Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

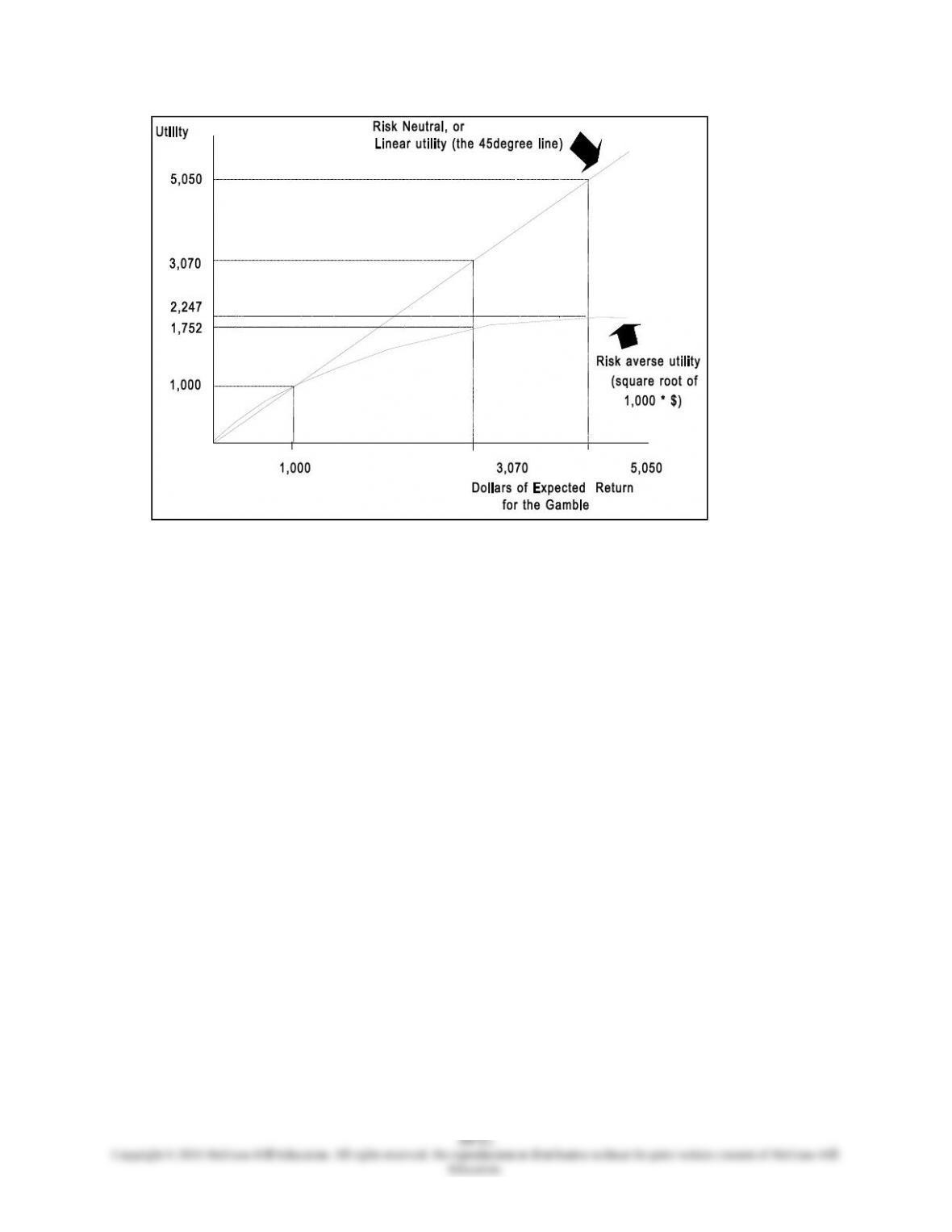

Exhibit 2: Risk Neutral and Risk Averse Utility Functions

Using mathematical transforms such as the square root or the logarithm of the dollars of expected

return provides a practical approach for representing risk-averse utility curves. When developing

incentive plans, the management accountant will consider tools such as this to provide the proper

motivation for the manager. The motivation is important to provide the incentive for both (a) a high level

of effort by the manager and (b) to provide a reward scheme which will cause the manager’s decisions to

be congruent with those of the relatively less risk-averse top management.

