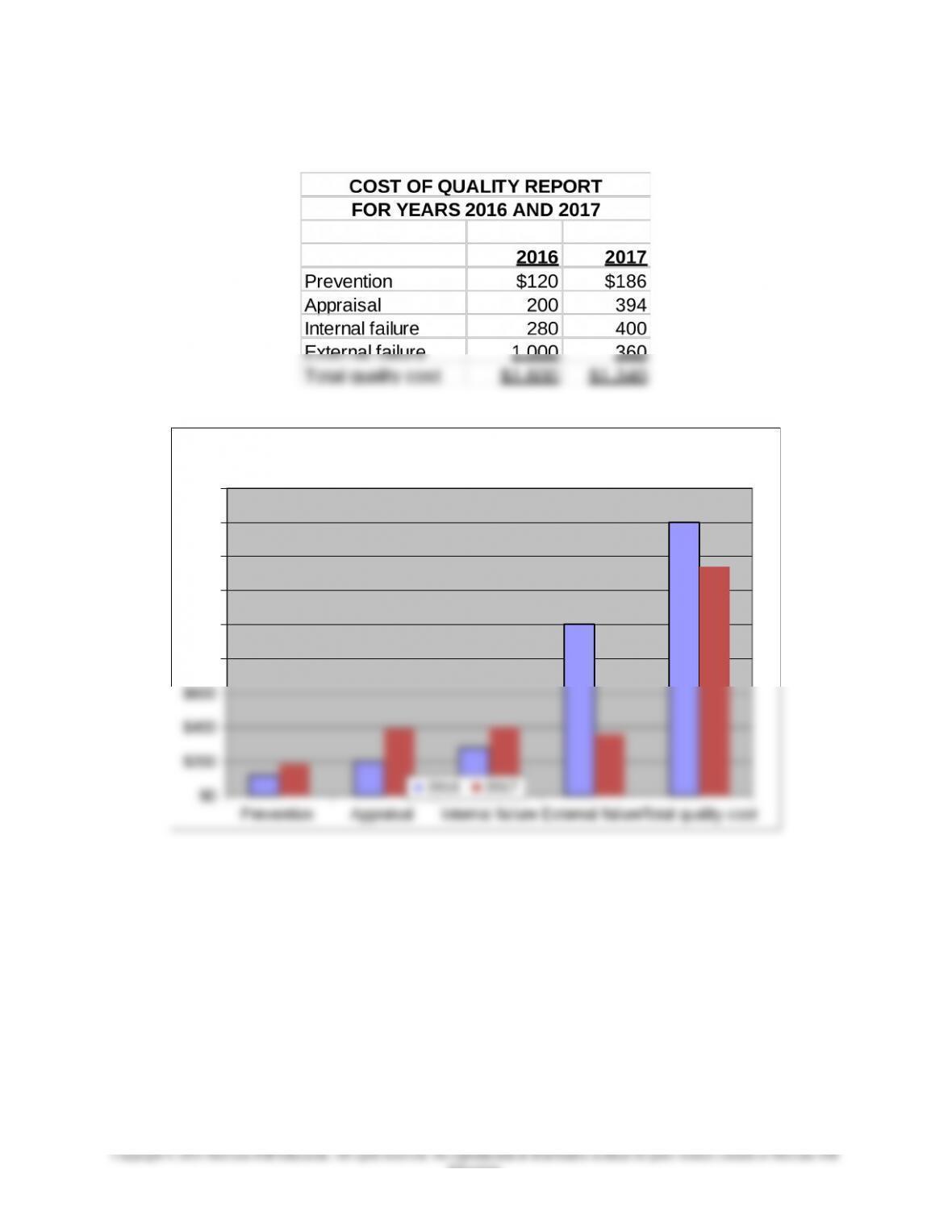

17-74 Cost-of-Quality (COQ) Reporting; Spreadsheet Application (50 Minutes)

1.

LEE ENTERPRISES

COST-OF-QUALITY (COQ) REPORT

FOR YEARS 2016 and 2017

17-80

Education.

Chapter 17 – The Management and Control of Quality

17-74 (Continued-1)

2.

Prevention Appraisal Internal failure External failure Total quality cost

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

$1,800

Cost of Quality (COQ) Summary: 2016 vs. 2017

2016 2017

17-81

Education.