The Role of Information and Risk Preferences in Decision Making

The note explains the role of information and risk preferences in decision making. The first step is to

understand how the value of information is determined. To do this, we adopt the widely used decision

model based upon expected valuesdecision analysis. Decision analysis provides a systematic approach

for a decision maker to determine the best of a set of choices, when the outcome of the choices is

uncertain. The criterion for choice is maximum expected utility, where utility is typically measured in

dollars. For simplicity, we will hereafter (except where otherwise noted) refer to utility in terms of dollars,

and use the criterion, “expected value.” For example, if for a given choice the decision maker faced two

outcomes, one with a value of $10 and the other with a value of $50, and the outcomes were equally

likely, then the expected value of the choice would be:

Expected Value = .5 x $10 + .5 x $50 = $30

Using this expected value measure, the decision maker would rank order the choices available and

choose the option with the greatest expected value. The role of information in this context is to improve

the expected values available to the decision maker by updating the odds, that is, updating the

probabilities for the different outcomes.

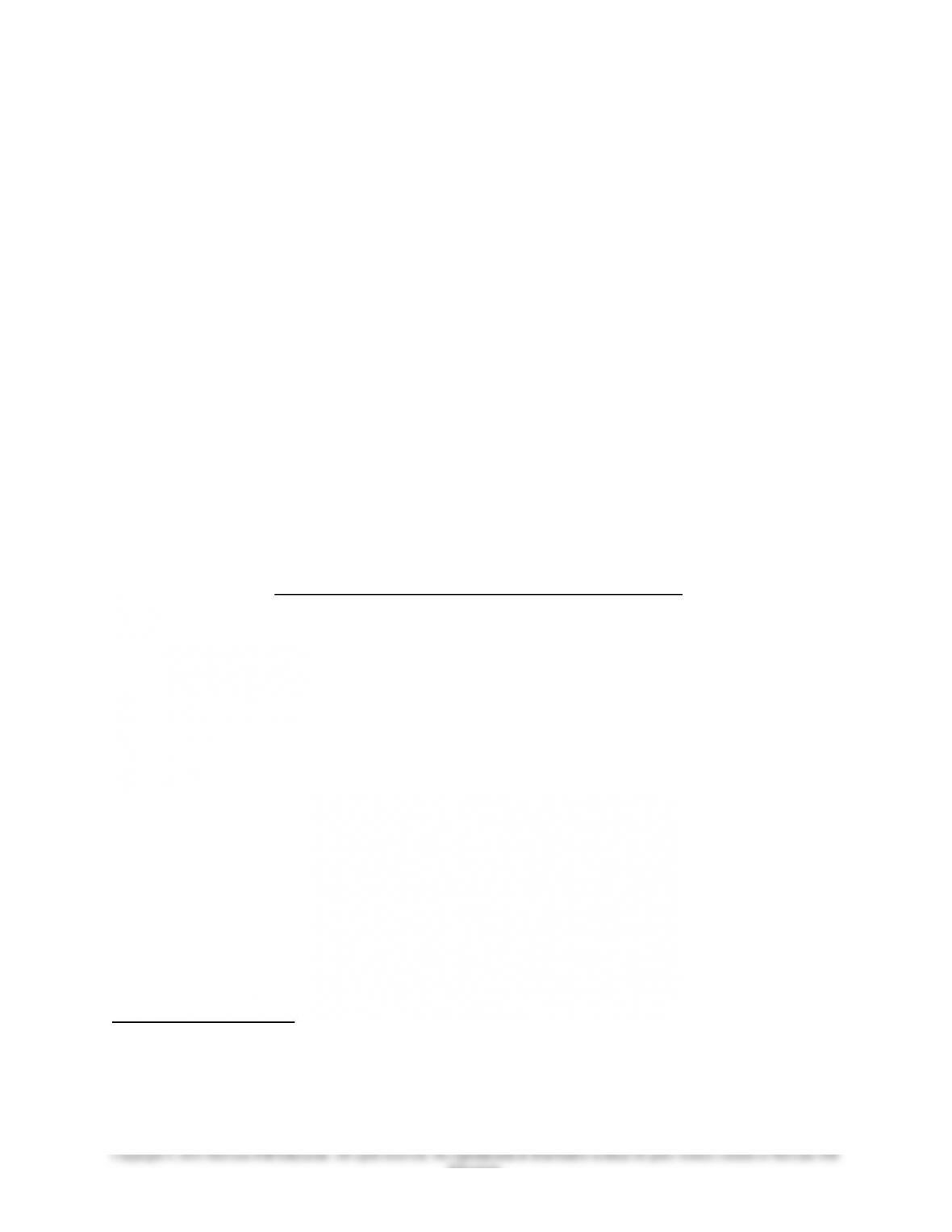

To illustrate, we develop the decision analysis for a manager who oversees the subcontractors who

provide services to a large construction company. The subcontractors perform certain services and then

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

bill the construction company. The manager must decide which, if any, of the bills submitted for payment

to the company are in error (usually including over-charges), and should be corrected. The uncertainty lies

in the fact that the manager does not know, prior to an extensive investigation of each bill, whether it is in

error or not. The manager can perform an investigation of the bill, which the manager estimates on the

average would cost $100, and when needed, a correction of the bill, which on the average would cost an

additional $100. Alternatively, the manager could let the bill pass and hope for the best. If the bill is in

error, the company will (unknowingly) pay for the overcharges, which will on the average be about

$1,000 per bill. We will call this the “cost of incorrect acceptance.” From experience, the manager knows

that the odds of an incorrect bill are about one in ten. However, without conducting an investigation, the

manager has no way of knowing which bill is in error, so that the best strategy for investigation will either

be to investigate all the bills, none of the bills, or perhaps some randomly selected sample. This decision

problem can be formalized, as is illustrated in Exhibit 1.

The manager wants to choose the option that will be least costly to the firm, and in this case, the

lowest expected cost is to accept each bill without investigation. This would produce an average cost of

$100 (one-tenth of the bills are in error by $1,000). The alternative “investigate and correct” strategy

would be more costly on the average, or $110 per bill (a total investigate and correct cost of $100 + $100

= $200 which is incurred one-tenth of the time, and the cost to investigate only, $100, the rest of the time;

for a total expected cost of .1 x $200 + .9 x $100 = $110).

After some experience with this decision setting, the manager can develop a simplified decision rule,

the “threshold ratio,” which is calculated as follows.1 The decision rule is to investigate a bill when the

odds that it is not-OK is greater than the threshold ratio. For this data, the threshold ratio is one-ninth,

which is determined from the ratio of the three different costs as follows:

Cost of Investigation

Threshold Ratio =

Cost of Incorrect Acceptance, less Cost of Correction

= $100/ ($1,000 – $100)

= 1/9

1 The decision rule is developed as follows. Let P = the probability of the not-OK condition, a = cost of

investigation, b = cost of correction, and c = cost of incorrect acceptance. Then, the manager will choose to

investigate if the expected cost of investigating is less than the expected cost of not investigating:

(a + b) x P + b x (1 – P) < c x P

or: p > b/(c – a)

18-12

Education.

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

Exhibit 1: The Value of Information in a Simple Decision Problem

The manager compares the threshold ratio to the odds for an incorrect bill to determine whether to

begin an investigation. Since the threshold ratio is less than the odds of the not-OK bill (1/10 is less than

1/9), the best decision is not to investigate.

The Role Of Information

Up to this point we have assumed that the manager knows only the proportion of bills in error, but

does not have information to identify those specific bills that are in error. This information would be

useful to the manager, as a means to reduce overall investigation, correction, and incorrect acceptance

costs.

Suppose the manager has access to a report in which accounting information is used to prepare a

“risk score,” which would perfectly identify the bills that are in error, so that the manager could avoid the

mistakes of incorrect acceptance and incorrect rejection for any given invoice. The risk score could be

developed from information about the biller’s accounting system (cash or accrual-based, the quality of the

internal accounting control system, whether or not there is an internal audit function, how product costs

are calculated, etc.). For example, the risk score might be the sum of the relevant risk factors noted for the

invoice, where the number of possible risk factors is 35, and the average number of risk factors noted for

the typical invoice is usually between 12 and 24. While it is unlikely such a score would perfectly signal

the true error condition, as we assume here, the assumption is useful for this simplified illustration.

18-13

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

With perfect information, the manager would be able to always choose the lowest cost outcome

(when there is an error, investigate and correct the bill; when no error, accept the bill). With perfect

information, the manager’s expected cost is simply the sum of the expected costs for each possible

outcome, given the best choice for each error condition: .1 x $200 +.9 x $0 = $20. With perfect

information, the manager will not conduct an investigation if the information reports there is no error in

the bill, and similarly, there is no possibility the manager will incorrectly accept a bill that is in error.

The value of the information, then, is the differential, $100-20 = $80, the difference between the expected

cost to the manager with and without the perfect information. This is called the expected value of perfect

information. It is called the expected value of perfect information because, while the manager can prevent

mistakes in identifying which bills have errors, the manager cannot prevent the occurrence of errors,

which has a probability of 10% for each invoice.

The expected value of perfect information is a useful concept for measuring the value of information.

It is particularly appealing in accounting, because it shows directly the maximum potential benefit to a

decision maker from receiving information that will reduce some of the uncertainty in the decision

setting.

Obtaining Probabilities from the Normal Probability Curve

Implementing the above decision rule will require the manager to estimate the costs of investigation,

correction, and incorrect acceptance, and to estimate the probabilities that a given invoice will be in one

of the two conditionsOK or not-OK. This section explains how the normal probability curve can be

used to facilitate development of the probability estimates.

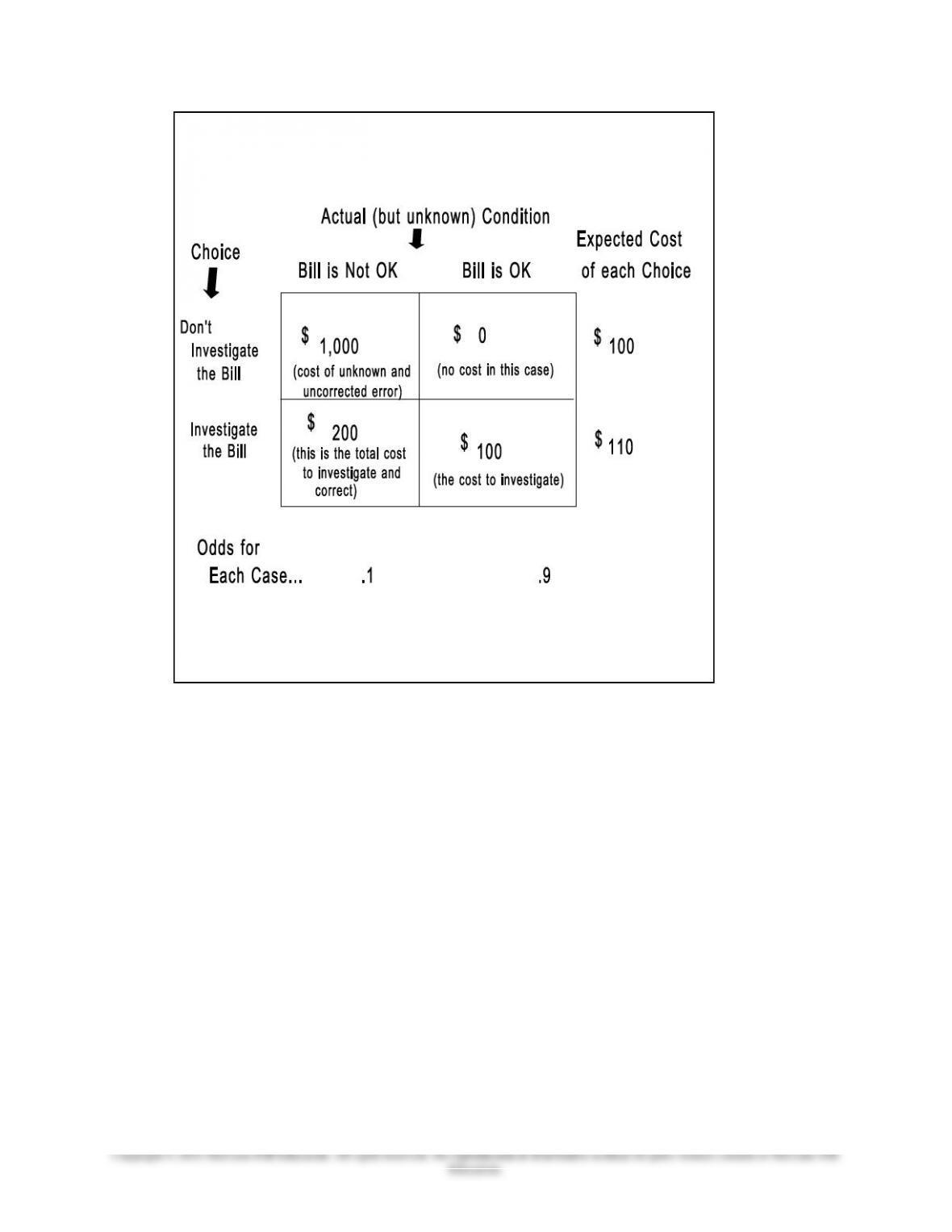

The first step in using the normal curve would be for the manager to maintain a “history” of the risk

scores of selected invoices for a given period, together with the outcome of whether the invoice was in

error or not. In this way the manager develops two frequency distributions, one for each error condition

that shows the frequency of all the different possible risk scores that are observed under that error

condition. Assuming that the method of calculating the risk score is useful and effective, invoices with

higher risk scores will more likely be in error than other invoices, and given a sufficiently large number of

invoices, the pattern will likely follow that of the normal curve for each error condition, as illustrated in

Exhibit 2.

Now, given the historical data in these two frequency distributions, it is possible for the manager to

develop a revised, more accurate probability estimate based upon the risk score of each invoice. To

illustrate, consider Exhibit 2, wherein the no-error distribution is assumed to be approximately normally

distributed with a mean risk score of 14 and a standard deviation of 4; similarly, the in-error distribution

has a mean of 22 and a standard deviation also of 4. Suppose that the manager observes that a given

invoice has a risk score of 16. Because the risk score is relatively low, the probability estimate that the

invoice is in error also should be low. Rather than to determine this estimate judgmentally, the manager

can use the information in the two historical distributions to obtain a quantitative estimate.

18-14

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

Exhibit 2: Normal probability distribution of Risk Scores

The first step is to obtain the probability for the point 16, by converting the value for 16 to a

standard normal value, which can then be found in tables for the standard normal curve. The conversion

of any point to a standard normal value is done by subtracting the mean of the normal distribution from

the value of the point, and then dividing by the standard deviation of the curve, as follows:

Standard normal equivalent for point 16 = (mean-16)/Standard deviation

To illustrate, since the mean of the in-error distribution of risk scores is 22, and the standard

deviation is 4, the standard normal equivalent for the point 16 would be, from the above formula:

(16-22)/4 = -1.5

Since the normal curve is symmetric, we can ignore the negative sign and go directly to a table of

normal probabilities, Exhibit 3, to find that the probability for the in-error condition at the point 16 is .

1295.

Similarly, the probability of the point 16 for the distribution of no-error risk scores can be found

from the mean (14) and standard deviation (2) of the no-error distribution, where the standard normal

value is (16-14)/4 = .5 and, from Exhibit 3, the probability for the no-error distribution at the point 16 is .

3521.

18-15

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

Risk Score Standard Normal Probability

.5 .3521

1.0 .2420

1.5 .1295

2.0 .0539

2.5 .0175

3.0 .0044

Exhibit 3: Values of the Standard Normal Probability Function

Now, the manager’s best estimate that the invoice with the 16 risk score is in error is given by the

ratio of the in-error to total probabilities, as follows:

.1295/(.1295 + .3521) = .2688

and the probability that the invoice is not in error is

1.0 – .2688 = .7312

Thus, the manager knows that based upon the favorable risk score, this invoice has a relatively

small chance of being in error. Without the risk score information, the manager’s best guess would be that

this invoice would have the same probability of being in error as for any other invoice, or 10%, since one

in ten invoices historically turn out to be in error. The risk score, and the use of the normal probability

curves, can significantly improve the manager’s estimate of the probabilities. For practice now, determine

the in-error probability for an invoice with a risk score of 20.2.2

In summary, what the manager has accomplished is to use the historical frequency data for risk

scores under each error condition to form a normal probability curve for each error condition, which then

can be used to better estimate the specific probability that a given invoice will be of either condition,

based upon the invoice’s risk score.3

The normal curve can be used in a variety of contexts such as this, where there is prior data or

experience available to develop a probability distribution from which the probability of any specific value

can be determined, as in the above illustration.

The Effect Of Risk Preferences On Decision-Making

The manager’s decision rule as presented above is a useful model for illustrating the role of risk

preferences in decision-making.

22 The standard normal value for the in-error condition is (20-22)/4 = .5, with a related probability of .3521. The

standard normal value for the no-error condition is (20-14)/4 = 1.5, with a related probability of .1295. The

probability of the invoice being in error is thus .3521/(.3521 +.1295) = .7312.

33 It is also possible for the manager to incorporate prior probability beliefs in this analysis, and to perform a

Bayesian analysis in a similar fashion. The Bayesian approach for this particular context is best illustrated by

Thomas R. Dyckman, “The Investigation of Cost Variances,” Journal of Accounting Research, Fall 1969, pp 215-

244.

18-16

Education.

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

The following illustration shows how risk preferences can produce an undesirable decision.4

Suppose the manager has the option to invest $25,000 in either a new manufacturing technology which

could improve the efficiency of the plant considerably, or alternatively, to spend the $25,000 in the

redesign of one of the product lines. The difference is that there is a substantial risk that the new

technology will not work, and relatively little risk that the product re-design will produce modest returns.

Suppose there is a 30% chance that the new manufacturing technology will produce a $100,000 savings in

plant costs, and a 70% chance of only a $20,000 savings. Also, the product re-design will produce with

fifty-fifty odds either a savings of $50,000 or a savings of $30,000. The manager will earn 15% of the net

savings generated from either investment, since managers’ compensation is based in part on a bonus of

15% applied to earnings before tax.

Suppose that top management of the entity has a risk-neutral approach to the decision problem

(i.e, linear expected utility in dollars), then top management would prefer the new manufacturing

technology over the product re-design, because of the higher expected value ($19,000 and $15,000

respectively). This is illustrated as follows:

Top Management’s Decision Analysis:

Expected Value of Investing in New Manufacturing Technology

(.3 x $100,000 + .7 x $20,000 = $44,000) – $25,000 = $19,000

Expected Value of Investing in Product Re-design

(.5 x $50,000 + .5 x $30,000 = $40,000) – $25,000 = $15,000

While the choice is clear to top management, the manager who is risk-averse has a different view.

First, we must describe the manager’s utility function. One way to describe a risk-averse utility function is

to use the square-root transform.5 Then, suppose the manager’s utility function can be described by the

square root of the amount, “dollars received times 100″ (the multiplication times 100 is a simple scale

factor to produce meaningful amounts). Then, the manager’s decision analysis can be illustrated as

follows:

The Manager’s Decision Analysis

Expected Utility of Investing in New Manufacturing Technology

Expected Utility of Investing in Product Re-design

It is clear that the manager has higher utility for the product re-design. The square root utility

function deflates the potentially high return of the new manufacturing technology investment, and the re-

44 This example is found in the article by Chee W. Chow and William S. Waller, “Management Accounting and

Organizational Control,” Management Accounting (April 1982), pp36-41.

55 The square root function reduces the outcome in dollars by an increasing proportion of the size of the amount,

and thus is a good proxy for risk aversion. That is, under uncertainty, the decision maker places a lower value on the

larger amounts in preference for smaller, more certain amounts.

18-17

Education.

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

design project has higher expected utility, if not higher expected monetary value. From top

management’s perspective, the 15% bonus incentive has dysfunctional consequences. Management should

therefore consider amending the pay plan to reduce the effect of the bonus scheme on managers’ decision-

making.

Assignments For Supplementary Material

Question 1: Decision Making (CMA adapted)

Video Recreation Inc. (VRI) is a supplier of video games and video equipment such as large-

screen televisions and video cassette recorders. The company has recently concluded a major contract

with Sunview Hotels to supply games for the hotel video lounges. Under this contract, a total of 4,000

games will be delivered to Sunview Hotels throughout the western United States, and all of the games

will have a warranty period of one year for both parts and labor. The number of service calls required to

repair these games during the first year after installation is estimated as follows.

Number of

Service Calls Probability

400 .1

700 .3

900 .4

1,200 .2

VRI’s Customer Service Department has developed three alternatives for providing the warranty

service to Sunview; these three plans are presented below and in the next column.

Plan 1

VRI would contract with local firms to perform the repair services. It is estimated that six such

vendors would be needed to cover the appropriate areas and that each of these vendors would charge an

annual fee of $15,000 to have personnel available and to stock the appropriate parts. In additional to the

annual fee, VRI would be billed $250 for each service call and would be billed for parts used at cost plus

a 10 percent surcharge.

Plan 2

VRI wold allow the management of each hotel to arrange for repair service when needed and then

would reimburse the hotel for the expenses incurred. It is estimated that 60 percent of the service calls

would be for hotels located in urban areas where the charge for a service call would average $450. At the

remaining hotels, the charge would be $350. In addition to these service charges, parts would be billed at

cost.

Plan 3

VRI would hire its own personnel to perform repair services and to do preventive maintenance.

Nine employees, located in the appropriate geographical areas, would be required to fulfill these

responsibilities, and their average salary would be $24,000 annually. The fringe benefit expense for these

employees would amount to 35 percent of their wages. Each employee would be scheduled to make an

average of 200 preventive maintenance calls during the year; each of these calls would require $15 worth

of parts. Because of this preventive maintenance, it is estimated that the expected number of hotel calls

for repair service would decline 30 percent and the cost of parts required for each repair service call

would be reduced by 20 percent.

18-18

Education.

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

VRI’s Accounting Department has reviewed the historical data on repair costs for equipment installations

similar to those proposed for Sunview Hotels and found that the cost of parts required for each repair

occurred in the following proportions.

Parts Cost

Per Repair Proportion

$30 15%

40 15

60 45

90 25

Required:

Video Recreation Inc. wishes to select the least cost alternative to fulfill its warranty obligations

to Sunview Hotels. Recommend which of the three plans presented above should be adopted by VRI.

Support your recommendation with the appropriate calculations and analysis.

Answer:

Video Recreation Inc. should adopt Plan 3 as the least cost alternative. Calculations for all three

plans are as follows.

Expected number of service calls

Number of Expected

service calls x Probability = calls

400 .1 40

700 .3 21

900 .4 360

1,200 .2 240

1.0 850

Expected value of parts costs

Parts cost Expected

per repair x Proportion = calls

$30 .15 $ 4.50

40 .15 6.00

60 .45 27.00

90 .25 22.50

1.00 $60.00

Plan 1

Vendor fees (6 x $15,000) $ 90,000

Service calls (850 x $250) 212,500

Parts ($60 x 850 x 1.1) 56,100

Estimated total cost $358,600

18-19

Education.

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

Plan 2

Urban service calls (850 x .6 x $450) $229,500

Rural service calls (850 x .4 x $350) 119,000

Parts ($60 x 850) 51,000

Estimated total cost $399,500

Plan 3

Employee salaries (9 x $24,000) $216,000

Fringe benefits (.35 x $216,000) 75,600

Preventive maintenance parts

(200 x 9 x $15) 27,000

Repair parts (850 x .7)($60 x .8) 28,560

Estimated total cost $347,160

Question 2. Expected values, utility curves.

A vacationer is in Las Vegas and wants to gamble on a new game at the casino. The vacationer

believes that there is a 20% chance of winning $1,000 and an 80% chance of losing $50 ( the price to play

the game).

Required

What is the expected value from playing this game? How much would the vacationer be willing

to pay for a chance to play the game if he or she were risk neutral? Risk averse? (assume a square root

utility function with a scale factor of 100)

Answer:

Expected value of the gamble:

.20 x $1000 – .8 x $(50)

18-20

Education.